You approve an order that looks clean. Billing and shipping match. The cart size is healthy. The customer doesn't trip any obvious alarms in Shopify. Then a few weeks later, the dispute hits, and the reason code barely matches what happened.

That's the kind of fraud that drains margin because it wastes inventory, ad spend, fulfillment cost, and your time. It also creates the worst kind of uncertainty. You can't tell if you made a bad judgment call or if someone built a fake customer profile that was designed to look normal from the start.

Synthetic identity fraud sits right in that blind spot. It sounds like a banking problem, but for Shopify merchants it often shows up as unauthorized purchases, friendly-fraud-looking disputes, and chargebacks that are hard to fight without solid evidence.

That Perfect Order That Ended in a Chargeback

You've probably seen this order before.

A first-time customer buys a few high-demand items. The address passes a quick smell test. The email isn't outrageous. The card authorizes. Nothing looks sloppy. You ship it because holding good orders hurts conversion and customer experience.

Then the cardholder disputes it.

Sometimes it comes through as fraud. Sometimes it looks more like a customer complaint than a stolen-card event. Either way, you're left with the same problem. The goods are gone, the revenue is frozen or reversed, and you still paid to acquire and ship the order.

Why these orders feel so hard to catch

Synthetic identity fraud doesn't behave like the obvious scams most merchants expect. You're not always dealing with a stolen identity used in a reckless way. You're often dealing with a carefully assembled identity that was built to survive basic checks.

That's why these cases are so frustrating. The fraudster wants the order to look boring.

Practical rule: If an order looks clean at a glance but feels oddly incomplete when you zoom in, trust that instinct and review it.

For Shopify merchants, this matters because the end result usually isn't some abstract bank loss. It's a chargeback on your store. If you need a refresher on the common paths that lead to disputes, this breakdown of why chargebacks happen on Shopify is worth keeping handy.

What a busy store owner should do next

Stop treating every confusing chargeback like random bad luck. Patterns exist. When a customer identity is fabricated well enough to pass normal checks, the job isn't just “block fraud at checkout.” The job is to identify clusters of weak signals before the order ships and to preserve enough evidence to respond if the dispute lands later.

That's the playbook that protects revenue.

What Is Synthetic Fraud and Why Is It Costing You Money

Synthetic fraud is a made-up identity built from mixed parts. Think of it as a Frankenstein customer profile. One piece may be real, like a legitimate personal identifier. Other pieces are fabricated, swapped, or controlled by the fraudster, such as the email, phone number, address details, or supporting profile data.

The dangerous part is patience. Fraudsters don't always rush. They can build credibility first, then use that identity to get payment instruments or account access that looks trustworthy enough for a merchant checkout flow.

How the money leaves your business

Here's the merchant version of the attack:

- A fraudster creates or matures a synthetic identity.

- That identity gets attached to a card or payment account that can pass basic screening.

- The fraudster places an order on your Shopify store.

- You fulfill it.

- The transaction later turns into a dispute, reversal, or loss event.

You don't need to be a lender to get hit. You just need to be the merchant who ships the order.

A lot of store owners underestimate the scale because they only see their own dispute queue. But the broader exposure is huge. Plaid's summary of TransUnion data says U.S. lenders faced $3.3 billion in potential losses from synthetic identities across credit cards, auto loans, personal loans, and retail cards at the end of 2024, an all-time high since tracking began in 2009. The same summary says Javelin's 2025 Identity Fraud Study reported nearly $27.2 billion in overall identity fraud losses in 2024, up 19% year over year.

Why synthetic identity fraud prevention matters at checkout

Most Shopify stores don't control the customer's upstream credit profile. But you do control whether a suspicious order gets approved, reviewed, delayed, or canceled before fulfillment.

That's why synthetic identity fraud prevention for e-commerce has to focus on transaction-level judgment, not just bank-grade onboarding. It also needs to work with conversion, not against it. If you're improving checkout flow and fraud screening at the same time, this piece on aligning your Shopify buying journey is a useful complement because a cleaner journey makes unusual behavior easier to spot.

The biggest merchant mistake is assuming a passed authorization means a trustworthy customer. It doesn't.

What this means in plain terms

Synthetic fraud costs you money in four ways:

| Loss area | What happens |

|---|---|

| Inventory loss | You ship goods you probably won't recover |

| Chargeback loss | Revenue gets reversed after fulfillment |

| Operational drag | Your team spends time reviewing, documenting, and replying |

| Risk spillover | Too many disputes can create processor pressure and more friction later |

That's why this isn't a niche fraud topic. It's a margin problem.

