Of course you can dispute a debit card charge. And you should. Federal law gives you some pretty powerful protections against everything from outright fraud to frustrating billing errors, so you're definitely not helpless when a transaction goes sideways.

Your Guide to Disputing a Debit Card Charge

That jolt of seeing an unexpected charge on your bank statement is something we've all felt. The good news? There’s a clear path to getting your money back, and it’s backed by a federal law called Regulation E. Think of this rule as your safety net for any electronic payment, especially those from your debit card.

The whole process might seem intimidating at first, but it really just boils down to a few key actions. Knowing how to navigate it is half the battle, and the secret sauce is always the same: act fast and get your evidence in order.

Common Reasons for a Dispute

First things first, you need to figure out exactly what kind of problem you’re dealing with. Is it a charge from a company you’ve never even heard of? Or maybe you paid for something that never showed up at your door or was completely different from what you ordered online.

The "why" behind your dispute really shapes how you should approach it. For instance:

- Unauthorized Transaction: This is classic fraud—someone used your card details without your permission.

- Billing Error: This bucket includes all sorts of mishaps, like being double-charged, seeing the wrong amount, or getting billed for a subscription you know you canceled.

- Goods or Services Not Received: You paid for it, but the merchant never delivered. Simple as that.

Pinpointing which category your issue falls into makes it much easier to explain the situation clearly to both the merchant and your bank. A well-defined problem is a problem halfway solved.

The entire card dispute process can feel like a lot to take on, but every step is there to protect you. Before we get into the nitty-gritty, let’s quickly break down the most common scenarios and the right first move for each. This will give you a solid starting point.

Common Debit Card Disputes and Your First Step

Think of this table as your cheat sheet. Find your situation, and you'll know exactly what to do first to get the ball rolling.

Knowing where to start removes a ton of stress. In almost every case that isn't obvious fraud, a quick, polite message to the merchant can resolve the issue without needing to involve the bank at all.

Know Your Rights When Disputing a Debit Card Charge

When you spot a funky charge on your debit card statement, knowing your rights is the first step to feeling in control. Your main backup comes from a federal law called the Electronic Fund Transfer Act (EFTA), which is put into action through something called Regulation E.

Think of Regulation E as the official rulebook for electronic payments. It's not just a bunch of legal jargon; it’s a practical safety net that gives you specific rights and tells your bank exactly what they need to do. The law is on your side, and understanding a few key parts of it makes a world of difference when you're trying to get your money back.

The Power of Regulation E

So, what does Regulation E actually do for you? It lays out the ground rules, setting important timelines and responsibilities for both you and your bank. It's the reason you can confidently say, "Yes, I can absolutely dispute this charge."

Here are the most important protections it gives you:

- A Clear Deadline: You have 60 days from the date your bank sends your statement to report an error or a transaction you didn't authorize. This is a hard deadline, so acting fast is a must.

- Prompt Investigation: Once you flag a problem, your bank has to get to work. They are legally required to investigate your claim, report their findings, and fix any errors within a set timeframe.

- Limited Liability: Your financial responsibility for fraudulent charges is limited, especially if you report the problem right away. The faster you act, the less you're on the hook for.

This setup ensures you have a real process to follow and that your bank is legally obligated to take you seriously. It fits into the bigger picture of your overall consumer protections, which you can learn more about in this guide to your general chargeback rights.

Why Time Is Everything with Debit Cards

Here’s the biggest difference between debit and credit card disputes: when you use a debit card, that money is gone from your bank account instantly. It's your cash, and it's missing.

With a credit card, you’re spending the bank’s money, which you just pay back later. This tiny distinction has a huge impact on the psychology and urgency of a dispute. Since it's your cash that has vanished, the stakes feel a lot higher, making a swift response even more important.

The key takeaway is simple: with debit card disputes, the clock starts ticking the moment the transaction happens. Don't wait around for the issue to resolve itself—take immediate action to protect your funds.

Clearing Up a Common Myth

There's a stubborn myth out there that winning a debit card dispute is nearly impossible. Many people believe the protections are weaker than those for credit cards, but that’s not the whole story. While the processes are a bit different, Regulation E provides strong, enforceable rights for consumers.

