So, what exactly is a debit card dispute? Put simply, it’s when a customer skips your return policy and goes straight to their bank to demand their money back.

This isn't like a simple return. It's a formal process that instantly pulls the money out of your account. On top of that, it usually slaps you with extra, non-refundable fees, no matter who wins.

What Debit Card Disputes Mean For Your Business

When a customer kicks off a debit card dispute, they’re telling their bank that a charge was fraudulent, incorrect, or completely unauthorized. This single action triggers an official investigation by the bank, which immediately reverses the transaction and gives the customer a provisional credit.

For you, the merchant, this isn't just a lost sale. It's a direct, immediate hit to your cash flow.

Think of it this way: a normal return is a conversation between you and your customer. You work it out together. A dispute, on the other hand, is a formal complaint where the bank becomes the judge, and you’re automatically considered guilty until proven innocent. The entire burden of proof is on you to prove the transaction was legitimate.

The Immediate Financial Impact

The fallout from a dispute is much bigger than just the original sale amount. Each one comes with its own penalty, creating a snowball effect that can seriously hurt your finances.

- Lost Revenue: The most obvious hit is the loss of the sale itself. That money is yanked right out of your merchant account.

- Chargeback Fees: Your payment processor will hit you with a separate, non-refundable fee for every single dispute filed against you. These typically run from $15 to $100, and you have to pay this fee even if you win the case.

- Operational Costs: Fighting a dispute eats up time and resources. Your team will spend hours digging up evidence, writing responses, and tracking the case—time that could have been spent growing the business.

These costs add up fast. A single $50 sale can easily turn into a $150 loss once you factor in the lost product, shipping costs, and the chargeback fee.

For merchants, a debit card dispute is more than a transaction reversal; it's a costly administrative process that directly drains revenue and operational resources. Ignoring them is not an option if you want to protect your bottom line.

Ultimately, a high dispute rate can also poison your relationship with your payment processor. If too many disputes are filed against your business, you can get labeled "high-risk." This often leads to higher processing fees or, in a worst-case scenario, the termination of your merchant account entirely. Understanding the true weight of debit card disputes is the first step toward building a solid defense and protecting the revenue you’ve worked so hard to earn.

