Ecommerce fraud prevention is all about using the right strategies and tools to shield your online store from financial hits caused by cybercrime, like transactions made with stolen credit cards or bogus chargebacks.

Think of it as the digital security guard for your business. A solid prevention plan does more than just stop bad guys; it protects your revenue, keeps your customer data safe, and maintains the hard-earned trust you've built. The real trick is finding that sweet spot between iron-clad security and a smooth, hassle-free checkout for your legitimate customers.

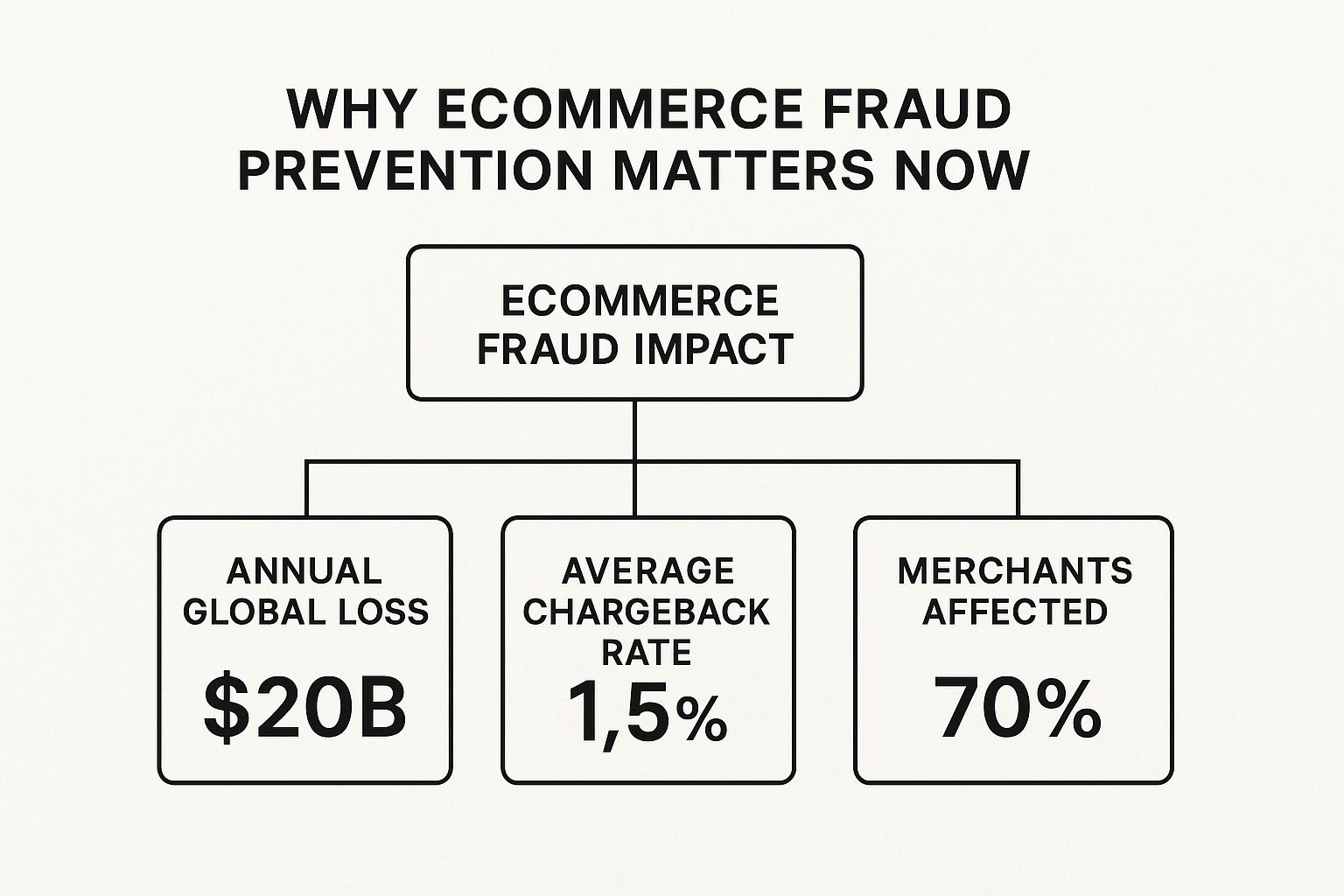

Why Ecommerce Fraud Prevention Matters Now

Welcome to the world of online selling, where every opportunity seems to come with a built-in risk. If you're running an ecommerce store, you’re not just moving products off a shelf. You’re a manager of payments, a guardian of customer data, and a builder of trust.

