A banking fraud investigation is just a formal way of saying financial institutions are digging into shady activities on an account. For anyone running an e-commerce store, this process is your lifeline for fighting chargebacks and clawing back revenue stolen through things like unauthorized card use, account takeovers, or even so-called "friendly" fraud.

Winning these fights really boils down to one thing: having the right evidence to prove a transaction was legitimate.

Why Banking Fraud Is a Growing Problem for Merchants

Let's be blunt—e-commerce fraud isn't just a minor hassle. It's a direct punch to your gut, financially speaking. Every bogus transaction and every chargeback eats away at your profits and sucks up time you should be spending on growing your business. For online merchants, you simply can't afford to look the other way.

Having a solid process for investigating banking fraud is non-negotiable for survival. It’s the system you lean on to push back against baseless claims and protect the revenue you worked so hard for. Without it, you're practically inviting criminals and opportunists to take your money.

The Most Common Threats to Your Store

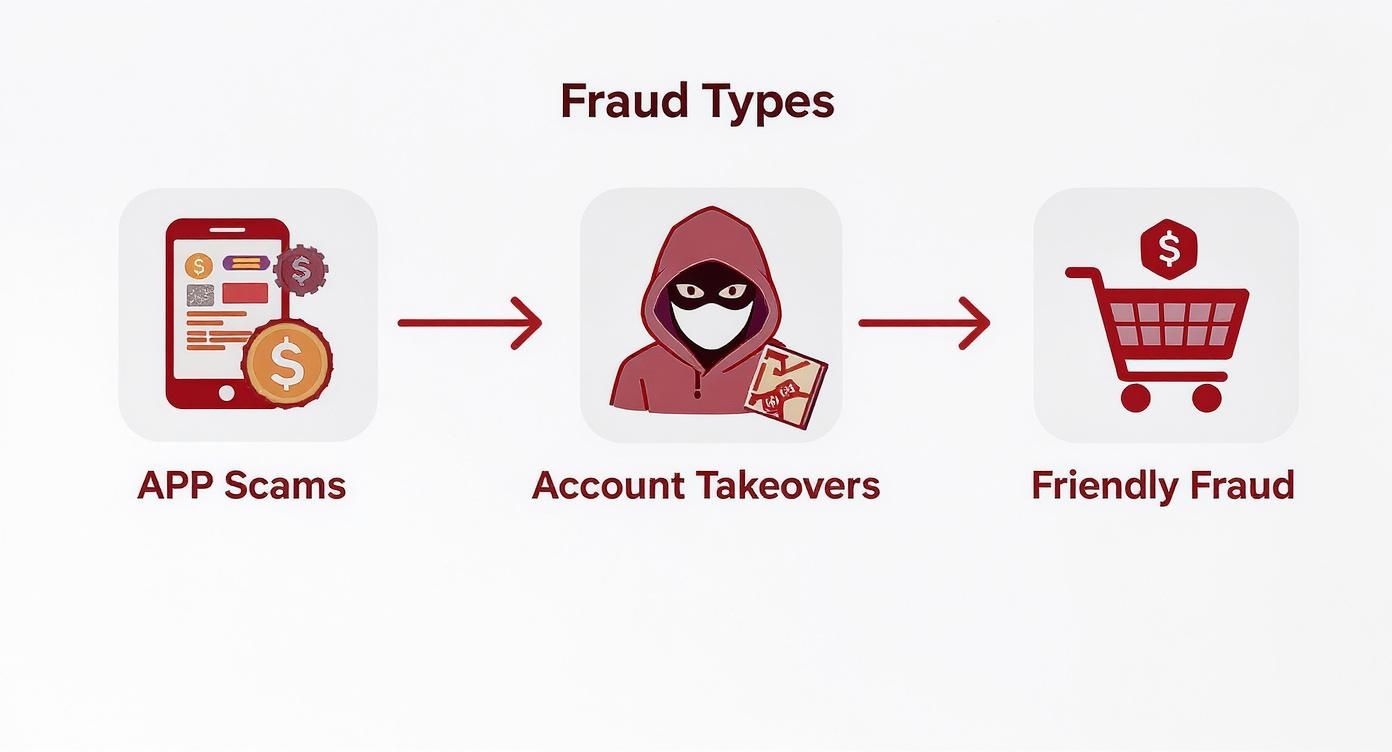

Fraud isn't a one-size-fits-all problem. E-commerce merchants get hit with a few specific schemes that can be incredibly damaging. Knowing what you're up against is the first step in building a decent defense.

