A bank fraud investigation is the formal process a bank kicks off to dig into suspicious transactions, figure out if they're legit, and track down the source of any funny business. It's a key part of how financial institutions protect everyone—customers and businesses alike—from financial crime. For you, as a merchant, this process usually starts when a customer disputes a charge, which then triggers a chargeback.

The Bank Fraud Investigation Process: What to Expect

Getting a notice about a bank fraud investigation can definitely be a little jarring. One minute you have a sale, the next it's being questioned and your revenue is on the line. But once you understand what's happening behind the curtain, you can trade that confusion for confidence.

Think of it like a detective's case file. An incident gets reported, evidence is gathered, and a decision is eventually made.

The whole thing almost always kicks off with an alert—usually a chargeback filed by a customer claiming a transaction was unauthorized. That's the first domino to fall. From there, the main players get involved: the customer's bank (the issuer), your bank (the acquirer), and the card network (like Visa or Mastercard).

Who's Who in an Investigation

Each party has a specific job. The customer's bank starts the process for their cardholder. Your bank is in your corner, passing the dispute notice along to you. And the card network? They're the referee, setting the rules and deadlines everyone has to play by.

Your role is to be the primary source of evidence. It's on you to prove the transaction was legitimate. The whole system is designed to create a fair—if sometimes complicated—path to resolution. If you want to dive deeper into how this works, check out our guide on the complete card dispute process.

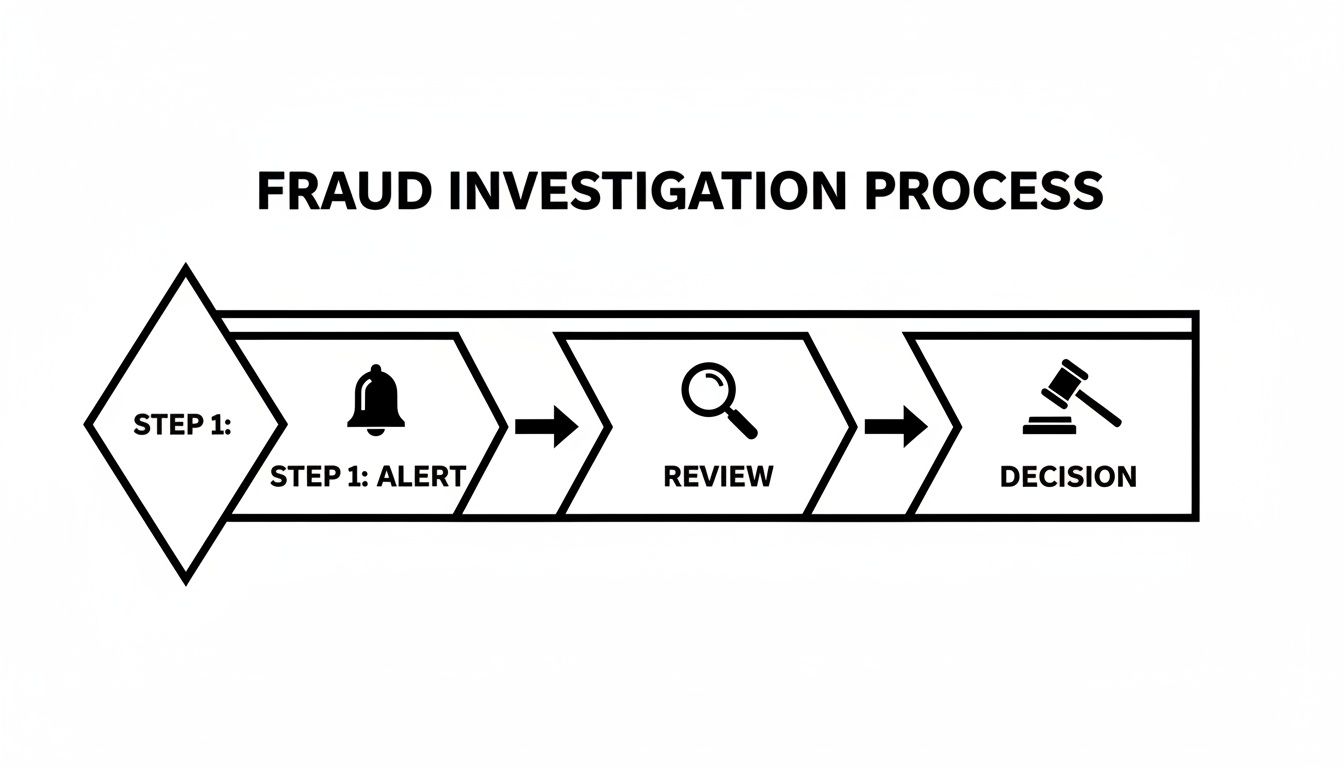

This flowchart breaks down the typical investigation into a simple three-step flow.

