Ever dealt with a con artist who spends months building a friendship, only to vanish after borrowing a huge sum of money? That’s the e-commerce version of bust out fraud. It’s a slow, patient scam where a criminal creates an account, builds a history of small, legitimate-looking purchases to earn your trust, and then hits you with a series of massive orders before disappearing completely.

What Is Bust Out Fraud?

Bust out fraud is a long-con scheme where criminals masterfully play the part of a perfect customer right before they strike. This isn't a quick smash-and-grab theft; this attack is all about patience and deception. The fraudster's goal is to build a squeaky-clean purchase history over weeks or even months.

They start small, making insignificant purchases and always paying on time. To a merchant, this behavior looks like a low-risk, genuine customer. A good starting point for context is understanding the different types of premeditated schemes out there, including common stablecoin scams, which also rely on building false trust.

Once they've built up a positive reputation—and maybe even earned a higher credit limit or trusted status—they execute the "bust out." This is the endgame, where they place one or more very large orders in quick succession, maxing out any credit they can. As soon as the high-value goods are shipped, the fraudster is gone.

The payments never come through, and the merchant is left holding the bag with a huge financial loss and a wave of inevitable chargebacks. This method is especially dangerous because all the initial activity seems perfectly normal, making it incredibly difficult for standard fraud detection systems to raise a red flag. It’s a calculated attack that exploits the very trust merchants extend to their seemingly loyal customers.

The Slow Burn Of Deception

What makes bust out fraud so wickedly effective is its gradual nature. A criminal might spend months nurturing an account, making it look completely indistinguishable from a real shopper. This slow burn is strategically designed to fly under the radar of security checks that are only looking for sudden, high-risk behavior.

A single bust out fraud attack can cost an organization tens or even hundreds of thousands of dollars in direct fraud losses. The indirect consequences, like reputational damage, are often just as severe.

This method often has some overlap with other types of fraud. In some cases, it's a form of first-party fraud, where a real person uses their own identity but with the premeditated plan to defraud a business from the start. You can get a deeper look into how customers can be the source of fraud by reading our guide on what is first-party fraud.

