Let's get straight to it. That little 3 or 4-digit code on a credit card? That's the CVV2, and it's your secret weapon for verifying your customer actually has the physical card during an online purchase. Think of it as the digital bouncer for your checkout page—it asks for proof before letting a transaction in.

What Is a CVV2, Really?

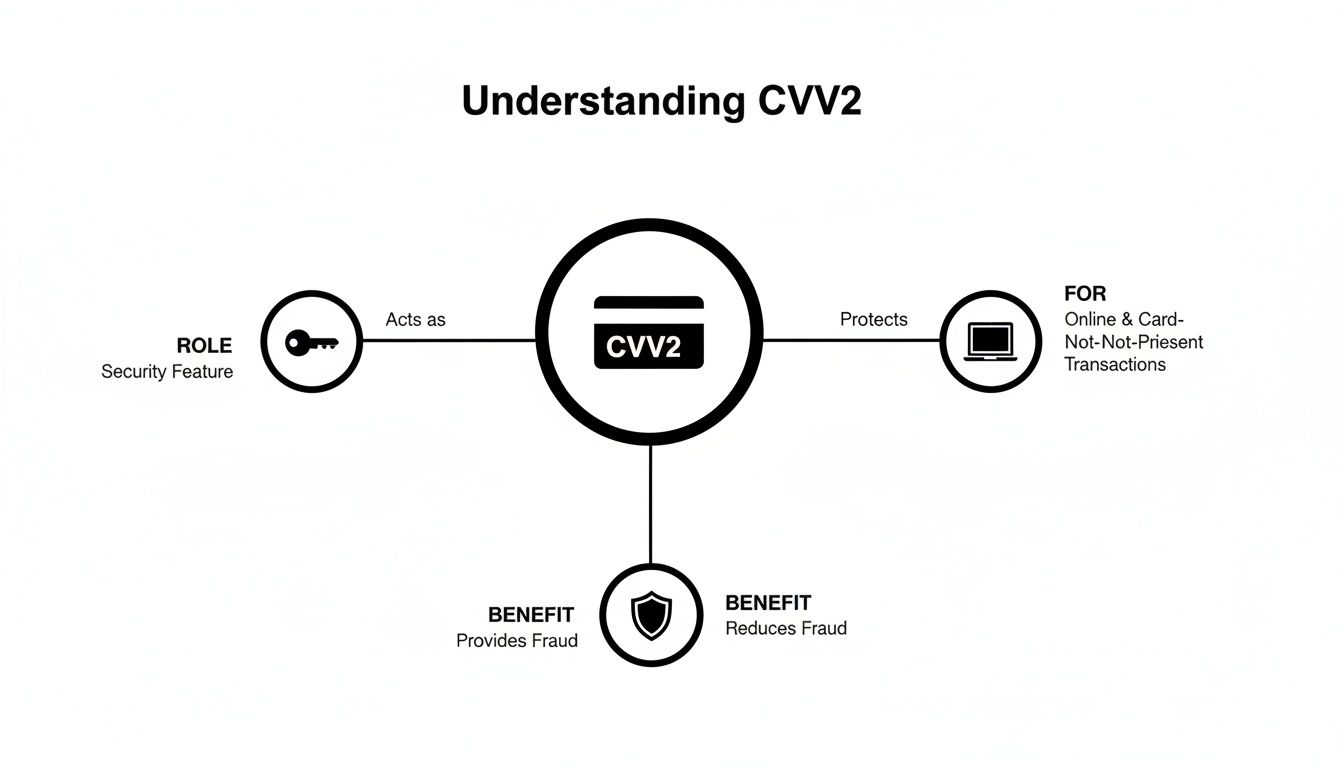

If you run an ecommerce store, you’re more than familiar with that little "security code" field at checkout. That’s the CVV2, and it’s one of the simplest yet most effective tools you have in the ongoing fight against fraud.

It stands for Card Verification Value 2, and its job is dead simple: to prove the person making the purchase has the credit card in their hands.

What makes this little number so powerful is that it isn't stored in the card's magnetic stripe or embedded in the chip. So, even if a massive data breach exposes a list of credit card numbers and expiration dates, the CVV2 is designed to stay separate and secure. When a customer types it in correctly, you get a solid piece of evidence that the transaction is legitimate.

Where Did the CVV2 Come From?