The Journey Of A Debit Card Dispute

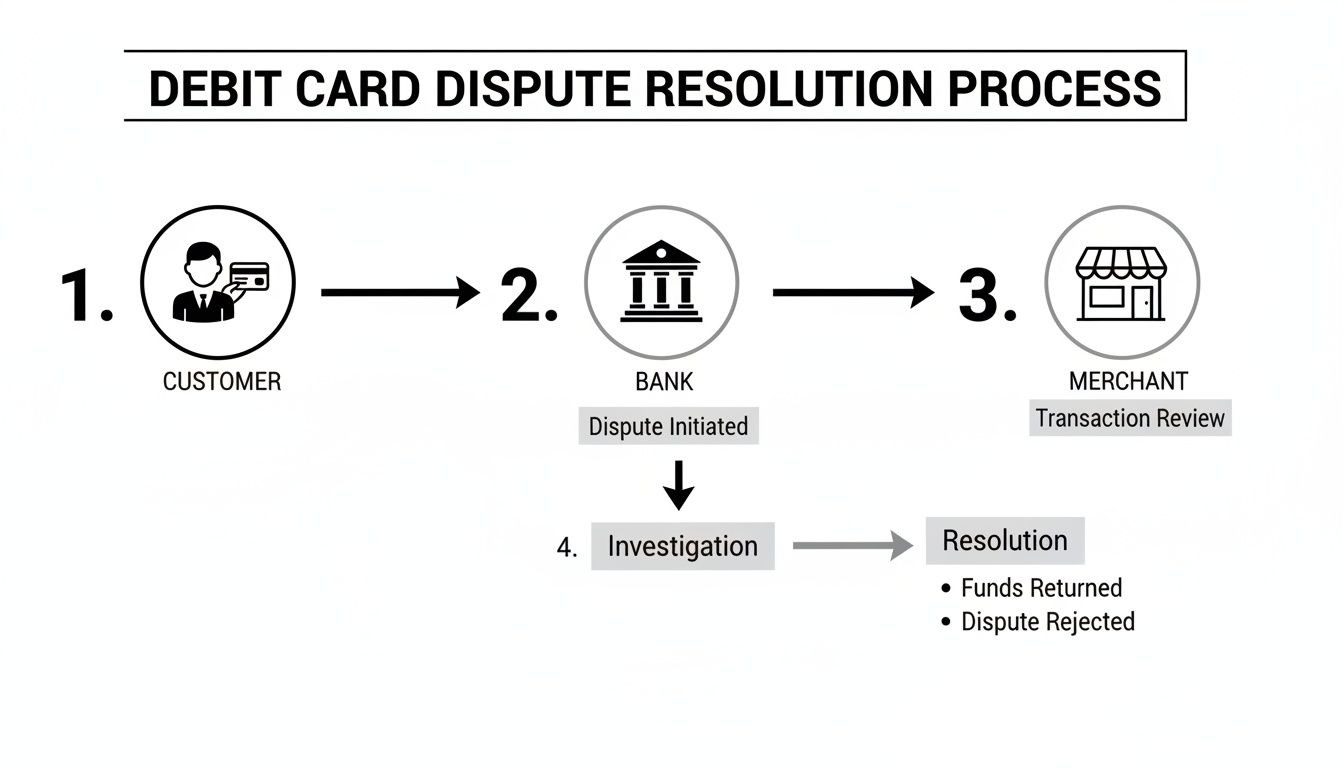

When a customer disputes a debit card charge, it sets off a complex, time-sensitive chain reaction that happens almost entirely behind the scenes. Think of it like a formal message traveling through a sophisticated postal system, with each stop adding another layer to the process. For you, the merchant, understanding this journey is critical—it tells you where you fit in and why acting fast is so important.

The whole thing starts the moment a cardholder calls their bank—the issuer—to report a problem with a transaction. This could be anything from a charge they don't recognize to a product that never showed up.

The issuer then takes a look at the customer's claim. If it seems legitimate, they file a formal dispute through the card network (like Visa or Mastercard) and give the customer a temporary credit. This is the point when the money is pulled from your account, often before you even know there's an issue.

From The Bank To Your Business

Once the card network gets the dispute, its job is to play middleman. It routes all the information over to your bank or payment processor, which we call the acquirer.

The acquirer is the institution that gives your business the merchant account needed to accept card payments. When they receive the dispute, they officially notify you, assign it a chargeback reason code, and pass along all the details. This is when the problem officially lands on your doorstep.

This flowchart breaks down the typical path a debit card dispute takes from start to finish.

As you can see, the process is a multi-step relay involving the customer, their bank, and your business, with strict rules governing every handoff.

The Clock Is Ticking

This is where the real pressure begins. The moment you're notified, a strict timeline kicks in. Depending on the card network, you usually have between 20 to 45 days to respond with compelling evidence that proves the transaction was legitimate. This formal response is called representment.

A debit card dispute isn't a simple back-and-forth. It's a regulated process with multiple players and non-negotiable deadlines. Missing your window to respond means an automatic loss, no questions asked.

If you don't respond in time, or if your evidence isn't strong enough, the temporary credit the customer received becomes permanent. You lose the sale, the product, and you're still stuck paying a non-refundable chargeback fee. The sheer volume of these cases is staggering. In 2023, global chargeback volume hit 238 million disputes—a clear signal of the growing headaches in e-commerce.

Merchants on platforms like Shopify or using gateways like PayPal and Stripe often bear the brunt of these conflicts, and data suggests they only win about 45% of the cases they fight.

But if you submit a strong response and win, the funds are returned to your account. This entire cycle, from initial complaint to final decision, is exactly why a deep understanding of the card dispute process is so essential for protecting your revenue. It turns a confusing ordeal into a manageable series of steps.

Understanding Why Customers File Disputes

To successfully fight a debit card dispute, you have to get inside your customer's head and figure out why they filed it in the first place. For a moment, forget the long, confusing list of reason codes that banks use. In the real world, just about every dispute you'll ever see boils down to one of three simple categories.

Think of yourself as a detective arriving at a crime scene. Your first job is to figure out what kind of case you’re dealing with because that will dictate your entire response. Was it a clear-cut crime, an honest mistake, or something much more complicated?

Category 1: True Fraud

This one’s the most straightforward. True fraud, often called criminal fraud, is exactly what it sounds like: a customer's debit card details were stolen and used by a criminal without their permission. The cardholder is a legitimate victim here, and the purchase was completely unauthorized.

For example, a thief might lift a physical card from a wallet, use a skimming device at an ATM to clone card information, or buy stolen card numbers off the dark web. When they use those details to buy from your store, the real cardholder is right to dispute the charge. They never made it.

