You open Shopify in the morning, scan orders, and then see the alert you hate most. A customer disputed a payment on an order that looked completely normal. The package shipped on time. Tracking shows movement. Support didn't get a complaint. Yet now the money is frozen, your team has work to do, and you're stuck proving that a real order was real.

That's the part most articles miss. Payment processor fraud isn't only about stolen cards or bad actors. It's also about the daily operational mess it creates for honest merchants. Someone on your team has to review the order, pull screenshots, find tracking, check customer emails, match policy pages, and submit a response before the deadline. If you're the operator, that “someone” is usually you.

I've seen this drain stores more than the fraud loss itself. The sale goes bad once. The admin pain keeps going.

That Sinking Feeling When a Good Sale Goes Bad

A lot of chargebacks don't start with a sketchy order. They start with an order you'd approve again if you saw it fresh.

The billing details look fine. The customer gets confirmation emails. Fulfillment goes out fast. Then the bank reversal hits. Now you're not asking, “Was this order legit?” You're asking, “How much time is this going to eat today?”

That's why payment processor fraud feels so frustrating. It doesn't just take revenue. It hijacks your attention. It breaks your workflow. It forces you to stop merchandising, marketing, inventory planning, or customer support so you can become a part-time dispute analyst.

Good merchants lose disputes every day because they don't have time to build a strong case, not because the order was actually fraudulent.

For Shopify operators, this gets old fast. One dispute becomes a pattern. A pattern becomes a weekly cleanup job. Then your processor starts watching your account more closely, and what started as a fraud problem turns into an operations problem.

You can't run a healthy store if every disputed order becomes a manual investigation.