Unfortunately, this also paints a big target on your back for fraudsters who are constantly cooking up new schemes to exploit online businesses. The tough reality is that modern online fraud is way more sophisticated than just the occasional stolen credit card number.

Fraudsters are getting smarter, and their methods create a ripple effect of problems that go far beyond a single lost sale. When they strike, you're left dealing with:

- Direct Financial Losses: When a fraudulent purchase goes through, you're out both the product you shipped and the money from the sale. It's a double whammy.

- Costly Chargeback Fees: Banks slap you with significant fees for every transaction a customer disputes—even if you ultimately win the case. Rack up too many of these, and your payment processor might just cut you loose.

- Damaged Reputation: Fraud erodes customer trust. Once word gets out, even your most loyal buyers might think twice before entering their card details on your site again.

This infographic paints a pretty clear picture of the staggering financial blow ecommerce fraud delivers to merchants across the globe.

The numbers don't lie. This isn't some minor inconvenience; it's a major threat that affects the vast majority of online businesses.

The True Cost of Inaction

Ignoring fraud prevention is like leaving the front door of your shop wide open overnight. You might get lucky for a little while, but sooner or later, someone's going to walk in and take advantage.

The costs of doing nothing pile up fast. Beyond the immediate sting of a fraudulent sale, there's the operational headache of managing disputes and chargebacks. This eats up precious time and resources that you should be investing in growing your business.

Chargebacks, in particular, are a silent profit killer. A single fraudulent chargeback doesn't just reverse the sale; it tacks on a penalty fee, often doubling your initial loss.

Getting a handle on how these disputes work is the first step in fighting back. For a deeper dive, our guide explains in detail how chargebacks hurt businesses and what you can do about them. This guide is here to give you a clear, straightforward look at what’s at stake, making it obvious why you need a proactive strategy to protect your store and secure its future.

Recognizing the Different Faces of Fraud

To get a handle on ecommerce fraud, you first have to know what you’re looking for. Fraud isn’t just one thing; it's a whole collection of different schemes, and each one leaves its own clues. Think of yourself as a detective—learning to spot the signs is the first step to cracking the case.

When you understand these common tactics, vague threats turn into recognizable patterns you can actually do something about. This knowledge is your first line of defense, helping you spot suspicious activity before it hits your bottom line.

Fraudsters are a creative bunch, so let's break down the most common schemes you're likely to run into.

Common Ecommerce Fraud Types Explained

Here’s a quick-reference table to help you get familiar with the different types of fraud, what they typically look like in action, and how they can hurt your business.

Getting a feel for these categories is the first step. Now, let's dive a little deeper into how each one works.

Classic Credit Card Fraud and Chargebacks

This is the one most people think of when they hear "fraud." A criminal gets their hands on stolen credit card numbers—maybe from a data breach or a phishing scam—and uses them to buy something from your store. The real cardholder eventually spots the transaction and reports it to their bank.

That single phone call kicks off a chargeback, which forcefully yanks the payment back from your account. You're out the product you shipped, the money from the sale, and you get slapped with a penalty fee. It’s a triple-whammy for any merchant.

Friendly Fraud: A Deceptive Twist

Here’s where it gets messy. Friendly fraud (sometimes called first-party fraud) happens when a real customer makes a purchase but later disputes the charge, claiming it was fraudulent or they never authorized it. Sometimes it's a genuine mistake, but a lot of the time, it's a deliberate play to get something for nothing.

The customer might claim the package never arrived when it did, or that they simply don't recognize the charge on their statement. Because the order comes from a real customer with a legitimate card, this type of fraud is notoriously difficult to spot and fight.

It’s really important for merchants to know the difference here. While both scenarios end in a chargeback, their origins couldn't be more different. We break down the specifics in our article comparing friendly fraud vs. chargeback fraud, which will give you a much clearer picture of what you’re up against.

