If billing disputes feel worse than they used to, you're not imagining it. They're no longer an occasional annoyance you clean up on Friday afternoon. For many Shopify merchants, they're a steady leak in revenue, time, and team attention.

I've seen the same pattern over and over. A store works hard to acquire a customer, fulfills the order, answers support tickets, and then loses the sale anyway because a bank yanks the money back. The part that hurts most isn't just the reversal. It's the feeling that you're doing real work and still getting punished for it.

The good news is that billing disputes are manageable when you understand what causes them, how the process works, and where automation changes the game.

Why Billing Disputes Are Costing You More Than Ever

Ecommerce chargeback rates rose 222% year over year between Q1 2023 and Q1 2024, and 72% of cardholders now view chargebacks as an acceptable alternative to merchant refunds, according to this chargeback statistics roundup. That changes the way merchants need to think about billing disputes.

This isn't just a fraud problem anymore. It's also a customer behavior problem.

A buyer who gets confused, impatient, or doesn't want to wait for a refund can go straight to their bank. When that happens, you lose control of the conversation. The order becomes a case file.

What this looks like in a Shopify store

For most merchants, the damage shows up in a few places at once:

- Lost sales: You lose the order revenue, and often the product is already gone.

- Operational drag: Someone has to stop what they're doing and pull screenshots, tracking info, policy pages, and customer emails.

- Cash flow pressure: Reversed funds create noise in your books and make forecasting harder.

- Team frustration: Support thinks operations missed something. Operations thinks support didn't document enough. Everyone feels behind.

Practical rule: Every billing dispute is two losses unless you respond well. You lose the transaction first, then you lose time deciding whether to fight it.

The old way of handling disputes doesn't hold up when volume climbs. Manual review works when cases are rare. It breaks when they become routine.

That's why merchants need a system, not just a checklist. If billing disputes have become part of normal business, then revenue recovery has to become part of normal operations too.

Understanding What Causes Most Billing Disputes

Most merchants hear "billing dispute" and think stolen card. That does happen. But it isn't the whole picture.

A billing dispute starts when a customer questions a charge with their bank. A chargeback is what happens when the bank pulls the funds back from you. Think of the dispute as the complaint and the chargeback as the penalty.

The three main causes

Billing disputes usually come from three buckets.

| Cause | What it means | Common example |

|---|---|---|

| Criminal fraud | Someone used a card without permission | A stolen card is used to place an order |

| Merchant error | The business made a preventable mistake | Duplicate charge, late refund, wrong amount |

| Friendly fraud | A real customer disputes a legitimate charge | They forgot the order, didn't recognize the descriptor, or chose the bank instead of support |

The biggest source is friendly fraud. 60% to 80% of all chargebacks are tied to consumers disputing legitimate charges, and 72% of cardholders don't understand the difference between refunds and chargebacks, according to The Payments Association's writeup on billing descriptor confusion and dispute behavior.

That matters because it changes how you defend your store. You're often not fighting a mastermind. You're dealing with confusion, convenience, or buyer's remorse.

Why customers file billing disputes when the order was valid

A customer may file a dispute even when you did your job correctly.

- They don't recognize the charge: Your statement descriptor looks different from your store name.

- They forgot the purchase: This happens often with subscriptions, gifts, and delayed shipping.

- They wanted a faster path to money back: The bank feels easier than waiting for support.

- Someone else in the household made the purchase: The cardholder sees the charge and assumes fraud.

- They were unhappy, but never contacted you: Instead of asking for help, they escalate first.

Billing disputes often start as a communication failure long before they become a fraud claim.

Where merchants get confused

A lot of store owners ask, "If the order was real, why did the bank accept the complaint at all?"

Because the system is built to act first and sort it out later.

Banks are trained to protect cardholders quickly. That means merchants often have to prove the sale was valid after the funds are already gone. If you treat every dispute like a legal argument, you'll miss the practical issue. The customer experience before the dispute often decides whether the dispute happens at all.