The need for a security feature like this became painfully obvious as ecommerce started to take off. The CVV2 showed up in the mid-1990s to tackle the explosion of card-not-present (CNP) fraud that came with the dot-com boom. As you can learn on chargebacks911.com, this simple addition made it much harder for criminals armed with nothing more than a stolen card number to go on an online shopping spree.

This check is just one part of the bigger puzzle of making sure a transaction is authentic. To see how it fits into the whole process, you can explore our guide on credit card number validation.

Key Takeaway: The CVV2 is a real-time security check. It confirms card possession for online or phone orders, helping you stop fraud before it happens and cut down your risk of dealing with expensive chargebacks later.

CVV2 at a Glance

To make it even simpler, here's a quick summary of everything you need to know about the CVV2.

In short, the CVV2 is a small but mighty tool. It's a first line of defense that every online merchant should be using to protect their business and their customers.

Decoding the Jargon: CVV, CVV2, CVC, and CID

It’s easy to get lost in the alphabet soup of payment security. You’ll see terms like CVV, CVC, CID, and CVV2 thrown around, and honestly, it can feel a little overwhelming. But here’s the simple truth: they are all just different brand names for the exact same security feature.

Think of it like soda, pop, and coke. Depending on where you live, you’ll hear different words for a carbonated soft drink, but everyone knows what you mean. The credit card world is no different. Visa, Mastercard, Discover, and American Express just slapped their own labels on the same core idea.

This is all about having a simple code that proves the person making the purchase actually has the physical card in their hands.

As you can see, the CVV2 is a critical piece of the puzzle for online transactions, acting as a gatekeeper to verify the cardholder is legitimate.

The Number That Really Matters to You Is '2'

For any online business, the most important part of this terminology is the number '2' you see in CVV2 or CVC2. That one little digit signals a huge difference in how the code is used. It specifically means the security code is for “card-not-present” transactions—your bread and butter online and over-the-phone sales.

There’s another version, the CVV1 or CVC1, that you'll likely never encounter. This code is encoded directly onto the card's magnetic stripe and is only read during an in-person swipe at a physical terminal. It’s completely invisible and inaccessible for online use, which is precisely why the CVV2 was created.

The '2' in CVV2 is your signal that the code is designed for remote transactions. It creates a firewall between online security and the security used for physical swipes, adding a vital layer of protection against fraud.

This distinction is key. If a fraudster skims a card's magnetic stripe data at a gas pump, they only get the CVV1. That information is totally useless for making a purchase on your website. To buy from you, they need the CVV2 printed on the physical card. It's an extra security step that works alongside other powerful tools like what is 3-D Secure authentication.

Card Security Code Cheat Sheet

While they all do the same job, each major card network uses its own name for the security code, and the location on the card can differ. Getting familiar with these small differences will make you fluent in payment security and help you guide customers who might get stuck at checkout.

Here’s a quick breakdown to help you keep everything straight:

Knowing these details helps you create a smoother checkout. For instance, you can add small visual cues or help text that says "Look for the 4-digit code on the front of your Amex card" to prevent customer friction and reduce cart abandonment. It’s a small touch that makes a big difference.

How CVV2 Protects Your Business from Fraud

Think of the CVV2 as the digital bouncer for your online store. In a world where stolen credit card numbers are unfortunately common, this simple three or four-digit code is your first line of defense. Its entire job is to answer one critical question at checkout: "Does the person making this purchase actually have the physical card in their hand?"

By requiring a CVV2, you immediately filter out a huge number of fraudsters. These criminals often operate with massive lists of stolen card numbers bought off the dark web. Those lists might have the primary account number and expiration date, but they almost never include the CVV2. That's because PCI compliance rules strictly forbid you—and every other merchant—from ever storing this code.

This simple verification step is a direct and powerful defense for your bottom line. It isn't just a technical formality; it's a security checkpoint that saves you from shipping products to criminals, losing revenue, and dealing with the nightmare of chargebacks.

The Power of a CVV2 Match

When a customer punches in their CVV2 at checkout, your payment gateway shoots a request over to the card-issuing bank. The bank then sends back a response code, which usually falls into one of three buckets.

- Match: The code is correct. This is a strong signal that the legitimate cardholder is making the purchase.

- No Match: The code is incorrect. This is a massive red flag for fraud.

- Not Processed: The issuing bank, for whatever reason, chose not to check the code.

A successful match is compelling evidence that the transaction is legitimate. A "No Match" response, on the other hand, should almost always trigger an automatic decline. Letting a sale go through after a failed CVV2 check is like hearing a fire alarm and ignoring it—it exposes your business to a risk that's easily avoidable.

