Don't let the term "chargeback" fool you here. When we talk about a return item chargeback, we're not talking about an angry customer disputing a purchase. It's much simpler than that.

Think of it as the digital version of a bounced check. It’s a bank-initiated reversal that happens when a payment, usually an ACH transfer, just can't go through because of a technical snag like insufficient funds.

The Real Meaning of a Return Item Chargeback

When most merchants hear "chargeback," their minds immediately jump to credit card disputes. That's a whole different beast. A return item chargeback isn't a customer service problem; it's a payment processing problem, triggered entirely by the banking system when a transaction fails.

Basically, it’s a reversal from the bank because the money wasn't actually there to begin with. The most common reasons are insufficient funds (NSF) or the payer's account being closed.

For example, imagine a customer pays a $150 invoice via an ACH debit from their bank account. A few days later, you get a notice that the transaction was reversed. That's a return item chargeback—the customer's bank pulled the money back because their account didn't have the $150 to cover it. You never actually got paid.

Why This Distinction Matters

Understanding this difference is really important because it completely changes how you respond. You don't "fight" a return item chargeback with shipping receipts and customer emails like you would a credit card dispute. Instead, your goal is to sort out the failed payment directly with your customer.

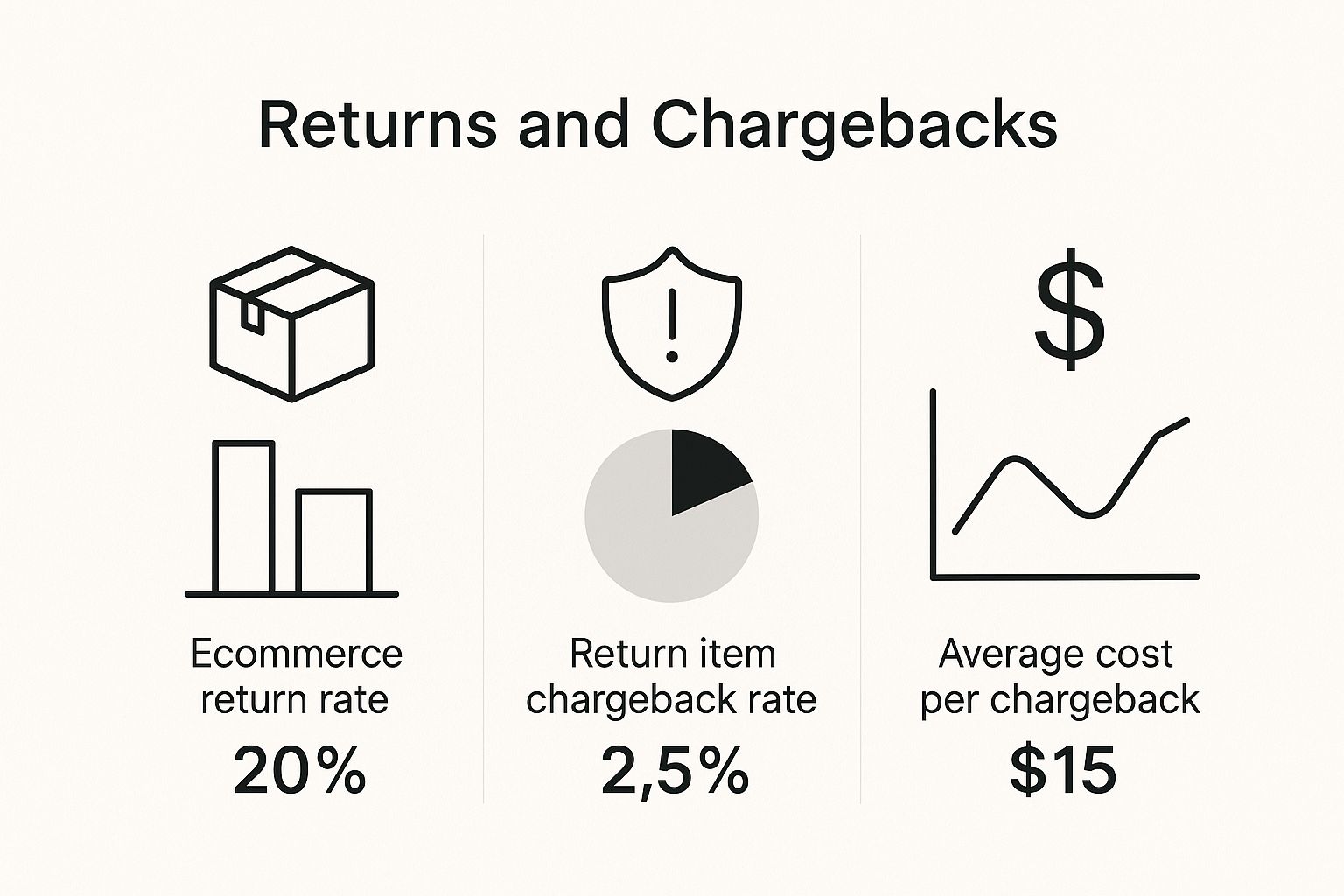

To put the financial hit into perspective, this image breaks down the rates of product returns versus return item chargebacks, and what they typically cost.

As you can see, while they might happen less often than product returns, the direct costs of these failed payments can pile up fast.

Protecting your revenue is a universal challenge for any online business, whether you're dealing with the complexities of understanding and resolving Amazon chargeback disputes or navigating the rules on other platforms. You can even see similar patterns in our guide on handling Cash App chargebacks.

Return Item Chargeback vs. Credit Card Chargeback

Let's break down the key differences in a simple table to make it crystal clear. While both result in lost revenue, their origins and solutions are worlds apart.

Ultimately, knowing which type of chargeback you're dealing with is the first step in protecting your bottom line. Treating a return item chargeback like a customer dispute is a surefire way to waste time and resources without ever getting paid.

So, Why Do Return Item Chargebacks Actually Happen?