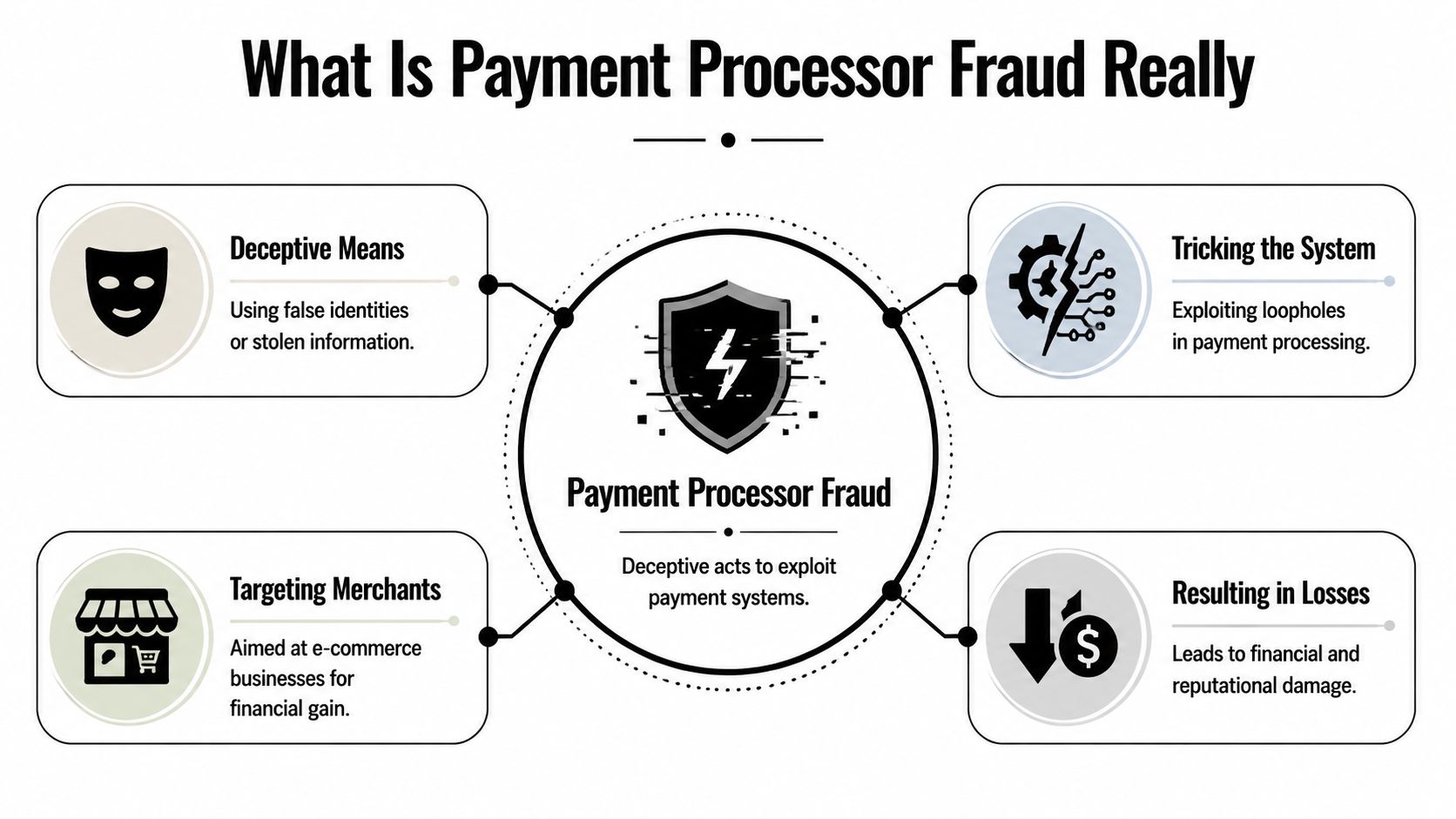

What Is Payment Processor Fraud Really

Payment processor fraud is any deceptive activity that manipulates the flow of payment data or money so that a merchant, processor, bank, or customer takes the loss. In plain English, someone fakes part of the transaction and your store deals with the fallout.

Think of a card payment like a digital handshake. The customer says, “I'm authorized to use this payment method.” The bank says, “I approve this transaction.” The processor passes the message between both sides and helps move the money. Fraud happens when one side of that handshake is false, stolen, manipulated, or impersonated.

Where the transaction breaks

At a basic level, every online payment has a few moving parts:

- The customer submits payment details.

- Your store sends the order and payment request.

- The processor routes and evaluates the transaction.

- The bank or card issuer decides whether to approve it.

If you want the simple mechanics behind that flow, this guide on what a payment processor does is worth reading.

Fraud can enter at several points:

- Stolen credentials get used at checkout.

- Fake identities open accounts or place orders.

- Compromised checkout pages skim payment details.

- Dishonest buyers use the chargeback system after receiving goods.

The fraud ecosystem behind your chargebacks

This isn't a small, isolated problem. Recorded Future reported that 269 million card records and 1.9 million stolen U.S. bank checks were posted on dark and clear web platforms in 2024, and nearly 11,000 unique e-commerce domains were hit by Magecart e-skimmer infections, roughly a threefold increase from 2023. The same report also identified about 1,200 scam domains linked to fraudulent merchant accounts, which shows how broad the ecosystem has become for merchants and processors alike (Recorded Future payment fraud intelligence report).

That matters because stolen data doesn't stay abstract for long. It shows up in your store as failed authorization attempts, suspicious card-not-present orders, post-purchase disputes, and support tickets from confused real customers.

Practical rule: If your team only thinks about fraud at the moment of checkout, you're already too late. The damage often starts long before the order reaches your store.

The Four Faces of Fraud You Will Encounter

Most Shopify merchants don't face just one type of payment processor fraud. They deal with a rotating mix of abuse patterns. Some are obvious. Some are annoying. Some look exactly like normal orders until the dispute lands.

Card-based payments remain a prime target. In the EU/EEA, fraudulent card transactions totaled EUR 1.3 billion in 2024, with a fraud rate of 0.033%. The rate may look small, but the value and transaction volume make card fraud a major operational risk for merchants processing card payments (EBA and ECB payment fraud report).

Classic criminal fraud

This is often the first version imagined. A fraudster gets stolen card details and uses them to place orders before the cardholder or issuer shuts the card down.

You'll often spot this through pattern mismatch. Overnight orders. Rush shipping. Different billing and shipping details. Multiple attempts with slightly changed card data. Expensive, easy-to-resell products.

This kind of fraud is noisy when the attacker is sloppy and expensive when they aren't.

Friendly fraud

This is the one merchants hate most because it feels personal. The cardholder places the order, receives the item, and later disputes the charge anyway. Sometimes they forgot the purchase. Sometimes a family member used the card. Sometimes they know exactly what they're doing.

A common example is “item not received” even though tracking shows delivery. Another is “unauthorized purchase” after the customer used the same email, same device, and same shipping address they've used before.

If you need a sharper breakdown, this guide on friendly fraud and chargeback abuse covers the pattern well.

Merchant identity fraud

Some bad actors don't target stores. They create fake stores.

