You’ve probably heard the term credit card chargeback, but what is it, really? Think of it less like a standard refund and more like a formal dispute process—a transaction reversal forced by a customer's bank. It’s a consumer protection measure that pulls money directly out of your business account when a customer contests a charge.

Unlike a simple, friendly refund between you and a customer, a chargeback is a much bigger deal. It involves banks, card networks, and a formal investigation, and it always comes with penalties for your business.

What Are Credit Card Charge Backs and Why They Matter

Let's paint a picture. A customer is unhappy with their purchase, and for whatever reason, they can't—or don't want to—work it out with you directly. So, instead of asking you for their money back, they call their bank to dispute the charge.

That single phone call kicks off the chargeback process. The customer’s bank essentially steps in as a referee between you two. The bank immediately gives the customer a provisional credit and then yanks those funds right out of your merchant account, often before you even know what's happening. You don't just lose the sale; you're now roped into a costly, time-consuming formal dispute that you have to fight to win back your money.

The Key Players in a Chargeback Dispute

To get a handle on chargebacks, you first need to know who's involved. It's not just you and the customer. Every dispute brings a few key parties to the table, each playing a distinct role:

- The Cardholder: This is your customer—the one who made the purchase and is now disputing it.

- The Issuing Bank: This is the cardholder's bank (think Chase or Bank of America). They're the ones who kick off the chargeback for their customer.

- The Acquiring Bank: This is your bank, the institution that gives you a merchant account so you can accept card payments in the first place.

- The Merchant: That’s you! It's your job to gather the evidence and prove the transaction was legitimate.

This chain of communication can be frustratingly slow and tangled, which is why responding quickly and correctly is so important. For a deeper dive, check out our guide on what a bank chargeback is and how it affects businesses.

More Than Just a Refund

It’s easy to think of a chargeback as just another refund, but that's a dangerous misconception. In reality, it's far more serious and damaging to your bottom line.

A simple refund is a direct agreement between you and your customer. A chargeback, however, is a formal dispute adjudicated by banks, signaling that the customer relationship has broken down and introducing financial penalties.

The financial hit goes way beyond the lost sale. Every single chargeback piles on non-refundable fees, sucks up your team's valuable time, and can seriously damage your standing with payment processors.

And this problem is only getting bigger, especially with the boom in ecommerce. Global chargeback volumes are exploding. The number of cases worldwide is projected to hit a staggering 337 million by 2025, which is a 27% increase from 2022 alone. This trend makes one thing crystal clear: ignoring credit card chargebacks is a luxury no online business can afford.

The Hidden Costs of a Single Chargeback Dispute

It’s tempting to look at a chargeback and only see the lost sale. A customer disputes a $100 purchase, you lose $100, and that’s the end of it, right? If only it were that simple.

The reality is that the financial damage cuts much, much deeper. Treating chargebacks as just another “cost of doing business” is a mindset that will slowly bleed your profits dry. Every single dispute acts like a snowball, picking up extra costs and fees as it rolls downhill, leaving you with a loss far greater than the original transaction.

Beyond the Sale Price

So, what are you really paying for when a chargeback hits your account? It’s a painful stack of fees and losses that go way beyond the initial sticker price.

For U.S. businesses, the sting is particularly sharp. On average, merchants lose a staggering $4.61 for every $1 charged back. That figure doesn't just cover the lost sale; it accounts for all the compounding costs, from inventory to staff time.

This financial drain comes from several places:

- The Original Transaction Amount: The full sale price is immediately pulled from your merchant account.

- Non-Refundable Processing Fees: You already paid your payment processor to handle the sale, and you’re not getting that money back.

- The Chargeback Fee: Platforms like Stripe and PayPal tack on a separate, punitive fee just for the hassle of dealing with the dispute.

- Lost Product or Service: In most cases, you've already shipped the product or provided the service. You won't be getting that back, either.

Understanding how these individual costs stack up is the first step. You can get a more detailed look in our guide on what is a chargeback fee.

A Real-World Example

Let's break down how quickly the costs escalate with a simple $100 online sale. A customer buys a product, you ship it, and a week later, they file a chargeback. Suddenly, that $100 transaction becomes a major liability.

To really see the impact, let's lay out all the costs involved.

The True Cost of a Single $100 Chargeback

That single dispute instantly cost your business over $133, wiping out the profit from several other successful sales.