Account Takeover Fraud

Imagine a thief doesn't just steal a wallet but steals someone's entire identity to go on a shopping spree. That's pretty much what an account takeover (ATO) is. Fraudsters use stolen usernames and passwords—often scooped up from data breaches on other websites—to break into a real customer's account on your store.

Once they're in, they can wreak havoc:

- Make purchases using saved credit cards.

- Change the shipping address to their own drop point.

- Steal personal data or cash in loyalty points.

Because the transaction looks like it's coming from a trusted customer, it often sails right past basic fraud filters. This makes ATO a particularly nasty and effective threat.

Synthetic Identity Fraud

This is one of the more sophisticated schemes out there. Instead of stealing one person's identity, a fraudster acts like a mad scientist, piecing together a completely new, fake one. They'll combine real information (like a legitimate social security number) with fake details (like a made-up name and address).

They use this "synthetic identity" to patiently build a credit history, apply for cards, and eventually make huge fraudulent purchases before disappearing. It’s a long game, but it’s a nightmare to trace because there’s no single, real victim to report the crime.

The Broader Spectrum of Fraud

Beyond these core types, the ways criminals can exploit your business are always evolving. And it's not just a big-business problem. Fraud management is now a must-have for online businesses of all sizes, but smaller merchants are often the least prepared to deal with it.

It's also worth remembering that fraud isn't limited to just customer transactions. If you run a partner program, for instance, you also need to know how to detect affiliate fraud in your SaaS program to protect your marketing budget. Getting familiar with all the different faces of fraud is the only way to build a defense that actually works.

Building Your Foundational Security Layer

Now that you have a picture of the common schemes fraudsters cook up, it's time to build your first wall of defense. Real, effective fraud prevention ecommerce doesn’t start with some complex, expensive software. It begins with a solid foundation built from essential, straightforward tools.

Think of this as setting up the basic locks and alarms for your online store before you even think about installing a laser grid.

These foundational practices are your first filter. Their job is to catch the most obvious and common fraud attempts before they can cause any real damage. The best part? These tools are already available on major platforms like Shopify, WooCommerce, and Stripe, often just waiting for you to flip a switch.

Start with the Absolute Basics: AVS and CVV

The most powerful first steps you can take involve two simple acronyms that are already part of every single credit card transaction: AVS and CVV. These checks are your frontline security guards, and putting them to work is a must for any serious merchant.

- Address Verification Service (AVS): This tool simply checks if the billing address entered by the customer matches the address their bank has on file. A mismatch is a classic red flag. It often means a fraudster is using stolen card details but trying to ship the goods to their own address.

- Card Verification Value (CVV): This is that little three or four-digit security code on the back of the card. Requiring it helps confirm that the person making the purchase physically has the card, since this number isn't stored in most breached databases.

Just by enabling these checks in your payment gateway settings, you can stop a surprising amount of low-effort fraud. It’s the digital equivalent of a bartender asking for ID—a simple step that weeds out a lot of trouble right away.

Introducing Risk Scoring

Once you’ve locked down the basics, the next layer of your security involves thinking a bit more like a detective. Not all orders are created equal; some are just plain riskier than others. This is where risk scoring comes into play.

Risk scoring is an automated process where your ecommerce platform or payment processor analyzes multiple data points in a single transaction to assign it a risk level—usually something simple like low, medium, or high. Think of it as a credit score, but for each individual order.

A high-risk score doesn't automatically mean an order is fraudulent, but it’s a clear signal to slow down and take a closer look. This automated flagging system is crucial for managing your time and focusing your manual review efforts where they're needed most.

This system helps you avoid the trap of treating every single order with the same level of suspicion, which can grind your fulfillment to a halt and frustrate perfectly good customers.

How to Set Up Simple Transaction Rules

Beyond automated scores, you can create your own custom rules to automatically flag or even block transactions that fit specific criteria you’ve noticed. This gives you direct control over your store's security, letting you act on the patterns you see. These rules act like digital tripwires.

