American Express disputes scare Shopify merchants for one reason. They feel automatic. A customer clicks a button, funds disappear, and you’re left proving you didn’t do anything wrong.

That fear is expensive. At ChargePay, we’ve handled 200K+ disputes, recovered $10.8M+, and delivered a 92.4% win rate for merchants using Shopify. Those numbers come from our own platform data and they matter for one reason: fraud american express cases are beatable when you respond with the right evidence, in the right format, before the deadline.

Most merchants don’t lose because the customer was right. They lose because the response was late, generic, or missing the exact proof AmEx wanted. That’s fixable.

Winning the Fight Against American Express Fraud

American Express has a reputation for being tough. That part is true. But tough isn’t the same as unwinnable.

If you run a Shopify store, you need to stop treating AmEx disputes like random bad luck. They follow patterns. The cardholder makes a claim. AmEx assigns a reason. You either match that claim with hard evidence or you lose by default. That’s the system.

Why merchants lose money they could have recovered

Most store owners make one of three mistakes:

- They answer emotionally. You know the order was legitimate, so you write an angry rebuttal instead of a factual one.

- They send too little proof. A tracking number alone rarely tells the full story.

- They miss the response window. Once that happens, the case is usually over.

Practical rule: Treat every dispute like a document problem, not a fairness problem.

AmEx cares about evidence that can be verified quickly. Order details. Delivery records. Customer communication. Billing and shipping consistency. Refund policy acceptance. Usage or download logs for digital goods. If that proof exists, you have a real chance.

The right mindset for fraud american express cases

You don’t need to guess your way through this. You need a repeatable process. That starts with understanding how representment works and how to structure your response around the cardholder’s claim, not around your frustration.

If you want a deeper breakdown of how to build that workflow, read our guide to mastering chargeback representment.

The goal isn’t to fight every case blindly. The goal is to know which disputes are winnable, respond fast, and package your evidence so the reviewer doesn’t have to hunt for your point. Merchants who do that recover revenue. Merchants who don’t keep donating margin to chargebacks.