- Authorized Push Payment (APP) Scams: These are especially nasty because the customer technically approves the payment. Scammers use social engineering tactics—think fake support calls or convincing phishing emails—to fool a real cardholder into sending them money. That money is then used to buy products from your store.

- Account Takeover (ATO) Fraud: This is when a crook gets into a legitimate customer's account on your site, often using credentials stolen from a data breach. Once they're in, they start placing orders with the saved payment info, leaving you and the actual customer to clean up the mess.

- Friendly Fraud: This one is probably the most frustrating. A real customer buys something, then turns around and disputes the charge with their bank. They might claim it was unauthorized or that the product never showed up. They're trying to get a freebie, and the burden of proof is on you to show the transaction was valid.

The sheer scale of this issue is hitting new highs. Globally, companies lost an average of 7.7% of their annual revenue to fraud in 2025. What’s really hitting online stores hard is the explosion in digital account takeover fraud, which shot up 21% between the first half of 2024 and the first half of 2025.

Even more alarming is the long-term view: ATO fraud has skyrocketed by a staggering 141% since 2021. That shows just how aggressively criminals are targeting online accounts.

As a merchant, you're not just selling products; you're managing risk. A banking fraud investigation isn't just about recovering a single sale—it's about defending your entire business model from sophisticated and relentless threats.

Expanding Your View of E-commerce Threats

Beyond the direct hit to your bank account, smart merchants also need to watch out for other attacks. Things like brand hijacking and counterfeit goods can poison your brand's reputation and steal sales that should have been yours.

To fight back, you can explore strategies like Amazon Brand Gating, which adds another layer of defense for your business.

Ultimately, being proactive is your best bet. By putting strong prevention and investigation processes in place, you make yourself a much harder target. You can get the full scoop on building a rock-solid defense in our comprehensive guide to e-commerce fraud prevention. This foundation is key as we get into the nuts and bolts of the investigation process in the next sections.

A Practical Framework for Investigating Fraud

When a suspicious transaction alert pings or a chargeback notice lands in your inbox, it's easy to feel a jolt of panic. But having a solid, repeatable workflow turns that chaos into a controlled process. A structured banking fraud investigation isn’t about playing detective; it’s about being methodical.

This framework breaks everything down into clear stages, helping you act quickly and effectively, every single time. It makes sure you don't miss a beat, whether you're staring down blatant criminal fraud or one of those tricky "friendly fraud" cases. Honestly, this kind of systematic approach is your best defense.

The process flows logically from one stage to the next, kicking off with identifying the problem and wrapping up with a resolution. The threats you'll face run the gamut, and each requires a slightly different focus.

As you can see, you're up against everything from outright scams and account hacks to customers trying to pull a fast one. Now, let’s get into the brass tacks of how to handle them.

Start with Smart Triage

Not every alert is a five-alarm fire. The very first thing you need to do is triage—quickly sorting alerts to figure out what needs your immediate attention. Think of it as an emergency room for your transactions.

Many fraud prevention tools assign risk scores to orders, which is a fantastic starting point. An order flagged with a 95% risk score is obviously where you should look first, not the one sitting at 5%.

If you're doing this manually, look for a combination of classic red flags:

- AVS Mismatches: The address verification system (AVS) is screaming that the billing address doesn't match what the bank has on file.

- International Orders: A sudden, high-value order shipping to a high-risk country should set off alarm bells.

- Proxy or VPN Usage: The customer is trying to hide their real location. For e-commerce, that’s rarely a good sign.

- Rapid-Fire Attempts: You see multiple failed payment attempts followed by a successful one. That’s often a fraudster cycling through stolen card numbers until one works.

Your goal here is to be fast and efficient. You want to quickly separate the obviously bogus orders you can cancel right away from the "maybe" pile that needs a closer look.

Capture Every Piece of Evidence

Once you've flagged a transaction for a full-blown investigation, your job is to become a digital evidence collector. The more relevant data you can grab and preserve, the stronger your case will be when a chargeback dispute inevitably follows. Don't wait on this—some data, like server logs or customer session details, might not stick around forever.

Don't just save the order confirmation. You need to build a complete timeline of the transaction from start to finish.

Key Evidence to Collect:

- Transaction and Order Data: This is the basic stuff—order ID, amount, date, what was purchased, and the customer's name and billing address.

- Device and Connection Information: Capture the customer's IP address, the device they used (e.g., iPhone 14, Windows PC), and browser info. This can help prove the order came from a legitimate person, not a botnet.

- Customer Communication: Save every single email, chat log, or support ticket. Did they ask about shipping times before placing the order? Did they complain about a "failed" payment? This context is pure gold.