Most platforms allow you to set rules based on a variety of factors. For example, you could easily create a rule to automatically flag orders that meet any of these conditions:

- AVS or CVV Mismatches: Automatically hold any order where the AVS or CVV check fails. This is the most fundamental rule you can set.

- Unusual Order Velocity: Flag accounts that place multiple orders in a very short period. Fraudsters love to do this to max out a stolen card before it gets shut down.

- High-Value First-Time Orders: Put a temporary hold on unusually large orders from brand-new customers, especially if they’re asking for next-day shipping.

- IP and Shipping Address Mismatches: Flag orders where the customer's IP address is in one country, but the shipping address is in a completely different one.

Setting up these rules empowers you to build a proactive defense. But it's also important to recognize that managing these systems, especially for businesses in higher-risk industries, often requires specialized support. A key part of building a strong security layer involves choosing the right high-risk payment processor that offers robust fraud protection and chargeback management tailored to your specific needs.

These foundational layers—AVS/CVV checks, risk scoring, and transaction rules—all work together to create a powerful security net. They handle the bulk of the obvious threats, which frees you up to focus on growing your business while giving you the insights needed for effective chargeback prevention. By mastering these basics, you're not just stopping fraud; you're building a smarter, more secure business from the ground up.

Using AI for Smarter Fraud Detection

As your business grows, trying to manually review every single order for fraud becomes impossible. It’s like trying to personally check the ID of every person entering a massive stadium—you’d create a huge bottleneck and still miss the clever troublemakers. This is where technology, especially Artificial Intelligence (AI) and machine learning, gives your fraud prevention ecommerce strategy a serious upgrade.

Think of an AI fraud detection system as your store’s super-powered security guard. This guard hasn’t just worked the door at one or two venues; they’ve analyzed millions of transactions from thousands of stores. With that kind of experience, they can instantly spot subtle patterns that would be completely invisible to a human.

These smart systems don't just look for one or two red flags. They analyze hundreds of data points in a split second to make a solid call, keeping your business safe without slowing down legitimate sales.

How AI Connects the Dots

An AI-powered system is all about connecting seemingly unrelated bits of information to build a complete picture of an order's risk. Behind the scenes, it's constantly asking questions to figure out if a transaction is the real deal.

Here are just a few of the data points it analyzes in real-time:

- Behavioral Biometrics: How is the user interacting with your site? Are they typing and scrolling like a normal person, or are they pasting in stolen info with robotic speed? AI can tell the difference.

- Device Information: Is this a new device that has never been used on your store? Does its digital fingerprint match others used in previous fraud across the web?

- Geolocation Data: Does the customer's IP address location make sense compared to their billing and shipping addresses? A login from Vietnam with a shipping address in Ohio is a pretty clear warning sign.

- Order Details: Is this a first-time customer making an unusually large purchase of your most expensive items and demanding overnight shipping? That's a classic fraud pattern.

By weaving all this information together, the system can assign a precise risk score to each transaction. Low-risk orders sail through instantly, while high-risk ones are flagged for review or automatically blocked. It’s a much smarter, more efficient defense.

The Power of Identity Verification

As criminals get more sophisticated, just looking at transaction data isn't always enough. This is why identity verification (IDV) has become such a critical tool. IDV is simply the process of confirming that a customer is genuinely who they claim to be, often by asking them to quickly scan a government-issued ID or take a selfie.

This might sound like a hassle, but customer expectations have shifted. The global e-commerce fraud scene is growing at an alarming rate, with a 21% year-on-year increase in fraudulent activity. Because of this, over 75% of consumers now expect some form of identity check when signing up for online services. For businesses, 83% are already using IDV, and 81% plan to expand these tools. You can find more insights on the 2025 ecommerce fraud protection trends from Veriff.

The beauty of modern IDV is that it can be applied selectively. A trusted, returning customer might never see an extra verification step. But a new customer placing a high-value order might be asked for a quick, automated check that takes just a few seconds to complete.

This balanced approach provides tight security without frustrating your real buyers.

Machine Learning Gets Smarter Over Time

Perhaps the most powerful part of using AI is its ability to learn and adapt. Unlike a static set of rules that you have to update by hand, a machine learning model gets smarter with every single transaction it analyzes.