Interestingly, disputes are actually less common with debit cards. Recent chargeback statistics reveal that credit cards had a chargeback ratio of 7.19%, while debit cards came in significantly lower at 5.93%. This makes debit cards a more secure payment method from a dispute frequency standpoint, and you can dig into more chargeback statistics on PayCompass.com to see the full breakdown.

Your success in a dispute doesn't come down to luck. It comes down to following the process correctly, providing clear evidence, and acting within the established timelines. Your rights are solid, and if your claim is legitimate, you have a very good chance of getting your money right back where it belongs.

How to File a Debit Card Dispute That Gets Results

Knowing you can dispute a charge is one thing. Actually filing a dispute that gets your money back? That's another beast entirely. A winning dispute isn't about luck; it's about having a clear, organized game plan. And before you even think about picking up the phone to call your bank, there's one step you absolutely shouldn't skip.

It's simple: contact the merchant directly.

This might feel like the last thing you want to do, especially when you're annoyed. But a quick phone call or a polite email can often clear things up in minutes. Many so-called "errors" are just simple misunderstandings or system hiccups, and believe me, businesses would much rather fix it for you than get tangled up in a formal bank dispute.

Besides, banks tend to look more favorably on customers who've already tried to work it out with the merchant. It shows you've done your homework and that escalating to a dispute is your last resort, not your first instinct.

Arm Yourself with Evidence

If you’ve already tried the merchant route (or if the charge is obviously fraudulent), it's time to put on your detective hat. Your mission is to gather every single piece of evidence related to that transaction. The more proof you have, the stronger your case will be.

Think of it like building a case file for a lawyer. You want to hand the bank a story so clear and well-documented they have no choice but to side with you. Don't leave anything out.

Here's a checklist of what you should be looking for:

- Receipts and Invoices: This is your foundational proof. It shows exactly what you were supposed to be charged for. A detailed breakdown can be incredibly persuasive. If you're not sure how to structure one, you can learn how to create a flawless itemized receipt template.

- Email Confirmations: Hunt down that order confirmation, any shipping notifications, and all other emails you got from the merchant.

- Communication Records: Screenshot any chats or emails you've exchanged. If you called them, jot down the date, time, and the name of the person you spoke with. A detailed log shows you’ve been proactive.

- Photos or Videos: Did you receive a damaged or completely wrong item? Pictures are undeniable proof. Take clear photos from a few different angles to really show the problem.

This isn't just busywork. This collection of evidence is the ammunition your bank will use to fight on your behalf. A well-prepared case is incredibly difficult for a merchant to argue against.