Requiring CVV2 at checkout is one of the most effective, low-effort fraud prevention measures you can implement. It acts as a real-time gatekeeper, stopping bad actors before they can cause damage to your business.

This one check is incredibly effective. Industry data shows that requiring a CVV2 at checkout can slash fraud attempts by up to 60-70% in high-risk categories like digital goods. Even better, mismatched codes alone can flag 25-30% of suspicious orders, stopping potential chargebacks dead in their tracks. For a deeper dive into this data, check out the analysis from Chargebacks911.com.

Real-World Scenarios Where CVV2 Saves the Day

Let's walk through a common fraud scenario. A fraudster gets their hands on a list of thousands of stolen card numbers and expiration dates from a data breach at a large retailer. They then use a bot to hammer various ecommerce sites with these numbers, looking for any store that doesn't require a CVV2.

If your store skips this step, you become an easy target. The fraudster places dozens of orders for your most expensive items. The initial transactions will likely get approved since the card number and expiry date are valid. You ship the products, and a few weeks later, the real cardholders notice the bogus charges and file chargebacks. Now you're out the product, the revenue, and you've been slapped with costly chargeback fees.

Now, let’s replay that same scenario, but this time with CVV2 verification turned on. The fraudster’s bot tries to make a purchase but hits a brick wall at the CVV2 field. Since the bot doesn't have the code, the transaction is immediately declined. You’ve just prevented fraud, saved inventory, and protected your revenue—all without lifting a finger. This proactive measure is a cornerstone of solid ecommerce fraud prevention best practices.

Building a Stronger Security Foundation

While the CVV2 offers crucial protection, it’s just one piece of a larger puzzle. Real security comes from a layered approach. A great CVV2 process works best when you combine it with other security measures.

Implementing multiple layers of defense creates a much more robust system that's far harder for fraudsters to break through. This not only protects your business but also builds trust with your customers. While the CVV2 is a fantastic tool, remember to treat it as one vital part of your overall security strategy. For a broader perspective, it's worth reviewing comprehensive website security best practices that cover every aspect of protecting your online presence.

Using CVV2 to Win More Chargeback Disputes

When a chargeback notification lands in your inbox, it can feel like a punch to the gut. But in the often-murky world of payment disputes, that little CVV2 code is your secret weapon, capable of turning a potential loss into a winnable fight.

Think of it this way: a chargeback is basically a customer telling their bank, "That wasn't me," or "I didn't authorize that." Your job is to prove they likely did. Presenting a successful CVV2 match is like having a star witness on your side.

This simple piece of data serves as powerful evidence that the legitimate cardholder was present—at least digitally—and gave the green light for the purchase. It systematically dismantles the all-too-common "unauthorized transaction" claim.

Turning Evidence into Revenue Recovery

When you respond to a chargeback, it's all about providing compelling evidence. The bank acts as a referee between you and the cardholder, and the side with the stronger proof usually comes out on top. A successful CVV2 match is one of the strongest pieces of evidence you can have for a card-not-present transaction.

Here’s how it strengthens your case:

- It proves card possession: The whole point of CVV2 verification is to confirm the customer has the physical card. By providing proof of a match, you show the bank it wasn't just a stolen number from a database breach.

- It counters friendly fraud: While it won't stop a truly determined friendly fraudster, it makes their claim much harder to justify. It’s difficult for a customer to argue a transaction was unauthorized when you can prove a code from their physical card was used.

- It adds credibility: A CVV2 match, combined with other data points like an AVS (Address Verification Service) match and a matching IP address, creates a layered defense that is very hard to poke holes in.

Submitting this data during the representment process can be the single deciding factor that gets a chargeback reversed in your favor, putting the revenue back where it belongs—in your account.

Key Insight: A successful CVV2 match shifts the burden of proof. It forces the cardholder to explain how their physical card's security code was used without their permission, a much higher bar than simply claiming a number was stolen online.

The Statistical Advantage of a CVV2 Match

The impact of using CVV2 verification isn't just theoretical; it's backed by hard numbers. In the high-stakes game of fraud prevention, data shows that transactions validated with a CVV2 enjoy 65-75% lower chargeback ratios compared to those without a match.

On the flip side, non-matches can spike fraud risk by 4x and trigger holds on 20-30% of orders. You can discover more insights about this on 3dmerchant.com.

This data tells a clear story. Requiring a CVV2 isn't just a best practice; it's a statistically proven strategy for cutting your financial risk right from the start.