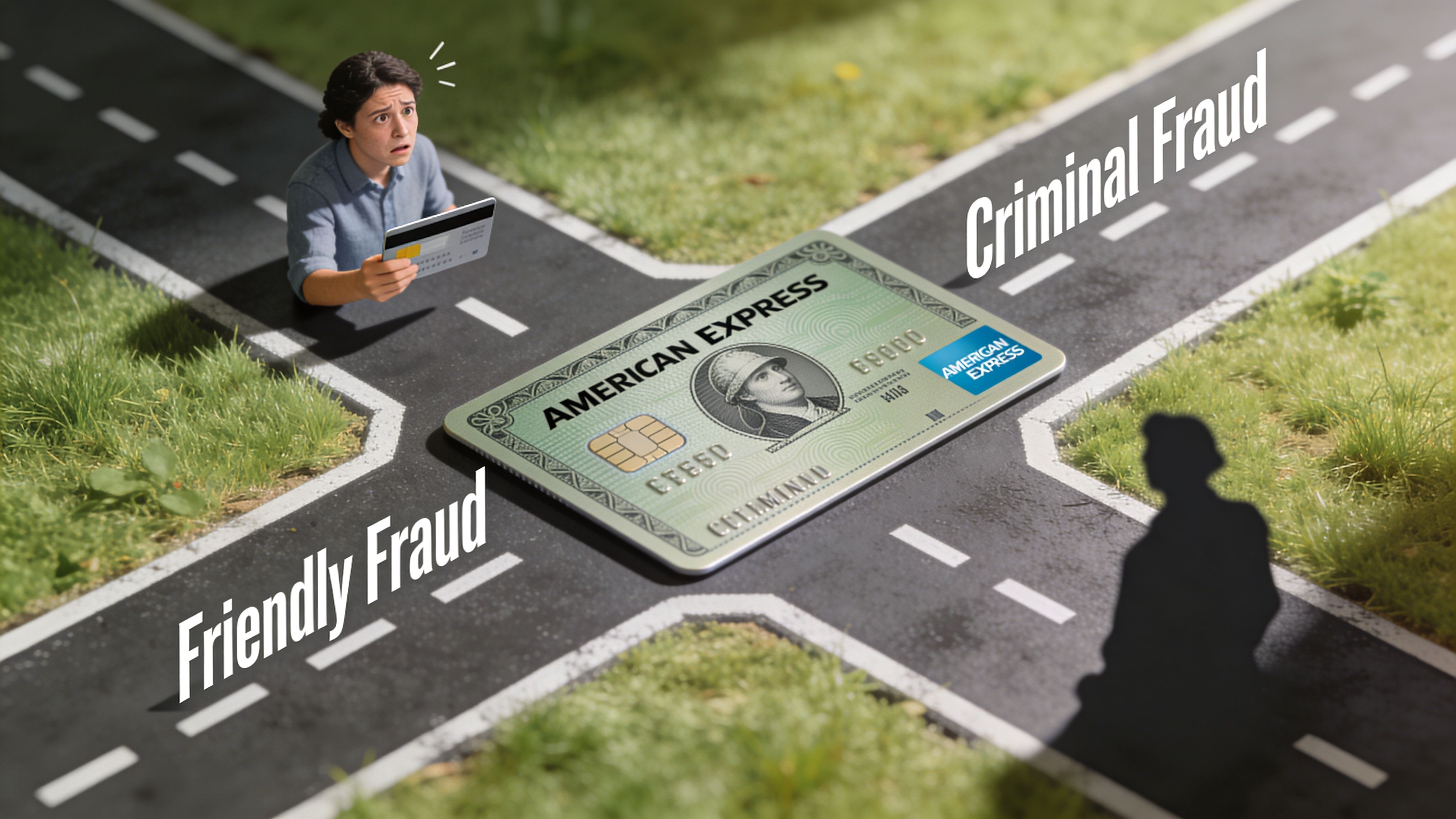

The Two Faces of American Express Fraud

Not all fraud looks the same, and that’s where merchants get burned. You can’t fight every AmEx dispute with the same template because the underlying problem changes the evidence you need.

Criminal fraud

This is the classic version. A stolen card or compromised account gets used to place an order. The cardholder didn’t authorize it.

For Shopify merchants, criminal fraud usually shows up in card-not-present orders with mismatched details, rushed shipping requests, odd buying behavior, or accounts that appear to exist only to place one order. American Express has also identified emerging fraud trends including bot-driven applications, social engineering scams, and synthetic identity fraud that mixes real and fake information into new credit profiles, which is why static fraud rules no longer work well enough on their own, as noted in American Express’s fraud trend update.

You should assume organized fraudsters test your checkout, your refund process, and your fulfillment speed.

Friendly fraud

This is the bigger headache. The customer placed the order, received the product, and then disputed the charge anyway. Sometimes they forgot the purchase. Sometimes a family member used the card. Sometimes they’re trying to get the item and the refund.

That’s not the same as criminal fraud. It’s closer to a customer using the banking system as a return shortcut.

Here’s the simple split:

| Fraud type | What actually happened | What usually helps you win |

|---|---|---|

| Criminal fraud | A bad actor used stolen payment details | Proof of risk checks, order validation, shipping controls, identity consistency |

| Friendly fraud | A real customer disputes a valid purchase | Proof of delivery, customer messages, refund policy acceptance, product usage or fulfillment records |

Why this distinction matters

If the card was stolen, your job is to show you screened the order carefully and fulfilled it in a commercially reasonable way. If the customer is committing friendly fraud, your job is to prove the purchase was valid and the cardholder benefited from it.

Those are different arguments. Merchants who mix them together lose.

When the customer says “I didn’t authorize this,” AmEx wants proof tied to identity and transaction legitimacy. When the customer says “I didn’t get it” or “I didn’t recognize it,” AmEx wants proof tied to fulfillment and clarity.

If you need a sharper breakdown between first-party abuse and true third-party theft, read our guide on friendly fraud vs chargeback fraud.

Red flags worth acting on

Before the dispute even happens, watch for patterns like these:

- Shipping pressure: The buyer wants overnight shipping to a risky or unusual address.

- Order mismatch: Billing and shipping details don’t line up and the customer can’t explain why.

- Communication gaps: The customer ignores verification emails but still demands immediate shipment.

- Synthetic behavior: New customer profile, high-value order, thin identity footprint, and no normal browsing history.

- Post-delivery silence: Everything looks fine until the dispute notice arrives with no prior support request.

Those signs don’t prove fraud. They tell you where to slow down and document everything.