Category 2: Merchant Error

This next category covers disputes that pop up because of a mistake or miscommunication on your end. While these errors are almost always unintentional, they create a frustrating experience for the customer, leaving them feeling like their only option is to call their bank. The customer is real, the purchase was legitimate, but something went wrong along the way.

These are often the most preventable types of disputes. Before you start looking at more complex reasons, it's always worth asking: "Did we mess something up?"

Fortunately, since these issues start on your end, they are also the easiest to fix and prevent from happening again.

Category 3: Friendly Fraud

This is the trickiest—and by far the most common—category you'll deal with. Friendly fraud is when a legitimate customer disputes a valid charge they absolutely made. It’s not "friendly" at all for you; it's a huge and growing problem that blurs the line between a simple mistake and outright deception.

Friendly fraud isn't driven by criminal intent like true fraud. Instead, it's fueled by convenience, confusion, or a case of buyer's remorse. The customer made the purchase, got the product, and disputes the charge anyway.

This can happen for a few reasons:

- Buyer's Remorse: The customer regrets their purchase and decides it’s just easier to file a dispute than to go through your official return process.

- Family Member Purchase: A child or spouse uses the card without asking, and the main cardholder doesn't recognize the transaction. Think of a teenager buying $100 worth of in-game currency on their parent's debit card.

- Simple Forgetfulness: The customer genuinely forgot they bought something or, again, doesn’t recognize your business name on their statement.

This problem has spiraled into a massive drain on businesses. Chargeback misuse and friendly fraud now account for up to 75% of all disputes, costing U.S. merchants over $170 billion every year. A huge driver is simple convenience; a recent survey in the 2025 Cardholder Dispute Index found that 76% of consumers would rather dispute a charge with their bank because it feels faster and easier than contacting the merchant directly.

Getting a handle on these three core categories is your first step toward building a powerful defense. When you can correctly identify the root cause—whether it’s true fraud, your own mistake, or a case of friendly fraud—you can gather the right evidence and dramatically improve your odds of winning. For a deeper dive, you can explore the various reasons for a chargeback and how to spot each one.

How To Build A Winning Dispute Response

When a debit card dispute lands in your account, it's easy to feel like you're already on the back foot. But that notification isn't a final verdict; it's your cue to step up and defend your revenue. Putting together a winning response, a process called representment, is all about systematically gathering and presenting compelling evidence to prove the transaction was legitimate.

Think of yourself as a detective building a case. Your job isn't just to say the charge was valid. It's to present such a solid pile of proof that the customer's bank has no choice but to rule in your favor. A messy, incomplete response just won't do the trick. You need to deliver a clear, powerful rebuttal.

Gathering Your Core Evidence

Every rock-solid dispute response starts with good documentation. The more relevant details you can dig up, the stronger your case becomes. For every single dispute, you should immediately start pulling together a core set of documents.

Here's your essential evidence checklist:

- Order Confirmations: This is the original receipt or invoice you sent the customer, showing exactly what they bought, when, and for how much.

- Customer Communications: Pull up any emails, support tickets, or chat logs you have with the customer. This is gold for proving a history of interaction and can easily poke holes in claims about not receiving an item or being unhappy.

- Billing Information: You need to show that the billing address the customer entered matches what their bank has on file.

- Terms of Service: A simple screenshot showing the customer checked the box agreeing to your terms, return policy, or subscription rules at checkout can be surprisingly powerful.

This first wave of evidence lays the groundwork, proving an order was placed and paid for. From here, you’ll add more specific proof that's tailored to what you actually sell.

Tailoring Evidence To The Product Type

Not all proof is created equal. The knockout evidence for a physical product is totally different from what you'd use for a digital download. Customizing your evidence package is absolutely critical to winning.

For physical products, your best friend is proof of delivery. And I mean more than just a tracking number.

- Shipping Confirmation: The email or notification you sent the customer with their tracking info.

- Proof of Delivery: A screenshot from the carrier's website (think FedEx or USPS) that clearly shows the package was delivered to the customer’s address. If you have signature confirmation, even better.

- Photos of the Delivered Package: Many carriers now snap a photo of the package on the customer’s porch, which is fantastic, hard-to-refute evidence.

For digital goods or services, the game changes. You need to prove digital access and usage, not physical delivery.

- IP Address Logs: Data showing the IP address that downloaded the product or accessed the service. If it matches the customer's general location, that's a huge point in your favor.

- Server or Activity Logs: Any evidence showing the customer logged in, downloaded files, or used the service after the purchase is compelling proof.