Spotting the Ghost in Your Order Queue

Most synthetic fraud won't announce itself. You catch it by noticing combinations that don't belong together.

That's also why relying on one score inside Shopify is risky. According to Thomson Reuters' summary of Federal Reserve white paper research, conventional identity-fraud models failed to flag 85% to 95% of potential synthetic-identity applicants. If those models miss that much, your store needs cross-checks that go beyond “Shopify said medium risk.”

Red flags in the order itself

Start with the details the customer typed.

- Oddly polished but generic identity data. The name looks common. The email looks plausible. But together they feel manufactured, especially if the inbox format is generic and the customer has no visible history with your brand.

- High-value first order. A brand-new buyer goes straight for easy-to-resell items, rush shipping, or a basket that's larger than what your normal first-time customer buys.

- Shipping destination that needs scrutiny. Freight forwarders, mail drops, vacant-looking buildings, and addresses that don't fit the buyer profile deserve a second look.

- Multiple attempts before the “successful” order. Failed payment attempts, repeated checkouts with tiny variations, or several cards tried in a short window all matter.

Red flags in the customer profile

Fraudsters often build just enough profile data to pass.

| Signal | Why it matters |

|---|---|

| New customer with no prior engagement | There's no relationship history to support the order |

| Thin contact footprint | Brand-new looking email or phone details can signal control by the fraudster |

| Mismatch between identity and behavior | The profile says stable customer. The order behavior says smash-and-grab |

A genuine customer can trigger one of these. The problem is the cluster.

If you see two or three weak signals lining up, stop trying to talk yourself out of them. Review the order before you ship.

For stores that want a practical response after detecting repeat suspicious behavior, a merchant-side guide to blocking and banning fraudulent customers on Shopify can help turn ad hoc decisions into a repeatable process.

Technical clues merchants often ignore

The strongest clues are often the least glamorous.

Look for IP location that doesn't line up with the billing story. Check whether several “different” customers seem tied to the same device, network pattern, or shipping behavior. Watch for rapid-fire order timing that suggests scripted testing instead of normal shopping.

Here's a useful explainer on how fraud teams think about these patterns in practice:

A simple manual review filter

Before shipping a flagged order, check:

- Address reality. Search the destination on Google Maps. Is it residential, commercial, vacant, or a forwarding location?

- Email plausibility. Does the format look throwaway or freshly created?

- Order logic. Does the basket make sense for a real customer, or does it look optimized for resale?

- Attempt history. Were there failed AVS or CVV attempts before success?

- Data overlap. Does this order share details with past risky orders?

No single item proves fraud. That's not the point. You're looking for enough smoke to justify slowing the order down.

