Think of a payment reversal as the financial equivalent of hitting "undo" on a customer's transaction. It's not a simple refund you issue; this is a process kicked off by the customer's bank for a specific reason, like a potential fraud alert or a serious problem with a product they received.

In short, it’s when the money from a sale—whether it's still pending or has already settled—gets pulled back and returned to the customer's account.

Understanding the Basics of Payment Reversals

Imagine you just sent a critical email and immediately spotted a typo. That frantic "recall message" function is a pretty good parallel for a payment reversal. It’s a mechanism designed to pull a transaction back after it has already been set in motion.

While this system is built to protect consumers, it can quickly turn into a massive headache for businesses. We're talking lost revenue, surprise fees, and a real disruption to your day-to-day operations.

Getting a handle on the process is your first line of defense. When a reversal happens, it’s not just a back-and-forth between you and your customer. It’s more like a multi-step dance involving several key players, each with a very specific role to play.

The Main Players in the Process

Let's break down who’s involved when a payment gets reversed. The whole system hinges on a chain of communication between these parties.

Here’s a quick overview of the key players and what they do in this process.

Knowing who’s who helps you understand where the request is coming from and what steps you need to take next.

At its core, a payment reversal is a protection mechanism for the cardholder. However, for merchants, it can feel like a sudden and confusing financial penalty, especially when it comes in the form of a chargeback.

It's also super important to understand that "payment reversal" is a broad term. It can cover different actions like chargebacks, refunds, and something called an authorization reversal. Each one has its own set of rules and impacts your business differently.

To really get a grip on the nuances, you can dive deeper into the differences between a chargeback vs refund vs reversal in our detailed guide.

The process might seem complicated at first, but understanding these fundamentals is key. When you know who does what, you’re in a much better position to figure out why a reversal happened and how you can respond effectively to protect your business.

The Different Types of Payment Reversals

When you hear “payment reversal,” it’s easy to picture one giant, messy problem. But in reality, not all reversals are created equal. Think of it like handling returns at a retail store: some are simple exchanges, while others involve a mountain of paperwork and a whole lot of headaches.

Getting a handle on the specific type of reversal you’re dealing with is the first step to managing it. Each one follows a different path, carries different risks, and requires a completely different response from you. Let’s break down the three main players in the reversal game.

Authorization Reversals The Quick Fix

An authorization reversal is the simplest and least painful of the bunch. This happens when a transaction is stopped before the funds actually settle and move from the customer’s account to yours. In short, it’s like canceling a temporary hold on the money.

Imagine a customer books a hotel room online. Their bank puts a hold on the funds to make sure they’re available. If that customer cancels their booking just a few hours later—long before their card is officially charged—the hotel can issue an authorization reversal. The hold is simply released, and the pending charge disappears from the customer's statement as if it never happened.

For merchants, this is the best-case scenario. There are usually no fees involved, and it’s over and done with in a couple of business days. It's a clean break with almost no financial sting.

Refunds The Standard Return

This is the one you know best. A refund is a reversal you, the merchant, initiate after a transaction has already been completed and the money has settled in your account. It's your standard operating procedure for customer returns, service hiccups, or billing mistakes.

Let's say a customer buys a shirt from your online store. The payment clears, the money is in your account, and you ship the product. A week later, they send it back because it’s the wrong size. You then process a refund, which pushes the money back to their original payment method.

While refunds obviously mean you’re giving back revenue, they’re a normal and expected part of doing business. In fact, handling them well is a sign of great customer service. You’re in the driver’s seat, and even though you might lose out on some non-refundable transaction fees, you avoid the heavy penalties that come with more aggressive reversal types.

Chargebacks The Customer-Led Dispute

This is where things get serious. Chargebacks are the most complex, costly, and frustrating type of payment reversal. Unlike the other two, a chargeback isn’t started by you; it’s initiated by the customer through their bank. This usually happens when a cardholder sees a charge on their statement they don't agree with, for any number of reasons.