- Welcome Emails: Show that the customer received their access credentials or download links right after they paid.

This tailored approach hits the most common dispute reasons head-on, making your response much harder to ignore.

Customizing Your Response To The Dispute Reason

Once you have your evidence pile, the final step is to weave it all into a story that directly shoots down the customer's specific claim. Think of this as your closing argument. Just dumping a bunch of files won't work; you have to connect the dots for the bank investigator.

A winning dispute response is not just a collection of documents; it's a clear, concise story supported by irrefutable evidence. You must directly address the reason for the dispute and prove it false.

If the claim is "Product Not Received," you lead with your shipping and delivery confirmation. Make it the star of the show. Start with the tracking number and the final "delivered" status from the carrier.

For a "Fraudulent Transaction" claim, your entire focus should be on identity verification. You need to highlight every security check the customer passed at checkout.

- AVS (Address Verification System) Match: Show that the street number and ZIP code they typed in matched what the bank has on file.

- CVV Match: Prove the three- or four-digit security code from the card was entered correctly.

- IP Address Match: If the IP address of the person placing the order is in the same city as the billing address, it makes a fraud claim look pretty weak.

Organizing your evidence is just as crucial as collecting it. Start with a sharp, to-the-point rebuttal letter that sums up your case, then attach your supporting documents in a logical sequence. To see how to structure this, check out this helpful example of a rebuttal letter that breaks down the key components.

By creating a repeatable, evidence-first process, you can face every debit card dispute with confidence and dramatically boost your chances of winning.

Practical Ways To Prevent Disputes From Happening

Fighting debit card disputes is a necessary part of business, but the best way to win is to stop them before they even start. Think of it this way: proactive prevention isn't just about dodging fees. It's about protecting your time, keeping customers happy, and building a stronger, more resilient business.

The good news? The most effective strategies are often simple tweaks to your daily operations. You don't need a massive budget or a dedicated team to see a real drop in your dispute rate. It all boils down to two things: clarity and communication.

Sharpen Your Communication

So many disputes are born from simple confusion. When a customer feels surprised or misled, their first instinct is often to call their bank for a quick fix. You can get ahead of this by making every touchpoint crystal clear.

- Write Ultra-Clear Product Descriptions: Go way beyond the basic specs. Use high-quality photos and videos, list accurate dimensions, and detail all the materials. If you sell clothes, a detailed size guide is non-negotiable for preventing those "not as described" claims.

- Make Your Policies Impossible to Miss: Your return, refund, and shipping policies should never feel like they're hidden in the fine print. Link to them from your website's header, footer, and right on the product page. A customer who understands the return process is far less likely to file a dispute.

- Use a Recognizable Billing Descriptor: A confusing charge on a bank statement is a one-way ticket to a dispute. Make sure your billing descriptor is your store’s name—or a clear version of it—not some generic code from your payment processor.

Offer Stellar Customer Support

Great customer service is your absolute best defense against friendly fraud and simple merchant errors. When a customer knows they can reach you easily and get a fast, helpful answer, they have zero reason to escalate things to their bank.

The easier you make it for a customer to ask you for a refund, the harder it is for them to justify filing a dispute. Make your support channels obvious, responsive, and empathetic.

Beyond just solving problems, proactive engagement builds goodwill. For example, implementing effective strategies for maximizing customer retention with a small business loyalty program can foster the kind of positive relationships that prevent small issues from ever becoming disputes.

Strengthen Your Checkout Security

While you can’t stop every instance of true fraud, you can absolutely make your store a much harder target for criminals. A few basic security checks at checkout are essential for any online merchant. These tools help confirm that the person making the purchase is actually the cardholder.

The two must-haves are:

- Address Verification System (AVS): This tool checks if the billing address the customer enters matches what the card-issuing bank has on file.

- Card Verification Value (CVV): This requires the customer to enter that three- or four-digit security code on the back of their card, proving they physically have it.

These simple checks are your first line of defense. They also give you powerful evidence if you do have to fight a fraud-related debit card dispute.

Let's be real: chargeback volumes are climbing. Global figures are projected to jump from 261 million in 2025 to 324 million by 2028—a 24% increase. With merchants only winning about 20% of the cases they fight, prevention is more critical than ever.

By combining clear communication, easy-to-reach support, and solid security, you create an environment where disputes are simply far less likely to happen. For an even deeper dive into defending your business, check out our complete guide to chargeback prevention for more strategies to protect your bottom line.