And honestly, this is a best-case scenario. It doesn't even touch on the operational costs—the hours your team spends digging up evidence, writing rebuttals, and tracking the case. When you multiply this by dozens or even hundreds of disputes a month, the damage to your bottom line becomes impossible to ignore.

Fighting chargebacks isn't just about winning back individual sales; it's a vital part of protecting the financial health of your entire business.

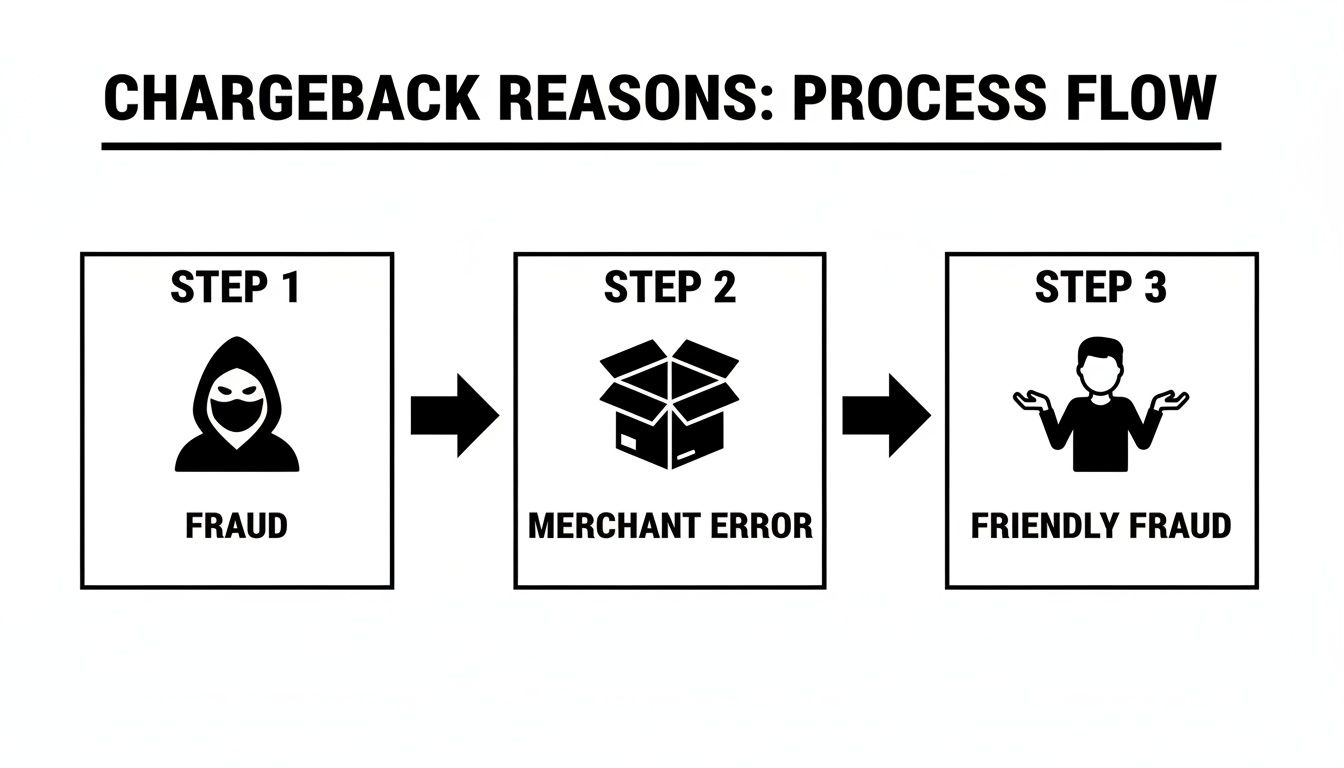

Common Reasons Customers Initiate Chargebacks

To win the chargeback fight, you first have to understand why it’s happening. Think of it like a detective showing up at a crime scene—you need to figure out the motive before you can solve the case. Not every dispute is a malicious attack on your business; many are just simple misunderstandings or honest-to-goodness mistakes.

But they almost always fall into one of three buckets. Each one calls for a totally different game plan, both for prevention and for fighting back. Once you can spot the root cause, you can stop wasting time and money on lost causes and start protecting the revenue that’s rightfully yours.

Merchant Error and Fulfillment Issues

Let's start with the most straightforward kind: chargebacks caused by preventable mistakes on your end. These are the classic "oops" moments that, if you don't get them under control, can snowball into some seriously expensive problems. Customers file these when they feel they didn’t get what they paid for, and honestly, they're usually right.

