A return item chargeback is a fee your bank might hit you with when a check you deposit bounces. This isn't the same as a credit card chargeback, where a customer disputes a purchase. This one is purely a banking issue that happens when a check transaction goes south.

What Exactly Is a Return Item Chargeback?

Getting a "return item chargeback" notice can feel like a direct hit to your bottom line, and frankly, it's confusing. Let's clear the air. This has nothing to do with a customer being unhappy with a credit card purchase. It's all about an old-school problem: a bad check.

Let’s say you sell a handmade leather wallet and the customer pays you with a check. You pop it in the bank, the funds show up in your account, and you ship the wallet. A week later, you see a "return item chargeback" fee on your statement. What happened? The customer's check bounced because they didn't have enough money in their account.

That scenario is the heart of the matter. Your bank had to deal with the unpaid check, and now they’re passing a fee on to you for the trouble. This is a world away from the typical chargeback process in banking most online merchants know, which centers on customer disputes over card payments.

Why Do These Chargebacks Happen?

The reasons for a return item chargeback are almost always tied to the check writer's bank account, not your product or service. The most common triggers are pretty straightforward:

- Insufficient Funds (NSF): This is the big one. The customer’s account was short on cash when your bank tried to process the check.

- Stop Payment Order: The person who wrote the check told their bank not to honor it.

- Account Closed: The checking account is no longer active.

- Suspected Fraud: The bank's fraud detection systems flagged the check as suspicious.

Understanding these root causes is key. It helps you see that this isn't a customer service issue—it's a payment processing failure.

Return vs. Return Item Chargeback

It's easy to get the terms confused, but a standard return and a return item chargeback are completely different beasts. Here’s a quick breakdown to keep them straight.

Seeing them side-by-side makes it clear: one is about your product and policies, while the other is strictly about the validity of a payment method.

The Real Cost for Merchants

The financial sting goes way beyond the bank fee itself. Every chargeback creates a ripple effect. The average chargeback in the United States costs a merchant $110 when you factor in the lost revenue, fees, and operational headaches.

A huge chunk of these disputes comes from "friendly fraud," where a customer disputes a valid charge. It’s wild, but research shows that simple buyer's remorse is behind 65.3% of these friendly fraud cases.

The key takeaway here is that a return item chargeback is not a failure on your part. It’s a payment failure. The customer's bank rejected the transaction, and your bank is just letting you know—while charging you a fee for it.

To really get a handle on what a return item chargeback is, it helps to first understand a general chargeback definition. That gives you the foundation to see just how different this specific banking action is. My goal is to give you a rock-solid understanding of what you’re facing so your next steps become crystal clear.

Your First Moves After a Chargeback Notice

That notification email is a gut punch. Seeing a return item chargeback can send anyone into a spin, but your best weapon is a calm, methodical response. The clock is ticking, but panic isn't on the agenda.

A fast, organized reaction is your greatest advantage in these first few critical hours. Think of it as building a case file. Your immediate goal is to gather every single piece of evidence related to the transaction. Don't wait.

Start Assembling Your Proof

Right away, you need to collect all the digital paperwork that tells the full story of the sale. This isn't just about proving you shipped something; it's about proving you held up your end of the deal completely, from start to finish.

Here's what you should pull together immediately:

- Customer Communications: Every email, chat log, or social media message you exchanged with the customer.

- Order Confirmation: The original order confirmation email you sent, detailing what was purchased and for how much.

- Proof of Delivery: This one is non-negotiable. Get the tracking number and a screenshot from the carrier’s website showing the item was successfully delivered to the correct address.

- Product Photos: If you take photos of items before shipping them out (a great practice for high-value goods), find them.

This initial evidence-gathering phase sets the stage for your entire dispute. It's the foundation you'll build your whole argument on.