- Proof of Delivery: This is absolutely non-negotiable. Always get signature confirmation and save the tracking information that shows the package was delivered to the address provided on the order.

A messy folder of random screenshots isn’t going to fly. Set up a standardized system for each case. Name files clearly (e.g., "OrderID-12345-IP-Log.txt"). This discipline pays for itself when you're racing against a tight dispute deadline.

Build Your Representment Case

If the fraud escalates to a chargeback, all that evidence you gathered becomes your arsenal. Representment is the formal process of fighting the chargeback by presenting your evidence to the bank. You are literally "re-presenting" the transaction as legitimate.

Your representment letter needs to be clear, concise, and professional. Stick to the facts and directly counter the customer’s claim. For example, if the reason code is "Item Not Received," your proof of delivery is your star witness.

A solid representment package usually includes:

- A rebuttal letter that summarizes your argument.

- A copy of the original transaction receipt.

- All the evidence you collected, especially AVS/CVV results and IP geolocation data.

- Proof of delivery with that crucial signature confirmation.

For a much deeper dive into the nitty-gritty of this process, our guide on navigating credit card fraud investigations has more detailed strategies.

Report and Learn from the Incident

The final step is to close the loop. Once the investigation is over—win or lose—you need to report the incident. If you lost the dispute, make sure to report the fraudulent customer and transaction details to your payment processor. This helps them strengthen their own fraud databases, which helps everyone.

More importantly, treat every case as a learning opportunity. Did you spot a new fraud pattern? Could one of your internal rules be tightened to catch this next time? Analyzing what happened helps you refine your prevention strategy, making your store a harder target for the next fraudster who comes knocking. This cycle of investigation, action, and learning is what turns you from a reactive victim into a proactive defender of your business.

Gathering the Right Evidence to Win Disputes

Let’s be honest: winning a chargeback dispute isn't about luck. It's about building an airtight case with undeniable proof. When you're in the thick of a banking fraud investigation, the quality and relevance of your evidence are everything. The bank is the judge, and they're only interested in cold, hard facts that prove the transaction was legitimate.

Think of yourself as a detective. You need to gather every piece of the puzzle to tell a story that’s impossible to poke holes in. It’s about going beyond the simple receipt and digging into the digital footprints the customer left behind.

Go Beyond the Basic Order Details

A simple receipt just won't cut it anymore. To build a compelling case, you need to connect the dots between the person who made the purchase, the legitimate cardholder, and the delivery address. This is where the technical data from the transaction becomes your most valuable asset.

These details paint a clear picture of a legitimate customer, not a fraudster. For example, if the order's IP address is in the same city as the billing address, that’s a powerful piece of evidence. If that same customer has a history of successful purchases with you? Even better.

Key pieces of evidence to hunt down include:

- IP Geolocation Data: This pinpoints the physical location where the order was placed. A match between the IP location and the billing or shipping address is a huge win for your case.

- AVS and CVV Match Results: Always, always include the Address Verification System (AVS) and Card Verification Value (CVV) responses. A "match" is strong proof that the person placing the order had the physical card in their hands.

- Device Fingerprint: This is unique data about the customer’s device—think operating system, browser, and screen resolution. A consistent device fingerprint across multiple orders suggests a returning, legitimate customer.

- Customer Purchase History: Showing that the cardholder has ordered from you before without any issues is extremely persuasive. It completely undermines any claim that they don't recognize your business.

Banks process thousands of disputes every single day. Make their job easy. A well-organized case file with strong, layered evidence is far more likely to get a favorable review than a messy pile of random screenshots.

Match the Evidence to the Chargeback Reason

Not all chargebacks are created equal. You wouldn't use the same proof to fight an "Item Not Received" claim as you would for an "Unauthorized Transaction" claim. You have to be strategic.

By tailoring your evidence to directly shut down the cardholder's specific reason for the dispute, you dramatically increase your chances of winning. Let's walk through a couple of common scenarios.

The "Unauthorized Transaction" Claim

This is the classic fraud claim where the cardholder says, "I didn't make this purchase." Your job is to prove they did—or at least that someone with authorized access to their card and location did.

- Your Best Evidence: An AVS and CVV match is your star player here. Back it up with IP geolocation data that places the order origin near the cardholder's billing address. Any past order history from the same customer or IP address is the final nail in the coffin.

The "Item Not Received" Claim

Here, the customer isn't denying they placed the order; they're claiming they never got the goods. This one is all about delivery.

- Your Best Evidence: Proof of delivery is king. You absolutely need a tracking number from a reputable carrier showing the item was delivered to the address provided in the order. If you can get it, signature confirmation is your golden ticket.