If these chargebacks aren't coming from unhappy customers, what's really going on? The answer is less about customer service and more about the nuts and bolts of the banking system.

Think of it as a technical failure, not a customer dispute. The payment simply couldn't clear for reasons that are all about banking rules and security protocols. It’s not about what the customer wants; it's about whether the transaction can go through.

The Most Common Culprits

Most of the time, a return item chargeback can be traced back to one of four main issues. Each one acts like a roadblock, stopping the money from ever reaching your account.

- Insufficient Funds (NSF): This is the classic "bounced check" scenario in the digital age. Your customer’s account just didn't have enough cash to cover the transaction when you tried to process it.

- Account Closed: This one's pretty common. The customer switched banks or simply closed the account they used for the payment, but forgot to update their billing information with you.

- Invalid Account Number: A simple typo during checkout is all it takes. If the bank can't find the account number provided, the payment hits a dead end.

- Stop Payment Order: Sometimes a customer will proactively tell their bank to block a specific payment. This often happens with recurring subscriptions they meant to cancel but forgot to do so on your end.

These problems are all tied to bank security and verifying that real, available funds are there before a transaction is finalized. When one of these payments fails, the bank doesn't just return the amount—they often tack on a fee for the trouble, usually somewhere between $10 and $20.

Imagine a loyal customer who uses your monthly subscription service. They get a new debit card from a new bank but forget to update their payment details on your site. When your system tries to charge the old, now-closed account, it immediately triggers a return item chargeback.

Getting a handle on these root causes is the first step toward building a solid defense. While these are technical glitches, they can sometimes look a lot like intentional fraud. For a deeper look into that side of things, check out our guide on what is chargeback fraud. By pinpointing exactly why a payment failed, you can tailor your response and start preventing these issues from happening again.

The True Financial Impact on Your Business

A return item chargeback feels like you just lost a sale, but the financial sting is much, much worse. The damage isn't just about the initial transaction amount; it's a multi-layered cost that can quietly bleed your business dry if you're not paying close attention. Think of it as a single tipped domino that sets off a chain reaction straight to your bottom line.