Decoding AmEx Chargeback Reason Codes

AmEx reason codes look technical, but they’re really instructions. Each code tells you what story the cardholder told and what kind of proof AmEx expects from you.

If you answer the wrong question, you lose. That’s why merchants need a cheat sheet, not guesswork.

What reason codes are really saying

When AmEx sends a dispute, don’t focus on the code first. Focus on the accusation behind it.

- “I didn’t make this purchase.”

- “I never got the item.”

- “The product wasn’t as described.”

- “I was billed more than I agreed to.”

- “I canceled and still got charged.”

The code is just AmEx shorthand for those claims. Your response should read like a direct rebuttal with evidence attached.

For a broader breakdown of dispute triggers across card networks, review our guide on reasons for a chargeback.

Common American Express Chargeback Reason Codes for Merchants

| Reason Code | What It Means | How to Fight It (Required Evidence) |

|---|---|---|

| F24 | Card Member does not recognize the transaction | Order record, customer account details, device or session consistency if available, billing and shipping match, delivery proof, customer communication, clear descriptor explanation |

| F29 | Card Member says the charge was fraudulent or unauthorized | AVS/CVV result if available, order timeline, proof item shipped to customer-linked address, communication from the purchaser, account login history or repeat customer history if available |

| C08 | Goods or services not received | Carrier tracking, delivery confirmation, shipment date, signed delivery if available, customer acknowledgment, support messages confirming receipt or no complaint before the dispute |

| C04 | Goods or services were returned or refused but not credited | Return tracking, refund policy, return approval status, evidence item was not returned or return was incomplete, refund timeline if processed |

| C05 | Goods or services canceled but still billed | Cancellation policy, date of cancellation request, terms accepted at checkout, proof service had already started or order had already shipped |

| C02 | Credit not processed | Refund records, processing timestamps, proof credit was issued, communication showing the customer was informed |

| C14 | Paid by other means | Proof of original payment method, order ledger, duplicate payment review, communication confirming only one successful transaction |

| C18 | No show or car rental related claims that can overlap with reservation disputes in some cases | Reservation terms, cancellation window acceptance, usage logs, timestamps showing the customer used or missed the booking under agreed terms |

How to read the code without overthinking it

Use this quick filter:

- Fraud claim means identity and authorization evidence matter most.

- Fulfillment claim means shipping, delivery, or access logs matter most.

- Credit or cancellation claim means policy acceptance and refund records matter most.

Merchant shortcut: Your evidence should answer the exact claim in the first two pages. Don’t bury the key proof on page eight.

What a weak response looks like

A weak AmEx response usually includes a screenshot of the order, a tracking number with no context, and a short note saying the charge was valid. That’s not enough. It doesn’t explain what happened, when it happened, or why the cardholder’s claim fails.

A stronger response does three things:

- Builds a timeline

- Matches every exhibit to the reason code

- States the conclusion clearly

That’s the difference between “here are some files” and “here is documented proof the dispute should be reversed.”

How AmEx Investigates Disputes and Sets Deadlines

American Express moves fast once a cardholder files a dispute. If you wait around, you lose control of the case.

The timeline you need to respect

For merchants, the most dangerous part of the AmEx process is the response window. In practice, that window is often 20 days, and if you miss it, you usually hand the win to the cardholder.

Here’s the flow most Shopify merchants experience:

- Customer files a dispute

- AmEx notifies you or your processor

- You collect evidence

- You submit your response

- AmEx reviews both sides

- AmEx issues the decision

That sounds simple until you realize you’re collecting order data, shipping proof, and customer communication while still running your store.

How AmEx thinks about risk

American Express processes over $1.2 trillion in annual transactions and uses machine learning to analyze thousands of data points in milliseconds for each transaction, according to the Harvard Digital Initiative review of AmEx fraud systems. That same source notes that AmEx’s Enhanced Authorization tool lets merchants submit extra data such as IP address, email, and shipping address, and it has reduced fraudulent transactions by 60% for participating merchants.

That tells you something important. AmEx values structured, transaction-level evidence. Not opinions. Not long emotional explanations. Data.

What that means for your response

If AmEx uses dense transaction data to score risk, your dispute response should mirror that logic.

- Use dates and timestamps

- Show address consistency

- Include order and fulfillment milestones

- Attach proof that the customer interacted with the order or delivery

- Present the file in a clean sequence

The strongest response feels easy to verify. If the reviewer has to guess what your evidence means, you’ve already made the case harder than it should be.

