An address verification credit card check is one of the simplest, yet most effective, fraud prevention tools working for you behind the scenes. Known in the industry as the Address Verification Service (AVS), it's an automated check that instantly compares the billing address a customer enters with what their bank has on file, giving you a quick signal on whether a purchase is legit.

What Is Credit Card Address Verification

Picture a customer at your online checkout. They’ve filled their cart, entered their credit card details, and are about to click that final ‘Pay’ button. In the split second that follows, a crucial security check kicks off automatically. That’s the Address Verification Service, or AVS, in action.

Think of it as a quick ID check at a club's entrance. It’s not a full background check, but it’s a fast, automated first look to see if the basic details line up. AVS compares the billing address your customer just typed in with the official address their card-issuing bank has on record. Its main job is to be your first line of defense against card-not-present fraud, a massive headache for any online merchant.

Why This Quick Check Matters

As e-commerce continues to boom, so does the threat of fraud. The numbers are pretty stark—global credit card fraud losses are projected to climb to a staggering $38.5 billion by 2027. This isn't just a background statistic; it's a real threat that makes tools like AVS absolutely essential, not just optional.

This simple verification step accomplishes a few key things for your business:

- Reduces Fraud Risk: It throws a wrench in the plans of criminals who have stolen card numbers but not the associated billing address.

- Lowers Chargeback Rates: By catching suspicious transactions before they’re even approved, AVS helps you avoid the pain and cost of chargebacks later on.

- Increases Approval Confidence: A solid AVS match is a strong green flag. It gives you the confidence to process and fulfill an order without hesitation.

AVS and CVV: A Powerful Duo

It's important to remember that AVS doesn't work alone. It’s one half of a powerful security team, and its partner is the CVV. While AVS verifies the address linked to the card, the CVV check confirms that the customer likely has the physical card in their hand. To get the full picture, you can check out our guide on what CVV is.

When you use both AVS and CVV checks together, you’re creating a much tougher barrier for fraudsters to break through.

AVS isn't a silver bullet, but it's an incredibly effective first filter. It quickly weeds out obvious fraud attempts, allowing you to focus your attention on orders that might need a closer look.

How AVS Really Works During a Transaction

When your customer clicks that "buy" button, the Address Verification Service check happens in the blink of an eye. It’s like a lightning-fast, automated conversation between your store, the credit card company, and your customer's bank.

This whole process is a key part of authorizing the payment, often happening right alongside a pre-auth check. We actually break down the entire authorization process in our guide to credit card pre-authorization.

For now, let’s unpack that super-quick digital handshake. It’s a lot simpler than it sounds.

The AVS Data Flow

The journey begins the second a customer submits their order. Your payment gateway, whether it's Stripe or Shopify Payments, doesn't do the check itself—it’s more like a secure messenger.

Your Store Sends the Request: First, your gateway bundles up the payment info, including the billing address the customer typed in. It zips this package over to the credit card network (like Visa, Mastercard, or American Express).

The Network Asks the Bank: The card network acts as a go-between, forwarding the address details to the customer’s issuing bank—the bank that actually gave them the card. This is where the real check happens.

The Bank Responds: The issuing bank takes the numbers from the customer's entry and compares them to what it has on file. It then sends back a single-letter AVS response code to the network, which relays it right back to your payment gateway.

This entire back-and-forth takes less than two seconds, but that single letter it returns is gold for making a quick risk assessment.

Here's the most common point of confusion: AVS only verifies the numeric parts of an address. It completely ignores alphabetic characters. This means it's only checking the street number and the ZIP code.

What AVS Actually Checks

Knowing what AVS looks at—and what it ignores—is the key to using it effectively. If a customer lives at "123 Main Street, Anytown, CA 90210," the AVS system is laser-focused on just two things:

- The Street Number:

123 - The ZIP Code:

90210

That's it. It completely disregards "Main Street," "Anytown," and "CA." This is why a customer could type "Main St" instead of "Main Street" and still get a perfect match.

