When you’re trying to understand a merchant account vs a payment gateway, it’s easy to get tangled up in the jargon. Here’s the simple breakdown: one is a special kind of bank account that holds your money, and the other is the digital plumbing that securely moves payment information.

To actually get paid, you need a merchant account. But to safely get the customer's card details to the bank for an approval in the first place, you need a payment gateway.

The Core Difference: A Simple Breakdown

Let's clear up the confusion right from the start. A merchant account is a specific type of bank account where funds from your customer's card payments are held before they land in your main business account. Think of it as a secure waiting room for your money.

A payment gateway, on the other hand, is the technology that acts like a digital credit card terminal. It’s the behind-the-scenes operator that securely captures, encrypts, and sends your customer's payment details to the right places to get the transaction approved. You almost always need both to accept card payments online, but they handle completely separate jobs.

To get the full picture, it helps to understand a third player in this process. You can learn more about how a payment processor fits into this equation in our detailed guide.

Key Roles in a Transaction

The roles are distinct but have to work together perfectly in every online sale. The payment gateway is the messenger, and the merchant account is the temporary vault.

- Payment Gateway: This is the customer-facing part of the tech. It's the "Pay Now" button, the checkout form, and the secure channel that encrypts and transmits card data. Its primary job is communication and security.

- Merchant Account: This is the financial backend. It’s where the money from an approved transaction gets deposited and held until it's settled and transferred to your primary business bank account. Its main job is fund management.

The gateway speaks, and the merchant account holds. One can't really do its job without the other in a typical online payment flow.

Key Takeaway: The payment gateway is the digital bouncer that checks the ID (card info) at the door, while the merchant account is the secure room where the money waits before being moved to the main safe (your business bank account).

Merchant Account vs Payment Gateway at a Glance

Sometimes, seeing the differences side-by-side makes it click. This table breaks down the core functions to make the distinction crystal clear.

Ultimately, both are essential cogs in the machine that lets you get paid online. The gateway handles the secure messaging, and the merchant account handles the money itself.

How a Merchant Account Manages Your Money

Ever wonder what actually happens to your money between a customer's purchase and the moment it hits your bank? That mysterious journey involves a critical stop: the merchant account. Think of it not as your regular business checking account, but as a specialized financial holding area built specifically to receive and manage funds from card transactions.

Once a payment gateway gives a transaction the green light, the money doesn't just magically appear in your bank account. Instead, it’s routed to your merchant account. This account acts as an intermediary, collecting all your approved sales in one place before the final settlement happens.

This separation is crucial for both organization and security. It gives the acquiring bank (the bank that provides your merchant account) a chance to batch transactions, handle any currency conversions, and deduct processing fees before sending you a clean, consolidated deposit.