If you want the exact timing details and submission windows that merchants regularly trip over, read our guide to American Express chargeback time limits.

The biggest deadline mistakes

Merchants rarely lose because they had zero evidence. They lose because they handled the evidence badly.

Common failures include:

- Submitting late: You had proof, but the case was already dead.

- Uploading partial records: Tracking without delivery details, or chats without timestamps.

- Ignoring the claim itself: You answered “item delivered” when the dispute was about cancellation.

- Relying on your processor to sort it out: Some processors pass along the notice, but they don’t build your case for you.

Treat every AmEx notice like a countdown. The moment it arrives, someone on your team should own the response.

Your Winning Response A Step-by-Step Guide

A good representment package does one job. It makes the reviewer comfortable ruling in your favor.

Start with a clean case summary

Don’t dump files into a portal and hope AmEx figures it out. Lead with a short rebuttal letter that includes:

- The dispute reason

- Your position in one sentence

- A timeline of purchase, fulfillment, and delivery

- A list of attached exhibits

Keep it tight. Professional beats dramatic every time.

Gather the evidence in the right order

Proof of order

Start with the Shopify order details. You want the full record, not a cropped screenshot.

Include the purchased items, order value, billing details, shipping details, date and time, and any customer account information tied to the order. If the customer is returning buyer behavior, note that too.

Proof of payment checks

If your checkout captured verification results, include them. AVS, CVV, and any internal fraud review notes help show that the order passed your controls at the time of purchase.

For fraud american express cases, this is especially useful when the cardholder claims they never authorized the transaction.

Proof of fulfillment and delivery

At this stage, most merchants either win or lose. Tracking alone is not enough unless it clearly shows the package reached the destination connected to the order.

Use:

- Carrier tracking pages: Show shipment acceptance, transit events, and final delivery.

- Delivery confirmation: Include signature or delivery photo if available.

- Address consistency: Match the destination to the order record.

- Fulfillment timestamps: Show when the order moved from payment to shipment.

If the package arrived and your file proves it clearly, don’t hide that in attachments. Put it in the first page summary.

Proof of customer interaction

Customer service logs are often the most underrated evidence in a chargeback response.

Add email threads, chat transcripts, support tickets, and any post-purchase messages. If the customer asked for shipping updates, requested a size exchange, or confirmed receipt, that directly undermines many disputes.

Here’s a useful walkthrough on how evidence packaging should look in practice:

Match your package to the dispute type

Not every dispute needs the same stack of documents.

For unauthorized transaction claims, prioritize identity consistency, verification results, shipping logic, and customer-linked activity.

For item not received claims, prioritize delivery proof, shipment confirmation, and any messages showing the customer knew the order was on the way.

For canceled or returned claims, prioritize your policy, the customer’s acceptance of that policy, and the actual return or cancellation timeline.

Write the rebuttal like an operator, not a victim

Your rebuttal letter should sound factual and calm. Something like this structure works well:

- State the transaction was valid

- Identify the order date and fulfillment date

- Explain the customer received or used the goods or services

- Reference the supporting exhibits by number

- Request reversal based on the attached evidence

Don’t rant about fraud. Don’t attack the customer’s character. Don’t paste your entire policy center into the response.

Build your internal checklist now

Create a repeatable checklist inside your team before the next dispute arrives.

- Order file ready: Full Shopify export or complete order screenshot set

- Fulfillment record saved: Tracking, carrier page, delivery proof

- Policy archive stored: Refund, return, cancellation, subscription, preorder, and shipping policies

- Comms centralized: Customer emails, chat, help desk, and SMS history in one place

- Submission owner assigned: One person accountable for deadlines

A chargeback response shouldn’t start from zero every time. The merchants who recover money consistently turn this into an operational process.

Advanced Prevention for Your Shopify Store

The cheapest chargeback is the one that never happens. If you’re only reacting after the dispute notice arrives, you’re already late.

Build friction where it matters

You don’t need to make checkout painful. You need to make fraud harder and buyer confusion less likely.

Start with basics inside Shopify and your payment stack:

- Require verification checks: Turn on CVV and AVS where available.

- Review high-risk flags manually: Don’t auto-fulfill suspicious orders just because revenue looks good.