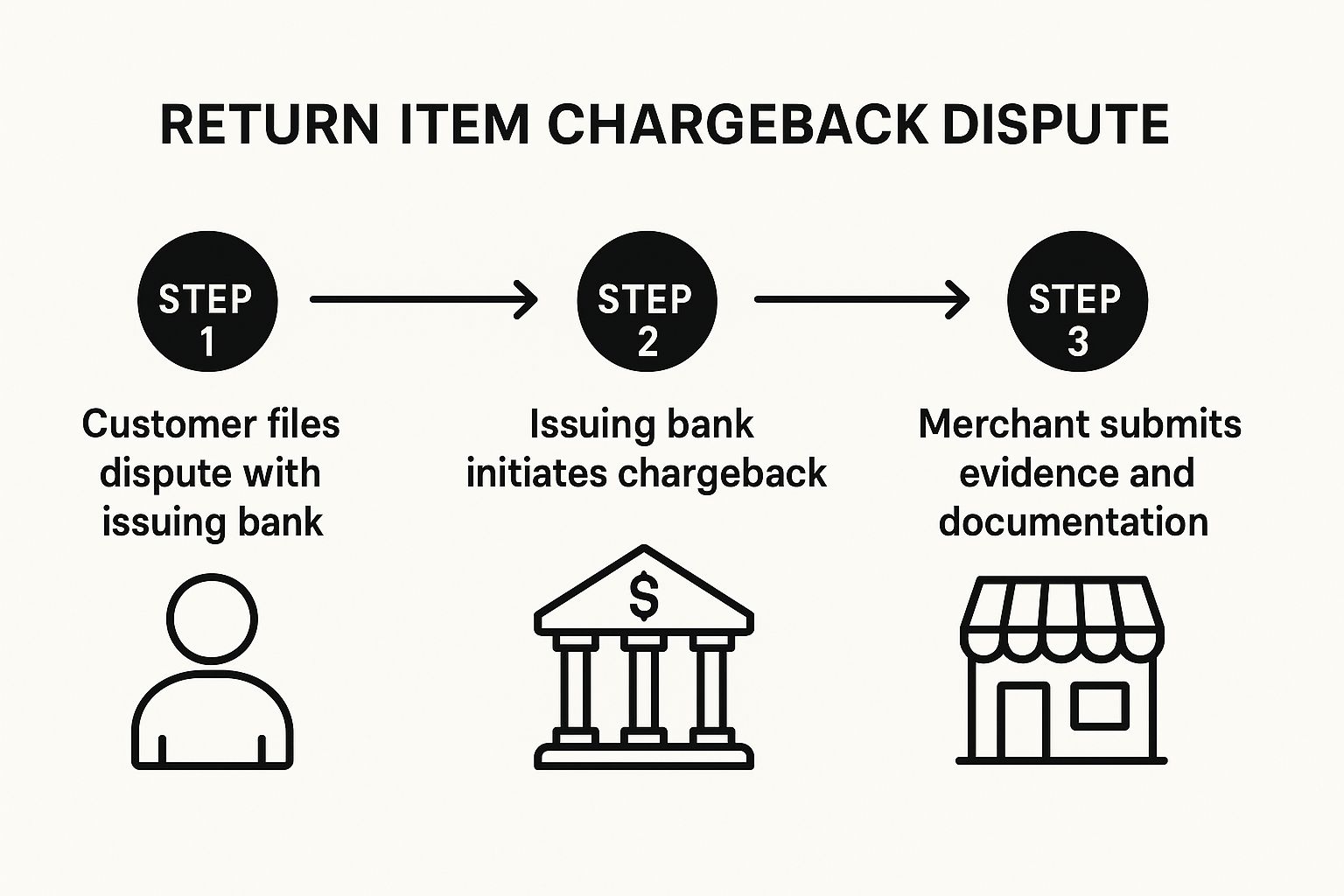

This infographic shows the typical journey a return item chargeback takes from the customer's initial action to your response.

As you can see, your evidence submission is the crucial final step where you get to present your side of the story and fight for your revenue.

Decode the Reason Code

Every chargeback comes with a "reason code." This little piece of information is gold. It’s the bank telling you exactly why the customer is disputing the charge. Don’t just gloss over it.

