A Stripe chargeback is what happens when a customer goes over your head and directly to their bank to reverse a payment they made to you. The bank forces a reversal, pulling the funds right out of your Stripe account, and they hold onto that money while everyone figures things out. To make matters worse, there's usually a non-refundable fee involved.

Demystifying the Stripe Chargeback Process

Getting that first chargeback notification from Stripe can feel like a punch to the gut. It’s not just a simple refund request—it’s a formal dispute where the customer’s bank steps in to play referee. And they almost always side with their customer first.

The moment a customer disputes a charge, their bank yanks the full transaction amount from your account. Bam. Money gone. On top of that, Stripe hits you with a separate dispute fee. You can dig into the full financial impact of the Stripe chargeback fee in our other guide, but the short version is: it stings. The funds vanish before you even get a chance to tell your side of the story.

Why Do Chargebacks Happen in the First Place?

If you want to stop chargebacks, you first have to understand why they happen. It’s easy to jump to the conclusion that it’s all criminal fraud, but the real reasons are often a lot more complicated. Most disputes boil down to one of these scenarios.

Decoding Common Stripe Chargeback Reasons

Here’s a quick-glance table breaking down the most frequent chargeback reasons you'll see in your Stripe Dashboard.

Understanding these codes is the first step, as each one requires a completely different type of evidence to fight back effectively.

These disputes are a massive headache for online businesses. In fact, e-commerce chargeback rates jumped by a staggering 222% in early 2024 compared to the year before. This spike is fueled by the boom in online shopping and a major uptick in "friendly fraud"—where legitimate customers dispute valid charges.

A chargeback isn't just a lost sale; it's an operational speed bump. It forces you to stop focusing on growth and start digging through records to defend your revenue.

The truth is, chargebacks are becoming a standard part of doing business online. Your goal isn't to eliminate them completely (that's impossible) but to manage them smartly so they don't sink your business.

Building Your First Line of Defense Against Disputes

Honestly, the best way to deal with a Stripe chargeback is to stop it from ever happening in the first place. This isn’t about shelling out for expensive security systems. It’s about building a solid foundation with clear communication and smart business practices that nip disputes in the bud.

Think of your checkout process as your first checkpoint. Is everything crystal clear? Vague product descriptions or a return policy that’s buried five clicks deep are common triggers for customer frustration. When a buyer feels misled or confused, their first instinct is often to call their bank, not you.

Fine-Tuning Your Customer Experience

Start by making your policies impossible to misunderstand. Don't hide your refund rules in the fine print of your website footer. Put a clear summary right on the product page or during the checkout flow where no one can miss it.

Another huge one is your billing descriptor—that’s the little line of text that shows up on a customer's credit card statement. If your official business name is "Global Ventures Inc." but you sell products under the brand "Cozy Home Goods," a customer might not recognize the charge. Their next move? Flagging it as fraud.

Pro Tip: Make sure your Stripe statement descriptor is set to your recognizable brand name. This simple change can dramatically cut down on "unrecognized transaction" chargebacks, which are frustratingly common and entirely preventable.

The human element is just as crucial. Proactive, friendly customer service can resolve an issue long before it escalates into a formal dispute. This really just means being responsive and making it incredibly easy for customers to get in touch with you.

You can also head off those pesky "product not received" claims with excellent post-purchase communication. It’s simpler than it sounds. Just implement these steps:

- Send immediate order confirmations that recap exactly what the customer bought.

- Provide shipping notifications with a working tracking link the moment the package is out the door.

- Follow up after delivery with a quick email to make sure everything arrived safely and that they're happy with their purchase.

These proactive touches build a ton of trust and give customers a clear path to resolve any problems directly with you. For a deeper dive, check out our guide on essential strategies for effective chargeback prevention. It's packed with more tips to help you build a stronger defense.

Crafting a Winning Chargeback Response

When a Stripe chargeback notification hits your inbox, the clock starts ticking. This isn't just about a single lost sale; it’s about defending your business’s reputation and bottom line. Firing back a response is more than just clicking "submit evidence"—it's about building a rock-solid, fact-based case that leaves zero room for doubt.

The first move is always to dissect the dispute reason code. A "Fraudulent" claim requires a completely different set of evidence than a "Product Not Received" claim. Resist the urge to just dump every piece of data you have on the bank. Instead, tailor your evidence to directly counter the customer's specific argument. A focused approach shows the card issuer you've actually understood the complaint and have a direct, compelling rebuttal.

