When you hear the term credit card AVS, it stands for Address Verification Service. In simple terms, it’s a fraud prevention tool that checks if the billing address a customer types in online matches the address their card-issuing bank has on file. Think of it as a quick, automated first line of defense for your e-commerce store.

What Is Credit Card AVS in Simple Terms

Imagine AVS as a bouncer at the door of your online shop. When a guest arrives at an exclusive event, a security guard checks their ID against the guest list. The guard isn't doing a full background check; they're just making sure the name on the ID matches the name on the list. It’s a simple, fast confirmation.

AVS works pretty much the same way. When a customer hits "buy," AVS doesn't get into their whole life story. It just compares the numbers in the billing address—the street number and the zip code—against what the customer's bank has on record.

Why This Simple Check Matters

This split-second check is a big deal for online businesses. When you're handling card-not-present (CNP) transactions, you can't see the physical card or the person holding it. AVS gives you an immediate signal about whether a transaction looks legitimate before you even process the payment.

AVS is your first filter. Its entire job is to quickly flag orders where the address details don't line up with the bank's records. This gives you a powerful signal to either approve, manually review, or just decline a sale.

This single step is key to protecting your revenue and building a trustworthy store. By catching these mismatches early, you can massively cut down on fraudulent purchases and the expensive chargebacks that always follow.

The system is especially good at tripping up fraudsters who’ve managed to get their hands on stolen credit card numbers but don't have the matching billing address. You can learn more about the unique challenges of these sales in our guide to card-not-present fraud.

While AVS isn't a silver bullet, it's an absolutely essential layer in any good fraud prevention strategy. It helps you make smarter, data-driven decisions in real-time, all without creating friction for your legitimate customers at checkout.

How an AVS Check Works During Checkout

So, your customer is ready to buy. They fill out their info, click that final button, and an incredibly fast—but important—security check kicks off behind the scenes. This entire credit card AVS process happens in the blink of an eye, completely invisible to the shopper.

Think of it as a smooth digital conversation happening between several key players, all working to verify that the person making the purchase is legit.

This journey starts the moment your customer hits “submit” on their payment details. The information they entered, specifically the billing address and zip code, gets bundled up with the card number and sent on a secure, high-speed trip through the payment network.

The whole thing follows a clear, four-step path that’s over in less than two seconds.

The Four Steps of an AVS Check

- Customer to Merchant: It all begins on your checkout page when the customer types in their billing address. Your website then passes this information to your payment gateway, whether that’s Shopify Payments, Stripe, or PayPal.

- Gateway to Card Network: The payment gateway securely sends the address details and the transaction request over to the right card network—think Visa, Mastercard, or American Express.

- Network to Issuing Bank: From there, the card network forwards the information to the bank that actually issued the customer's credit card. This is where the real check happens.

- Bank Sends Response Code: The issuing bank takes the numeric parts of the address (the street number and zip code) and compares them against what it has on file. It then fires back a single-letter AVS response code to your gateway, signaling a match, a partial match, or a total mismatch.

This lightning-fast check provides an immediate risk signal. Your payment system then uses this code, along with other fraud filters, to decide whether to approve the charge. It’s a critical step that happens before any money is actually captured. You can see how this fits into the bigger picture in our guide on how to pre-authorize a credit card.

You can picture it like a quick conference call. Your gateway calls the card network, which patches in the bank. The bank gives a quick "yes," "no," or "maybe," and hangs up. It’s all automated and happens almost instantly.

Based on that response code, the rules you’ve set up in your store take over. A full match gets an immediate green light. A mismatch, on the other hand, might trigger an automatic decline or flag the order for a quick manual review. This entire sequence is designed to protect you from fraud without slowing down legitimate sales.

Understanding AVS Response Codes

When a customer hits that "buy" button, a lot happens in just a few seconds. Your payment system sends the transaction details to their bank, and almost instantly, you get a reply. Part of that reply is a single-letter AVS response code.