As you can see, the journey begins with an alert, moves into a review phase where your evidence is everything, and ends with a final decision.

Why Are These Investigations So Common Now?

Unfortunately, the need for these investigations is skyrocketing. Banks are drowning in a massive wave of fraud attempts. Financial institutions earning over $10 million a year are now dealing with an average of 2,000 fraud attempts every single month.

That's a 60% jump in reported attacks over the last year alone. To make matters worse, organized crime rings are behind nearly 75% of these incidents.

The table below gives you a quick summary of what to expect at each stage.

Key Stages of a Bank Fraud Investigation

This process might seem complex, but it's a structured way to ensure fairness. Your job is to be prepared and respond effectively.

A bank fraud investigation isn't a personal attack on your business. It's just a standard procedure in a massive system built to keep digital payments trustworthy. Your only job is to provide the facts that clearly tell your side of the story.

By understanding this roadmap, you can prepare effectively, respond with confidence, and ultimately protect your business.

Common Types of Fraud Merchants Face

To win the battle against fraud, you first need to understand the enemy. Fraud isn't a one-size-fits-all problem; it comes in many different flavors, each with its own tricks and telltale signs. For anyone running an ecommerce store, being able to spot these patterns is the first step to protecting your hard-earned revenue.

These schemes can be anything from deceptively simple to incredibly complex. Knowing the difference helps you build a stronger defense and gives you a much better shot during a bank fraud investigation.

Friendly Fraud The Accidental Culprit

One of the most frustrating types is friendly fraud, which you might also hear called chargeback fraud. This is what happens when a real customer buys something from your store, receives it, and then disputes the charge with their bank anyway.

It's not always malicious. Maybe they just didn't recognize the business name on their statement, or perhaps a family member used their card without asking. But even if they didn't mean any harm, the result is the same for you: a lost sale and a costly chargeback to deal with.

Don't let the name fool you—'friendly fraud' is anything but friendly to your bottom line. It accounts for a huge chunk of all chargebacks and requires just as much evidence to fight as a criminal attack.

This kind of dispute can feel like an uphill battle. You did everything right, but you're still stuck having to prove it. For a deeper dive, check out our guide on what friendly fraud is and how to prevent it.

Criminal Fraud More Sophisticated Schemes

Beyond those accidental disputes, you've got the deliberate attacks from criminals using stolen information. These schemes are built from the ground up to exploit any weakness they can find in the payment process.

Here are a few of the most common criminal tactics to watch out for:

- Account Takeover (ATO): This is when a fraudster gets into a legitimate customer's account on your site. They use the saved payment info to make unauthorized purchases, often having the items shipped to a totally different address.

- Triangulation Fraud: This one is a bit more complex. A fraudster sets up a fake online storefront, listing popular items at unbelievably low prices. When a customer places an order, the fraudster takes their "clean" money. Then, they use a stolen credit card to buy that same item from your store and have it shipped directly to their customer. They pocket the profit, and you're left with the chargeback when the real cardholder spots the fraudulent transaction.

- Card-Not-Present (CNP) Fraud: This is the most classic type of ecommerce fraud. Criminals simply use stolen credit card numbers to buy things online, over the phone, or through mail order. Since you don't have the physical card in hand, it's a lot harder to verify that the buyer is who they say they are.

The scale of these scams is just staggering. Globally, consumers lost an estimated $442 billion to scams in 2025, and shopping-related scams made up 54% of all reported incidents. Even though 73% of people think they can spot a scam, 23% have still lost money—a huge vulnerability for merchants. You can explore more data in the global state of scams in Feedzai's 2025 report.

Getting a handle on these different fraud types is crucial. Each one leaves a different trail of evidence and demands a unique strategy to fight back effectively. By knowing what you're up against, you can better prepare your business for the bank fraud investigation that will inevitably follow.

How to Gather Evidence That Wins Disputes

When a fraud claim lands on your desk, the first thing you feel is probably frustration. But instead of getting angry, get strategic. The best way to channel that energy is by methodically building an airtight, evidence-based case.