It’s also why a fraudster who has stolen a card number, ZIP code, and house number might pass an AVS check, even if they have no idea what the street name is.

This numbers-only approach is what makes AVS so fast and efficient. But it also shows why you should treat it as one important signal, not a complete fraud-detection system. It gives you a crucial piece of the puzzle, but it’s not the whole picture.

Making Sense of AVS Response Codes

After an AVS check completes its lightning-fast round trip, your payment gateway gets a single-letter response code back from the customer's bank. These codes can feel like a secret language, but learning to translate them is how you turn raw data into smart, revenue-protecting decisions.

Think of these codes as traffic signals for your transactions. They help you quickly sort orders into categories you can act on: a green light for a full match, a yellow light for a partial match that needs a closer look, and a red light for a clear mismatch that you should probably decline.

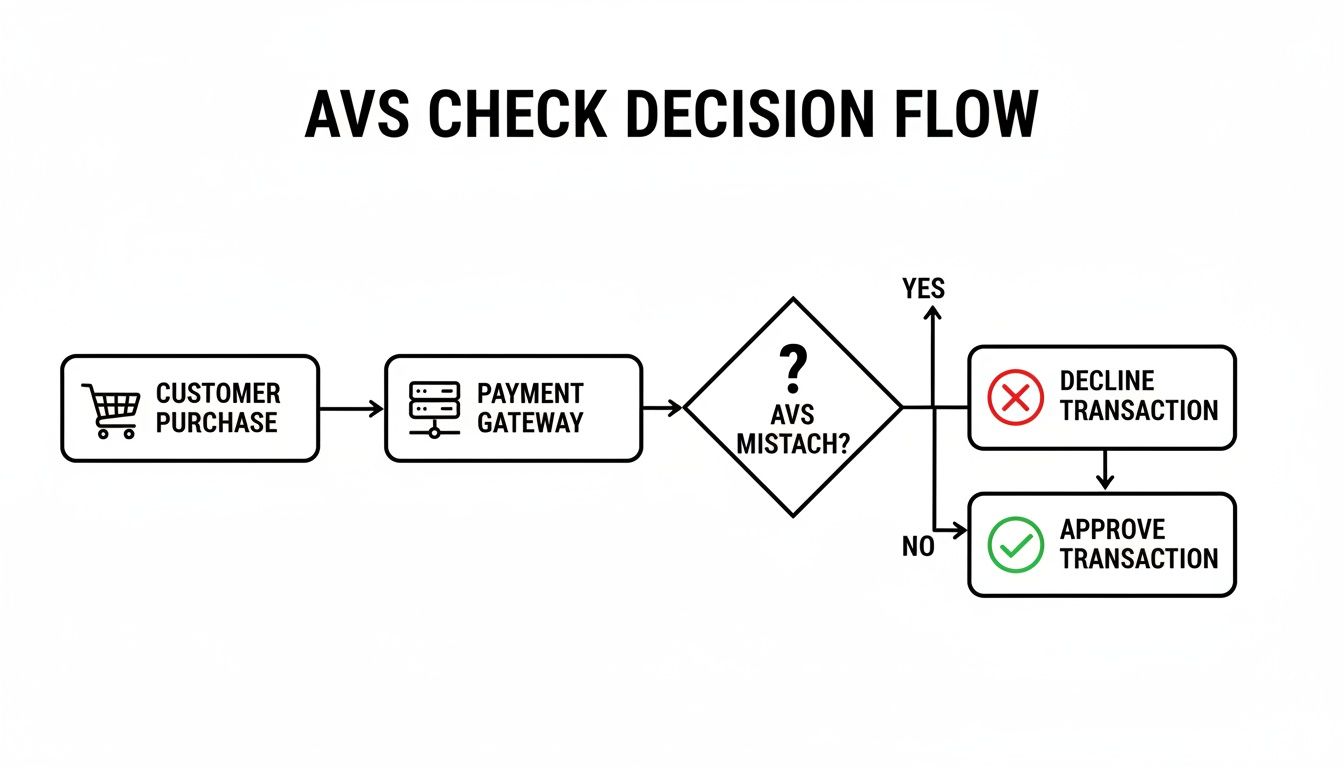

This decision-making flow shows how an AVS check fits into the broader transaction process.