Building an Airtight Chargeback Case

While a CVV2 match is crucial, it’s most effective when it’s part of a complete evidence package. To build the strongest possible defense against a chargeback, you should always include the following:

- Proof of CVV2 Match: Clearly state that the CVV2 provided by the customer matched the code on file with the issuing bank.

- AVS Match Results: Show that the billing address entered by the customer matched the address the bank has on record.

- Order and Shipping Details: Include invoices, shipping confirmations, and delivery tracking numbers to prove you held up your end of the bargain.

- Customer Communications: Provide any emails, chat logs, or support tickets that show interaction with the customer.

By compiling this information, you create a comprehensive narrative that demonstrates the transaction was legitimate. This approach is fundamental if you want to learn how to win a credit card dispute more consistently. It’s not about just one piece of evidence but the combined weight of all the evidence.

The Golden Rule of CVV2: Never Store It

When it comes to handling CVV2 codes, there’s one non-negotiable, golden rule you absolutely have to follow: never, ever store them. This isn't just a friendly suggestion—it’s a hard-and-fast requirement from the Payment Card Industry Data Security Standard (PCI DSS). Breaking this rule can bring massive consequences down on your business.

The rule is simple. Once a transaction is authorized, any CVV2 data you collected must be permanently wiped. Storing this three or four-digit code, even if it's encrypted, turns your systems into a goldmine for hackers. If you get hit by a data breach, stolen card numbers are far less valuable to criminals without their matching CVV2s.

Why Storing CVV2 Is So Risky

Imagine a fraudster gets their hands on a list of credit card numbers from a compromised database. Without the CVV2, that list is mostly useless for online shopping. But if you’ve been storing CVV2s and your system gets breached? You’ve just handed criminals the keys to the kingdom.

This single mistake can lead to devastating outcomes for your business and your customers. The PCI Security Standards Council put this rule in place for a few very good reasons:

- To Limit Breach Impact: By not storing the CVV2, you make sure that even if other card data is stolen, it can't be immediately used for fraudulent online purchases.

- To Protect Customers: You have a responsibility to protect your customers' financial data. Storing CVV2s puts them at unnecessary risk of fraud.

- To Avoid Severe Penalties: Violating PCI DSS rules can result in hefty fines, the loss of your ability to process credit cards, and serious damage to your brand's reputation.

Following this golden rule is a critical part of implementing comprehensive data breach prevention strategies and protecting the sensitive information your customers trust you with.

How Modern Payment Processors Keep You Safe

Here's the good news. If you're using a modern, compliant payment processor like Stripe, PayPal, or Braintree, this is all handled for you automatically. These payment gateways are designed from the ground up to be fully PCI compliant, which means they manage the entire verification process without ever storing the CVV2 on your servers.

When a customer enters their card details on your checkout page, that information is sent directly to the payment gateway through a secure connection. The gateway then forwards the CVV2 to the card’s issuing bank for verification. After the transaction is approved or declined, the gateway immediately purges the CVV2 code.

Crucial Takeaway: Using a PCI-compliant payment gateway is the easiest and safest way to follow the rules. These systems are built to handle sensitive data securely, shielding you from the massive liability and technical burden of doing it yourself.

This process often involves even more advanced security methods. For instance, many gateways use a technique where sensitive card details are replaced with a unique, non-sensitive identifier. To see how this works in more detail, you can learn about what is tokenization in payments in our dedicated guide. It adds another powerful layer of security, ensuring real card data never even touches your system.

By relying on a trusted payment partner, you can focus on growing your business with the peace of mind that you're protecting your customers and staying on the right side of the law.

Smart Ways to Use CVV2 in Your Checkout Flow

Knowing what a CVV2 is and why it matters is half the battle. The other half is actually putting that knowledge to work in your checkout process. A clunky, confusing checkout flow is a surefire way to lose customers to abandoned carts, while a smart one builds security without creating friction.

The goal here is to make providing the CVV2 as painless and intuitive as possible. That means clear labeling is non-negotiable. Don't just slap "CVV" on the field and call it a day. Use more descriptive text like "Security Code" or even "3-digit code on back" to guide your customers.

Want to take it a step further? Add a small help icon (like a little question mark) next to the field. When a customer hovers over it, a pop-up can show a quick visual of where to find the code on a Visa versus an American Express card. It’s a simple touch that eliminates confusion and keeps the checkout process humming along smoothly.