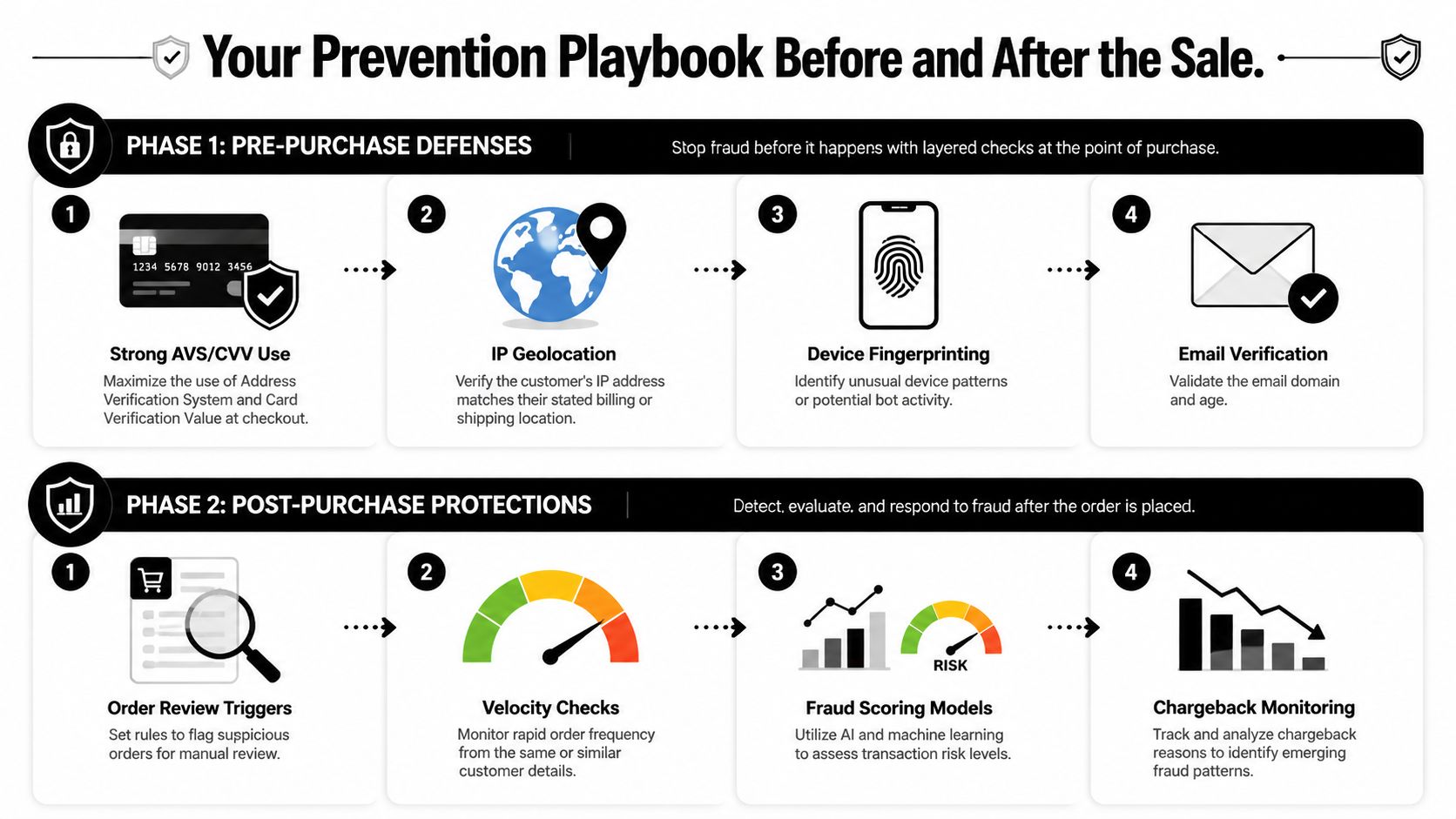

Your Prevention Playbook Before and After the Sale

Synthetic identity fraud prevention works best when you stop thinking in terms of one fraud app or one checkout rule. You need layers. Veridas puts it plainly. The most effective setup is a multi-layered pipeline with device fingerprinting, behavioral biometrics, graph analytics, and collaborative fraud feeds, because isolated point solutions miss the networked nature of synthetic identities.

That sounds technical, but the merchant version is straightforward. Add friction where it protects you. Remove guesswork where your team keeps making inconsistent decisions.

Before the sale

Your first job is to make checkout harder for bad actors without wrecking conversion for real buyers.

Tighten payment checks

Use AVS and CVV aggressively. If your gateway and market allow it, don't treat failed checks like a mild suggestion. Treat them as strong evidence that the order belongs in review or decline.

Also use 3D Secure strategically. You don't need to force it on every transaction if that hurts good customers. But for orders with increased risk signals, extra authentication can be worth the friction.

Pay attention to device and location context

A billing address in one place, an IP from somewhere unrelated, and a shipping destination that looks like a forwarding path is a bad combination. One inconsistency can be innocent. Stacked inconsistencies are where losses start.

Validate the email and the pattern, not just the card

A card can authorize while the surrounding customer footprint still looks wrong. Check for odd email construction, unusual account creation timing, repeated attempts from related details, and behavior that doesn't match a normal shopping session.

If you want a broader operating checklist, this guide to e-commerce fraud prevention best practices is a solid companion for building store-level rules.

Store-owner shortcut: Build review rules around combinations, not single events. “High order value” alone is weak. “High order value plus first-time buyer plus address inconsistency” is actionable.

After the sale but before fulfillment

Many merchants often relax their guard once the payment has gone through. This is a critical error.

Hold flagged orders briefly

A short review window can save you from shipping inventory into a guaranteed dispute. You don't need a giant risk team. You need a consistent hold-and-check routine for suspicious orders.

Do fast human checks

Use tools your team already has.

- Map the address to see whether the location makes sense.

- Search the customer details for overlap with past suspicious orders.

- Review order timing to see if several purchases hit in a burst.

- Check line items for obvious resale appeal.

Use velocity and linkage rules

Synthetic fraud often leaves traces across multiple orders. Shared device patterns, repeated addresses, recurring customer attributes, or several applications and orders tied together matter more than any single document or checkout event.

After fulfillment

Not every bad order is caught in time. When that happens, your prevention process should still help you later.

Keep clear notes on why an order was approved, reviewed, or flagged. Save fraud-analysis outputs, AVS and CVV results, customer communication, fulfillment timestamps, tracking events, and any unusual behavior you observed. That information becomes useful if the order turns into a dispute.