A simple way to diagnose the root cause

When a case comes in, ask three questions:

- Was the cardholder legitimate?

- Did our store create confusion or friction?

- Do we have records that clearly show what happened?

If the answer to the first is yes, the second is no, and the third is yes, you're usually looking at a dispute you should fight.

If the second answer is yes, fix the process even if you decide not to fight that one case. Billing disputes are expensive, but they also reveal where your store is hard to understand.

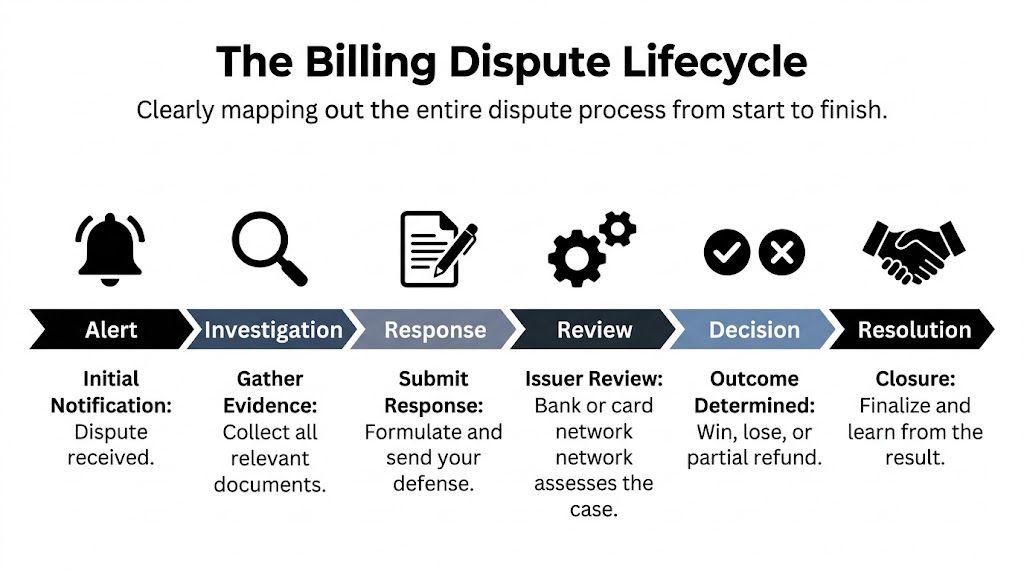

The Billing Dispute Lifecycle From Alert to Resolution

A billing dispute feels sudden when it lands in your dashboard. In reality, it moves through a sequence. Once you know the sequence, it becomes much easier to act without panic.

If you want a deeper walkthrough of the steps and terminology, ChargePay has a useful guide to the card dispute process.

Stage one through three

The early stages decide whether you have a real chance to recover the money.

Alert

You receive notice that a customer challenged a transaction. Sometimes this starts as an inquiry. Sometimes it arrives as a formal chargeback.Investigation

You pull the order details. That includes payment record, fulfillment status, tracking, customer messages, policy acceptance, and any prior refunds or replacements.Response decision

You decide whether to accept the loss or contest it. Many merchants waste time here. They know the order was valid, but they don't know if they can prove it cleanly.

Stage four through six

Once you choose to fight, the issue becomes a documentation job.

- Evidence assembly: You build a packet that matches the dispute reason. Not every case needs the same proof.

- Issuer review: The bank reviews what you submitted against the cardholder's claim.

- Final resolution: You either recover the funds, lose the case, or get a partial outcome depending on the network and reason code.

Why deadlines create so much pressure

The hardest part of billing disputes isn't usually understanding what happened. It's getting everything together before the deadline closes.

Support has one set of records. Ops has another. Your shipping data lives in a carrier dashboard. Screenshots sit in Slack. A policy changed after the order date. Suddenly a simple dispute turns into a scavenger hunt.

Miss the response window and the quality of your evidence no longer matters.

That's why merchants with growing order volume need a repeatable workflow. The dispute lifecycle rewards speed, organization, and relevance. It punishes delay.