How to Interpret Payment Gateway Responses

When a customer hits "pay," your payment gateway talks to the card-issuing bank almost instantly to verify the CVV2. The bank then sends back a response code that tells you if the number was a match. Learning to read these responses is critical for setting up automated fraud rules that actually work.

The responses boil down to one of three main categories:

- M = Match: The CVV2 the customer typed in is correct. This is a great sign that the transaction is legitimate.

- N = No Match: The CVV2 is wrong. This is a massive red flag and points to a high probability of fraud.

- P = Not Processed: The bank didn't check the CVV2. This can happen for a few reasons, but it means you don't have that extra layer of security you were hoping for.

Think of these codes as a direct line of communication with the bank, giving you real-time intel on how risky each transaction is.

Best Practice: Treat a "No Match" response as an immediate stop sign. Pushing a transaction through after a failed CVV2 check is just asking for trouble—it's an unnecessary risk that almost guarantees you'll face fraud and lose the inevitable chargeback.

Setting Up Smart Automated Rules

Your payment processor or fraud prevention software should let you create rules based on these CVV2 responses. Dialing these in correctly will maximize your security without accidentally blocking legitimate buyers who might have just made a typo.

Here’s a practical way to set up your rules:

- Always Decline on 'No Match' (N): This should be your most rigid rule. Any transaction that comes back with a "No Match" response should be automatically declined, no questions asked. The fraud risk is just too high to approve it.

- Flag 'Not Processed' (P) for Review: Since the bank didn't give you a thumbs-up on the code, these transactions are a bit riskier. Instead of an automatic decline, you can set up your system to flag these orders for a quick manual look-over, especially if other risk factors pop up (like a huge order value or an international shipping address).

- Approve on 'Match' (M): A successful match is exactly what you want to see. These transactions can typically be approved automatically, particularly if they also pass other checks like the AVS (Address Verification Service).

By automating these decisions, you build a powerful, hands-off system that weeds out the most obvious fraud while giving your good customers a seamless experience. It's a proactive approach that strengthens your defenses, cuts down your chargeback rate, and protects your hard-earned revenue.

Got Questions About CVV2? We've Got Answers.

Even once you get the hang of what CVV2 is all about, a few practical questions almost always come up. Let's walk through the most common ones to clear up any confusion and make sure you're using this security code with total confidence.

What if a Card Doesn't Have a CVV2?

First up, what do you do if a card simply doesn't have a CVV2 code printed on it? While this is incredibly rare these days, you might occasionally run into an older or specialized card without one.

In these situations, you unfortunately lose that critical layer of security. This makes it doubly important to keep a close eye on other potential fraud signals, like any AVS mismatches that might pop up.

Should I Ever Process a Transaction Without a CVV2?

This leads to another big question: is it ever okay to process a payment without the CVV2? While your payment gateway might technically let you do it, this is a massive gamble. Skipping the CVV2 check is like leaving your front door unlocked for fraudsters who only have a stolen card number.

You also give up your best defense if a chargeback hits. Without a successful CVV2 match on record, your odds of winning an "unauthorized transaction" dispute drop dramatically. That one sale is almost never worth the high risk of fraud and the near-guaranteed loss from a chargeback.

Crucial Insight: Think of the CVV2 as a non-negotiable part of modern online security. Processing a payment without it might seem harmless in the moment, but it opens your business up to fraud you could have easily prevented and guts your ability to fight back against chargebacks.

Why Do CVV2 Codes Sometimes Wear Off?

Finally, what about customers who say their CVV2 has rubbed off from wear and tear? This is a real issue, especially with older cards that have seen a lot of use. The printed numbers can fade over time, becoming impossible to read.

If a customer runs into this, the safest and most secure path is to advise them to contact their bank for a new card. You shouldn't encourage them to guess the code or try to find a way to bypass the check. It might feel like a hassle for the customer, but it protects both of you from potential fraud if that card ever gets lost or stolen. Keeping every single transaction secure is always the right move.

This kind of vigilance is vital when you consider how damaging stolen card data can be. A prime example is the 2013 Target data breach, which exposed 40 million cards, including their CVV2 data. This single event fueled a 40% spike in chargebacks that year, costing merchants an estimated $2.5 billion. You can find more details about the impact on Chargebacks911.com.

Stop losing revenue to confusing chargebacks. ChargePay uses AI to automatically fight and win disputes for you, recovering up to 80% of lost funds without any manual work. Protect your business and boost your win rate overnight.

.svg)

.svg)

.svg)

.svg)