Common slip-ups include things like:

- Shipping the wrong product: They ordered a blue shirt, but a red one showed up.

- Incorrect size or quantity: The order was for a large, but a small arrived instead.

- Damaged goods: The item was broken in transit or just poorly packed.

- Duplicate billing: The customer was accidentally charged twice for one order.

These are frustrating experiences for any customer. If your return process is a nightmare to navigate, a chargeback becomes the path of least resistance. The good news? These are the easiest disputes to prevent. A little more quality control and clearer communication can go a long way.

The Problem of Friendly Fraud

This is where the lines get blurry. Friendly fraud happens when a real, legitimate customer disputes a purchase they actually made. It's not a stolen card situation; it's a customer misusing the chargeback system, whether they mean to or not.

Friendly fraud is the single biggest driver of disputes. It’s a situation where your actual customer disputes a charge they knowingly made, often due to buyer’s remorse, forgetting the purchase, or not recognizing your business name on their statement.

For example, a customer might not recognize your store's billing descriptor. If "Dave's Awesome Tees" appears on their statement as "DAT LLC," they might hit the panic button and report it as fraud. In other cases, maybe a family member used the card without asking, or the customer just has a case of buyer's remorse and sees a chargeback as an easier out than a standard refund. To get a better handle on what goes through a customer's mind, you can explore the various reasons for a chargeback in more detail.

Outright Criminal Fraud

Finally, we have criminal fraud—the kind you see in the movies. This is when a thief gets their hands on stolen credit card details and goes on a shopping spree in your store. When the actual cardholder spots the charge, they will, of course, file a chargeback. And they'll be 100% in the right.

Unlike friendly fraud, these disputes are impossible to win. You unknowingly processed a transaction without the true cardholder's permission. Your energy here isn't best spent fighting the chargeback itself, but on beefing up your fraud detection to stop these transactions from ever going through.

Chargeback rates vary wildly by industry, but a common thread is the rise of 'friendly fraud'—where legitimate customers misuse the system—driving about 75% of cases. The global average rate is 0.65%, but e-commerce retail sits higher at 0.95%, and digital goods soar to 1.85%. These disputes often arise from poor communication, complex refund policies, or simple billing descriptor confusion. Discover more insights about Mastercard's findings on chargebacks.

Your Step-By-Step Plan to Fight and Win a Chargeback

When that chargeback notification lands in your inbox, it's easy to feel a pit in your stomach. But this isn't the time to throw in the towel. With the right game plan, you can effectively challenge bogus claims and get back the money you rightfully earned.

This whole process of fighting a credit card chargeback has a formal name: representment. Think of it as your second chance—your opportunity to present your case again, this time armed with solid proof that the original transaction was completely legit. You're essentially telling your side of the story directly to the customer's bank.

Step 1: Assemble Your Evidence—Immediately

The clock starts ticking the second you get that notification. Payment processors like Shopify or Stripe give you a painfully short window to respond, often just 7-10 days. If you wait until the last minute, you're basically handing them an automatic win. You have to move fast.

The secret to a successful representment is simple: provide evidence that directly shuts down the customer’s claim. The exact documents you'll need will depend entirely on why they filed the dispute in the first place.

Knowing whether a chargeback came from actual fraud, a mistake on your end, or "friendly fraud" (when a customer disputes a valid charge) is key. It tells you exactly what kind of proof you need to start gathering.

Step 2: Tailor Your Evidence to the Claim

A generic, one-size-fits-all evidence packet just won't cut it. You have to customize your response to match the specific reason code provided in the chargeback notification. Every claim demands a different set of documents to be persuasive.

Your goal is to create an undeniable record of a valid transaction. The more relevant, clear, and specific your evidence is, the harder it will be for the issuing bank to side with its customer over you.

For instance, if the customer claims they never got their order, a signed delivery confirmation from the courier is your silver bullet. If they're arguing the product wasn't as described, you'll need screenshots of the product page, along with any customer service emails where you tried to make things right.

Let's break down what this looks like in the real world.

Essential Evidence Checklist by Chargeback Reason

When a chargeback hits, you need to know exactly what to grab. This table is your quick-reference guide for gathering the right proof for the most common claims, making sure you don't miss anything critical.

Having this kind of documentation ready to go makes the whole ordeal smoother and seriously boosts your odds of winning.