Gathering Your Evidence

Your mission is to paint an undeniable picture of a legitimate transaction for a bank reviewer who likely spends mere minutes on each case. Make their job easy. Structure your evidence logically, label everything clearly, and keep it professional.

Depending on the dispute, here’s a quick checklist of the kind of powerful evidence you should be pulling together:

- Communication Records: Got emails, live chat transcripts, or support tickets with the customer? Include them. This proves you were responsive and tried to resolve the issue directly.

- Proof of Delivery: For physical goods, this is non-negotiable. A shipping confirmation with a tracking number that clearly shows "Delivered" to the customer's verified address is your golden ticket.

- Service Usage Logs: If you're running a SaaS or selling digital products, this is your proof. Provide logs showing the customer logged in, used key features, or downloaded their content after the purchase date.

- AVS and CVV Matches: Don't forget the basics. Point out that the Address Verification System (AVS) and CVC/CVV codes matched during checkout. This is a strong signal that the real cardholder made the purchase.

The financial hit from chargebacks is no joke, and it's only getting bigger. Global chargeback volumes are projected to jump from 261 million in 2025 to a staggering 324 million by 2028. In the U.S. alone, the average chargeback value sits at $110 per dispute, which underscores just how critical a solid response strategy is.

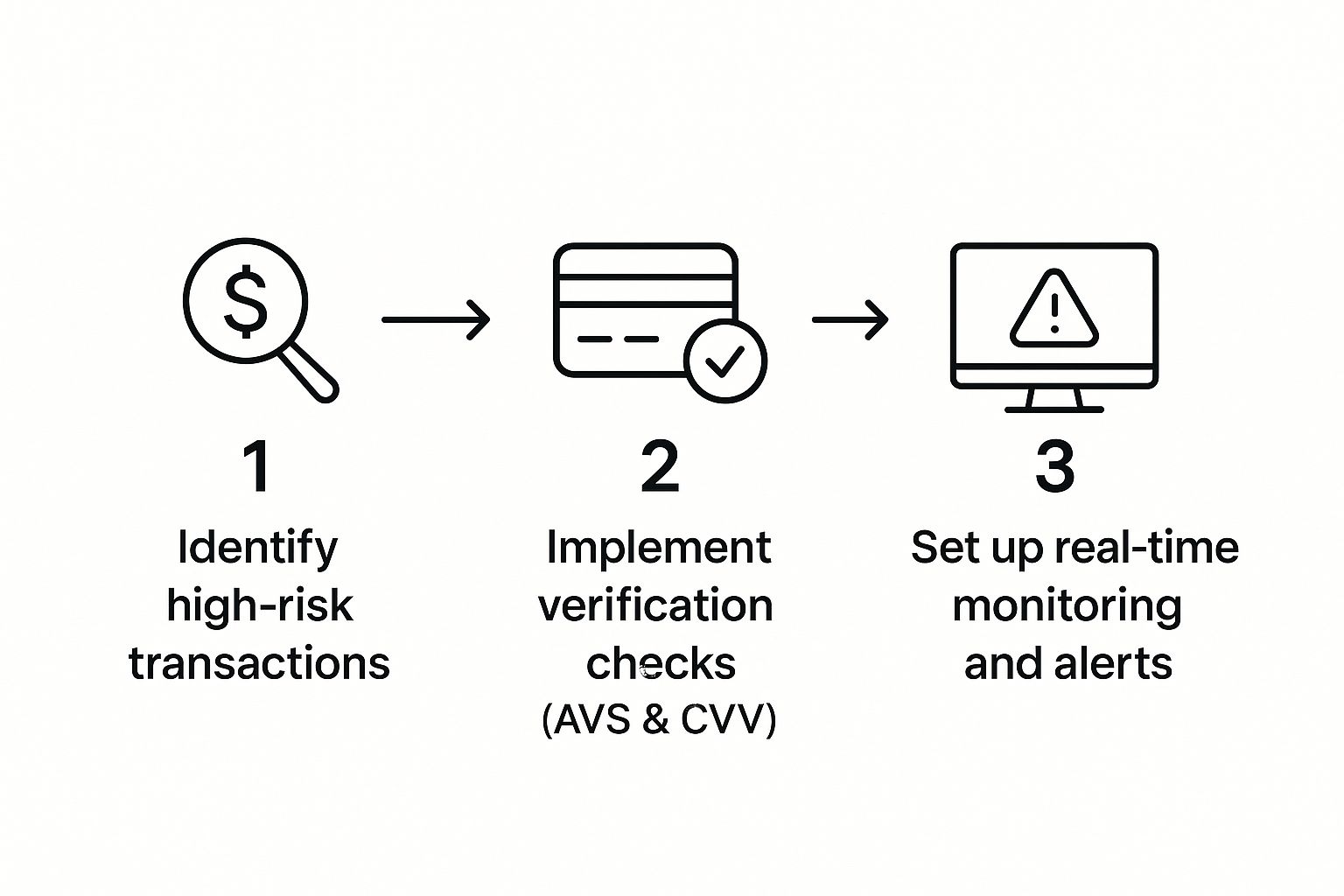

This visual breaks down a simple flow for getting ahead of high-risk transactions before they ever turn into disputes.

As you can see, the best defense is a proactive one. It starts with identifying risky behavior, moves to verification, and finishes with ongoing monitoring to catch problems early.

Structuring Your Rebuttal

Think of your rebuttal letter as your closing argument. It needs to be a concise, professional summary that ties all your evidence together into a clear narrative.

Start by stating the basic facts of the order. Then, address the customer's claim point-by-point, using your evidence to systematically disprove their argument. For a fantastic starting point, you can reference a good chargeback rebuttal letter template.

Your response should be an open-and-shut case. Present the evidence so clearly that the bank reviewer can only come to one conclusion: the charge was legitimate.

Finally, get everything submitted through the Stripe Dashboard. The platform makes it pretty straightforward to upload your documents and write your response. Once you hit submit, the decision is in the hands of the customer’s bank, but a well-crafted response dramatically improves your odds of winning the dispute and getting your hard-earned revenue back.

Getting the Most Out of Stripe's Built-in Tools