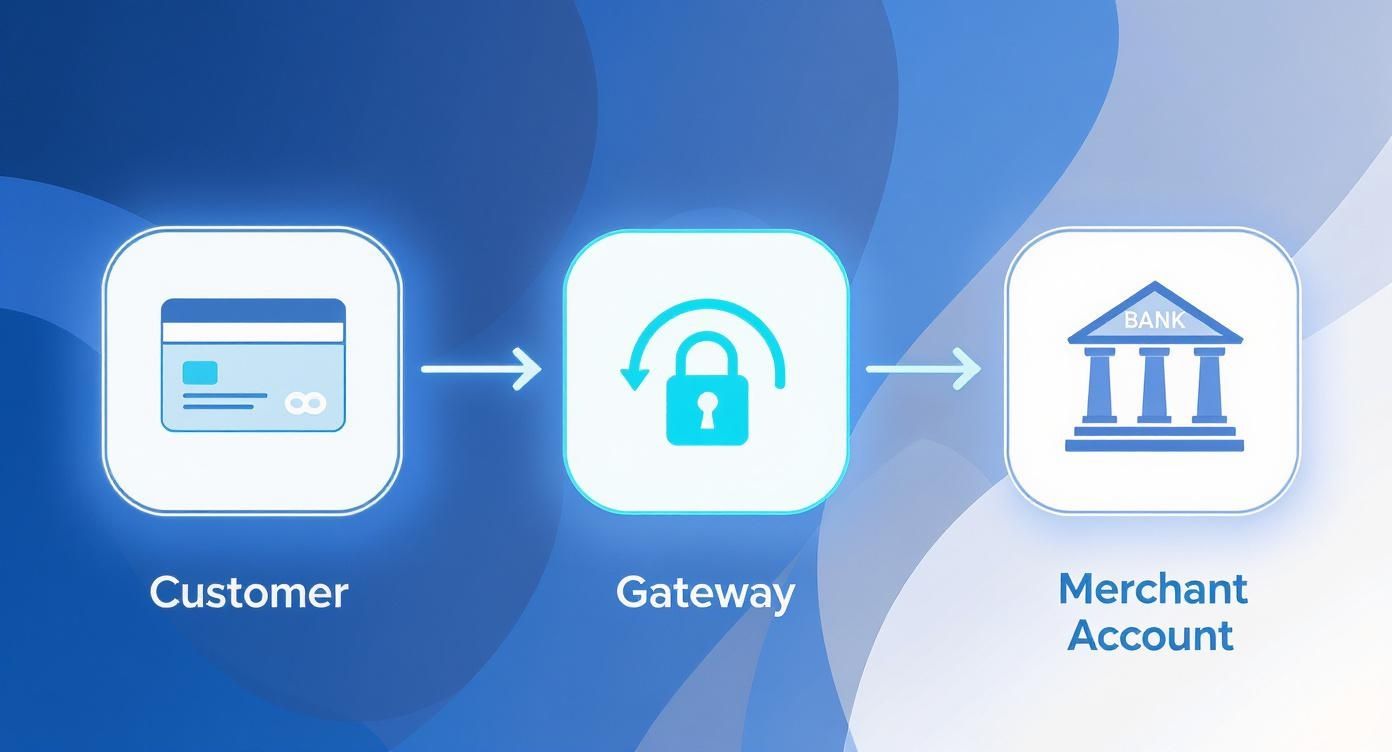

This flow shows how the money travels from the customer's card, through the secure gateway, and finally lands in the merchant account.

As you can see, the merchant account is the financial destination that holds the funds right after the gateway has done its job of securely transmitting the payment details.

Dedicated vs. Aggregated Accounts

Not all merchant accounts are created equal. They generally fall into two camps, and the right one for you depends entirely on your business.

Dedicated Merchant Account: This is an account underwritten and issued specifically for your business. The big win here is often lower per-transaction fees, which makes it a great fit for high-volume or high-risk businesses. The catch? You’ll go through a much more rigorous application process where your business history, credit, and overall risk profile are put under a microscope.

Aggregated Merchant Account: This is the model that all-in-one providers like Stripe and PayPal use. Your business operates under their master merchant account, sharing it with thousands of other businesses. Setup is incredibly fast and easy, but the trade-off is typically higher transaction fees and less direct control over the account.

The global merchant services market, which includes these accounts, is growing fast, projected to jump from USD 66.71 billion in 2025 to USD 201.41 billion by 2032. This surge shows the different needs of modern businesses—from startups needing the quick setup of an aggregated account to larger enterprises saving big with the lower fees of a dedicated one.

Choosing between a dedicated or aggregated account is a key strategic decision. Let your sales volume and risk level be your guide, as this choice directly impacts your bottom line and operational flexibility.

A major responsibility that comes with having a merchant account is managing disputes. When a customer files a chargeback, the whole process is funneled through your merchant acquiring bank. Protecting your account from getting hit with too many disputes is absolutely vital, which is why having a solid strategy for merchant chargeback protection is non-negotiable.

How a Payment Gateway Secures Your Transactions

Think of the payment gateway as the bouncer at the front door of your online store. It's the very first point of contact for every transaction, and its entire job is to handle security and communication, making sure everything is legitimate before it goes any further.

The moment a customer types in their credit card details and hits "Buy Now," the gateway springs into action. Its most critical role is to securely grab those card details from your website. It immediately encrypts this sensitive data, scrambling it into an unreadable code to shield it from any fraudsters who might be snooping around. This encrypted package is then safely passed along to the payment processor, who takes it from there to get the bank's approval.

This initial handshake is the gateway's core function—it's a secure digital messenger that ensures every payment starts off on the right foot, long before it ever touches a merchant account.

The Role of Encryption and Tokenization

To keep all that data locked down, payment gateways rely on two powerful techniques: encryption and tokenization. Encryption is what protects the data while it’s in transit, making it completely useless to anyone who might try to intercept it.

Once the transaction is authorized, many gateways then use tokenization. This process swaps the customer's actual card number for a unique, non-sensitive string of characters—a "token." This token can be stored safely for things like recurring subscriptions or one-click checkouts, all without ever exposing the real card details. If you want to dive deeper, our guide explains what tokenization is in payments and why it's such a game-changer for security.

This two-pronged security strategy is absolutely fundamental to modern ecommerce.

By encrypting data in transit and tokenizing it for storage, a payment gateway significantly reduces the risk of a data breach and simplifies your security obligations.

Meeting PCI DSS Compliance

Any business that accepts card payments has to play by the rules of the Payment Card Industry Data Security Standard (PCI DSS). These are strict regulations designed to protect cardholder data, and becoming compliant on your own can be a massive headache and a huge expense.