As you can see, the AVS check is a critical fork in the road. A mismatch should trigger a more cautious approach, not an automatic approval.

So, what do these codes actually mean? While there are dozens of them, they generally fall into one of the three "traffic light" categories. Let's break down the most common ones you'll encounter.

Green Light Codes: Full Match

A full match is the best-case scenario. It means both the street number and the ZIP code entered by the customer line up perfectly with what the issuing bank has on file. This gives you a high degree of confidence that the person making the purchase is the legitimate cardholder.

- Code Y: (Visa, Mastercard, Discover, Amex) - This means the street address and the 5-digit ZIP code both match perfectly. For US-based transactions, this is the strongest positive signal you can get.

- Code X: (Amex, Discover) - Also a full match, this code indicates that both the street address and the 9-digit ZIP code are correct.

When you see a full match, especially when combined with a successful CVV check, you can typically fulfill the order with confidence.

Yellow Light Codes: Partial Match

Partial matches are where things get interesting and require a bit of judgment. These codes tell you that one piece of the address matched, but not the other. This isn't an automatic red flag for fraud; it could be a simple typo or a customer using a new address that hasn't been updated at their bank yet.

A partial match requires context. An AVS mismatch on a small, routine order from a returning customer is very different from the same mismatch on a high-value, first-time international order.

Common "yellow light" codes include:

- Code A: The street address matches, but the ZIP code does not. This could easily be a typo (e.g., entering 90210 instead of 90211). It's worth a second look, especially on larger orders.

- Code Z: The 5-digit ZIP code matches, but the street address does not. This is a common result that could be anything from a simple typo to something more suspicious.

- Code W: The 9-digit ZIP code matches, but the street address does not. Similar to Code Z, this calls for a closer review.

For these transactions, you need to look at the bigger picture. Does the shipping address match the billing address? Is the order unusually large? Does the customer's IP address location make sense?

Red Light Codes: No Match or System Issue

Finally, we have the "red light" codes. These indicate a complete mismatch or a technical problem with the verification itself. You should treat these with extreme caution and, in most cases, decline the transaction outright to avoid a likely fraudulent chargeback.

- Code N: Neither the street address nor the ZIP code matches the bank's records. This is a major red flag for fraud.

- Code U: Address information is unavailable. This often happens because the card-issuing bank doesn't support AVS, which is common for many international banks.

- Code R: System unavailable. The check couldn't be performed due to a timeout or other technical issue. It's safest to retry or decline.

To make this even easier, here's a quick reference table of the most common AVS response codes you'll see from networks like Visa, Mastercard, and American Express.

Common AVS Response Codes and What They Mean

Remember, these codes aren't standalone commands—they are pieces of a larger puzzle. Using them wisely alongside other fraud-prevention tools is the key to protecting your business without turning away good customers.

How to Set Up AVS in Your Payment Tools

Knowing what AVS response codes mean is one thing, but actually putting that information to work is what saves your business from fraud. You need to get under the hood of your payment tools and make sure they’re set up to act on those signals.

The good news? Most major platforms—think Shopify, Stripe, and PayPal—enable address verification credit card checks right out of the box.

But here's the catch: their default settings are usually designed to be one-size-fits-all. What works for a high-volume, low-value shop might not work for a business selling luxury goods. A few minutes spent customizing these rules can dramatically lower your fraud risk without accidentally blocking good customers.

The market for this tech is booming for a reason. It's expected to jump from $1.71 billion in 2024 to $1.83 billion in 2025, which shows just how seriously businesses are taking this. You can see the full breakdown of this growth on thebusinessresearchcompany.com.