For a deeper dive into evidence strategies, check out our guide on how to win a credit card dispute for more tactics.

Evidence Checklist for Common Chargeback Reasons

When you're up against a tight dispute deadline, it's easy to forget a critical piece of evidence. This table is your go-to cheat sheet for matching the right proof to the most common chargeback reasons. Being prepared can be the difference between recovering your revenue and taking an unnecessary loss.

Having this information organized and ready to go will put you in the best possible position to defend your sales and protect your bottom line.

Working with Banks and Payment Processors

When you're hit with a banking fraud investigation, it’s easy to feel like you're on an island. But you're not in it alone. Your financial partners—specifically your acquiring bank and the customer's issuing bank—are crucial players in this whole process. Figuring out how to work with them, not against them, can make all the difference.

Here’s a helpful way to think about it: your acquiring bank (the one processing your payments) is like your legal counsel in a dispute. The issuing bank (the customer's bank) is the judge. Your job is to arm your counsel with a case so strong and clear that the judge has no choice but to rule in your favor.

Understanding Each Player's Role

When a customer disputes a charge, the issuing bank kicks off the chargeback. Your acquiring bank then delivers the bad news to you, along with a request for evidence. It's a formal dance with very specific steps and tight deadlines.

It’s absolutely critical to know who does what:

- The Issuing Bank: They represent the cardholder. Their primary obligation is to investigate the customer's claim, but they will absolutely review compelling evidence from you.

- The Acquiring Bank: They represent you, the merchant. They act as the middleman for communication and evidence, but they won't build your case for you. That's on you.

- The Card Networks (Visa, Mastercard, etc.): They set the rules of the game. Their regulations dictate everything from timelines and reason codes to what counts as valid evidence.

The entire financial services sector is under constant attack. In fact, a staggering 79% of organizations faced payment fraud attempts in 2024. Fraudsters are hitting different channels strategically—high-value fraud on international wires and high-frequency scams on faster digital payments. You can get more details by checking out this comprehensive payments fraud survey.

Communicating for Success

How you present your evidence matters just as much as the evidence itself. Banks are drowning in disputes, so making your case dead simple to understand is a massive advantage. Don't just dump a folder of random screenshots on them.

Instead, craft a short, sharp rebuttal letter that walks them through the evidence. Clearly label every document (e.g., "Exhibit A - Proof of Delivery," "Exhibit B - AVS Match Confirmation"). Your goal is to make it effortless for the reviewer to connect the dots and see that the transaction was legitimate.

Pro Tip: Find the direct contact or specific portal for your payment processor's disputes team. Sending evidence to a generic support email can cause delays that blow your deadline—which is an automatic loss.

Knowing your merchant agreement and the card network rules is also a game-changer. These documents spell out your rights and responsibilities. Being familiar with them helps you build a better partnership with your acquirer and signals that you know what you're doing. For more on navigating these relationships, check out our guide on handling disputes with banks.

Ultimately, a professional, organized, and timely approach will always serve you best.

How AI Can Automate Your Fraud Investigations

Trying to manually sift through every transaction and fight every single chargeback is a surefire path to burnout. It's a slow, draining process that pulls you away from what you should be doing—growing your business. This is where modern AI tools stop being a buzzword and start becoming your most powerful ally in any banking fraud investigation.

Think of it this way: a human can only review so many orders in a day, and we're all prone to missing subtle clues under pressure. AI and machine learning systems, on the other hand, can analyze thousands of data points in the blink of an eye. They spot those suspicious patterns a person could easily overlook.

But the real game-changer isn't just about spotting fraud—it's about automating the entire fight.

Moving Beyond Manual Reviews

The old way of investigating fraud involved a lot of guesswork and tedious checklist-ticking. You'd have to manually cross-reference an IP address with a billing location or eyeball a customer’s order history to see if anything felt "off." It was time-consuming and, frankly, not very effective against today's sophisticated fraudsters.

AI flips that script completely. It doesn't just check a few boxes; it builds a comprehensive risk profile for every single transaction, all in real time.

- Behavioral Analysis: AI algorithms learn what normal customer behavior looks like for your store. This means they can instantly flag an order that deviates from the norm—like a long-time customer suddenly shipping a high-value order to a new country using a different device.

- Link Analysis: These systems can connect seemingly unrelated data points. For instance, an AI might discover that ten different orders, all using different names and credit cards, originated from the same device. That’s a massive red flag for fraud that would be nearly impossible to catch manually.

- Predictive Scoring: Instead of just giving you a binary "good" or "bad" verdict, AI assigns a dynamic risk score. This lets your team focus their limited time only on the highest-risk orders, while the vast majority of legitimate transactions sail through automatically.