Good fraud prevention isn't just about stopping the shipment. It's about preserving enough evidence to make the next decision better.

Connecting Prevention to Your Daily Operations

Fraud prevention falls apart when it lives in a separate tab that nobody checks during the workday. It has to sit inside your normal Shopify operations. Checkout settings, payment review, fulfillment holds, support notes, and dispute handling all need to connect.

This matters even more with synthetic fraud because the attack often unfolds slowly. The verified data shows fraudsters often use synthetic identities to artificially inflate credit scores over 6–12 months before maxing out. It also states that data from the Federal Reserve and LexisNexis shows over 80% of new account fraud is synthetic, yet 70% of prevention tools fail to detect the subtle, long-term patterns of rapid credit building.

Put fraud controls where orders already move

Your team doesn't need a separate fraud war room. You need checkpoints.

| Operational point | What your team should do |

|---|---|

| Checkout | Route risky combinations into review instead of auto-approving |

| Payment review | Check AVS, CVV, IP mismatch, order history, and item risk |

| Pre-fulfillment | Hold suspicious orders briefly and document why |

| Support inbox | Log any odd customer contact, address changes, or urgency tactics |

| Dispute handling | Reuse the earlier fraud notes instead of starting from zero |

Don't waste the signals you already collected

A lot of merchants make the same mistake. They gather useful fraud signals before shipping, then ignore them when the chargeback arrives.

That breaks the chain.

If an order had a suspicious address pattern, repeated payment attempts, or mismatched customer details, log it clearly at the time. Later, when the bank asks for compelling evidence, your dispute response is stronger because it reflects what happened during the transaction lifecycle.

The stores that manage chargebacks well don't treat disputes as isolated events. They connect them back to the original order behavior.

That's where monitoring matters. If you want to make this operational instead of reactive, these transaction monitoring solutions for e-commerce are a useful reference point for building a review process that catches more than obvious fraud.

Make decisions faster, not heavier

You do not need a massive SOP for every order. Use a simple triage model:

- Approve fast when the order is clean.

- Review briefly when several weak signals stack up.

- Cancel confidently when the pattern clearly looks wrong.

That keeps your team focused. It also reduces the worst outcome, which is shipping a questionable order because nobody wanted to make the call.

Stop Losing Sleep Over Chargebacks with ChargePay

You're a merchant. You shouldn't have to become a full-time fraud investigator just to protect your margin.

The hard part about synthetic fraud isn't just spotting it. It's dealing with what happens after the loss. Once a dispute lands, you need the right evidence, the right framing, and the right submission timing. Otherwise even a suspicious order that you documented well can still turn into a preventable loss.

ChargePay handles that side of the job for Shopify merchants. It automatically builds dispute responses, organizes evidence, and submits representments on time so your team isn't stuck chasing screenshots, tracking events, and customer records by hand.

Why this matters for synthetic-fraud-related disputes

Synthetic identity fraud often creates messy chargebacks. The customer profile can look real enough to create doubt, but the order behavior still leaves signals. Those signals need to be pulled together into a coherent case.

ChargePay is built for exactly that operational problem. According to the publisher data provided for this article, ChargePay has a 92.4% win rate across 200K+ cases and has recovered $10.8M+ for merchants. It also has a 4.9-star rating on the Shopify App Store and carries the Built for Shopify badge.

What store owners actually get

Instead of manually fighting each dispute, merchants get a system that:

- Tracks the full dispute lifecycle from alert to resolution

- Builds evidence packages automatically using order and transaction data

- Helps identify friendly fraud patterns that would otherwise look random

- Removes deadline risk by submitting responses on time

- Aligns cost with results through a pay-per-win model

If you want the product details directly, you can review ChargePay's product page for Shopify merchants.

Good chargeback management doesn't start when the dispute arrives. It starts when the order is placed, the signals are saved, and the evidence trail stays intact.

Synthetic identity fraud prevention is still worth doing at checkout. You should tighten rules, review suspicious orders, and improve fulfillment controls. But some bad orders will get through anyway. When they do, the difference between taking the loss and recovering revenue comes down to how well you fight the dispute.

Chargebacks don't fix themselves, and synthetic fraud won't get easier to spot by guesswork alone. If you want a faster way to recover lost revenue, fight bad disputes, and take chargeback work off your team's plate, install ChargePay from the Shopify App Store. It's built for Shopify, rated 4.9 stars, and designed for merchants who want results instead of more admin.

.svg)

.svg)

.svg)

.svg)