This is where a good payment gateway really proves its worth. Most modern gateways are already PCI DSS compliant right out of the box.

- Hosted Gateways: These are the simplest. They redirect your customers to a secure page hosted by the gateway provider to enter their payment info. Since the sensitive data never even touches your servers, your PCI compliance burden is dramatically reduced.

- Integrated Gateways: These keep the customer on your site for a smoother experience but use secure fields (often called iframes) to collect the card data. Again, this isolates your systems from the sensitive information, taking much of the PCI responsibility off your plate.

The global payment gateway market was valued at USD 31.0 billion in 2023 and is expected to rocket to USD 161.0 billion by 2032, with hosted gateways leading the charge. It’s no surprise businesses prefer these solutions; they offer a ready-to-use, compliant system that offloads a huge amount of security risk.

Comparing Costs and Key Responsibilities

Figuring out the numbers behind your payment setup is non-negotiable if you want to stay profitable. When you put a merchant account and a payment gateway side-by-side, you'll see their fee structures and who-does-what are worlds apart. Nailing this choice helps you forecast costs accurately and know exactly who’s on the hook for every part of the process.

A traditional merchant account often runs on interchange-plus pricing. This model is refreshingly transparent, breaking your costs down into two parts: the non-negotiable interchange fee that goes to the card-issuing bank, and a small markup for the processor. It’s typically the more cost-effective route for high-volume businesses, but it can look a bit complicated at first glance.

On the other side of the coin, payment gateways—especially those bundled into all-in-one solutions like Stripe or PayPal—tend to use flat-rate pricing. You pay one predictable percentage plus a fixed fee for every transaction. This makes bookkeeping a breeze for smaller businesses or startups.

A Closer Look at Fee Structures

The pricing differences aren't just minor details; they can be significant. For instance, traditional merchant accounts might have transaction fees climbing up to 5% plus a flat fee, while all-in-one gateways often hover around 3% plus a smaller fixed fee. That variance can make a real dent in your margins, so it's a critical factor when setting your own prices.

Ultimately, a great setup is about balance. You need the smooth customer experience from a reliable gateway combined with the efficient fund management of a merchant account. This combination is what helps your business boost sales and keep cash flow healthy.

Here’s a snapshot of a typical flat-rate fee structure from Stripe, which rolls its gateway and aggregated merchant account services into one simple price. This is exactly why these platforms are so popular.

The screenshot shows a clear, predictable fee (like 2.9% + $0.30 per successful card charge), which is the hallmark of modern, all-in-one payment service providers.

Who Handles What: A Responsibility Breakdown

Beyond the costs, knowing who is in charge of critical tasks is key. This division of labor is one of the most defining factors in the merchant account vs. payment gateway debate.

PCI Compliance

- Payment Gateway: This is the gateway's territory. It handles the heavy lifting of encrypting and tokenizing sensitive card data, which massively reduces your PCI DSS compliance burden. If you're using a hosted gateway, they often take care of almost all of it for you.

- Merchant Account: While your account provider must be compliant, the buck ultimately stops with you, the merchant. You are responsible for ensuring your entire business environment meets PCI standards. The gateway just makes that job a whole lot easier.

Chargebacks and Disputes

- Merchant Account: This is a core function of the merchant account provider. When a customer files a chargeback, the acquiring bank that holds your account is the one that manages the formal dispute process with the card networks.

- Payment Gateway: The gateway is more of a data provider here. It gives you the transaction records and details you need to fight the dispute, but it isn’t financially or operationally involved in the chargeback resolution itself.

Your merchant account is your partner in the dispute process, but the ultimate responsibility for preventing and winning chargebacks falls on you. Effective chargeback automation is vital for protecting your revenue.

For businesses looking to slash losses from disputes, it's smart to explore tools that offer transparent, success-based pricing for chargeback management. You can get a feel for how that works by checking out this overview of ChargePay's pricing.

Refunds

- Payment Gateway: The gateway gives you the technical interface—think of it as the "refund" button in your dashboard—to kick off the process.

- Merchant Account: The merchant account does the actual work of moving the money. It processes the refund transaction and ensures the funds are returned from your account to the customer's card.

Choosing the Right Payment Setup for Your Business

Figuring out your payment setup—whether you go with a bundled, all-in-one solution or a separate merchant account and payment gateway—isn't just a tech decision. It's a choice that hits your bottom line, your level of control, and how easily you can grow.

There’s no magic bullet here. The right setup is completely tied to your business model, how much you’re selling, and your industry’s risk profile. Getting this right from day one will save you a world of headaches and keep processing costs from chewing up your profits. Let’s walk through the common scenarios to see where you fit.

When to Use an All-in-One Solution

For most new businesses, startups, and small ecommerce stores, an all-in-one payment service provider (PSP) like Stripe, PayPal, or Square is a no-brainer. These guys bundle the payment gateway and an aggregated merchant account into one neat, simple package.