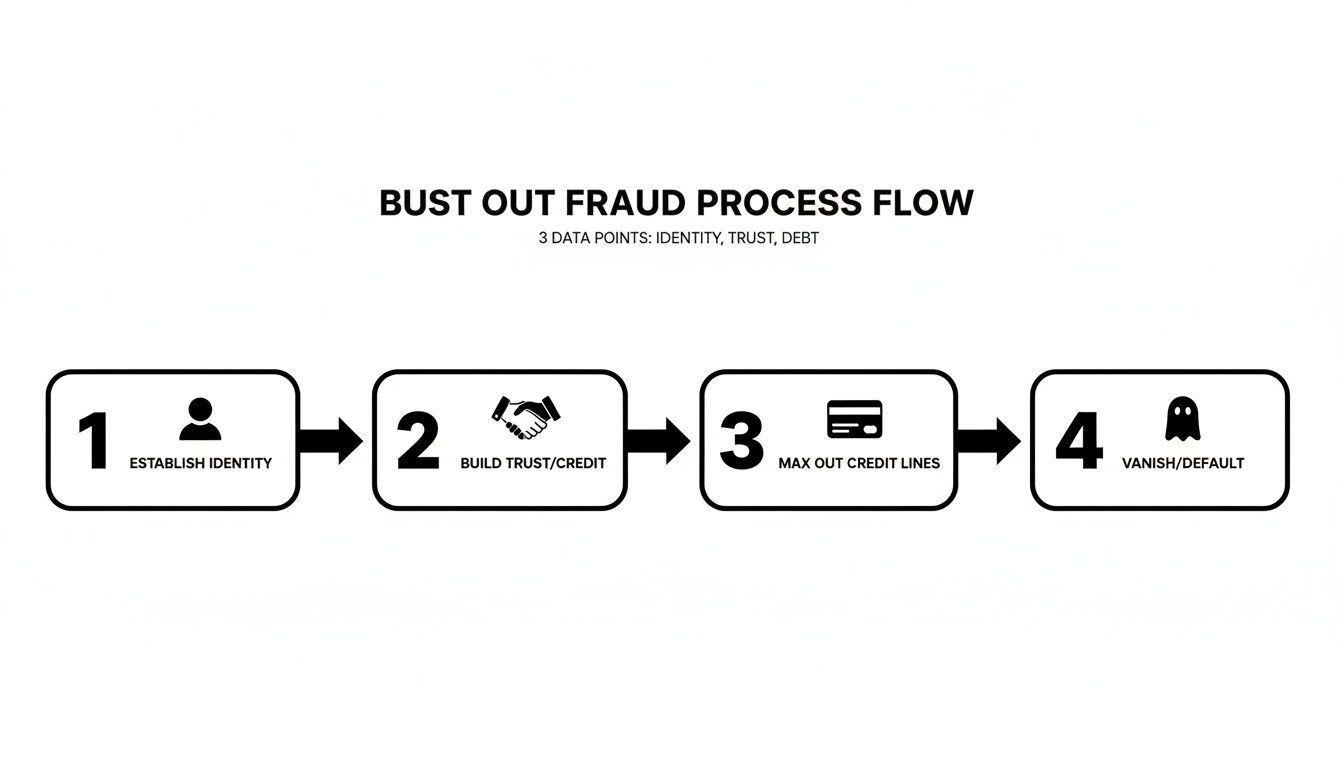

The infographic below breaks down the simple, four-step playbook these fraudsters follow.

As you can see, the process is methodical. It moves from establishing a seemingly legitimate presence all the way to the final act of disappearing with the goods.

The Four Stages Of A Bust Out Fraud Scheme

To really get a handle on the attacker's playbook, it helps to break the whole scheme down into distinct stages. Each step is carefully planned with a specific goal in mind, all building toward that final, costly bust out.

Here’s a look at how it typically unfolds:

By understanding this lifecycle, you're better equipped to spot the warning signs before the final, devastating stage.

The Anatomy of a Bust-Out Fraud Attack

To really get a handle on bust-out fraud, you have to think like a criminal for a minute. This isn't a smash-and-grab job; it's a long con. It's a calculated, patient attack that unfolds in stages, a lot like a hunter carefully setting a trap before springing it.

Fraudsters don't just kick down the digital door and take what they want. They patiently build a believable cover story, earning your trust before they make their move.

The whole process kicks off with the creation of a fake identity. For this, criminals usually pull from one of two playbooks: using a completely stolen identity or creating a synthetic identity. A stolen identity is exactly what it sounds like—they get their hands on a real person's name, address, and personal details and simply impersonate them.

A synthetic identity, on the other hand, is a bit more crafty. Fraudsters stitch together bits of real and fake information to create a brand-new persona. Think of a real Social Security number paired with a made-up name and a temporary drop-shipping address. This creates a "Frankenstein" profile that’s incredibly hard for automated systems to flag because some of the key pieces are actually legitimate.

The Grooming Phase: The Slow and Steady Deception

With a fake identity in hand, the "grooming" phase begins. This is where the fraudster’s patience really pays off. They'll open an account with your store and start making small, completely normal-looking purchases.

These aren't random buys. Every single transaction is a deliberate move designed to build a history of good behavior. They might buy a cheap item one week, wait a few more, then buy something else. And the most important part? They always pay their bills on time.

To you or your fraud detection system, this account looks like a model customer. It shows a pattern of reliable payments and perfectly reasonable buying habits. Over weeks, or even months, this "good customer" earns your trust, which might unlock perks like a higher credit limit or access to express checkout. The fraudster is basically aging the account like a fine wine, getting it ready for the final act.

Bust-out fraud is a billion-dollar problem for lenders and merchants. The slow, methodical approach is designed to deceive not only individual businesses but also the credit bureaus that track consumer behavior.

This slow burn is exactly what makes this scam so brutally effective.

The Bust-Out: The Final Heist

After months of meticulous grooming, the fraudster decides it’s go-time. This is the "bust-out," and when it happens, it happens fast. The behavior of your once-perfect customer changes on a dime, with no warning whatsoever.

All of a sudden, the account that was making small, infrequent purchases starts maxing out its credit limit with huge orders. They might buy thousands of dollars worth of high-value, easily resalable goods like top-of-the-line electronics or designer clothes.

And it's rarely limited to just one store. A sophisticated fraud ring will often use the same synthetic identity to hit multiple merchants at the exact same time, maximizing their haul in a very short window. As soon as the orders are confirmed and the items have shipped, the fraudster makes their final move.

They vanish.

The account goes dark, the payments stop, and the phone number and email address become dead ends. You're left holding the bag for a massive loss, and pretty soon, the chargebacks start rolling in. The financial hit from a bust-out attack goes way beyond the lost merchandise; you’re also on the hook for fees, penalties, and a damaged relationship with your payment processor. Unfortunately, this isn't a rare occurrence; to understand how this works, take a look at our guide on what is chargeback fraud.

The world of payment fraud is changing. Global chargeback volume hit 261 million transactions in 2025 and is projected to jump to 324 million by 2028—a 24% increase in just three years. This isn't just a cost of doing business anymore; it's a direct threat to your bottom line.

Red Flags to Help You Spot Bust Out Fraud Early

Catching bust out fraud before the final "bust" is everything. Because these schemes are a slow burn, the warning signs can be incredibly subtle at first. They have a nasty habit of hiding in plain sight, looking a lot like the actions of a new, enthusiastic customer.