Winning a dispute during a bank fraud investigation isn't about arguing or pleading your case. It's about presenting undeniable, black-and-white proof that the transaction was legitimate and you held up your end of the bargain.

Think of yourself as a detective putting together a case file for a judge. The bank investigator doesn't know you, your business, or your customer. They only know what the documents in front of them say. Your job is to make that paper trail so clear and convincing that there’s no other possible conclusion.

The Foundation of Your Defense: Transaction Details

Every solid case starts with the fundamentals. This is the first layer of proof you’ll present, and it sets the stage by proving a real transaction occurred through the proper channels. It's your opening statement, establishing a legitimate customer interaction from the get-go.

Start by gathering all the basic transaction records. This shows the bank that a real order was placed and processed correctly.

Here’s what you absolutely must have:

- Transaction Receipt: A copy of the digital or physical receipt showing the date, time, and amount charged. This is non-negotiable.

- Order Details: A screenshot or export from your e-commerce platform (like Shopify or PayPal) that details exactly what the customer purchased.

- AVS and CVV Match Results: This is huge. Showing that the Address Verification System (AVS) and Card Verification Value (CVV) checks were successful proves you took the right steps to verify the cardholder. While a mismatch can be a red flag, getting a solid match is powerful evidence in your favor.

This first batch of evidence confirms the "what, where, and when" of the purchase, creating a baseline of legitimacy for the investigator to build on.

Building Your Case with Customer and Shipping Data

Once you’ve laid the foundation with the transaction basics, it's time to connect that purchase to the person who received the goods or services. This is where you prove you delivered on your promise and show the cardholder was directly involved.

This part of your evidence file closes the loop. It links the digital purchase to a physical delivery or an online interaction, directly countering common claims like "I never got the product" or "my card was stolen."

For instance, any data you have that ties the order to the customer's known information helps build a powerful narrative.

An IP address that matches the cardholder’s billing address is one of the most compelling pieces of evidence you can provide. It strongly suggests the legitimate owner of the card placed the order from their home or another familiar location.

Here’s a checklist of compelling evidence to pull together:

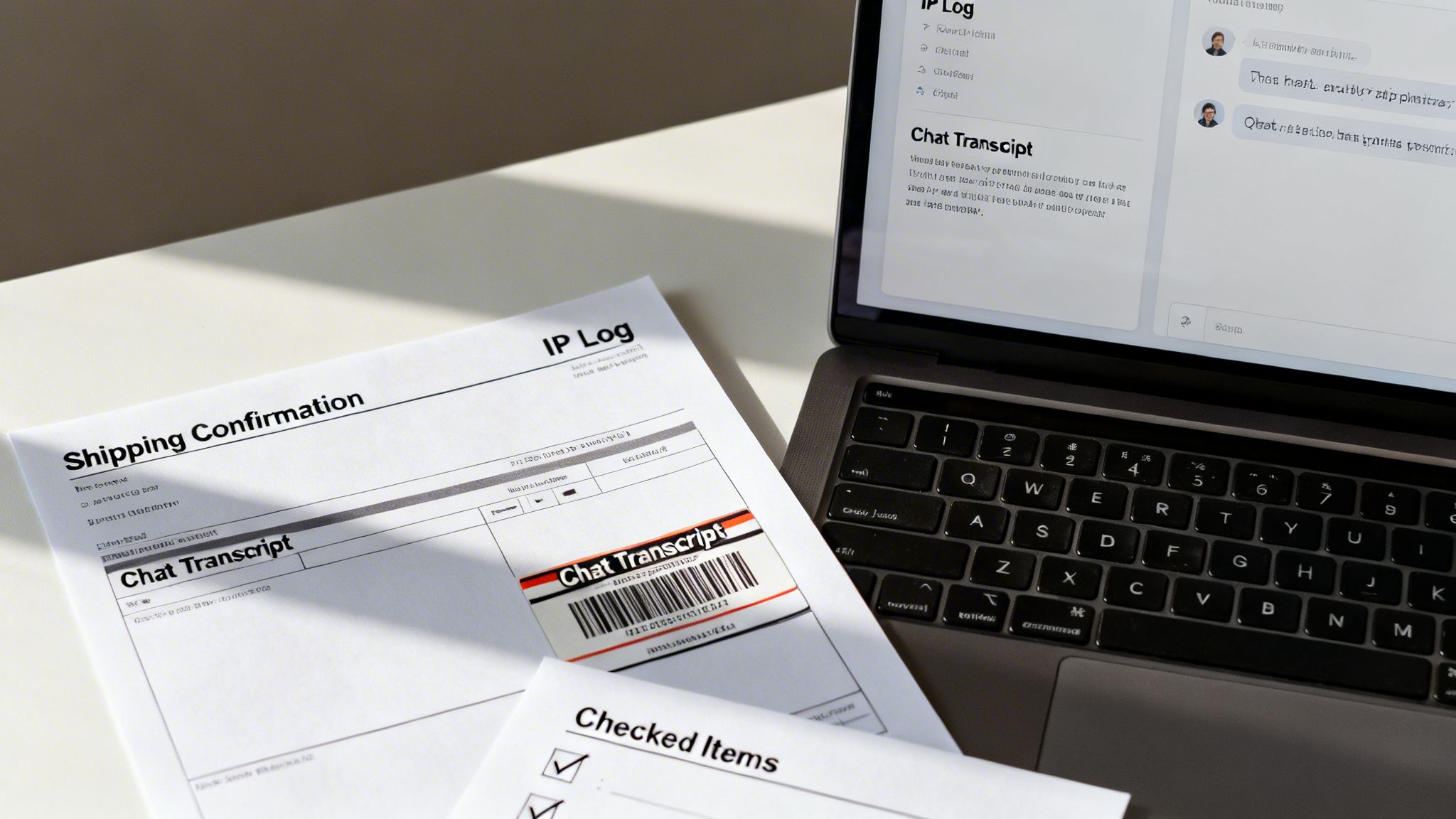

- IP Address Logs: The IP address used to place the order. If it matches the billing address city and state, make sure to point that out clearly.

- Shipping Confirmation and Tracking: For physical products, this is your smoking gun. Provide the tracking number and a direct link to the carrier’s website showing proof of delivery. A signed delivery confirmation is even better—it’s gold.

- Customer Communications: Dig up any emails, live chat transcripts, or support tickets related to the order. If the customer contacted you about their purchase before the dispute, it proves they were well aware of the transaction.

- Account History: If the customer has an account with your store, provide their order history. A pattern of previous successful purchases makes a one-off fraud claim look incredibly suspicious.

Each document adds another layer to your story, making it harder and harder for the bank to side with a baseless claim. When you're ready to pull this all together, our article on creating an example of a rebuttal letter can give you a solid template. Remember, presenting this information in a clear, organized way is just as important as the evidence itself.

Communicating Effectively with Banks and Card Networks

When you get hit with a bank fraud investigation, how you respond is just as important as the evidence you pull together. Just dumping a folder of documents on an investigator won't cut it. Your communication with the bank and card network has to be fast, clear, and professional.

Put yourself in their shoes for a second. The person on the other end is juggling dozens, maybe even hundreds, of cases just like yours. You have a tiny window to get their attention and tell a story that makes sense. A messy, confusing response makes it incredibly easy for them to just side with their cardholder and move on.

But a well-structured and persuasive rebuttal? That tells a clear story backed by solid facts. This approach doesn't just up your chances of winning the dispute; it also helps you maintain a good relationship with your financial partners.

The Golden Rule: Act Fast and Never Ignore a Request

The single worst thing you can do during a bank fraud investigation is… nothing. Ignoring a dispute request is an automatic loss, plain and simple. The clock starts ticking the second you’re notified, and those deadlines are non-negotiable.

Responding quickly shows you're an engaged and responsible merchant. It signals to the bank that you take this stuff seriously and have your act together. Any delay can look like disorganization or, even worse, like you know you're at fault.

When a bank sends a request for information, they're handing you a chance to defend your revenue. Ignoring it is like forfeiting the game before it even starts. Treat every single deadline like it's set in stone.

Your goal should be to get your evidence package submitted well before the final due date. This gives you a buffer to double-check everything and sidestep any last-minute technical hiccups.

Evidence Is Your Best Defense

When it comes to fighting a fraud claim, the quality of your evidence is everything. A strong paper trail can be the difference between winning and losing. You need to gather documentation that proves the transaction was legitimate and the cardholder participated.

Here is a quick checklist of the most compelling types of evidence you can provide to an investigator.

Having these documents organized and ready to go will make your response process much smoother and far more effective.