What a healthy workflow looks like

A working process usually has these traits:

- One owner: One person or system is responsible for the case from start to finish.

- Case-specific evidence: The submission matches the reason code instead of dumping every document you have.

- Documented timeline: You can show when the order was placed, fulfilled, delivered, and discussed.

- Deadline tracking: No case sits unseen until the response date is too close.

A dispute process should feel like a queue, not a fire drill. When merchants solve that part, billing disputes stop consuming the whole team.

How to Gather Winning Evidence for Your Case

Evidence wins billing disputes. Opinions don't.

Banks don't care that a customer was rude. They don't care that your team is certain the claim is false. They care whether your records make the case easy to approve.

There's also a real cost to weak documentation. A Stripe merchant could lose about $181 when fighting and losing a chargeback on a $100 physical product order, factoring in lost merchandise, shipping, fees, and staff time, as noted in the same Swell dataset cited earlier.

Your evidence checklist

For a physical product order, these are the first items I want in front of me:

- Order confirmation: The order number, items, amount, billing details, and timestamp.

- Payment record: Authorization result, transaction ID, and card details as available in your processor.

- Fulfillment proof: Tracking number, carrier scan history, delivery confirmation, and signature confirmation if you have it.

- Customer communication: Emails, chat logs, help desk tickets, and any messages where the buyer discussed the order.

- Store policies in effect at the time: Refund, shipping, subscription, and cancellation terms. Use the version that applied on the purchase date.

- Product page evidence: Screenshots showing the item description, delivery estimates, and any variant selected.

- Account history: Prior successful orders can help show a pattern of legitimate use.

If you need to tighten up the very first document in that chain, this guide on order confirmation shows what a clear post-purchase record should include.

Match the proof to the claim

Here, many merchants lose cases they should win. They submit good documents, but for the wrong argument.

| Dispute claim | Most useful evidence |

|---|---|

| Item not received | Tracking, delivery scan, signature, shipping address match |

| Transaction not recognized | Descriptor explanation, order confirmation, customer identity match |

| Canceled order or refund expected | Cancellation policy, refund timeline, customer messages |

| Product not as described | Product page, variant selection, photos, communications about use or condition |

Don't send a giant pile of screenshots and hope the reviewer sorts it out. Make the evidence answer the exact complaint.

Keep records like someone else will need them later

A good rule is simple. If a person outside your company couldn't understand the order history in two minutes, your records need work.

That means:

- save policy screenshots when orders come in

- keep shipping and support data connected to the order

- avoid scattered notes in personal inboxes

- standardize file names and timestamps

Some merchants also use outside admin support when disputes pile up. If your team is overwhelmed by document collection, a service like Hire Paralegals can be a practical resource for organizing case materials and written records.

The goal isn't more paperwork

The goal is a clean story.

You want the reviewer to see one clear conclusion: the cardholder placed the order, your store disclosed the terms, the item was fulfilled as promised, and the complaint doesn't match the record.

When your evidence does that, billing disputes become far less random.

Writing a Representment Response That Actually Wins

A representment response isn't a customer service email. It's a case summary for a reviewer who has limited time and no context.

That means emotional writing usually hurts you. Long explanations hurt you too. The winning response is short, specific, and tied directly to the documents.

For a practical breakdown of how representment works, this article on chargeback representment is worth reading.

What weak responses sound like

Weak responses usually have one of these problems:

- They argue feelings: "This customer is lying."

- They ramble: Three long paragraphs before the actual facts appear.

- They don't map evidence to the claim: Attachments are included, but the reviewer has to guess why.

- They sound defensive: The merchant writes as if they are arguing with the customer, not helping the bank make a decision.