Step 3: Write a Clear and Concise Rebuttal Letter

All that great evidence needs a cover story. That's your rebuttal letter. It's a short, professional summary that walks the bank investigator through your evidence and spells out exactly why the chargeback is invalid. Keep it simple and stick to the facts. No fluff.

Your letter should briefly cover:

- What the customer ordered.

- The evidence you've attached to prove the transaction was valid.

- A clear conclusion stating why the charge should be reversed back to you.

Avoid emotional language or long, rambling stories about the customer. The person reviewing your case is sifting through hundreds of these a day; make their job easy by giving them a clear, logical, and evidence-backed argument. For more tips on crafting your response, you can learn more about how to win a credit card dispute and see how to structure your case for maximum impact.

Step 4: Submit Your Case Before the Deadline

Once your documents are gathered and your letter is written, submit the whole package through your payment processor's portal. Do one last check to make sure you've met all their formatting requirements and that everything uploaded correctly.

After you hit submit, the waiting game begins. The customer's bank will review everything you sent and make a final call, which can take several weeks. If you win, the money gets put back in your account—although that frustrating chargeback fee is almost never refunded.

Proactive Strategies to Prevent Chargebacks

Knowing how to fight a chargeback is important, but let's be honest—the best strategy is always prevention. Think of it this way: fighting a chargeback is playing defense after the other team has already scored. Preventing one is like running a perfect offense that keeps them out of your end zone entirely.

By getting ahead of potential problems, you can shut down disputes before they even start. This saves you an incredible amount of time, money, and headaches down the road. The goal is to build a business that’s naturally resilient to disputes, and that starts with clarity, communication, and top-notch service at every step.

Set Clear Expectations from the Start

A surprising number of disputes, especially the "friendly fraud" variety, boil down to simple confusion. When a customer sees a charge they don't recognize or feels a product missed the mark, a chargeback often feels like the easiest path to a solution.

You can head these issues off at the pass just by being crystal clear in your communications.

- Use a Recognizable Billing Descriptor: Make sure the name that pops up on your customer's credit card statement is one they'll immediately recognize. If your shop is "Dave's Awesome Tees," your billing descriptor shouldn't be a generic "DAT LLC." This one tweak can prevent a huge number of confused disputes.

- Write Detailed Product Descriptions: Don't leave anything to the imagination. Use high-quality photos from multiple angles, list the exact dimensions, and specify the materials used. The more accurate your descriptions are, the less room a customer has to claim the product was "not as described."

- Be Upfront About Policies: Your shipping, return, and refund policies need to be easy to find and even easier to understand. Hiding them in the fine print is a recipe for disaster, leaving you with frustrated customers who will turn to chargebacks when they feel backed into a corner.

Provide Outstanding and Accessible Customer Service

When a customer runs into a problem, your goal should be to make it ten times easier for them to contact you than it is to contact their bank. Your customer service isn't just a support function; it's one of the most powerful chargeback prevention tools in your arsenal.

The moment a customer feels they can't reach you or that you won't help them, they're already mentally drafting their dispute. Making your support team accessible and genuinely helpful transforms a potential dispute into an opportunity to build loyalty.

If a customer has to dig through your website just to find a contact number or waits days for a simple email response, they’re far more likely to give up and file a chargeback. Providing excellent support is a non-negotiable proactive strategy. To really sharpen your team's skills, look into mastering telephone customer service to resolve issues long before they escalate.

Strengthen Your Fraud Detection Measures

Finally, while merchant error and friendly fraud are the usual suspects, you can't ignore outright criminal fraud. The only way to deal with these transactions is to prevent them from ever being approved in the first place, stopping the inevitable chargebacks that follow.

Implementing robust fraud prevention tools is essential for any online business today. These systems can automatically flag suspicious orders based on a variety of risk factors, giving you a chance to manually review them before you ship the product and lose both the merchandise and the money.

Look for tools that analyze these key signals:

- AVS and CVV Mismatches: These are the basic, must-have checks that confirm the billing address and the card's security code match what the issuing bank has on file.

- IP Geolocation: An order placed from a high-risk country but shipping to a completely different one? That's a classic red flag that needs a closer look.

- Order Velocity: A sudden, unusual spike in orders from a single customer or IP address can be a strong indicator of fraudulent activity.

By weaving together clear communication, stellar service, and smart fraud tools, you create multiple layers of defense. This proactive approach doesn't just cut down your number of credit card chargebacks; it helps you build a stronger, more trustworthy business overall.