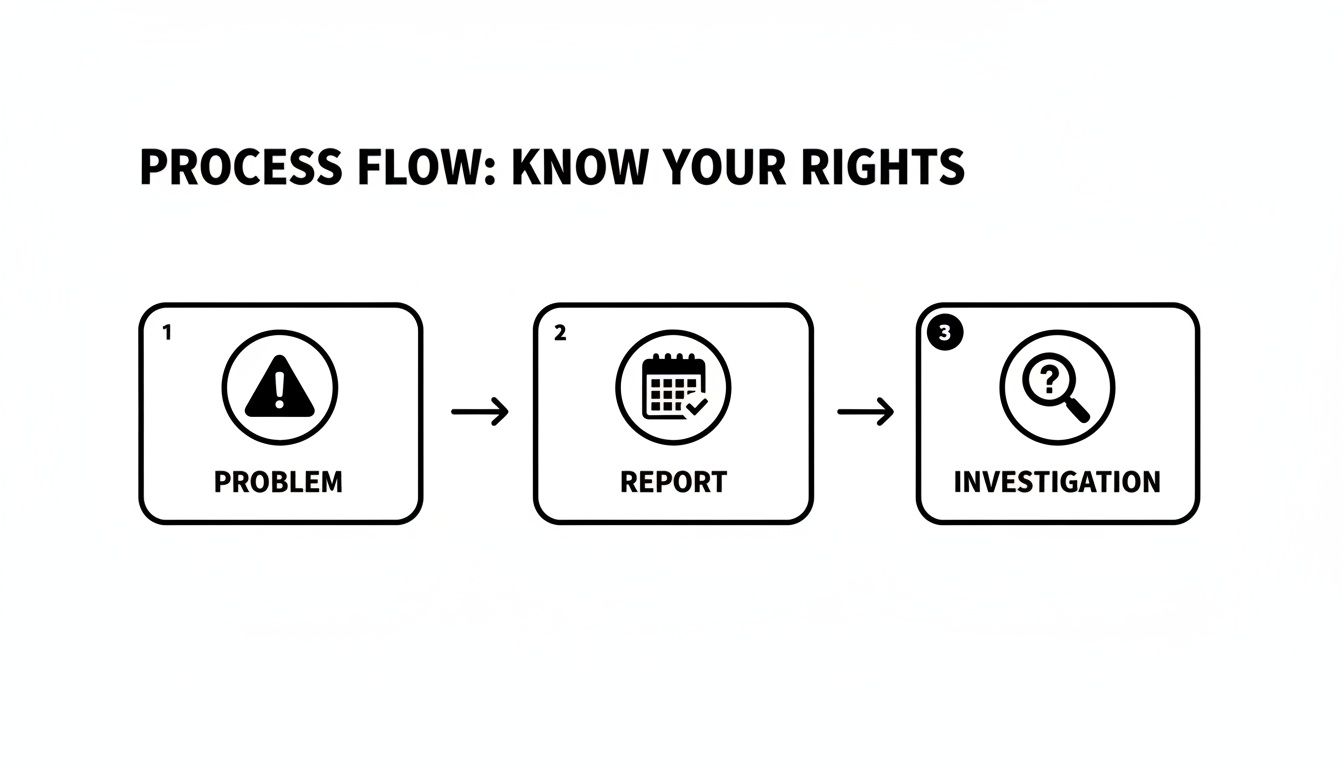

This simple flow chart breaks down the key stages of a dispute, from identifying the problem to the bank's investigation.

As you can see, moving from a problem to a resolution involves clear, sequential steps that put you in control.

Contacting Your Bank the Right Way

With your evidence file ready, it's time to officially file the dispute. Most banks give you a few ways to get the ball rolling, so you can pick what works for you.

You can usually start a dispute by:

- Making a Phone Call: This is often the fastest way to get the process started and speak directly with a representative.

- Using the Online Portal or App: Many banks let you report a bad transaction right from their online banking platform or mobile app.

- Sending a Formal Letter: It's a bit old-school, but sending a written dispute via certified mail creates a powerful paper trail that's hard to ignore.

No matter which method you choose, preparation is everything. Have your account information, transaction details (date, amount, merchant name), and your evidence file within arm's reach. When you explain what happened, be clear, stick to the facts, and avoid emotional language. For a great model on how to structure a compelling argument, check out this helpful example of a rebuttal letter.

Pro Tip: Your job isn't over once you file the dispute. Keep a meticulous record of every interaction with your bank. Write down the name of every person you speak to, the date of the call, and a quick summary of the conversation. This documentation is your safety net.

Let's walk through a quick example. Imagine you were double-charged for dinner. When you call the bank, you don’t want to just say, "I was overcharged."

Instead, try something like this:

"Hi, I'm calling to dispute a charge on my debit card. On October 25th, I was charged twice by 'The Corner Bistro' for $54.30. My statement shows two identical charges, but my receipt only shows one transaction. I have a copy of the receipt and my bank statement showing the duplicate charge."

This approach works because it's specific, factual, and immediately signals to the bank that you have the proof to back up your claim. It takes you from being just another frustrated customer to being a prepared advocate for your own money.

What Happens After You File a Dispute

So you've gathered your evidence and officially filed the dispute with your bank. What’s next? This part is mostly a waiting game, but knowing what’s happening behind the scenes can make it a lot less stressful. Once you hit "submit," the bank kicks off its formal investigation.

The first good news you’ll likely see is a provisional credit hitting your account. This is just the bank temporarily returning the disputed amount while they sort everything out. It’s a great feeling to see that money back, but remember, it isn't permanent just yet.

Under Regulation E, banks have to move quickly. They’re required to resolve claims within 10 business days. If the investigation gets complicated and they need more time, they can take up to 45 days, but only if they've already given you that provisional credit.