The reason code dictates your entire strategy. If the code is for "Product Not Received," your proof of delivery becomes the star of the show. If it's "Product Not as Described," your product page descriptions and customer emails suddenly become much more important.

Think of the reason code as the bank giving you a massive hint. They're telling you which specific claim you need to disprove. Focusing on that point makes your rebuttal infinitely stronger.

Sometimes, the initial notice isn't a full-blown chargeback but a retrieval request, which is an earlier, less severe stage in the dispute process. It’s important to know the difference. You can learn more about retrieval requests and chargebacks in our guide to better understand exactly where you stand.

By gathering your documents and pinpointing the reason code, you move from a reactive state of shock to a proactive position of control. You’re no longer just defending yourself; you're actively building a case to reclaim your money.

Crafting a Rebuttal That Actually Wins

Okay, you’ve gathered all your evidence. Now it's time to build a case that’s so clear and logical it’s almost impossible to argue with. A disorganized, emotional, or rambling response is a fast track to losing. This is where you transform that pile of proof into a compelling, fact-based story.

Your goal is a professional rebuttal letter that gives the bank everything they need, with zero fluff. Think of yourself as a detective presenting the facts of the case. You’re not arguing with the customer; you’re simply showing the bank that the transaction was legitimate and you held up your end of the deal.

Structuring Your Winning Argument

A strong rebuttal needs a clean, logical structure. You want to make it incredibly easy for the reviewer to understand your side. Don't make them hunt for information or connect the dots themselves.

Kick things off with a brief summary of the transaction—customer’s name, order number, purchase date, and amount. Then, get straight to the point by directly addressing the chargeback reason code.

For example, if the reason is “Product Not Received,” your opening line should immediately counter that by stating the product was delivered and you have the proof. This sets the tone and tells the reviewer exactly what you’re about to demonstrate.

The single biggest mistake I see merchants make is getting emotional or personal in their rebuttal. Stick to the facts. The bank doesn’t care about your frustration; they only care about clear, indisputable evidence.

This focus on facts is even more crucial when you look at the bigger picture. One report highlights that while banks classify up to 72% of chargebacks as fraud, merchants only attribute about 45% to that cause. This gap shows many disputes are just simple misunderstandings, making clear communication in your rebuttal that much more important. You can find more details in Ethoca's comprehensive chargeback report.

Building a Point-by-Point Takedown

After your intro, you need to systematically dismantle the customer's claim. The best way I've found to do this is with a simple, chronological timeline of events, backing up each step with a piece of evidence.

Here’s what that looks like in practice:

- January 10: Customer placed Order #1234 for one "Handmade Leather Wallet." (Attach order confirmation email).

- January 11: Order #1234 was shipped via UPS with tracking number 1Z987XYZ. (Attach shipping confirmation).

- January 14: UPS tracking confirms the package was successfully delivered to the customer’s verified address. (Attach screenshot of delivery confirmation).

- January 25: Customer contacted us with a question about leather care, confirming they had the item. (Attach email correspondence).

This format is powerful because it’s so direct and fact-based. It guides the reviewer through the entire transaction, leaving no room for doubt. If you're looking for a solid starting point, you can check out a helpful rebuttal letter template in our detailed guide to make sure you've covered all your bases.

Finally, close your letter with a polite but firm summary. Reiterate that you have provided compelling evidence that proves the charge is valid and respectfully request that the return item chargeback be reversed. Keep it professional, attach all your documents clearly, and get it submitted well before the deadline hits.

Smart Ways to Prevent Future Chargebacks

https://www.youtube.com/embed/5ou8zEcFwRU

Winning a dispute is a relief, but honestly, it’s a reactive game. You're always playing defense. The real victory is stopping a return item chargeback from ever happening in the first place.

Shifting your focus from fighting fires to fire prevention is the single best thing you can do for your bottom line. This means making your business a less attractive target for friendly fraud and clearing up the common mix-ups that lead to legitimate disputes. The good news? You can put most of these strategies into play right away.