Automating Your Chargeback Defense with AI

When your business starts to take off, that slow trickle of credit card charge backs can quickly become a torrent. Suddenly, you're spending hours fighting every single dispute by hand—digging through order histories, pulling up tracking numbers, and trying to write the perfect rebuttal. It becomes a full-time job, pulling you away from what actually matters: growing your business.

This is exactly where automation comes in to change the game. Instead of treating every chargeback like an emergency you have to handle manually, you can use technology to build a defense system that works for you. Tools like ChargePay are built specifically to take over the entire representment process, using AI to fight and win on your behalf.

How AI Transforms Chargeback Management

Think of an AI chargeback solution as your expert paralegal, working 24/7. It plugs directly into your payment platforms like Shopify, Stripe, and PayPal, so the moment a dispute lands, the AI is on the case.

It instantly pulls together all the critical evidence needed to build a strong defense:

- Customer order history and all the little details

- Shipping confirmations and tracking numbers

- AVS/CVV match results from the transaction

- IP address logs and device information

From there, the AI analyzes the chargeback reason code and pieces together the most compelling evidence into a professional rebuttal letter. This whole dance happens in seconds, so you never have to worry about missing a response deadline. This shift from a reactive to a proactive stance is a total game-changer. To see how AI can also bolster other areas of your operations, check out what’s possible with AI customer support software.

The Tangible Benefits of Automation

The real beauty of automating your chargeback defense isn't just about saving a headache; it's about real results that hit your bottom line. We're talking about dozens of hours saved every single month—time you can now invest back into your products and customers.

Here’s a look at what an automated dispute dashboard offers, giving you a clear, real-time overview of every chargeback.

When all your dispute information is organized in one place, you can finally track your win rates and see exactly how much revenue you're recovering without lifting a finger.

Even more importantly, these AI systems are trained on data from millions of disputes. They know what evidence works best for every type of claim and every card network. This built-in expertise gives your win rate a serious boost, often recovering revenue you might have previously written off as a loss.

By handing this critical process over to automation, you get your time and money back. For a deeper look, check out our complete guide to automated chargeback and dispute management using AI.

Got Questions About Chargebacks? We’ve Got Answers.

Even when you think you have chargebacks figured out, new questions always pop up. It’s a confusing part of running a business, no doubt about it. Here are some quick, straightforward answers to the questions we hear most often from merchants.

How Long Do I Have to Respond to a Chargeback?

Officially, the card networks like Visa and Mastercard give you anywhere from 20 to 45 days to respond. But that number is dangerously misleading.

In reality, your payment processor—think Shopify, Stripe, or PayPal—sets its own, much shorter deadline. You’ll often only have 7-10 days to get your evidence submitted. They build in this buffer to make sure they have time to review and forward your case before the final network cutoff. If you miss your processor's deadline, you lose automatically. Speed is everything here.

If I Win a Chargeback, Do I Get My Money Back Right Away?

Winning feels great, but the money doesn't reappear instantly. Once the bank rules in your favor, it can take anywhere from a few business days to several weeks for the disputed funds to be returned to your account.

And here's the kicker: that initial chargeback fee your processor hit you with? You almost never get that back. Even when you win the dispute, that fee is gone for good.

This is exactly why preventing chargebacks from happening in the first place is always the best financial strategy. An ounce of prevention is truly worth a pound of cure.

What Is a Chargeback Ratio and Why Does It Matter So Much?

Your chargeback ratio is one of the most important health metrics for your business, and the card networks watch it like a hawk. It’s a simple calculation: the number of chargebacks you get in a month divided by your total transactions for that same month.

This little number is a huge deal for a few reasons:

- It’s a Risk Signal: To the card networks, a high ratio screams "risky business." It suggests you might have issues with fraud, customer service, or product quality.

- It Comes with Penalties: If your ratio creeps over the accepted threshold (usually around 0.9%), you can land in a monitoring program that comes with hefty monthly fines.

- It Can Be a Business Killer: If you can't get your ratio back down, the networks can revoke your ability to accept credit card payments entirely. For most online businesses, that’s game over.

Keeping a low chargeback ratio isn’t just about avoiding fees; it’s fundamental to keeping your business alive and well.

Stop letting complicated disputes drain your revenue. ChargePay uses AI to automate your entire chargeback defense, recovering up to 80% of your lost funds without you lifting a finger. Get started with ChargePay today.

.svg)

.svg)

.svg)

.svg)