Fine-Tuning AVS in Shopify

If your store runs on Shopify Payments, you’re already set up with both AVS and CVV checks. Shopify’s own fraud analysis uses these signals to flag potentially shady orders. But you can get more hands-on.

Using a tool like Shopify Flow, you can build your own simple automations. For instance, you could create a rule that slaps a "Review" tag on any order that returns a partial AVS mismatch (like codes A or Z). This simple step makes sure your team manually eyeballs those questionable orders before anything gets shipped.

Customizing AVS Rules in Stripe

Stripe's fraud tool, Radar, is powerful, and it leans heavily on AVS data to generate a risk score for every single transaction. It’s pretty smart on its own, but you can teach it to be even smarter by creating custom rules that fit your store's specific risks.

Head over to the Radar rules section in your Stripe dashboard. From there, you can get incredibly specific.

For example, you could set up a rule to automatically block any payment attempt where the AVS ZIP code fails, but only if the order total is over $200. This is a fantastic way to stop high-value fraud attempts in their tracks.

This kind of detailed control lets you be aggressive with transactions that scream "fraud" while letting less risky ones slide through without a hitch. And if you’re juggling multiple payment gateways, applying these rules consistently is key. You can get a better handle on managing these complex setups by checking out our guide on the payment orchestration platform.

Checking Your PayPal AVS Settings

Over on PayPal, your AVS settings are usually tucked away in your account’s "Payment Receiving Preferences" or fraud management filters.

In this section, you can tell PayPal exactly how to handle transactions based on their AVS and CVV responses. You can choose to accept them, deny them flat out, or flag them for a manual review. It’s a good idea to pop in and check these settings every few months to make sure they still make sense for your business and aren't leaving you exposed to easily preventable fraud.

Where AVS Falls Short and How Fraudsters Adapt

While the Address Verification Service is a fantastic first line of defense, it’s not an impenetrable shield. Thinking of it as a complete fraud solution is a common—and costly—mistake.

The real value of AVS comes from seeing it as just one layer in a much smarter, multi-layered security setup. To build that setup, you first need to know where the weak spots are.

One of the biggest blind spots for AVS is international orders. The system was originally built for cardholders in places like the US, Canada, and the UK. While its reach is growing, many banks in other parts of the world simply don't support it yet.

This means that when a legitimate international customer makes a purchase, their transaction might return a code like 'U' (Unavailable) or 'G' (Global Non-Match), which can look like a red flag. If you automatically decline these orders, you could be turning away perfectly good customers and losing out on sales.

How Cunning Fraudsters Sidestep AVS

Even when AVS is fully supported, determined criminals have found ways to get around it. They know how the system works and they exploit its limitations. This is exactly why a simple address verification credit card check can't be your only tool.

A common tactic involves using stolen data that is partially correct. Here are a few ways they do it:

- Correct Billing, Different Shipping: A fraudster gets their hands on a full card number and the correct billing address from a data breach. They’ll pass the AVS check with flying colors, but then have the package shipped to a different "drop" address they control.

- Social Engineering: Sometimes, a criminal will call the cardholder's bank, pretend to be the legitimate customer, and add a secondary address to the account. Once that's done, this new address will pass an AVS check without a problem.

- Exploiting System Gaps: The global expansion of AVS has helped, but it has also created inconsistencies. For instance, Visa is mandating that more Asia-Pacific countries support AVS by April 2025, but effectiveness varies wildly because of different address formats and banking rules. This patchwork of support creates opportunities for fraudsters who know which banks are less strict. You can find more details about this geographic expansion on fraud.net.

Understanding these weaknesses isn't about dismissing AVS; it’s about having a realistic view of its role. It’s a valuable signal, but it has to be combined with other tools. By recognizing where AVS falls short, you can start building a more robust approach to ecommerce fraud prevention that protects your revenue without blocking legitimate customers.

Building a Stronger Fraud Defense Strategy

So, we've established that the Address Verification Service isn't a silver bullet. Think of it as one key player on a full fraud-fighting team. Relying solely on AVS leaves your business exposed, but layering it with other simple checks creates a much stronger defense.