Here's the difference in plain terms.

| Weak response | Strong response |

|---|---|

| "The customer is wrong and we always ship on time." | "Order #4581 was placed on March 4 and shipped on March 5 to the verified address on file." |

| "Please see attached screenshots." | "Attachment A shows the order confirmation. Attachment B shows carrier delivery confirmation." |

| "We did nothing wrong." | "The evidence shows the transaction was authorized, fulfilled, and delivered under the disclosed policy." |

A simple response structure

Use this order when you write:

State the conclusion first

Example: The disputed transaction was valid and fulfilled according to the order terms.Summarize the transaction

Include order date, item, amount, fulfillment date, and delivery result.Address the claim directly

If the reason is "item not received," lead with delivery proof. If it's "transaction not recognized," lead with identity and descriptor context.Reference each attachment clearly

Name the document and explain why it matters.Close without emotion

Ask that the chargeback be reversed based on the submitted evidence.

A reviewer should be able to skim your first paragraph and know exactly why you believe the chargeback should be overturned.

What bank reviewers are really looking for

They want clarity, consistency, and relevance.

They don't want ten pages when two pages would do. They don't want screenshots with no labels. They want the shortest path to a confident decision.

Manual responses often fail because the merchant knows too much. You lived the order. The reviewer didn't. Your job is to reduce the case to a clean timeline with proof attached.

Why AI-written responses usually outperform rushed manual ones

A person writing under deadline tends to overexplain or miss key details. A good system doesn't get flustered. It pulls the same categories of evidence every time, follows the same structure, and matches the language to the dispute type.

That's the primary advantage. Not fancy wording. Just consistency.

Billing disputes become easier to win when your response reads like a case file instead of a frustrated note from the founder.

How ChargePay Automates Your Entire Dispute Workflow

Manual dispute management breaks in the same place every time. Data lives in too many systems, deadlines arrive too fast, and every case starts from scratch.

The fix is to turn billing disputes into a process that runs automatically.

According to Kount's discussion of chargeback data analysis and automated representment, merchants who combine processor chargeback data with CRM details can map dispute patterns and act earlier. The same source notes that ChargePay has a 92.4% win rate across 200K+ cases and recovered $10.8M by submitting evidence packages before deadlines.

What automation actually does

In practice, an automated workflow handles the repetitive parts that slow humans down:

- Detects the case fast: New disputes get surfaced as soon as they're available.

- Pulls the right records: Order data, tracking, customer messages, and policy records are collected from the source systems.

- Reads the reason code: The case type shapes the evidence packet.

- Builds the response: The representment is assembled around the actual claim.

- Submits on time: Deadline risk drops because the workflow doesn't rely on someone remembering to circle back.

You can see how this fits together on the ChargePay product page.

Why this changes the economics

When you handle billing disputes manually, each case has to justify the staff time. Smaller-value orders often get written off because fighting them feels inefficient.

Automation changes that calculation. If a system can collect the records, structure the argument, and submit before the cutoff, more valid cases become worth contesting.

That shifts disputes out of the "annoying admin task" category and into revenue recovery.

What matters when choosing a tool

If you're comparing options, don't focus only on dashboards. Check whether the tool can complete the work.

Look for:

- Shopify connection quality: It should pull order and customer data without manual exports.

- Evidence generation: Not just storage. Actual case assembly.

- Submission handling: Deadlines matter more than nice charts.

- Pricing logic: A pay-per-win model lines up with recovered revenue.

- Merchant trust signals: App reviews and platform vetting help you avoid extra operational headaches.

ChargePay fits that model for Shopify merchants. It has a Built for Shopify badge, a 4.9-star rating, and pay-per-win pricing. What's more, it handles the operational work that usually causes merchants to lose.

The real value of automation isn't speed by itself. It's removing the human gaps that cause good cases to fail.

Proactive Strategies to Prevent Billing Disputes

The cheapest dispute to fight is the one that never happens.

Most prevention work isn't glamorous. It's basic store hygiene done consistently. But it protects revenue better than most merchants expect.

One of the biggest fixes is your billing descriptor. Unclear billing descriptors cause 35% of all transaction disputes, and optimizing them with dynamic details can reduce chargebacks by 30% to 40%, according to this explanation of billing descriptors and unknown charge disputes.