They use fraudulent merchant accounts to test stolen cards, process sham transactions, or move illicit money through a storefront that looks just real enough to pass initial checks. Legitimate merchants feel the impact indirectly when processors tighten underwriting, hold funds, or increase scrutiny across the board.

Account takeover

This sits in a nasty middle ground. The fraudster doesn't need a stolen card if they can get into the customer's real account. Once inside, they can use saved payment methods, loyalty balances, or trusted shipping details to make the order look clean.

That's why some of the hardest fraud cases aren't new-customer orders at all. They're repeat-customer accounts that were compromised undetected.

The True Cost Is More Than Just the Lost Sale

Merchants make a mistake when they treat a chargeback as a revenue write-off and move on. The sale amount is only the first layer of damage. The primary hit is operational.

A disputed order creates work across support, fulfillment, finance, and whoever owns the payment stack. It also leaves your processor with one more reason to classify your account as risky.

What the loss actually includes

Even without attaching a fixed amount to every store, the pattern is consistent:

- Lost revenue: The original sale is in dispute or reversed.

- Lost product cost: You already paid for inventory or production.

- Lost shipping and fulfillment effort: The parcel still moved.

- Chargeback fee exposure: Processors commonly assess dispute-related fees.

- Internal labor: Someone has to gather evidence and respond.

If you want the processor side of that expense explained clearly, this article on how chargeback fees work is useful.

The hidden drain merchants underestimate

The biggest blind spot is time. Chargebacks rarely arrive when your team has spare capacity. They show up during launches, stock issues, ad swings, and support spikes.

A single dispute forces you to answer questions like these:

| Operational task | What your team has to do |

|---|---|

| Order review | Check risk flags, payment details, and order timeline |

| Evidence gathering | Pull tracking, delivery proof, customer emails, and policy screenshots |

| Response drafting | Match evidence to the bank's dispute reason |

| Deadline management | Submit on time and track status updates |

| Processor monitoring | Watch for patterns that could trigger account scrutiny |

This is why payment processor fraud wears teams down. It creates admin debt. The store keeps selling, but your back office keeps bleeding time.

The merchant who spends hours each week defending legitimate orders is paying a fraud tax, even before the outcome is decided.

There's another risk. U.S. regulators and banking guidance treat processors as higher-risk intermediaries and recommend monitoring merchant return rates, merchant activity, and suspicious patterns because unusually high returns or unauthorized debits can signal fraud or attempts to evade network limits (FFIEC guidance on processor risk).

So even if you can absorb some losses, your processor may not tolerate the pattern forever.

Your Practical Playbook for Detection and Prevention

Fraud prevention works when you stop looking for one perfect filter and start building layers. That's how processors do it, and merchants should think the same way.

Modern fraud systems typically combine velocity checks, device and behavioral signals, and rule-based controls such as AVS and CVV validation because each layer blocks a different attack path and helps reduce false negatives when used together (layered payment fraud controls).

Build a layered checkout defense

Start with the controls closest to the transaction:

- AVS checks: Compare the billing address entered at checkout against issuer records.

- CVV validation: Catch a chunk of low-effort stolen-card attempts.

- Velocity rules: Flag repeated attempts from the same card, email, device, or IP pattern in a short window.

- Device signals: Look for mismatched environments, suspicious repeat behavior, or automation patterns.

None of these tools is magic on its own. Together, they force fraudsters to beat several checks at once, and most won't bother.

Tighten the parts merchants ignore

A lot of disputes are easier to fight, or avoid, when the store itself is cleaner.

Use this checklist:

- Clear policy pages: Make your shipping, return, refund, and cancellation terms easy to find before purchase.

- Consistent descriptors: Make sure your billing descriptor matches what customers will recognize on statements.

- Order communication: Send confirmation, shipping, and delivery updates that create a clean record.

- Manual review triggers: Hold orders with unusual combinations, such as high value plus expedited shipping plus address mismatch.

- Account security: Require stronger login protection for customer accounts with stored payment methods.

For a broader operational view, this piece on preventing fraud in corporations is a useful reminder that fraud control is partly a systems problem, not just a checkout problem.

Prepare for the disputes you won't prevent

Even a strong setup won't stop every case. Some fraud is authorized, manipulated, or only becomes visible after settlement. The Faster Payments Council reported in 2024 that fraud tied to faster payments is rising with adoption, and identified account takeover, social engineering, and stolen credentials as the most common consumer fraud types in that environment (Faster Payments Council fraud bulletin).

That matters because user-initiated fraud can slip past classic card filters. Merchants need records that stand up later.