The whole process is formal and immediately puts you on the defensive.

A chargeback isn't a simple request; it's a forced reversal of funds kicked off by the cardholder’s bank. It completely bypasses you and triggers a formal dispute process through the card network.

Common triggers for a chargeback include:

- True Fraud: The classic case of a criminal using a stolen credit card. The legitimate cardholder sees the charge and rightfully disputes it.

- Merchant Error: Maybe you accidentally double-charged the customer, or a technical glitch caused a problem during checkout.

- Customer Dissatisfaction: The customer claims the product wasn’t as described, showed up damaged, or never arrived at all.

- Friendly Fraud: This is the real kicker. It’s when a legitimate customer disputes a perfectly valid charge. They might have forgotten about the purchase, not recognized your business name, or are deliberately trying to get something for free. Some reports even show friendly fraud is to blame for up to 75% of all chargeback cases.

Chargebacks bring a storm of consequences. You lose the revenue, the product you shipped, and get slapped with steep chargeback fees that can run from $20 to $100 per incident. Too many can even jeopardize your relationship with your payment processor. Sometimes, this process starts with a retrieval request, where the bank just asks for more info on a transaction. You can learn more about the difference between retrieval requests vs chargebacks in our complete guide.

How the Payment Reversal Process Actually Works

When a customer disputes a charge, the whole process can feel like a confusing, behind-the-scenes mystery. It's not a simple back-and-forth between you and your customer; it's more like a multi-stage relay race involving several banks and card networks, each with its own strict rules and deadlines. Let's pull back the curtain and walk through what really happens during a typical chargeback.

The entire thing kicks off the moment a customer contacts their bank—the issuing bank—to question a transaction. That single action is the spark that ignites the whole reversal process.

Step 1: The Customer Kicks Things Off

It all starts with the cardholder. Maybe they don't recognize a charge on their statement, claim a product never showed up, or feel the item wasn't what they were promised. So, they call their bank, log into their banking app, or even send a letter to formally contest the transaction.

The customer's bank takes a look at the claim. If it seems legitimate based on the reason given, the bank slaps a specific reason code on the dispute and pushes it forward. This code is a huge deal because it dictates exactly what kind of evidence you'll need to provide if you decide to fight back.

Step 2: The Banks Get Involved

Once the issuing bank accepts the dispute, it temporarily credits the customer's account for the amount in question. Then, it sends the dispute through the card network (like Visa or Mastercard) over to your bank, which is known as the acquiring bank.

This is where you, the merchant, are officially pulled into the ring. Your acquiring bank gets the chargeback notification and immediately yanks the disputed amount, plus a non-refundable chargeback fee, right out of your merchant account. And yes, this happens before you've even had a chance to tell your side of the story.