Putting Your Dispute Management On Autopilot

Let's be honest. For any business that's starting to see real growth, trying to fight every single debit card dispute by hand is a fast track to burnout.

It’s tedious, painstaking work. A single missed deadline or one forgotten piece of evidence means an automatic loss. Those small mistakes start to pile up, costing you money you simply can't afford to lose. As your order volume grows, the administrative weight of just managing disputes becomes a serious drag on your entire operation.

This is where you have to modernize. It’s time to move beyond juggling spreadsheets and setting calendar reminders. The solution is automated chargeback management.

What Is Automated Dispute Management?

Imagine a smart assistant working for you 24/7, handling the entire dispute process from the moment it lands until it's resolved. That's the core idea behind automation. These tools plug directly into your e-commerce platform, like Shopify, and your payment processors, whether that's Stripe, PayPal, or another provider.

When a new dispute comes in, the system instantly kicks into gear.

Instead of you having to stop everything to dig through order histories, customer emails, and shipping records, the software automatically gathers all the relevant evidence. It pulls up order details, grabs customer communications, and finds delivery confirmations in seconds.

This hands-off approach turns chargeback management from a frantic, reactive chore into a streamlined, automated workflow. The system doesn't just collect data; it analyzes the dispute and uses AI to build the strongest possible case on your behalf.

How Automation Boosts Your Win Rate

The real magic of automation is its ability to create a perfect, professional response, every single time. An automated system doesn't get tired, distracted, or make careless mistakes. It knows precisely what evidence to include based on the specific dispute reason code provided by the bank.

- It Gathers the Right Evidence: The software instantly pulls critical data like AVS/CVV match results, IP address logs, and shipping confirmations to create a rock-solid evidence package.

- It Writes a Professional Rebuttal: Using AI, the system crafts a clear, concise rebuttal letter that presents your case in the exact format that banks expect and prefer.

- It Never Misses a Deadline: Automation guarantees your response is submitted well within the required timeframe, completely eliminating the risk of losing a winnable dispute due to a simple oversight.

This level of precision and speed is almost impossible to replicate manually, especially as your business scales. Merchants who switch to these tools often see a dramatic increase in their win rates, recovering revenue that would have otherwise vanished.

The key benefit of automation is turning a time-consuming cost center into a hands-off system that actively protects your revenue. It allows you to focus on growing your business, not on fighting endless paperwork.

By putting your dispute management on autopilot, you reclaim countless hours and vital resources. The system handles the tedious details, so you can concentrate on what you do best: serving your customers and building your brand. To learn more about how this technology works, check out this complete guide to automated chargeback and dispute management using AI.

Got a Few More Questions About Debit Card Disputes?

Even with a solid game plan, you're bound to have a few questions pop up about debit card disputes. We've pulled together the most common ones we hear from merchants to help clear up any lingering confusion. Think of this as your quick-reference guide to reinforce what you’ve learned.

What’s the Real Difference Between a Debit Card Dispute and a Credit Card Chargeback?

Honestly, for you as the merchant, they feel almost identical. In both scenarios, money gets yanked directly from your account, and you get hit with a fee. The process on your end is pretty much the same.

The main difference is on the customer's side of the fence. A debit card dispute is tied to actual funds in their checking account, while a credit card chargeback is filed against their credit line. But when it comes to the rulebook written by the card networks, the process for fighting them is virtually the same.

How Long Do I Have to Respond to a Dispute?

This is where the clock is your biggest enemy. You typically have a very strict window of 20 to 45 days to get your response submitted, though this can vary depending on the card network and your processor.

Miss this deadline, and it's an automatic loss. It's non-negotiable. The money is gone for good. This is exactly why having a fast, organized system in place isn't just nice—it's essential.

A word of caution: Never refund the customer directly after a dispute has been filed. It's a common mistake, but it won’t close the case. You’ll end up losing the original transaction amount and the separate refund you sent.

If I Win a Dispute, Do I Get the Chargeback Fee Back?

Unfortunately, no. The moment a dispute is filed, most payment processors charge a non-refundable administrative fee, usually somewhere between $15 and $100. This fee covers their cost of handling the back-and-forth.

So, even when you put up a great fight and win—getting the original transaction amount back—that chargeback fee is gone for good. This simple fact makes dispute prevention your single most powerful and cost-effective strategy.

Ready to stop losing revenue to manual errors and missed deadlines? ChargePay uses AI to automate your entire dispute response process, boosting your win rate and recovering lost funds while you focus on your business. Protect your bottom line today at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)