The Bank and Merchant Go Head-to-Head

With your claim filed, your bank steps into the ring on your behalf. They’ll contact the merchant's bank (known as the acquirer) and present your side of the story. This is where all the evidence you carefully gathered becomes absolutely essential.

The merchant then gets their chance to respond. They can either accept the dispute and let the refund stand, or they can fight back by providing their own evidence to prove the charge was legitimate. This back-and-forth is the core of the investigation. The timeline can vary, and if you want to dive deeper into the nitty-gritty, you can learn more about how long chargebacks take in our detailed guide.

This investigation phase is precisely why your initial documentation is so important. A clear, evidence-backed claim makes it much harder for a merchant to successfully challenge your dispute.

The Two Possible Outcomes

After the back-and-forth wraps up, your bank will let you know their decision. At the end of the day, it’s going to go one of two ways.

Scenario 1: Dispute Closed in Your Favor

If the bank sides with you—or if the merchant simply doesn't provide a compelling rebuttal—the dispute is resolved. That provisional credit you received becomes permanent, and the money is officially yours again. You’ll get a final notification, and the case is closed. Success!

Scenario 2: Your Claim Is Denied

On the other hand, the bank might side with the merchant. This usually happens when the merchant comes back with strong evidence, like proof of delivery with your signature or server logs showing you used a digital service. If your claim is denied, the bank will unfortunately reverse the provisional credit, taking the money back out of your account.

What to Do If Your Dispute Is Denied

Getting denied can feel like a major setback, but it’s not necessarily the end of the road. If you're certain the bank made the wrong call, you still have options to keep fighting for your money. Don't give up hope just yet.

Here are your next steps:

- Appeal the Decision: You can ask the bank to take a second look. This is especially effective if you have new evidence you can submit that wasn't part of your original claim.

- File a Complaint: If you feel the bank didn’t conduct a fair investigation as required by law, you can file a formal complaint with the Consumer Financial Protection Bureau (CFPB). The CFPB is a government agency that will review your case and make sure the bank followed all the proper procedures.

It's frustrating to get a denial when you know you're in the right. But staying persistent and using the appeals process can sometimes turn the outcome around. Knowing your rights is a powerful tool in any consumer dispute.

How Merchants Can Proactively Manage Disputes

For any business owner, that dispute notification is a gut punch. It’s not just the lost sale that stings; it's the mountain of paperwork, the wasted time, and the sheer frustration of it all. The best way to deal with a debit card dispute, hands down, is to stop it before it even starts.

This is all about shifting your mindset. Instead of just reacting to problems, you need to actively build a customer experience that prevents them from happening in the first place. This doesn't just cut down on disputes—it builds the kind of trust and loyalty that keeps customers coming back.

Building a Stronger Defense Against Disputes

The first line of defense is simply being clear. You'd be surprised how many disputes, especially those pesky "friendly fraud" ones, come from pure confusion. A customer sees a charge they don't recognize on their statement, panics, and immediately calls their bank.

You can get way ahead of this with a few simple but incredibly effective strategies:

- Use Clear Billing Descriptors: Make sure the name that pops up on a customer's bank statement is one they’ll instantly recognize. "ACMEWIDGETS" is a world away from a cryptic holding company name like "AW-INTERNET-PURCH."

- Offer Responsive Customer Service: Put your contact information everywhere. An easy-to-find, helpful support team can sort out an issue long before a customer even thinks about calling their bank.

- Maintain a Straightforward Return Policy: Keep your return policy clear, fair, and easy to find. When customers know they can easily send something back, they have very little reason to file a dispute.

Taking these steps creates a transparent and trustworthy experience for your customers. They feel more secure, which makes them far less likely to jump to a chargeback. You can dig into more strategies in our guide to effective chargeback protection for merchants.

Responding When a Dispute Arrives

Even with the best game plan, some disputes are just going to happen. It's an unfortunate reality of doing business today, and the numbers don't lie. Global chargeback volume hit a staggering 238 million transactions in 2023, and experts predict that number will soar to 337 million by 2026. That's a 41% jump in just three years. You can find more insights on these trends from the experts at Chargebacks911.com.