So many merchants think of Stripe as just a way to take payments. That’s a huge mistake. You're missing out on some seriously powerful, built-in features that are specifically designed to protect your bottom line. It's time to stop just reacting to disputes and start proactively using Stripe’s own tools to get ahead of chargebacks.

Stripe's secret weapon here is Stripe Radar, its fraud detection system that runs on machine learning. It works pretty well on its own, right out of the box, but you can unlock its real power by tweaking it to fit your specific business. Please, don’t just leave it on the default settings.

Just to give you an idea of its power, during peak shopping seasons like Black Friday, Radar has blocked over 5 million fraudulent transactions per day. That’s more than $229 million in daily losses prevented for businesses like yours. This is the same beast of a system that giants like Amazon and Shopify rely on.

Customizing Your Stripe Radar Rules

This is where you can really make a difference. You can create custom rules to automatically block transactions that look sketchy for your business. Think about what a typical fraudulent order looks like for you. Is it a huge order from a brand-new customer? Is it shipping to a high-risk country?

Here are a few ideas for rules you could set up right now:

- Block any payment coming from a country you don’t even ship to. Easy win.

- Flag any order where the shipping address is thousands of miles from the cardholder's billing address.

- Automatically send any transaction that's way larger than your average order value to a manual review queue.

A well-tuned set of Radar rules is like having a bouncer at the door of your checkout. It automatically turns away the bad guys before they even get a chance to cause trouble. This is your first, and best, automated line of defense.

Of course, fighting disputes is only one part of the puzzle. It's also smart to keep an eye on your processing costs. Getting a handle on Stripe's fee structure by understanding payment gateway fees can help you manage your finances much more effectively.

Is Stripe Chargeback Protection Worth It?

Stripe offers another layer of defense called Chargeback Protection. This is basically an add-on service where, for a fee, Stripe will cover the disputed amount and the dispute fee for you. The best part? No evidence is required from you.

It sounds like a dream, but it does come at a cost, usually a small percentage of each transaction. It’s really built for businesses that crave total predictability in their cash flow. They'd rather pay a small, consistent fee than gamble on the unpredictable costs and time suck of fighting disputes.

To figure out if it's right for you, you have to run the numbers. Our complete guide on https://www.chargepay.ai/blog/stripe-chargeback-protection can walk you through the pros and cons to help you decide if the cost makes sense for your business.