- Use clear descriptors: A customer who doesn’t recognize your statement descriptor becomes tomorrow’s dispute.

- Send immediate order confirmation: Include product details, billing descriptor, and support contact info.

Use stronger authentication for risky orders

Fraud is changing fast. American Express has dealt with AI-generated deepfake audio and video used to impersonate executives and authorize bogus transactions, and those defenses now include multi-channel verification and behavioral AI, according to this analysis of the AmEx GBT deepfake attack and SafeKey 2.0. That same source says AmEx SafeKey 2.0, built on EMV 3-D Secure, can reduce friendly fraud chargebacks by 40-50%.

For Shopify merchants, the lesson is simple. Add stronger authentication where the risk justifies it. High-value orders, mismatched details, unusual velocity, and first-time buyers deserve extra scrutiny.

More authentication at the right moment is cheaper than losing product, shipping cost, and revenue to a preventable dispute.

Stop friendly fraud before it starts

A lot of friendly fraud starts with avoidable confusion. The customer doesn’t recognize the charge, forgets the purchase, or gets impatient before contacting support.

Fix that upstream:

- Send shipping updates proactively

- Make your return policy easy to find

- Answer support tickets fast

- Show expected delivery timelines clearly

- Use product pages that match what you ship

If you want a full operating playbook for reducing chargebacks before they happen, read our guide on chargeback prevention.

Keep better records than the fraudster

Fraudsters adapt. Disorganized merchants don’t.

Keep copies of policy pages by date. Save fulfillment evidence early. Archive customer communication. Tag suspicious orders for review. If a dispute hits weeks later, you should be able to rebuild the story fast without chasing screenshots across five tools.

Automate Your Wins with ChargePay

Disputes eat margin twice. You lose the order, then you lose staff time trying to recover it.

That manual grind is where Shopify merchants fall behind. Your team opens the notice, hunts through Shopify, pulls support logs, checks tracking, writes a rebuttal, uploads files, and repeats the process tomorrow. That is not a defendable operation. It is revenue leakage dressed up as admin work.

Payment processors see broad fraud signals, but merchants rarely receive them in a form they can use fast. As noted in Payments Dive’s reporting on AmEx fraud intelligence gathering, processors gather broad fraud trend signals while merchants often lack actionable intelligence about new attack patterns. You need your own system for turning store data into a strong response before the deadline expires.

What automation should do

Do not buy a dashboard and call it a strategy.

Good automation should read the dispute reason, pull the right Shopify order data, collect supporting evidence, build a usable representment package, and submit on time. If a tool cannot do those five jobs, it is adding software cost without fixing the work that causes losses.

ChargePay is a Shopify-focused chargeback management app built to handle that workflow. It automates evidence collection, prepares representment responses, and manages submission across the dispute lifecycle. According to ChargePay platform data, merchants using it have seen a 92.4% win rate across 200K+ cases, with $10.8M+ recovered, and the app carries a 4.9-star rating plus a Built for Shopify badge.

Why merchants switch from manual work

Manual processes fail in the same places over and over:

| Manual process problem | What it causes |

|---|---|

| Evidence lives in different tools | Slow responses and missing documents |

| No one owns the deadline | Preventable losses |

| Generic templates | Weak arguments that do not fit the dispute |

| Support and ops teams work separately | Incomplete timelines |

We see the same pattern constantly. The merchant has enough evidence to fight the case, but it is scattered across email, Shopify, tracking tools, and support platforms. By the time someone assembles it, the deadline is close or the response is too generic to win.

Automation fixes that by turning disconnected records into one case file. Your store data, fulfillment proof, customer communication, and policy evidence should move into the dispute response without manual chasing. That is the difference between reacting to AmEx fraud and building a repeatable system to beat it.

Your team should spend time shipping orders and helping customers, not acting as part-time chargeback analysts.

The standard you should demand

Whether you use software, an internal team, or an agency, require the basics:

- Fast intake

- Evidence matched to the claim

- Clear submission workflow

- Deadline control

- Reporting on outcomes

If your current process misses any of those, it is costing you money before AmEx even makes a decision.

If American Express disputes keep eating your margin, install ChargePay from the Shopify App Store. It is built for Shopify, rated 4.9 stars, carries the Built for Shopify badge, and works on a pay-per-win model. You only pay when recovered revenue comes back to your store.

.svg)

.svg)

.svg)

.svg)