Think of it as a quick thumbs-up or thumbs-down from the bank about the billing address the customer entered. Getting this code is just step one. Knowing what it means—and what to do about it—is how you actually protect your business from fraud.

Each code is a signal telling you how risky the transaction might be. A perfect match? That’s a green light. A complete mismatch? That's a huge red flag waving right in your face, telling you to hit the brakes. The trick is to see these codes as clues in a bigger investigation, not as the final word. They help you build a real-time risk profile for every single order.

Decoding the Most Common AVS Signals

While there are dozens of AVS codes out there, you’ll really only see a handful on a regular basis. The most important thing is to understand the difference between a full match, a partial match, and no match at all. This is the foundation for setting up smart fraud rules in your payment gateway.

Some codes are crystal clear, but others live in a gray area that might need a second look.

For example, a partial match could be an honest mistake from a good customer who just moved, or it could be a fraudster working with stolen, incomplete information. How you handle these situations is what makes or breaks your credit card AVS strategy.

This kind of layered thinking is central to modern fraud prevention. It's not just theory, either. Companies that use advanced AVS platforms have seen a 60% drop in address-related fraud and achieve a staggering 97.5% match accuracy across different countries. You can find more details about global address verification on shuftipro.com.

AVS Codes and Recommended Actions

To make smart, fast decisions, you need a game plan for each AVS response. A full match or a total mismatch are easy calls. It's the partial matches that require a bit more finesse. This is where you have to balance stopping fraud with not accidentally blocking legitimate customers—a frustrating experience known as a false decline.

Here’s a quick-reference table to help you understand what the most common codes mean and what you should probably do about them.

Common AVS Response Codes and What They Mean

AVS is a fantastic first line of defense, but it's even more powerful when you pair it with other security measures. Check out our guide on what 3-D Secure authentication is to learn about another crucial tool that adds an extra lock to your digital storefront. By creating smart rules based on these codes, you can put much of your fraud prevention on autopilot and get back to growing your business.

The Limitations of AVS You Need to Know

While the Address Verification Service is a powerful first line of defense, it's not a silver bullet for fraud. Think of it like a basic lock on your front door—it's great for stopping casual opportunists, but a determined professional will find a way around it. Understanding where AVS falls short is critical to building a fraud prevention strategy that actually works.

One of the biggest hurdles is geography. AVS works like a charm in the U.S., UK, and Canada because the banking systems there are fully on board. But once you start selling internationally, things get dicey. Many issuing banks outside these regions don't support AVS, which means you'll get a response code saying the check was unavailable. If you rely only on credit card AVS for global sales, you're stuck between a rock and a hard place: either block legitimate international customers or risk letting fraudsters slip through.

When AVS Falls Short

Even in countries where AVS is fully supported, it has its blind spots. For instance, a sophisticated fraudster who has stolen a complete identity—card number, CVV, and the correct billing address—will sail right through an AVS check without raising any flags. This is exactly why you can never depend on AVS alone.

Then there’s simple human error, which can cause perfectly good transactions to get declined. We've all been there. Common slip-ups include:

- Formatting Issues: A customer types "Apartment 10" when their bank has "#10" on file. Mismatch.

- Recent Moves: Someone just moved and their bank hasn’t caught up with their new address yet. Mismatch.

- Typos: A simple slip of the finger on a street number or zip code is all it takes. Mismatch.