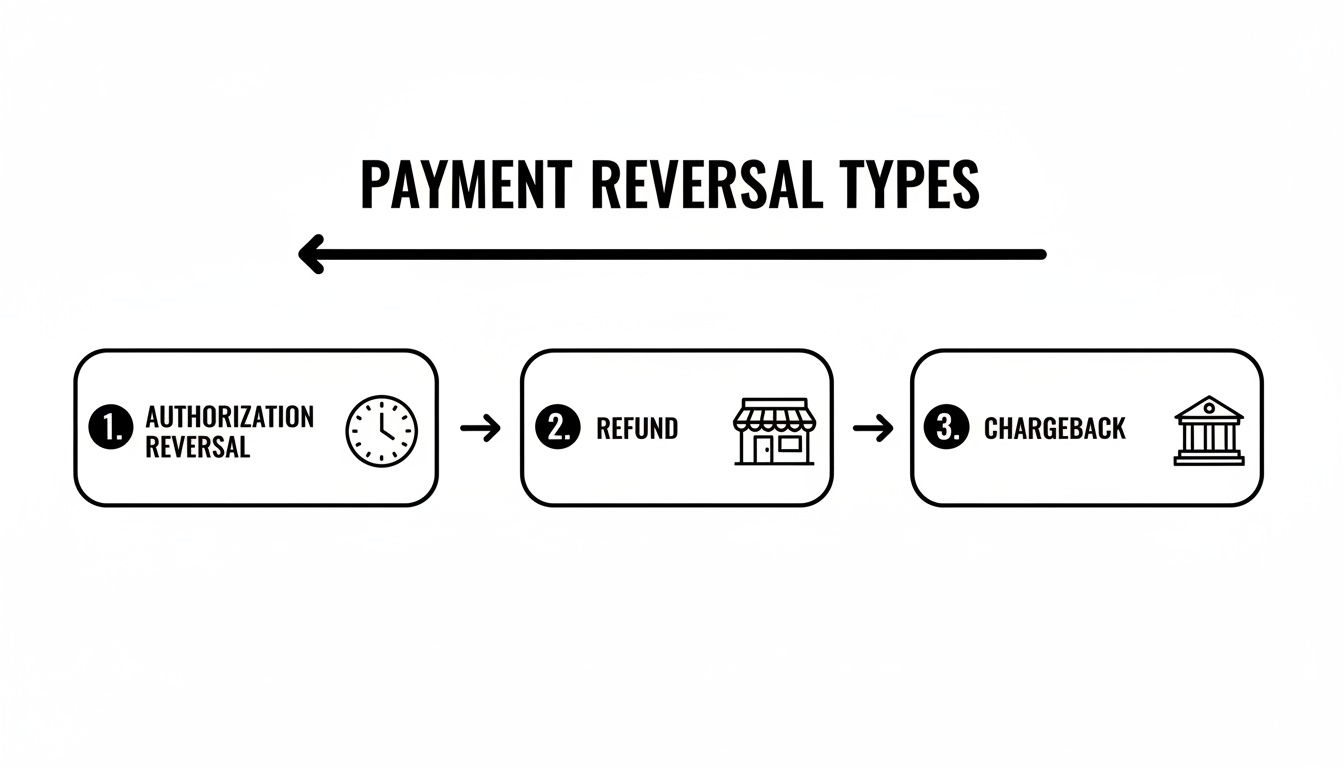

This infographic shows where the different types of payment reversals—authorization reversals, refunds, and chargebacks—originate from.

As you can see, while some reversals are initiated by you (like a refund), the most complex and costly ones (chargebacks) are kicked off by the customer's bank, setting this formal process in motion.

Step 3: The Merchant Responds

Now, your acquiring bank lets you know about the chargeback. You've reached a fork in the road: do you accept the chargeback and eat the loss, or do you fight it?

If you decide to fight, you’ll need to assemble compelling evidence to prove the transaction was totally legitimate. This fight-back process is officially called representment. The evidence you'll need hinges on that reason code, but it often includes things like:

- Proof of Delivery: Think shipping confirmations with tracking numbers and, ideally, a delivery signature.

- Customer Communication: Any emails or chat logs that show you resolved the customer’s issue or that they were happy with their purchase.

- Terms of Service: A copy of the policies the customer agreed to when they checked out.

- Order Details: Invoices and receipts that perfectly match the disputed charge.

You're on the clock here. You usually have a tight window, typically just 20-45 days, to get this evidence package submitted to your bank. A solid understanding of the card dispute process is non-negotiable at this stage to make sure you hit every deadline with the right documents.

Step 4: The Final Judgment

After you submit your evidence, your acquiring bank sends it back through the card network to the customer's issuing bank. From there, the issuing bank plays judge and jury, making the final call. They'll weigh your evidence against the customer's original complaint.

If your evidence is rock-solid and proves the dispute is invalid, the chargeback gets reversed. The money is returned to your account (though you're usually still out the chargeback fee). Victory.

But if they decide your evidence isn't strong enough, the chargeback stands. The temporary credit the customer received becomes permanent. At this point, you’ve officially lost the revenue, the product, and the chargeback fee.