When you confirm an order was fraudulent, the system learns from the unique characteristics of that transaction. It then uses that new knowledge to get better at spotting similar fraud attempts in the future. This creates a feedback loop that continuously strengthens your defenses over time—without you having to lift a finger.

This adaptive tech is also incredibly useful for managing disputes. If you're interested, our complete guide to automated chargeback and dispute management using AI explores how these systems can help recover revenue automatically. By embracing these intelligent tools, you move from a reactive security posture to a proactive one, staying a step ahead of whatever threats come next.

Balancing Security With a Great Customer Experience

Here’s the million-dollar question for every online merchant: how do you stop fraudsters without making your real customers feel like they're trying to crack a safe just to buy a t-shirt? It’s a delicate dance, that’s for sure.

Go too soft on security, and fraudsters will happily eat into your profits. But get too aggressive, and you’ll frustrate good customers right out of their shopping carts. The real goal isn't just to block the bad guys; it's to make the good guys feel welcome and completely secure.

The secret is what we call a "frictionless" security approach. Instead of treating every shopper with the same level of suspicion, you only introduce extra checks when they're actually needed. This risk-based model gives most people a smooth ride, with just a few gentle speed bumps for the occasional suspicious order.

What Frictionless Security Looks Like

Think of your checkout process like airport security. Most travelers—your legitimate customers—get to breeze through the standard line. But if someone sets off the metal detector, representing a high-risk order, they get pulled aside for an extra check. You don't make everyone take off their shoes just because one person might be hiding something.

That’s exactly how a smart, frictionless system operates. It uses data to make intelligent decisions behind the scenes, creating different paths for different users.

Let's look at a real-world example:

- The Smooth Path: Sarah, a returning customer, logs into her account from her usual laptop. She places an order and ships it to her saved address. The system instantly recognizes her and lets the purchase fly through without a single hiccup. It's fast, easy, and exactly what she expects.

- The Bumpy Path: A new visitor, John, tries to buy three of your most expensive items. The red flags start waving: he's using a credit card with a billing address in one state and a shipping address in another. The system flags this as unusual and might trigger a quick, automated check—like sending a one-time code to his phone to confirm he’s the real cardholder.

This dynamic approach keeps the checkout flow buttery smooth for the 99% of good customers while putting a stop to potential fraud.

How to Implement a Risk-Based Approach

Putting this balanced strategy into action doesn't have to be a massive headache. It all starts with using the tools you have to tell the difference between low-risk and high-risk behavior, only adding friction when it's truly justified.

Here are a few tips to get started:

- Trust Your Regulars: Give your loyal, returning customers an express lane. If they're logged in and using familiar devices and addresses, there's no reason not to trust the transaction.

- Look for Red Flag Combos: Apply extra verification steps only when multiple high-risk indicators show up together. A large first-time order paired with a mismatched IP address and shipping location is a classic example.

- Use Dynamic Authentication: Employ tools that can trigger multi-factor authentication (MFA) or a quick ID check only for orders that cross a certain risk score. This is so much better than forcing every single customer through extra hoops.

- Review, Don't Just Block: Instead of automatically blocking medium-risk orders, flag them for a quick manual review. Sometimes a legitimate order can look a little fishy, and a quick check can save a valuable sale and keep a good customer happy.

The ultimate goal is to make security feel almost invisible to your trustworthy shoppers. It should work silently in the background, only becoming noticeable when it's actively protecting them—and you.

Talking About Security the Right Way

How you frame your security measures really matters. Instead of presenting them as annoying hurdles, position them as benefits that protect your customers. A simple message like, "We've added an extra security step to protect your account," makes customers feel cared for, not inconvenienced.

Great communication can turn a potentially frustrating moment into one that builds trust. For a deeper look into this, check out our guide on the best practices in customer service, as these same principles apply directly to how you handle security interactions. By striking this balance, you'll prove that strong security and a fantastic user experience don’t just coexist—they actually support each other.

Alright, let's put everything we've talked about into a simple, straightforward action plan. Think of this as your starting point for building a much tougher defense against fraud. This isn't a one-and-done setup; it's about making smart, ongoing adjustments.