Use Every Dispute as a Lesson, Win or Lose

Every single chargeback that hits your Stripe account is a piece of intel. I know it’s tempting to just sigh, deal with it, and move on, but treating each dispute as a learning opportunity is how you get ahead of the problem. This is the moment you shift from constantly reacting to proactively protecting your business.

Start by looking for the patterns. Go into your Stripe dashboard, export your dispute data, and really look at it. Are most of your chargebacks piling up on a specific product? Maybe the description isn't quite right, or the photos don't tell the whole story. You'd be surprised how often a wave of disputes can be traced back to one small, fixable issue.

Turning That Data Into Action

Once you've got a handle on the "what," it's time to dig into the "why." Don't just glance at the reason codes the bank provides; you have to think about the entire customer journey that led to that dispute.

- Regional Spikes: Seeing a bunch of "product not received" claims from one country? That could be a huge red flag about your shipping carrier in that specific region.

- Campaign-Related Disputes: Did you just run a big marketing campaign and now you're drowning in "product not as described" chargebacks? It’s likely the ad copy promised a little too much.

- Checkout Confusion: If you keep getting hit with "unrecognized transaction" disputes, it might mean your billing descriptor is still confusing customers, even if you thought you'd already fixed it.

Performing this kind of post-mortem on every dispute helps you find the weak spots in your operation. Fixing these root causes is always going to be more effective than just getting better at fighting individual chargeback cases after they happen.

This analytical approach is absolutely critical, especially when you consider that winning disputes is never a sure thing. For a dose of reality on that front, our article on how often merchants actually win chargeback disputes breaks down the numbers.

Get into the habit of reviewing your chargeback data at least once a quarter. This simple routine will help you make smart, informed changes that steadily bring your dispute rate down over time.

Your Top Stripe Chargeback Questions Answered

Dealing with a Stripe chargeback can feel like you’ve been thrown into the deep end, especially when you have a million other things on your plate. You just need clear, quick answers. We’ve pulled together some of the most common questions we hear from merchants to help you get a handle on the dispute process.

How Long Do I Have to Respond to a Dispute?

Time is not your friend here. Once a dispute lands in your Stripe Dashboard, the clock starts ticking. You’ll typically have between 7 and 21 days to pull together your evidence and submit it.

This isn’t a deadline set by Stripe—it comes directly from the card network (like Visa or Mastercard), which means it’s non-negotiable. If you miss that window, you automatically lose. No second chances. Always treat the deadline in your dashboard as the final cutoff.

Can I Just Refund the Customer to Stop the Chargeback?

It's a common impulse. You see the dispute, you just want it to go away, and a refund seems like the quickest path. Unfortunately, it doesn't work that way.

The moment a chargeback is filed, a formal dispute process kicks off with the bank. The funds are already pulled from your account, and issuing a refund at that point won't stop the process or get the dispute fee waived.

Once a chargeback is initiated, the only way forward is through the official dispute process. You either accept the loss or you fight it. Refunding outside of that system means you lose the money twice—once from the chargeback and once from the refund.

What Is This "Smart Disputes" Feature from Stripe?

You might have noticed this feature popping up in your dashboard. Stripe's "Smart Disputes" is an AI-powered tool designed to help automate your responses. The idea is that it analyzes the dispute reason and automatically pulls what it thinks is relevant evidence from your transaction history to submit for you.

Stripe built this to help merchants recover more revenue by creating tailored responses for certain types of disputes. It’s their attempt at helping you fight back more efficiently, but you'll want to take a close look at how it works to decide if it's the right fit for your business.

Does Winning a Chargeback Get My Dispute Fee Back?

This is a really frustrating part of the process for a lot of merchants, but the short answer is no. The dispute fee, which is typically $15 in the U.S., is a fee Stripe charges for the administrative work of managing the case with the bank.

This fee is non-refundable, even if you win the dispute and get the original transaction amount back. It’s best to think of it as the cost of going to bat.

Manually managing chargebacks is a constant drain on your time and resources. ChargePay uses AI to automate the entire dispute process, from generating compelling evidence to submitting responses in real-time. Stop letting tedious disputes eat into your revenue and let our technology recover it for you. Learn how ChargePay can boost your win rate.

.svg)

.svg)

.svg)

.svg)