Learning to spot these red flags is like developing an early warning system for your business. It’s all about recognizing when normal customer behavior crosses the line into something suspicious, giving you a chance to act before a fraudster can do real damage.

New Account and Identity Indicators

The first place to look for clues is right at the beginning—when the account is created. Fraudsters often leave behind small but significant tells when they’re setting up their fake profiles.

For instance, a new account using a freshly registered email address or a temporary phone number should immediately catch your eye. Real customers almost always use established email accounts they’ve had for years.

Other identity red flags to watch for include:

- Vague or Generic PII: The use of a generic name like "John Smith" paired with a free email provider (think Gmail or Yahoo) can be a signal, especially when combined with other indicators.

- Shipping to a Freight Forwarder: Scammers love using freight forwarding services or mail drops. It obscures the final destination of the goods and makes them much harder to trace.

- Inconsistent Data: Always look for mismatches. A billing address in Miami with a shipping address in Seattle is one thing, but an IP address from another country entirely is a major red flag.

Any one of these signs on its own might be nothing. But when you see several of them together, they start to paint a pretty clear picture of a high-risk account.

Sudden Shifts in Buying Behavior

The most telling signs of a bust out scheme pop up in the customer's transaction patterns. After weeks or even months of small, predictable purchases, a sudden and dramatic shift in behavior is the biggest warning you'll get.

This is the moment the fraudster decides the "grooming" phase is over and it's time for the "bust out." They've earned your trust, and now they're ready to cash in on it.

Spotting anomalies here is crucial. A fraudster might make ten purchases of $50 over two months, then suddenly place three orders for $1,000 each in a single day. This abrupt escalation is a classic bust out indicator.

This is where having robust systems in place makes all the difference. Effective transaction monitoring solutions can automatically flag these sudden spikes, giving you a crucial window to intervene before it’s too late.

Early Warning Signs of Bust Out Fraud

To make monitoring accounts easier, it helps to have a clear checklist of warning signs. The table below breaks down the most common red flags, what they actually look like, and why they should set off alarm bells for your team.

Keeping these signs top-of-mind will make your team much more effective at telling the difference between a loyal customer and a patient criminal waiting for the perfect moment to strike.

How Bust-Out Fraud Really Hurts Your Business

When a bust-out fraud scheme finally detonates, it’s less like a single explosion and more like a landmine that sets off a chain reaction. The first hit is obvious: you’ve shipped out valuable products that you’ll never get paid for. That direct blow to your bottom line hurts, but it's just the beginning.

The real damage kicks in when the fraudster disappears, and the chargebacks start pouring in. This isn't just one or two disputes. A well-executed bust-out attack can unleash dozens at once, burying your team in an administrative nightmare and creating a serious cash flow crisis.

The Financial Fallout Beyond Lost Goods

Every single one of those chargebacks comes with its own non-refundable fee from your payment processor. These fees, typically between $20 and $100 per transaction, are charged regardless of whether you win the dispute. With a wave of fraudulent transactions, these fees alone can quickly snowball into thousands of dollars of dead loss.

This sudden spike in disputes completely torches your chargeback-to-transaction ratio. Payment networks like Visa and Mastercard watch this metric like a hawk. If your ratio creeps over their threshold—usually around 1%—you’ll find yourself in hot water.

The true cost of chargebacks extends far beyond the disputed transaction amount itself, creating a significant financial burden that many merchants fail to fully quantify.

Landing in a high-risk monitoring program is serious business. You’re looking at much steeper processing fees, and you might be forced to keep a hefty cash reserve on hand just in case. In a worst-case scenario, if you can't wrestle your chargeback rate back down, your payment processor could shut down your merchant account entirely, leaving you dead in the water and unable to accept card payments.

The Hidden Costs Sinking Your Business

The financial bleed doesn’t stop with lost goods and penalties. The real cost of fraud is always much higher than what you see on the surface. In fact, for every $1 lost to fraud, merchants actually lose an average of $3.35 once you factor in the cost of the goods, shipping, operational expenses, and those punishing chargeback fees.

This problem is only getting bigger. By 2026, chargeback fraud is expected to drain $28.1 billion from merchants worldwide—that's a staggering 40% jump from 2023.

On top of the financial drain, these attacks are a massive time-suck. Instead of focusing on growth, your team is stuck digging through records and fighting disputes they have almost no chance of winning. This also poisons your relationship with your financial partners. A history of high fraud makes it much tougher to get good terms with banks and processors down the road. To get a broader perspective, you might be interested in our article exploring how chargebacks hurt businesses in various ways.

Ultimately, stopping bust-out fraud isn't just about protecting your inventory. It's about protecting your financial stability, your reputation, and your very ability to stay in business.