Make Your Policies Impossible to Miss

Ambiguity is the enemy of a smooth transaction. A customer should never, ever have to dig for your return or shipping policies. If they can’t find the rules, they're far more likely to just bypass you and go straight to their bank for a chargeback.

Get your policies out in the open. Make them crystal clear and put them in highly visible spots on your site. I'm talking footer links, product pages, and especially right there on the checkout page. And use plain English—no one wants to decipher dense legal jargon.

A clear, accessible policy pulls double duty:

- It Sets Expectations: Customers know exactly what to expect when it comes to return timelines, conditions, and the steps they need to take. No surprises.

- It Builds Trust: Transparency shows you’re a legitimate seller who stands by your products and has a process in place.

One of the best ways to streamline this entire process and cut down on policy-related confusion is by implementing efficient returns management platforms.

Improve Your Customer Communication

Fantastic customer service is your absolute first line of defense. When a customer has a problem, they need to feel that contacting you is the easiest, fastest path to a solution. If they feel ignored or get frustrated, a chargeback is the next logical step in their mind.

Answer emails and messages quickly and with a bit of empathy. Even if the answer is "no," a prompt and respectful explanation can stop a dispute in its tracks. Also, keep your customers in the loop with automated order and shipping confirmations. These small touchpoints go a long way in reassuring them that everything is being handled correctly.

Think of it this way: every unanswered email is a potential chargeback waiting to happen. An open line of communication makes customers feel heard and valued, which drastically cuts their incentive to file a dispute.

Strengthen Your Transactional Clarity

Sometimes, a chargeback is just a simple case of mistaken identity. The customer scrolls through their bank statement, sees a charge from "SP *MERCHANTBIZ LLC," and has no clue who it is.

Using a clear billing descriptor that actually matches your store name is a simple but incredibly powerful fix.

On top of that, you absolutely must use delivery confirmation with tracking for every single order. This is non-negotiable. It’s your concrete proof that you held up your end of the deal. Without it, winning a "product not received" claim is nearly impossible.

Getting proactive is more critical than ever. Global chargeback volumes are projected to hit 324 million by 2028—that's a 24% jump in just three years. This surge is largely because 63% of merchant transactions now happen online. As the volume climbs, prevention becomes everything.

By tightening up these key areas, you build a much stronger, more resilient business. If you're looking for more ways to get ahead of disputes, check out our complete guide on effective chargeback prevention.

Your Go-To Chargeback Management Checklist

Let's pull everything together into a practical game plan. Think of this as your battle-ready guide for handling a return item chargeback, from the second it hits your inbox to building long-term defenses against the next one.

Having a solid plan is what separates a prepared business owner from a potential victim. When you know exactly what to do, you can move confidently to protect your revenue instead of scrambling.

When the Notice Arrives: Your First 24 Hours

This is the triage phase. Speed and organization are everything. The clock starts ticking the moment you get that notice, so don't put this off.

- First, stay calm. Panicking is the fastest way to make a mistake. Take a deep breath and immediately create a new digital folder for this specific case.

- Next, gather your evidence. Pull every piece of digital documentation tied to the order. This means grabbing the order confirmation, any and all emails or chat logs with the customer, and—most importantly—the proof of delivery from your shipping carrier.

- Identify the reason code. The bank includes a specific code that tells you exactly why the customer is disputing the charge. Your entire rebuttal needs to focus on proving that one specific reason is invalid.

Building Your Winning Rebuttal

Alright, now you're ready to build the case that gets your money back. Your goal here is to be professional, factual, and crystal clear.

- Write a clean, professional rebuttal letter. Start with the basic order details right at the top. Then, create a simple, step-by-step timeline of the entire transaction, from the moment they clicked "buy" to the moment the package was delivered.

- Back it up with compelling proof. For every point you make in your timeline, attach the corresponding piece of evidence. This connects the dots for the bank and makes your case hard to deny.