This strategy isn't about adding a ton of complexity; it’s about adding layers of security. Each new check you add helps catch something the previous layer might have missed, which can dramatically reduce your risk of facing a painful chargeback.

Your Fraud Prevention Checklist

Consider AVS as step one. When a transaction comes in—especially one with a "Yellow Light" partial AVS match—it’s smart to run through a few more quick checks. These signals, when looked at together, paint a much clearer picture of whether an order is legit.

Always Check the CVV: This one is non-negotiable. The CVV check confirms that the customer likely has the physical card in their hands. An AVS match without a CVV match is still a massive red flag.

Compare IP Geolocation: Take a look at where the customer’s IP address is located. If they're placing an order from a device in a different state or country than their billing address, it’s a good reason to pause and investigate further.

Flag Shipping and Billing Mismatches: This is a classic move for fraudsters: use a valid billing address but ship the goods to their own "drop" location. While there are plenty of legitimate reasons for different addresses (like sending a gift), a mismatch on a high-value order definitely warrants a closer look.

As you build out your fraud defense, it also helps to know about the frameworks that govern consumer credit. Gaining insights into topics like the legal rights under the Fair Credit Reporting Act can provide some valuable context for your policies.

When to Bring in Reinforcements

Here's the hard truth: even with the best preventative measures, some fraudulent transactions will inevitably slip through. When they do, they turn into chargebacks, creating a whole new set of problems for your business. This is where your strategy needs a final, crucial layer.

A strong defense is both proactive and reactive. You need tools to block fraud upfront and a system to fight the disputes that still get through.

This is where a dedicated chargeback management solution fits into the picture. Instead of getting bogged down fighting every dispute yourself, these tools can automate the entire process, handling the evidence gathering and recovery for you. For a deeper dive, check out our complete guide on chargeback fraud prevention.

By combining AVS with other manual checks and backing it all up with an automated chargeback solution, you create a robust system that protects your revenue at every stage of the transaction.

Got Questions About AVS? We've Got Answers

Let's clear up some of the most common questions merchants have about credit card address verification. Getting these concepts straight will help you use AVS to its full potential.

What's the Difference Between AVS and CVV?

Think of AVS and CVV as two security guards at a checkpoint, each looking for something different. They work best as a team.

The Address Verification Service (AVS) is the guard who checks the shopper's ID to make sure the billing address they typed in matches what the bank has on file. The CVV check, on the other hand, is the guard asking for the secret code—that 3 or 4-digit number on the physical card—to prove the customer actually has the card in their hand.

They're separate but equally vital security checks. Using both gives you a much stronger defense against fraud than relying on just one.

Does a Failed AVS Check Always Decline a Payment?

Nope, not automatically. A failed AVS check doesn't have to be an instant dealbreaker. You're the one in the driver's seat, setting the rules inside your payment gateway, whether that's Shopify, Stripe, or another platform.

You have the power to decide whether to accept, flag for manual review, or automatically decline payments based on the specific AVS response code you receive.

This is where the real art of fraud management comes in, letting you find the perfect balance between tight security and a smooth checkout experience for legitimate customers.

Can AVS Stop All Types of Chargebacks?

I wish I could say yes, but unfortunately, it can't. AVS is a fantastic tool for sniffing out straightforward fraud where a scammer is using stolen card numbers. It's incredibly effective at preventing those kinds of chargebacks.

But AVS can't do anything about chargebacks filed for other reasons. For example, a customer might still file a dispute claiming a product wasn't what they expected or that they never received their order—even if the AVS check was a perfect match. AVS confirms the cardholder's identity at the point of sale, but it can't prove what happened after that.

Even with the best fraud prevention strategy, some chargebacks will inevitably slip through the cracks. ChargePay uses AI to take over the entire dispute process, recovering your lost revenue without you lifting a finger. Learn how ChargePay can protect your business.

.svg)

.svg)

.svg)

.svg)