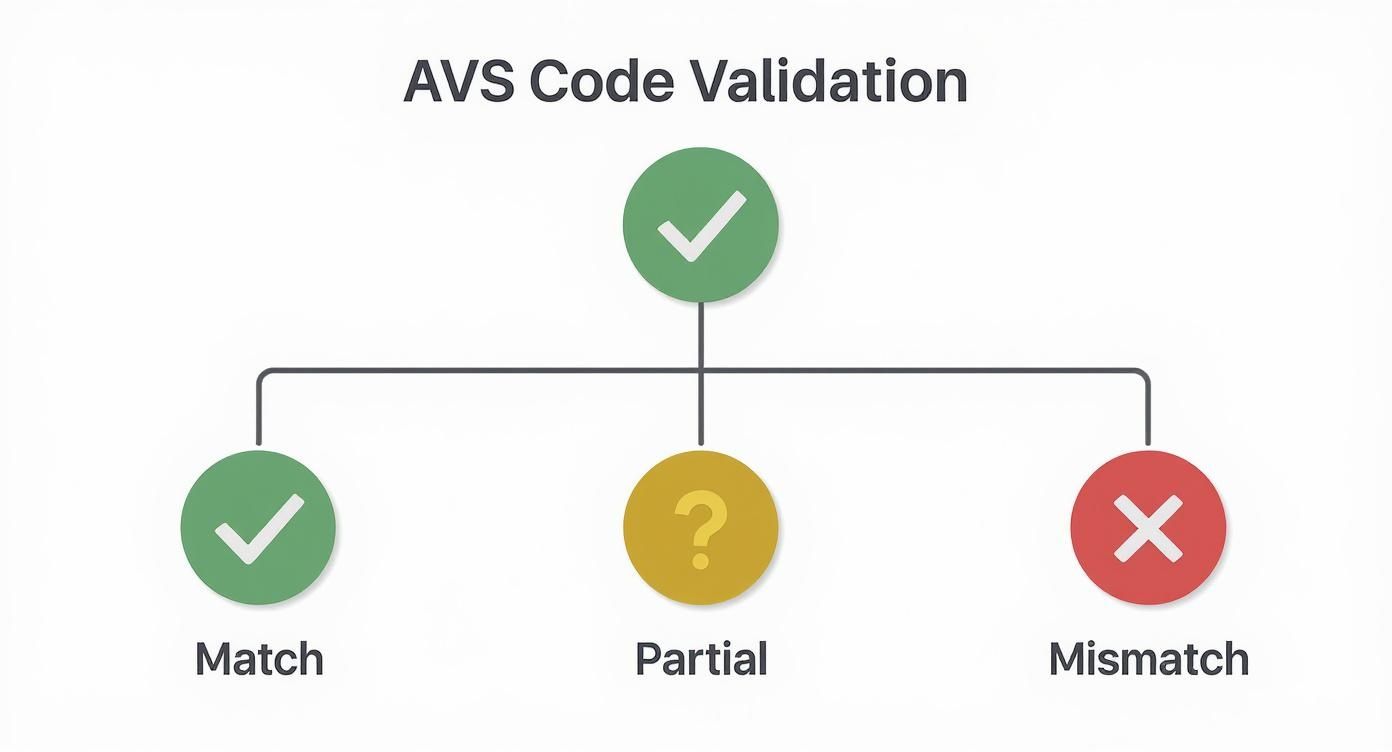

These false declines frustrate good customers and can cost you sales. This flowchart gives you a simple visual of how AVS sorts transactions into matches, partial matches, and mismatches.

As you can see, only a perfect match gets a clear green light. Everything else requires a closer look.

A Layer, Not a Fortress

All these limitations show why AVS should only be one layer in your security setup, not the entire fortress. Credit card fraud is a massive global problem, with projected losses expected to hit $38.5 billion by 2027. While AVS is a helpful tool, the fact that global payment fraud tripled between 2011 and 2020 proves that criminals are constantly improving their tactics.

AVS is excellent at catching low-effort fraud, but it's not designed to stop skilled attackers. It provides a signal, not a verdict.

To truly protect your business, you need to think in layers. Combining AVS with other tools like CVV checks, 3D Secure, and intelligent fraud analysis software creates a much stronger defense. This multi-layered approach is the foundation of any solid chargeback fraud prevention strategy that can stand up to modern threats.

Building a Complete Fraud Prevention Strategy

While AVS is a fantastic first line of defense, relying on it alone is like locking your front door but leaving all the windows wide open. A truly solid security plan layers multiple tools together, creating a defense that’s much harder for fraudsters to crack.