Practical Strategies to Prevent Bust Out Fraud

Knowing the red flags of bust-out fraud is one thing, but building a solid defense plan is how you actually protect your business. Preventing this patient scam requires a layered approach, blending smart manual checks with powerful automated tools. The goal isn't just to catch fraud but to make your store such a difficult target that criminals decide it's not worth the effort.

Think of your defense like securing a building. You need strong locks on the doors, cameras monitoring the hallways, and a security guard who knows what to look for. No single layer is foolproof, but together, they create a formidable barrier against intruders.

Fortify Your Front Door with Verification

The best place to stop bust-out fraud is right at the beginning—during account creation and at the checkout. Think of robust identity and payment verification tools as your digital bouncer, turning away suspicious characters before they can even get inside.

These tools are essential for making sure a customer is who they claim to be. Here are the core components of a strong front-door defense:

- Address Verification Service (AVS): This is a fundamental check. It compares the billing address a customer enters with the one their card-issuing bank has on file. A mismatch is an immediate red flag that needs a closer look.

- Card Verification Value (CVV): That three- or four-digit code on the back of a credit card is a simple but effective way to ensure the customer physically has the card, making life much harder for fraudsters who only have stolen card numbers.

- IP Geolocation: Checking the physical location of a customer's IP address can reveal some major inconsistencies. For instance, an order placed from an IP in a high-risk country that asks for local shipping should absolutely trigger an alert.

Monitor Account Behavior Proactively

Once an account is created, your surveillance system kicks in. Bust-out fraudsters rely on that "grooming" phase to build trust, but that’s also where they leave clues. By actively watching for unusual patterns, you can catch them before they make their big move.

This means paying close attention to sudden changes. An account that historically spends $75 a month and then suddenly places three orders for $1,500 in one day is a massive warning sign. This is where setting velocity limits—rules that cap the number or value of transactions an account can make in a short period—is so critical.

Setting intelligent velocity limits is one of the most effective ways to disrupt the "bust out" phase. It acts as an automatic circuit breaker, preventing a fraudster from extracting maximum value before they vanish.

This is also an area where AI-powered fraud detection tools really shine. They can analyze thousands of data points in real-time, spotting subtle correlations and anomalies that a human analyst might miss. They learn what normal buying patterns look like for your store and instantly flag anything that deviates, giving you a powerful early warning system. These advanced strategies are a core part of effective chargeback fraud prevention.

The challenge is that not all fraud comes from shadowy criminals. In fact, a huge chunk originates from legitimate customers. Friendly fraud, where authorized customers dispute valid purchases, now accounts for about 75% of all chargebacks globally, turning what was once a nuisance into a major threat to your bottom line. You can learn more by reading the full report on retail chargebacks. This is why a multi-layered defense that addresses both malicious and opportunistic fraud is so important for protecting your revenue.

Got Questions About Bust-Out Fraud?

Even after you get a handle on the basics of bust-out fraud, some specific questions almost always pop up. Let's tackle a few of the most common ones we hear from merchants.

Is Bust-Out Fraud Just Another Name for Identity Theft?

Not quite, though they definitely travel in the same circles. Identity theft is pretty straightforward: a criminal steals a real person's information and uses it to commit fraud. Bust-out fraud can start that way, but often it involves a synthetic identity—a totally fabricated persona made from a cocktail of real and fake details.

The real difference is the game plan. Bust-out fraud is a long con. It’s all about patiently building a history of good behavior before maxing everything out and disappearing, no matter whose identity is being used.

Wait, Can a Real Customer Pull a Bust-Out Scheme?

Absolutely, and it happens more than you'd think. When a legitimate customer opens an account using their own, real identity but secretly plans to defraud you from day one, it's a type of first-party fraud. They play by the same rules: make small purchases, pay on time, build trust, and then—bam—they place huge orders and vanish.

The heart of bust-out fraud isn't really about the identity being used. It's the premeditated plot to earn trust just to exploit it for a big payday. This intent is what separates a fraudster from a good customer who just falls on hard times.

Why Doesn't My Standard Fraud Filter Catch This?

This is the million-dollar question. Your typical fraud filters are programmed to look for immediate red flags—things like mismatched billing and shipping addresses, sketchy IP locations, or a massive first-time order from a brand-new account. Bust-out fraud is engineered specifically to fly right under that radar.

Think about it: the fraudster's initial activity looks perfect. They make small, regular purchases and always pay their bills on time. To an automated system, they look like an ideal, low-risk customer. By the time they get to the "bust-out" phase and the big-ticket purchases start, they've already built up a squeaky-clean reputation, tricking your system into thinking everything is perfectly normal.

Ready to stop losing revenue to fraudulent chargebacks? ChargePay uses AI to automate the entire dispute process, generating winning evidence and recovering up to 80% of your lost funds without you lifting a finger. See how much you can recover at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)