When a dispute does land on your desk, your response needs to be fast and backed with solid proof. The clock is ticking, and a slow or poorly documented reply is almost a guaranteed loss. This is where modern tools can completely change the game.

Platforms like this focus on "hands-free" automation, integrating directly with payment processors to fight disputes and get your money back for you.

Automating Your Dispute Management

Think about it: manually digging up receipts, shipping confirmations, and customer emails for every single dispute is a massive time sink. It pulls you away from what you should be doing—growing your business.

For many merchants, the real cost of a dispute isn't just the lost sale—it's the hours of administrative work required to fight it. Automation gives you that time back.

This is where AI-driven platforms like ChargePay are designed to step in and take over. By plugging directly into your payment systems, these tools can automatically:

- Analyze the Dispute: The second a dispute is filed, the system reads the reason code and knows exactly what kind of evidence is needed to build a winning case.

- Gather Compelling Evidence: It pulls all the critical data together—order details, shipping tracking numbers, customer IP addresses, communication logs—and weaves it into a cohesive response package.

- Submit the Response: The platform formats everything into a professional rebuttal letter and fires it off to the bank on your behalf, well within the strict deadlines.

This automated approach is a killer defense against friendly fraud, where a legitimate customer disputes a perfectly valid charge. The AI can instantly assemble the proof needed to show the transaction was real and the product was delivered, which can dramatically boost your win rate.

By turning to automation, you can save countless hours, recover a significant chunk of revenue, and keep your payment processor happy. It frees you up to focus on what you do best—running your business—while a smart system handles the messy work in the background.

Still Have Questions About Disputing Charges?

Even with a step-by-step guide, it's natural to have a few more questions rattling around. The debit card dispute process can feel a little intimidating, so let's clear up some of the most common sticking points. Think of this as the final piece of the puzzle to give you total confidence moving forward.

How Long Do I Have to Dispute a Debit Card Charge?

The clock starts ticking right away. Under federal law—specifically Regulation E—you have 60 days to report an unauthorized transaction or billing error. This isn't just a suggestion; it's a hard deadline that starts from the date your bank statement was sent.

If you miss that 60-day window, your bank might not be legally obligated to help, which could seriously jeopardize your chances of getting your money back. Some banks are a bit more flexible with their own policies, but you should always treat the 60-day rule as your absolute last day to act. My advice? Report any issue the moment you spot it.

Will Disputing a Charge Hurt My Relationship with My Bank?

Honestly, no. Filing a dispute for a legitimate reason is a standard part of banking. It won't get you on your bank’s bad side. They are legally required to investigate these claims and have entire departments dedicated to handling them.

That said, the process is designed for genuine problems—think fraud, duplicate charges, or merchants not delivering what they promised. If a bank sees an account filing a constant stream of weak or unfounded disputes, it might raise a red flag. But as long as you're using the system as intended, you have absolutely nothing to worry about.

Think of the dispute process as a built-in feature of your account, not a complaint against your bank. It’s a tool they provide to help you protect your money, and they expect you to use it when necessary.

What If the Merchant Refuses to Give Me a Refund?

This happens more often than you'd think, and it can be incredibly frustrating. But this is exactly what the dispute process is for. If you’ve already tried to sort things out with the merchant and hit a brick wall, that’s your cue to bring in the bank.

When you file your dispute, make sure to lead with the fact that you already tried to resolve it directly. Show them any emails, chat logs, or even notes from your phone calls. This context is essential because it shows you did your due diligence. Your bank will then take over and act as the mediator.

Is It Better to Dispute with a Debit or Credit Card?

While both cards offer solid consumer protections, there's a key difference that makes people feel safer with credit cards. When you dispute a credit card charge, the money in question is the bank's, not yours. Your actual cash isn't tied up during the investigation.

With a debit card, the money comes directly out of your checking account, and you're waiting for it to be returned. However, the protections under Regulation E are very strong. The most important thing isn't which card you used, but how fast you report the problem. Whether it's debit or credit, immediate action is what really drives a successful outcome.

Managing chargebacks can feel overwhelming, but it doesn't have to be. With ChargePay, you can automate the entire dispute process, saving time and recovering lost revenue effortlessly. Learn how ChargePay can protect your business.

.svg)

.svg)

.svg)

.svg)