- Submit well before the deadline. Don't procrastinate. As soon as your well-documented case is ready to go, send it in.

A well-structured argument, backed by solid proof, makes it easy for the bank to see the transaction was legitimate. Stick to the facts, avoid emotion, and focus on disproving the reason code.

Long-Term Prevention Strategies

Winning disputes is great, but avoiding them altogether is even better. It’s time to shift your focus from reactive to proactive.

- Make your policies impossible to miss. Your return and shipping policies need to be clear, concise, and easy to find on your website. No fine print.

- Offer standout customer service. Quick, helpful, and professional responses can solve a customer's problem long before they even think about calling their bank.

- Use clear billing descriptors. Make sure the name that appears on your customer's credit card statement is instantly recognizable as your business. "XYZ WEBSERVICES" is much better than a generic or confusing descriptor.

Juggling disputes can easily feel like a full-time job. For merchants looking to get that time back, exploring different chargeback management tools can be a game-changer, offering powerful, hands-free solutions.

Answering Your Most Common Chargeback Questions

When you get hit with a return item chargeback, it’s natural to have a million questions swirling around. I’ve been there, and I’ve heard just about every question from other merchants over the years. Let's cut through the confusion and get you some straight answers.

How Long Do I Have to Respond to a Chargeback?

This is probably the most urgent question, and for good reason. The clock starts ticking the second you're notified.

Typically, you'll have somewhere between 20 to 45 days to get your evidence submitted. This window can change depending on the card network (Visa, Mastercard, etc.) and the specific bank involved. The key takeaway? Treat that deadline in your notification email as gospel. If you miss it, you automatically lose the dispute. No appeals, no second chances—the money is just gone.

Can I Contact the Customer Directly After a Chargeback Is Filed?

Yes, and honestly, sometimes it’s the smartest first move. A quick, friendly, and non-accusatory email can work wonders. More often than not, the whole thing is a simple misunderstanding. Maybe they didn’t recognize your business name on their statement or forgot about an auto-renewal.

If you can clear things up and they agree to drop the dispute, that’s a huge win. Just make sure you get it in writing. Ask them to send a simple email confirming they've contacted their bank to withdraw the chargeback. You can then submit that email as a knockout piece of evidence in your official response.

This is a delicate conversation. Your goal isn't to argue or pressure them; it's to open a helpful dialogue. A calm, problem-solving approach can resolve the issue faster than the entire formal dispute process.

Is It Even Worth Fighting a Chargeback for a Small Amount?

I get this question all the time. It feels like a lot of hassle for a tiny transaction, right? But in almost every case, the answer is a hard yes. This isn't just about recovering that one small sale; it's about protecting your business's future.

Consistently fighting every single chargeback sends a powerful message to the banks: you're a diligent merchant who takes fraud seriously. But more importantly, every chargeback you receive—won or lost—dings your chargeback-to-transaction ratio.

If that ratio gets too high, your payment processor will start seeing you as "high-risk." That can lead to a world of pain, including higher processing fees, a rolling reserve (where they hold back a percentage of your money), or even shutting down your merchant account entirely. Fighting the small stuff is a long-term play for your business's health.

For more in-depth answers, you can always check out our complete chargeback management FAQs for more insights.

What Happens If I Lose the Chargeback Dispute?

Losing a dispute is a gut punch, no doubt about it. When the final decision doesn't go your way, the funds are officially gone for good, sent back to the customer. On top of that, you’re still on the hook for the non-refundable chargeback fee from your processor.

In some rare cases, you might have the option to escalate the fight to the next stage, known as pre-arbitration or arbitration. Be warned, though: this is a much more expensive and complicated battle. It’s typically only worth considering for extremely high-value disputes where you’ve uncovered some new, game-changing evidence that wasn't in your first response.

Navigating the maze of a return item chargeback can be exhausting, but you don't have to go it alone. ChargePay leverages AI to handle the entire dispute process for you, crafting evidence-backed responses to win back your revenue while you focus on your business. See how you can protect your bottom line at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)