How to Structure Your Response for Maximum Impact

Organizing your evidence logically is the key to building a case that's easy to win. Don't just attach a bunch of files and hope for the best. You need to craft a narrative that walks the investigator through the transaction from beginning to end.

A winning response should always start with a concise rebuttal letter that summarizes your side of the story and points to the specific evidence you’ve attached. Think of this letter as a road map for the investigator.

Here are the essential pieces to include:

- A Clear Summary: Kick things off with a simple paragraph stating that you are disputing the chargeback and believe the transaction was completely legitimate. Be sure to include the transaction date, amount, and order number.

- A Chronological Story: Lay out the sequence of events. For example: "The customer placed their order on [Date] from an IP address in [City, State], which matches their billing address. The AVS and CVV checks both came back successful. We shipped the item on [Date] via [Carrier] with tracking number [Tracking #], and it was delivered and signed for on [Date]."

- Evidence Callouts: Directly reference each piece of evidence you’re providing. For instance, "Please see Attachment A for the full order receipt and Attachment B for the signed delivery confirmation from FedEx."

- A Professional Closing: Wrap it up with a polite but confident statement that reaffirms the charge was valid.

This structured approach makes the investigator's job a whole lot easier, which can only help your cause. It turns a random pile of files into a coherent, persuasive argument that shows you’re a professional and makes your case much, much stronger.

Using Automation to Streamline Your Defense

Let's be honest, manually fighting every fraud claim is a soul-crushing time suck. What starts as a manageable task can quickly spiral into a full-time job as your business grows. This is exactly where technology can step in and offer a smarter, more efficient way to handle the relentless pressure of bank fraud investigations.

Automating your defense isn't just about speed. It’s about putting systems in place that are built to be more precise, consistent, and analytical than even the most dedicated person on your team. These tools work around the clock, so you never miss a deadline or overlook a crucial piece of evidence again.

How Automation Transforms Your Dispute Process

Think of an automated system as your own fraud investigation specialist. The moment a new dispute hits your account, it gets to work. Instead of you frantically logging into Shopify, digging through your payment processor's records, and hunting for shipping confirmations, the software pulls it all together in seconds.

AI-powered tools can instantly analyze the dispute's reason code, gather all the necessary evidence from your different platforms, and assemble a professional response tailored to that specific bank and card network's requirements. This frees you up to focus on what actually moves the needle—growing your business.

By automating the repetitive, data-gathering part of a bank fraud investigation, you shift from a reactive scramble to a proactive, strategic defense. The system handles the grunt work, so you can handle the business.

This kind of automation builds a standardized, high-quality response every single time. It ensures no steps are missed and that your evidence is always presented in the most compelling way possible, which can seriously improve your chances of winning.

Going Beyond Speed with Intelligent Insights

The real magic of automation is its ability to spot patterns a human might easily miss. An AI system can analyze thousands of data points from past disputes—both yours and others—to figure out what kind of evidence works best for different types of claims. It learns, adapts, and fine-tunes its strategy over time.

For example, it might notice that for disputes from a certain bank, including IP address geolocation data leads to a 15% higher win rate. A person might never catch such a subtle trend, but for an AI, it’s just another data point to build into its next response. To further enhance your defense against fraud, consider leveraging modern solutions like workflow automation.

This data-driven approach is becoming non-negotiable. The 2025 Global eCommerce Payments and Fraud Report points out that e-commerce scams are the most common type of fraud by sheer volume. To fight back, 15% of banks globally are already using data analytics and machine learning to spot weird activity. When you adopt the same tech, you're just leveling the playing field. You can read more about the latest trends in the MRC Global Payments and Fraud Report.

By automating your chargeback responses, you can start reclaiming lost revenue and protecting your business's bottom line. You can learn more about how this works in our complete guide to automated chargeback and dispute management using AI.

Proactive Strategies to Prevent Future Fraud

Winning a dispute is great, but preventing it from happening in the first place? That’s the real victory. While a solid defense during a bank fraud investigation is essential, the ultimate goal is to make your business a much harder target for criminals. A proactive, multi-layered security strategy is your best bet for keeping your revenue safe and your chargeback rates down.

Think of it like securing your home. You don’t just lock the front door and call it a day. You also close the windows, set an alarm, and maybe even add a camera. Each layer makes a break-in that much tougher, and the same logic applies to protecting your online store.