While the process was created to protect consumers, its complexity and cost make it crystal clear why every merchant needs to understand each step. Knowing the roadmap helps you prepare, respond effectively, and protect your bottom line when a dispute inevitably lands on your desk.

Common Triggers That Cause Payment Reversals

To stop payment reversals, you first have to understand why they happen. These events don’t just pop up out of nowhere; they’re the end result of specific problems, ranging from outright criminal fraud to simple human error. Once you can spot these triggers, you can start patching the weak spots in your own process before they turn into expensive headaches.

Think of a reversal as the final domino to fall. The problem might have started much earlier, maybe with a confusing checkout page or a billing statement that left a customer scratching their head. Let's dig into the most common reasons a customer or their bank might hit the undo button on a sale.

Criminal Fraud: The Obvious Culprit

This is the one everyone thinks of first. Criminal fraud is exactly what it sounds like: a thief uses stolen credit card details to buy something from your store. The real cardholder eventually spots the strange charge, reports it to their bank, and boom—a chargeback is initiated.

This kind of fraud is a direct hit on both the cardholder and your business. You lose the product you shipped and the payment for it. It's a clear-cut loss with no gray area.

While criminal fraud is a serious threat, it’s often not the biggest source of reversals for many businesses. The more frequent—and frankly, more frustrating—triggers often come from simple misunderstandings and customer-initiated disputes.

Processing and Merchant Errors

Sometimes, the call is coming from inside the house. Processing errors are those accidental slip-ups on your end that can easily push a confused or annoyed customer to dispute a charge. The good news is these are often the easiest to prevent, but they can cause major problems if they go unnoticed.

A few common examples include:

- Duplicate Charges: Accidentally billing a customer twice for the same order.

- Incorrect Amount: Charging the wrong price for an item or service.

- Delayed Shipping: Taking too long to ship an order, leading the customer to believe it’s never coming.

These are honest mistakes, but to a customer, they can feel like a raw deal, prompting them to call their bank instead of your support team.

Customer-Related Issues

A huge chunk of payment reversals start with the customer's experience. This bucket covers a wide range of issues where the customer feels like the product or service just didn't live up to the promise.

Here are the most common customer-related triggers:

- Product Not as Described: The item that shows up looks nothing like the photos online or feels much cheaper than they expected.

- Item Never Received: The customer insists their order never made it to their doorstep.

- Subscription Confusion: A customer completely forgets about a recurring charge or didn't realize they were signing up for a subscription in the first place.

- Unrecognized Billing Descriptor: The charge on their credit card statement is cryptic (e.g., "SP*WEBSERVICES" instead of "YourBrandName Puzzles"), so they assume it’s fraudulent and report it.

These situations really underscore how vital clear communication is, from your product descriptions all the way to the name that shows up on a customer's bank statement.

The Rise of Friendly Fraud

This is one of the fastest-growing and most maddening triggers for any merchant. Friendly fraud happens when a legitimate customer buys something from you but then disputes the charge with their bank to get their money back. It's essentially an attempt to get something for free.

They might falsely claim the product never arrived or wasn't as described, even if everything was perfectly fine. This behavior, also known as "chargeback abuse," leaves you in a tough position. You have a valid order from a real customer, but you’re still staring down a chargeback. Fighting it requires rock-solid evidence. You can explore effective strategies for dealing with friendly fraud in our in-depth article.

Historically, the cost of reversals has grown right alongside e-commerce. It's a painful reality that U.S. merchants often lose $4.61 for every dollar of fraud they face. This trend isn't slowing down, either. As new payment methods emerge, forecasts predict that chargeback costs could balloon to $41.69 billion by 2028. You can find more data on how the payment processing market is evolving on ClearlyPayments.com.

The True Cost of Reversals for Your Business

When a payment reversal hits your account, it's easy to fixate on the most obvious damage: the lost sale. But that initial sting is just the tip of the iceberg. The true cost of a reversal ripples through your entire business, creating a financial and operational mess that goes way beyond a single lost transaction.