This is the perfect route if you are:

- Just Starting Out: The setup is ridiculously fast. You can be up and running, accepting payments in a matter of hours—not weeks. No painful, long-winded underwriting process to slog through.

- Processing Lower Volumes: If your monthly sales are under $10,000-$20,000, the simple, predictable flat-rate fees are usually way more cost-effective than a complicated interchange-plus model.

- Lacking Technical Resources: These platforms are built for simplicity. They offer pre-built integrations for systems like Shopify and have massive libraries of documentation, so you don't need a developer on speed dial.

Real-World Scenario: A new Shopify store selling handmade jewelry needs to launch, like, yesterday. By using Shopify Payments (powered by Stripe), the owner can flip a switch and start taking credit cards. The fees are predictable and easy to bake into pricing, and there’s no separate merchant account application needed.

The trade-off for all this convenience? You get less control and will likely face higher fees as your business scales. But for sheer speed and simplicity, you can't beat an integrated solution.

When to Get a Dedicated Merchant Account

Once your business starts to mature and your sales volume really takes off, the math begins to shift. This is when a dedicated merchant account paired with a separate payment gateway (like Authorize.net) starts looking like a much smarter play. This setup is generally the right move for established businesses.

You should seriously consider this path if you are:

- A High-Volume Business: Once you're consistently processing a high volume of sales, the lower interchange-plus pricing from a dedicated merchant account can save you thousands of dollars a year compared to flat-rate fees.

- Operating in a High-Risk Industry: If you’re in a business like CBD, supplements, or travel, all-in-one providers will often shut the door on you. A dedicated high-risk merchant account is specifically underwritten to handle your kind of business.

- Seeking More Control and Flexibility: Having separate providers gives you more leverage to negotiate fees. It also lets you swap out your gateway or merchant account provider independently if a better deal comes along. For really complex operations, you might even start looking into a payment orchestration platform to manage multiple providers from a single dashboard.

Getting a dedicated merchant account is a more formal process. It involves a full application and underwriting, where the provider digs into your financials and risk profile. It takes more time, but for a growing business, the long-term cost savings and stability are almost always worth it.

A Few Lingering Questions

Even after breaking it all down, a few common questions always seem to pop up. Let's tackle those head-on to clear up any final points of confusion.

Can I Have a Payment Gateway Without a Merchant Account?

Generally, no. If you want to accept credit or debit card payments online, you absolutely have to have a merchant account where the money can land. Think of the payment gateway as the secure messenger that carries the card details for approval; the merchant account is the bank account that actually gets the cash.

However, modern all-in-one providers like Stripe or PayPal have blurred this line. When you sign up with them, you’re getting both the gateway technology and a merchant account—it just happens to be an aggregated account that they manage. This means you don't have to go out and apply for a separate, dedicated account on your own.

Key Insight: You can’t get paid without a merchant account, but modern payment service providers bundle the two so seamlessly that it often feels like you’re only dealing with one service.

Which Service Handles Chargebacks and Disputes?

The merchant account is where the buck stops with chargebacks. When a customer disputes a charge, the whole formal process is managed by the merchant acquiring bank—the institution providing your account. They’re the ones on the hook for talking to the card networks and seeing the dispute through from start to finish.

Your payment gateway has a critical supporting role. It’s the source of all the transaction data and records you'll need to build your case and fight the chargeback. But the financial liability and the official dispute process fall squarely on your merchant account provider.

Do I Need Separate Providers for Each Service?

Not always. For a lot of businesses, keeping them separate isn't the best move. The right answer really comes down to your business's size, sales volume, and what you specifically need.

Here’s a quick way to think about it:

- Go for a bundled solution (like Stripe or PayPal) if: You're a small to medium-sized business, a startup, or just getting your feet wet with ecommerce. The speed and simplicity of getting an integrated gateway and merchant account are hard to beat. It’s the fastest path to start accepting payments with zero fuss.

- Consider separate providers if: You're a larger operation with a high volume of transactions. Securing a dedicated merchant account directly from a bank and pairing it with a separate gateway (like Authorize.net) can lead to significantly lower transaction fees. This route gives you more control and customization, but be prepared for a more involved and longer setup process.

For most businesses, especially when starting out, the sheer convenience of a bundled solution makes it the clear winner. As your business grows, you can always re-evaluate whether the cost savings from a dedicated setup justify the extra complexity.

Ready to stop losing money to chargebacks? ChargePay uses AI to automatically fight and win disputes for you, recovering up to 80% of your lost revenue. Find out how you can automate your chargeback management and protect your bottom line by visiting ChargePay.

.svg)

.svg)

.svg)

.svg)