Building Your Multi-Layered Defense

Relying on a single security measure just doesn't cut it anymore. The most effective strategies combine several tools and practices that work together, creating a net that flags suspicious activity before it ever turns into a financial loss.

Here are a few essential layers every merchant should have in place:

- Require CVV and AVS Checks: This is non-negotiable. The Card Verification Value (CVV) confirms the customer physically has the card, while the Address Verification System (AVS) checks that the billing address matches what the bank has on file. They aren't foolproof, but they stop a huge amount of low-level fraud.

- Use Fraud Scoring Tools: Many payment gateways offer tools that analyze hundreds of data points for each transaction in real-time. They look at things like IP geolocation, the age of an email address, and past buying habits to assign a risk score. This lets you automatically flag or block high-risk orders.

- Set Up Transaction Alerts: Configure your systems to ping you when something unusual happens. This could be multiple failed payment attempts, a sudden spike in orders from one IP address, or orders where the billing and shipping addresses don't match. Catching these red flags early gives you a chance to review the order before it ships.

A proactive fraud prevention strategy isn't about blocking every sale that looks a little off. It's about having the right information to make smarter decisions—stopping clear-cut fraud while letting legitimate customers shop without any friction.

The Power of Clear Customer Communication

Not all chargebacks are malicious. A surprising number start with a simple misunderstanding, often leading to friendly fraud. This is where clear, consistent communication becomes one of your most powerful prevention tools. A well-informed customer is far less likely to file a dispute out of confusion.

Put yourself in their shoes. An unfamiliar charge on their statement can cause instant panic. By making sure your communication is crystal clear from the get-go, you can head off these issues before they even start. Our guide on eCommerce fraud prevention best practices dives even deeper into these strategies.

Here’s how to use communication to your advantage:

- Send Detailed Confirmations: Right after a purchase, send an email with an itemized list of what they bought, the total amount charged, and your store’s name exactly as it will appear on their credit card statement. This little detail is huge.

- Provide Shipping Updates: Send a notification when the order ships, complete with a tracking number and a direct link to the carrier’s site. Follow up with another email to confirm delivery. This builds a clear paper trail and keeps customers in the loop.

By combining robust technical defenses with thoughtful customer communication, you build a powerful shield around your business. You won’t just reduce the number of disputes you have to fight; you’ll also create a safer, more trustworthy experience for all your legitimate customers.

Frequently Asked Questions About Bank Fraud Investigations

Getting hit with a bank fraud investigation can feel overwhelming, especially if it's your first time. You've got questions, and getting straight answers is the first step to feeling in control. Let's tackle some of the most common questions we hear from merchants.

How Long Does a Bank Fraud Investigation Take?

Patience is a virtue here. A typical investigation can take anywhere from 30 to 90 days from start to finish. The exact timeline really depends on the complexity of the case, how quickly everyone responds, and the specific rules of the banks involved.

But here’s the critical part for you: your window to act is much, much shorter. As a merchant, you'll usually get between 7 and 21 days to pull together all your evidence and submit your response. After that, it's a waiting game while the issuing bank reviews everything and makes its decision.

Can I Lose Money Even If I Prove a Transaction Was Legitimate?

Unfortunately, the answer is yes. It's a tough pill to swallow, but even with ironclad proof, the cardholder's bank has the final say. They often lean toward protecting their customer, especially in those frustrating "friendly fraud" cases where the real cardholder is making a false claim.

That said, don't throw in the towel. A clear, well-organized response with compelling evidence makes it significantly harder for a bank to side against you. Your goal is to make your case so strong that they can't ignore the facts.

What Happens If I Get Too Many Fraud Chargebacks?

This is where things can get serious. If your chargeback numbers creep over the thresholds set by card networks like Visa and Mastercard (usually around 0.9% of your transactions), you'll land on their radar.

First, you could be placed into a high-risk monitoring program. Think higher fees, more paperwork, and intense scrutiny of your business. If you can't get the rate down, you run the very real risk of having your merchant account shut down completely. Losing the ability to take card payments can be a business-killer, which is why managing fraud and disputes proactively is absolutely essential.

For those trying to navigate specific P2P scams, this Zelle scam refund guide offers some great advice on potential recovery paths.

Stop losing revenue to fraudulent chargebacks. ChargePay uses AI to automate the entire dispute process, gathering evidence and generating winning responses to recover your money for you. See how much you can reclaim at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)