Automating the Entire Chargeback Dispute

Spotting fraud is only half the battle. The other half is the soul-crushing paperwork that comes with fighting chargebacks. This is where specialized AI platforms, like ChargePay, truly shine by automating the complete chargeback and dispute management process from start to finish.

This isn't just about filling out a form faster. It’s a complete overhaul of your workflow:

- Automated Evidence Gathering: The moment a chargeback hits, the AI instantly pulls all the relevant evidence—transaction IDs, AVS/CVV results, IP geolocation, delivery confirmation, and customer communication. No more frantic searching through half a dozen different systems.

- AI-Powered Rebuttal Writing: The system then uses this evidence to generate a clear, compelling, and properly formatted representment letter tailored to the specific chargeback reason code. It knows exactly what the banks want to see.

- Automatic Submission: Finally, the entire dispute package is submitted to the correct bank or payment processor through the right portal, ensuring you never miss a tight deadline.

The goal of AI in a banking fraud investigation is simple: to make human intervention the exception, not the rule. It frees your team from repetitive tasks so they can focus on complex cases and high-level strategy.

The Real-World Benefits of Automation

This shift isn't just theoretical; it's a critical response to how criminals operate right now. Today, over 50% of fraud involves AI and deepfake technology, forcing financial institutions to fight fire with fire.

In fact, 90% of banks are now using their own AI to speed up fraud investigations and detect new criminal tactics. The scale of this arms race is staggering, with financial institutions spending $21.1 billion on fraud prevention. By adopting automation, you're not just keeping pace; you're giving your business a serious advantage.

The benefits are tangible and immediate: recovering more revenue, saving countless work hours, and finally getting out from under that mountain of paperwork. To understand the broader implications of this technology, it's worth exploring resources on AI in banking and finance law to see how the entire industry is adapting.

Quick Answers to Your Fraud Investigation Questions

When you're staring down a potentially fraudulent order, you don't have time to waste. You need answers, and you need them fast. We get it. Here are some of the most common questions we hear from merchants in the trenches, with the straightforward advice you need to make the right call.

I Think an Order Is Fraudulent. What's My First Move?

Stop everything. Immediately put that order on hold.

Whatever you do, don't ship the product or fulfill the service. Your number one job is to stop a potential loss in its tracks. Once the shipment is halted, you can take a breath and pivot to investigation mode. Start pulling together the evidence we've talked about—order details, customer emails, any flags from your payment gateway. In these situations, speed is your best friend.

How Long Do I Have to Fight a Chargeback?

This is where the clock really starts ticking. The moment you get that chargeback notification, your response window opens, and it varies a lot depending on the card network (Visa, Mastercard, etc.) and the banks involved.

Generally, you're looking at a window of 7 to 45 days to get your evidence together and submit your dispute. This tight turnaround is exactly why having a dialed-in investigation process is a game-changer.

Miss that deadline, and it's an automatic loss. It doesn't matter how rock-solid your evidence is. This is one of the biggest reasons merchants lean on automation—it ensures you never lose revenue just because you missed a cutoff date.

Is There a Way to Completely Stop Friendly Fraud?

Honestly, no. You can't eliminate it entirely. Friendly fraud is tricky because it often comes from a place of genuine customer confusion, a case of buyer's remorse, or sometimes, someone just trying to get something for free. But you can absolutely get ahead of it and cut it down dramatically.

Your best bet is to be proactive. Focus on crystal-clear communication and a great customer experience:

- Make Your Billing Descriptor Obvious: The name on their credit card statement needs to be instantly recognizable. "SPARKLEJEWELRY.COM" is a thousand times better than a vague holding company name like "SJ HOLDINGS LLC."

- Over-Communicate (in a good way): Send those order confirmations. Follow up with shipping updates and tracking numbers. Send another notification when it's delivered. The more you keep the customer in the loop, the harder it is for them to claim they forgot about the purchase or never got it.

- Have an Easy-to-Find Return Policy: If a customer can get a refund from you with a few clicks, they're way less likely to go through the hassle of filing a chargeback with their bank. Make your support team accessible and your return process painless.

At the end of the day, making every part of the transaction transparent and familiar for the customer is the most powerful way to shut down this frustrating problem before it even starts.

Stop losing revenue to tedious, manual chargeback disputes. ChargePay uses AI to automate the entire process, from gathering evidence to submitting winning representment cases, recovering up to 80% of your lost funds. See how much revenue you can reclaim with ChargePay.

.svg)

.svg)

.svg)

.svg)