It’s not just a simple deduction. It’s an expensive, multi-layered problem.

The Direct Financial Damage

The first hit is the most direct—the money that vanishes from your account the moment a reversal is processed. These are the costs you can see right away, and they add up fast, turning a once-profitable sale into a significant net loss.

Here’s a quick breakdown of what you're immediately out:

- The Original Transaction Amount: The full value of the sale is gone. That money is clawed back from your account and sent back to the customer.

- The Shipped Product: If you sell physical goods, you've probably already sent the item. Now you’ve lost the product and the payment you were supposed to get for it.

- Hefty Chargeback Fees: Your payment processor will slap you with a non-refundable fee for every single chargeback. These penalties can range from $20 to $100 per incident, and you have to pay them whether you win the dispute or not. For a deeper dive, learn more about what a chargeback fee entails in our detailed article.

It's easy to see how a $50 sale can quickly spiral into a $150 loss. It’s a painful financial hit, but unfortunately, the damage doesn't stop there.

A single payment reversal costs a business far more than the initial sale. It’s a triple threat: lost revenue, lost product, and added penalty fees that can quickly erode your profits.

The Hidden Operational Costs

Beyond the immediate financial drain, reversals create a cascade of hidden costs that are much harder to track. These are the operational burdens that steal time, energy, and resources from what you should be doing: growing your business.

Think about the hours your team has to spend fighting just one dispute. Someone has to drop what they're doing to gather evidence, write a compelling rebuttal, and then track the case through its entire lifecycle. That's valuable time that could have been spent on marketing, customer service, or product development.

To really get a handle on the financial impact of reversals, it's crucial for businesses to also focus on strategies for mastering small business cash flow management.

Long-Term Account Health Risks

Perhaps the most dangerous cost of all is the long-term threat to your merchant account. Payment processors and the major card networks like Visa and Mastercard are constantly watching your chargeback ratio—that’s the percentage of your transactions that turn into a chargeback.

If that ratio creeps too high (the industry standard is typically above 0.9%), you get flagged as a "high-risk" merchant.

Once you have that label, you can expect:

- Higher processing fees on all your transactions.

- Your acquiring bank placing a hold on your funds, sometimes for weeks.

- The eventual termination of your merchant account, leaving you completely unable to accept card payments.

This is why staying on top of reversals is so critical. Even though overall fraud rates are declining, many small and mid-sized businesses are still dangerously exposed. Recent reports show that while global payments revenue is growing, reversals threaten the sector's average 18.9% return on equity, making proactive management essential for survival. You can discover more insights about these global payment trends from McKinsey.

How to Proactively Prevent and Manage Reversals

The best defense against payment reversals is a good offense. Instead of just playing damage control when a dispute lands on your desk, you can take practical steps to stop most of them before they ever start. This isn't just about saving money; it's about building trust with your customers.

Let's dive into the strategies you can put in place right away to protect your business.

Create Crystal-Clear Communication

So many reversals, especially chargebacks, start with a simple misunderstanding. A confused customer is far more likely to call their bank than your support team, which makes clarity in every interaction your first line of defense.

One of the biggest culprits here is a confusing billing descriptor. That's the little line of text that shows up next to a charge on their credit card statement. If they see "SP*WEBSERVICES" instead of "Your Awesome Sock Store," they're probably going to assume it's fraud and hit the dispute button.

A clear billing descriptor is one of the easiest and most effective ways to prevent friendly fraud. It should immediately connect the charge to your brand, leaving no room for doubt.

To tighten up your communication, you should:

- Use a recognizable business name on your billing descriptor. Don't get cute; make it obvious.

- Send detailed order confirmations and receipts the second a purchase is made.

- Provide proactive shipping updates with tracking information so customers feel in the loop.

- Make your return and refund policies impossible to miss and easy to understand.