Keep these ready:

- Proof of delivery

- Customer communication history

- Order metadata from Shopify

- Policy acceptance evidence

- Any prior purchase history tied to the same customer

For a more complete merchant-focused framework, read this guide on ecommerce fraud prevention.

Navigating Processor Rules and Legal Considerations

Processors aren't strict because they enjoy making life harder for merchants. They're strict because they sit under regulatory pressure, card network rules, and banking oversight. If your account starts showing unusual dispute or return patterns, they have to care.

That's why payment processor fraud becomes your problem even when you didn't cause it. The processor sees risk at the portfolio level. If your store starts producing too many bad signals, they may add reserves, increase scrutiny, or restrict activity.

Why processors watch merchants so closely

FinCEN and related U.S. banking guidance treat payment processors as higher-risk intermediaries. The concern isn't only stolen cards. It includes fraud schemes, identity theft, illicit transactions, suspicious merchant activity, and unusual return patterns.

From the merchant side, this means one thing. You cannot treat disputes as random noise. Processors often read patterns as indicators.

A few warning signs they care about:

- High return or dispute activity

- Sales patterns that don't fit your normal profile

- Unauthorized debit complaints

- Merchant behavior that suggests rule evasion

What strong evidence actually looks like

Banks don't care that you “know” the order was good. They care whether the file shows it.

Good evidence is organized, relevant, and tied to the exact claim. If the cardholder says the item wasn't delivered, provide delivery proof and communication. If they say the transaction was unauthorized, show account history, address consistency, prior successful orders, login data when available, and order timeline details.

Weak evidence loses for two reasons. It's either incomplete, or it doesn't answer the claim the bank is reviewing.

Build your dispute files like you're handing them to someone who knows nothing about your store. Because you are.

That means:

- Chronology first: Show the sequence from order to delivery.

- Policy support: Include the terms active at the time of purchase.

- Customer recognition signals: Match names, email addresses, devices, or repeat-order behavior where available.

- Readable formatting: Don't dump screenshots without labels.

The merchants who win consistently usually aren't more emotional. They're more organized.

The Smart Way to Automate Your Fraud Defense

Manual chargeback handling is a bad use of operator time. It's repetitive, deadline-driven, and easy to get wrong when you're juggling the rest of the business. That's why automation matters. Not because it sounds modern, but because humans have better things to do than rebuild the same dispute packet over and over.

If you're still managing chargebacks from inbox alerts and scattered Shopify notes, you're running an expensive workaround.

What automation should actually remove

A good system should take these jobs off your plate:

- Evidence collection: Pull order details, tracking, communication, and policy records from the right systems.

- Reason-code matching: Build the case around the actual dispute claim.

- Submission workflow: Keep deadlines from slipping.

- Pattern tracking: Surface repeat abuse instead of treating every dispute like a standalone event.

That's the shift merchants need. Chargeback handling shouldn't live as tribal knowledge inside one overworked team member's head.

There's also a compliance angle. Strong security controls upstream reduce the mess downstream. If your team needs a practical reference point, this checklist of actionable PCI DSS steps is a useful companion to tighter payment operations.

Why AI changes the workload equation

AI is useful here because disputes follow patterns, but each case still needs a customized response. That's exactly the kind of work that drains people and suits automation.

A solid AI dispute workflow can review the dispute reason, identify the evidence that matters, draft a structured representment, and submit on time without your team assembling the file manually every single time. The payoff isn't only recovered revenue. It's fewer context switches, fewer missed deadlines, and fewer nights spent combing through order timelines.

For a deeper look at that process, this guide to automated chargeback and dispute management using AI lays it out well.

Here's a quick walkthrough of what that looks like in practice:

The point isn't to add another dashboard to babysit. The point is to remove a recurring operational burden before it spreads into finance, support, and founder time.

When merchants talk about fraud, they usually focus on the bad order. I'd focus on the bad workflow. Fix that, and you stop paying for the same problem twice.

Chargebacks don't have to keep stealing revenue and attention from your team. ChargePay is built for Shopify merchants and automatically handles the dispute lifecycle from alert to resolution. It has a 92.4% win rate, has handled 200K+ disputes, and recovered $10.8M+ for merchants. It also has a 4.9-star rating on the Shopify App Store and a Built for Shopify badge. You only pay when it wins. If you're ready to stop treating payment processor fraud like a permanent admin burden, install ChargePay from the Shopify App Store.

.svg)

.svg)

.svg)

.svg)