Think of AVS as the foundation of your fraud prevention house. It's essential, but you still need to build the walls and add the roof. The goal is to combine different verification methods that check different things. For instance, AVS confirms the billing address, but it has no way of knowing if the person placing the order actually has the physical card in their hand. That’s where other tools come into play, each adding another piece to the puzzle.

Creating a Multi-Layered Defense

To build a stronger barrier against fraud, you need to add more checkpoints to your checkout process. This multi-layered approach makes it incredibly difficult for criminals to sneak through, even if they manage to get past one of your defenses.

The most effective strategies pull together several key tools:

- CVV Verification: This checks the 3 or 4-digit code on the back of the card. A successful CVV match is a strong signal that the customer physically has the card.

- 3D Secure (e.g., Visa Secure, Mastercard ID Check): This adds an extra authentication step where the customer must verify their identity directly with their bank, usually with a password or a one-time code sent to their phone.

- IP Geolocation: This tool simply checks if the customer's IP address is in the same country as their billing address. A big mismatch is a major red flag.

Imagine this: an order comes in and passes the credit card AVS check perfectly. But then, the CVV check fails, and the IP address is from a completely different continent. That tells you to hit pause and investigate immediately—something AVS alone would have missed entirely.

This kind of comprehensive setup is quickly becoming the standard. As technology has evolved, companies have started launching AI-driven suites to make AVS more accurate. This shift is also being pushed by new regulations, with 42 jurisdictions now requiring address checks as part of their e-KYC (Know Your Customer) rules.

The overall effectiveness of your fraud prevention, including how you implement AVS, often comes down to strong leadership. For those with experience in this space, it's worth noting the growing demand for payments leadership roles.

Ultimately, a layered strategy is the only reliable way to cut down on chargebacks and protect your revenue. To see how all these pieces fit together, check out our complete guide to fraud prevention for ecommerce.

Got Questions About Credit Card AVS? We’ve Got Answers.

Even after you get the hang of AVS, a few practical questions always seem to pop up. Think of this as the go-to spot for those "what if" moments. We'll tackle the most common questions we hear from merchants who are using the Address Verification Service every day.

Does Using AVS Cost Extra Money?

Generally, no. AVS is a standard feature baked into most payment processors like Stripe, PayPal, and Shopify Payments. The cost is so small that it’s usually just rolled into your normal transaction processing rate, so you won’t ever see it as a separate line item on your bill. It's just considered a fundamental part of doing business securely.

Can a Legitimate Transaction Fail an AVS Check?

Absolutely, and it happens more often than you'd think. A perfectly good customer might fail a credit card AVS check for some very simple, human reasons:

- They just moved and haven't gotten around to updating their billing address with their bank.

- A simple typo in the street number or zip code. We've all been there.

- Using a slightly different address format (like typing out "Street" instead of "St.").

This is exactly why you shouldn't automatically decline every single transaction that doesn't get a perfect match. A smarter approach is to use those partial match codes as a signal—a little flag that tells you to take a closer look at the order for any other potential red flags.

Is AVS the Same as the CVV Code?

Nope, they're two different security sidekicks working together to protect your store.

AVS checks the customer's billing address to confirm they know where their card statements are sent. The CVV (Card Verification Value) is that little 3 or 4-digit code on the card itself, which helps prove the customer actually has the physical card in their hand.

When you use both AVS and CVV checks, you're building a much stronger wall against fraud than if you were just relying on one.

Where Do I Find My AVS Settings?

AVS is usually switched on by default on platforms like Shopify or with processors like Stripe. If you want to tweak the rules, you can typically find them in your payment settings or fraud prevention dashboard. This is where you get to decide how your store handles transactions with partial or no matches—for example, you can set it up to automatically decline them or just flag them for a quick manual review.

Even with the best fraud prevention tools in place, you can't stop every single dispute. When chargebacks do happen, ChargePay uses AI to automatically fight them on your behalf, recovering lost revenue without you having to lift a finger. Learn how ChargePay can boost your win rate and protect your bottom line.

.svg)

.svg)

.svg)

.svg)