Offer Top-Notch Customer Service

When a customer has a problem, they want a fast, easy solution. If your support is hard to reach or takes forever to respond, their next call is going straight to their bank. Making your customer service accessible and efficient can stop a potential dispute in its tracks.

Believe it or not, nearly 40% of consumers return an online purchase at least once a month. If you treat these interactions as opportunities to provide great service, you can prevent a simple return from blowing up into a costly chargeback.

Beef Up Your Fraud Detection

While you can't stop every fraudster, modern tools can catch most suspicious activity before a transaction even goes through. For any online business, implementing basic security checks is non-negotiable. Think of these tools as a digital bouncer, protecting both you and legitimate cardholders.

Here are the key fraud prevention tools you need:

- Address Verification Service (AVS): This tool checks if the billing address the customer entered matches what the card issuer has on file.

- Card Verification Value (CVV): Requiring that three- or four-digit security code on the back of the card proves the customer physically has the card in their hand.

- 3D Secure (3DS): This adds an extra layer of authentication, often requiring a password or a one-time code sent to the cardholder's phone to verify the purchase.

Keep Detailed Records for Every Transaction

Even with the best prevention strategies in place, some reversals are going to slip through. When they do, your ability to fight back depends entirely on the quality of your records. Good documentation is your best weapon in a chargeback dispute.

For every single order, you should keep organized records of:

- Customer communications (emails, chat logs).

- Signed receipts or contracts, if applicable.

- Shipping and delivery confirmations (with tracking numbers!).

- Proof that the customer accepted your terms of service.

When you get hit with a dispute, this collection of evidence becomes your official rebuttal. A well-documented, compelling response is the only way you can challenge an unfair payment reversal and get your hard-earned revenue back.

Common Questions About Payment Reversals, Answered

Let's be honest, the world of payment reversals can feel like a maze. To help you find your way, we’ve put together answers to some of the most common questions merchants ask. Think of this as your quick-reference guide for those moments you need a clear, straightforward answer.

Isn't a Payment Reversal Just a Refund?

Not quite, but it’s a common mix-up. A refund is definitely a type of payment reversal, but the key difference boils down to who kicks things off.

When you issue a refund, you—the merchant—are in the driver's seat. You’re voluntarily returning the customer’s money after a transaction has already settled. It's an agreement between you and them.

But other reversals, like the dreaded chargeback, are started by the customer through their bank. This forces the funds out of your account and throws you into a formal dispute process, often bringing extra fees and penalties along for the ride.

How Long Does a Payment Reversal Take?

That all depends on the type of reversal. Each one follows a different road with its own speed limits, so the timeline can vary quite a bit.

- Authorization Reversals: These are lightning-fast. Since the money never actually landed in your account, they typically clear in just 1-3 business days.

- Refunds: A standard, merchant-initiated refund usually takes about 5-7 business days to process and show up back in the customer’s account.

- Chargebacks: This is the marathon of the bunch. Because of all the back-and-forth investigation and evidence review, a chargeback can take anywhere from a few weeks to several months to finally resolve.

Can a Merchant Stop a Payment Reversal?

While you can't always stop a customer from starting one, you absolutely have the power to fight back—especially when it comes to chargebacks. If you’re confident a customer’s dispute is baseless (hello, friendly fraud), you can challenge it through a process called representment.

This is your chance to prove the transaction was legitimate by submitting solid evidence to your payment processor. Things like shipping confirmations, delivery photos, and customer emails are your best weapons for getting an unfair reversal overturned and winning back your money.

A payment reversal isn't the final word. Merchants have a right to dispute chargebacks with solid evidence, turning a potential loss into a recovered sale.

Getting a handle on these key differences helps you prepare for whatever comes your way, protecting not just your revenue but your business’s hard-earned reputation.

Tired of manually fighting disputes and losing money? ChargePay uses AI to automate the whole process, building winning evidence packages to recover your revenue without you lifting a finger. Stop letting unfair chargebacks drain your profits and see how much you can reclaim at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)