First things first, do a quick audit of what you’ve already got. Are you actually using foundational tools like Address Verification Service (AVS) and CVV checks? These are your absolute first line of defense. Just enabling them in your payment gateway is an immediate win against the most basic fraud attempts.

Next, figure out exactly what your team should do when an order gets flagged as suspicious. This doesn’t mean you have to hit the cancel button right away. Often, a quick manual review can save a legitimate sale and keep a good customer from having a frustrating experience.

Building Your Long-Term Strategy

Once you've got the basics locked down, you can start picking the right tools for your store's specific situation. A smaller shop might get by just fine with the built-in analytics from its platform. But if you’re a larger business, you'll get a massive benefit from an automated, AI-driven solution that can crunch thousands of data points in a blink.

Your ultimate goal is to build a layered defense that shields your store without driving your customers crazy. This really boils down to:

- Reviewing your security rules on a regular basis to keep up with new fraud tactics.

- Training your team on how to spot the red flags we’ve covered.

- Keeping a close eye on your chargeback rate to catch problems before they spiral.

Putting in this effort isn't just about preventing lost revenue. While global ecommerce fraud losses are projected to rocket to $48 billion by 2025, the real cost of doing nothing is so much more than just lost products. It's the chargeback fees, the operational headaches, and the roadblocks that can completely stall your growth. You can find more insights on this in these ecommerce trends at netguru.com.

At the end of the day, a solid fraud prevention plan is about taking back control. When you take these steps, you're not just protecting your revenue—you're building customer trust and freeing yourself up to focus on what really matters: growing your business with confidence.

Got Questions About Ecommerce Fraud? Let's Unpack Them.

Even with the best game plan, questions about ecommerce fraud are going to pop up. It's just the nature of the beast. Let's tackle a few of the most common ones we hear from merchants, breaking them down with practical answers that build on everything we’ve covered so far.

What Is the First Step I Should Take?

The absolute first thing you should do is switch on the foundational tools already built into your payment gateway. We’re talking about the Address Verification Service (AVS) and requiring the Card Verification Value (CVV) for every single purchase.

Think of these two checks as your simplest, yet most powerful, first line of defense. They instantly cross-reference the billing address and the 3-4 digit security code on the card with what the customer's bank has on file. Flipping these switches will immediately shut down a massive amount of basic, low-effort fraud attempts. It's a quick win.

How Can I Reduce Friendly Fraud?

Tackling "friendly fraud" boils down to two things: crystal-clear communication and meticulous record-keeping. Sometimes, genuinely good customers file chargebacks by mistake simply because they don't recognize a charge or can't get a hold of you. You can head this off by making your business easy to recognize and even easier to work with.

Here are a few things you can do right now:

- Set a Clear Billing Descriptor: Make sure your store's name—not some cryptic company name—appears clearly on your customers' credit card statements.

- Be Proactive with Updates: As soon as an order is placed, send a confirmation. When it ships, send an update with the tracking information. Don't leave them guessing.

- Make Policies Easy to Find: Your shipping and return policies shouldn't be buried. Display them prominently so customers know what to expect.

- Offer Stellar Support: Good, responsive customer service can resolve an issue long before a customer even thinks about calling their bank.

And when a dispute does happen? Having solid proof of delivery and a clear email trail will dramatically increase your chances of winning the case.

Are Expensive Fraud Tools Necessary for a Small Business?

Not right out of the gate, but your needs will definitely evolve. When you're just starting, the fraud analysis tools built into platforms like Shopify or Stripe are often more than enough to get by. They do a decent job of flagging the most obviously suspicious orders.

The real turning point comes when you find yourself spending way too much time manually reviewing orders, or when you start seeing more sophisticated fraud attempts slipping through. At that point, the cost of an automated, AI-powered solution is easily justified by the time and money it saves.

These more advanced tools don't just stop fraudsters in their tracks; they also free up countless hours and, just as importantly, reduce the risk of accidentally declining legitimate customers. The key is to start with the tools you have and scale up to more powerful solutions as your sales volume and risk level grow.

At ChargePay, we help you get ahead of fraud instead of just reacting to it. Our AI-driven platform automates chargeback management, recovering lost revenue so you can focus on what you do best: running your business. Protect your store with ChargePay today.

.svg)

.svg)

.svg)

.svg)