Start with the charge customers actually see

Customers don't dispute your beautifully designed product page. They dispute the line on their statement.

If your legal entity, processor name, or shortened descriptor looks unfamiliar, a buyer may assume fraud before they ever search their inbox.

Good descriptors are:

- Recognizable: Close to your storefront brand name

- Specific: Sometimes with useful context such as a product or order reference

- Consistent: Similar across checkout, confirmation email, and statement experience

Clean up the moments that create doubt

Billing disputes usually start when something feels off to the customer.

Review these friction points:

- Checkout messaging: Shipping windows, renewal terms, and refund rules should be easy to spot.

- Order emails: Send confirmations and shipping updates that make the purchase easy to remember later.

- Support access: A visible support path gives customers somewhere to go besides their bank.

- Subscription reminders: If you bill on a recurring cycle, remind people before the charge lands.

A lot of the same clarity work applies across channels. If you also sell on marketplaces, this guide to Amazon listing optimization is a useful reminder that clear product presentation reduces confusion before and after purchase.

Prevention works best when it's operationalized

Policy pages alone won't save you if your team can't apply them consistently.

Build a few habits into your store operations:

| Prevention habit | Why it helps |

|---|---|

| Save policy versions by date | Lets you prove what the customer agreed to |

| Send tracking fast | Reduces "where is my order" uncertainty |

| Keep support history tied to the order | Makes future defense easier |

| Review dispute reasons monthly | Shows recurring points of confusion |

If you want more practical prevention ideas, this guide on chargeback prevention covers the operational side well.

A short walkthrough can also help if you're auditing your current setup:

Prevention is still revenue recovery

Some merchants think prevention and dispute management are separate jobs. They aren't.

Every prevented dispute protects the original sale. Every clean descriptor, clear email, and documented policy reduces the chance that a valid order turns into a bank claim later.

That's why the strongest stores treat billing disputes as a systems issue. Not bad luck.

Frequently Asked Questions About Billing Disputes

What's the difference between an inquiry and a chargeback

An inquiry is an early question about a transaction. A chargeback is the actual reversal of funds.

Treat an inquiry seriously. It may be your best chance to clarify the issue before it becomes a formal loss.

Should I contact the customer after they file a dispute

Usually, yes, but carefully.

Keep the message professional and focused on facts. Don't pressure them. Don't accuse them of fraud. The goal is to resolve confusion and document the interaction, not to escalate emotions.

Can I refuse to ship an order that looks risky

Yes. If an order shows clear warning signs, it's usually better to pause, verify, or cancel than to fulfill and hope for the best.

The key is consistency. Use clear internal rules so your team doesn't approve risky orders just because it's a busy day.

Should I always fight every billing dispute

No.

Fight the cases you can support clearly with evidence. If your store made a mistake, fix it quickly. If the order was valid and documented well, contest it.

What's the most common merchant mistake

Submitting too much irrelevant information or responding too late.

A messy packet can be almost as harmful as no packet. Reviewers need the right documents, not all documents.

What if the customer says they don't recognize the transaction

Start with the statement descriptor, order confirmation, and any proof tying the cardholder to the purchase. This type of case often comes down to recognition and documentation.

Can a refund still help after a dispute starts

Sometimes, but you need to coordinate carefully.

If the dispute is already active, refunding without a plan can create extra confusion. Check the case status and processor guidance before acting.

How do small teams keep up with billing disputes

They usually don't, at least not manually.

That's why small brands benefit the most from a system that tracks deadlines, gathers records, and prepares responses without adding more admin work to a support team that is already stretched.

If billing disputes are eating into your margins, ChargePay is built to handle the work that usually slows merchants down. It automates evidence collection, response creation, and submission for Shopify disputes so your team doesn't have to manage every case by hand. If you want billing disputes to stop feeling like a recurring fire drill, install it from the Shopify App Store and put recovery on autopilot.

.svg)

.svg)

.svg)

.svg)