First, there's the most obvious hit: the lost revenue from the sale itself. Poof. The money you thought was securely in your account is gone. But it doesn't stop there. Your bank then tacks on a separate return item fee, which usually runs anywhere from $10 to $25, just for the trouble of dealing with the bounced payment.

The Hidden Costs You Can't Ignore

Beyond the direct bank fees and the reversed sale, a whole slew of hidden operational costs sneak in. Every single time a payment fails, someone on your team has to drop what they're doing to:

- Figure out why the payment failed in the first place.

- Get in touch with the customer to sort it all out.

- Manually re-enter or update their billing information.

That wasted time is money you'll never see again. An employee spending even 30 minutes chasing down a failed payment costs your business real money in payroll and lost productivity. To really get a handle on this ripple effect, digging into effective managing cash flow strategies is a must for your business.

Let's run the numbers for a small business: Imagine you get just five return item chargebacks this month on sales of $100 each. You've instantly lost $500 in revenue, paid out around $100 in bank fees, and burned through several hours of your staff's time. That's a minimum of $600—plus payroll costs—that just vanished from your business over a handful of transactions.

This is exactly why knowing what a return item chargeback really means and having a plan to deal with them is so important. It's not a minor annoyance; it's a genuine threat to your financial health.

How to Proactively Stop These Chargebacks

Dealing with the fallout from a return item chargeback is a headache, no question. The good news? You can get ahead of these issues by putting a few smart, proactive strategies in place.

Instead of just reacting when a payment fails, you can build a system that minimizes them from ever happening. This approach doesn't just save you money and fees; it creates a much smoother, more professional experience for your customers.

Verify Before You Charge

This is the single most effective way to stop these chargebacks in their tracks. You need to confirm the customer's bank account is valid and actually has funds before you try to process a payment. It sounds complicated, but it's simpler than you might think.

- Account Verification Services: Tools like Plaid or micro-deposits can instantly check that a customer's bank account is legitimate and active. This step alone weeds out a huge number of problems caused by simple typos or closed accounts.

- Real-Time Balance Checks: Some payment services can also perform a quick check to see if there are sufficient funds available right at the moment of the transaction. This is a game-changer for preventing those frustrating NSF-related failures.

Communicate Clearly and Often

A surprising number of return item chargebacks, especially for recurring subscriptions, happen because customers just plain forgot. A little communication can go a very long way.

By sending a simple automated email reminder a few days before a recurring payment is due, you give customers a chance to ensure their account is funded or update their payment information if needed.

This small step can dramatically reduce accidental payment failures. It shows respect for your customer and helps them avoid overdraft fees, all while preventing that "Oh, I forgot about that" moment that leads straight to an NSF charge on your end. For a deeper dive, our guide on chargeback fraud prevention strategies has even more tips that can help.

Make Your System Smarter

Finally, you can build resilience right into your payment processing workflow. Automation is your best friend here, turning a potential loss into a recovered sale without you having to lift a finger.

Think about setting up these automated actions:

- Automated Retries: If a payment fails, don't just give up. Configure your system to automatically retry the transaction a few days later. Oftentimes, a customer just needs a day or two for a paycheck to land in their account.

- Flexible Payment Options: Guide customers toward payment methods less prone to failure, like credit cards, particularly if they've had an ACH payment fail in the past. This gives them control while protecting your revenue.

Your Step-by-Step Response Plan

Prevention is your best defense, but let's be real—sometimes a return item chargeback is going to slip through. So what happens then?

The good news is that handling one of these is much more straightforward than fighting a traditional credit card dispute. Since there's no formal, evidence-heavy process, your focus shifts entirely to clear, professional communication with your customer.

The goal here is simple: recover the payment while keeping the relationship intact. This isn't about pointing fingers; it's about fixing a simple payment hiccup. And these hiccups happen a lot. With over 238 million chargebacks popping up worldwide in 2023 alone, having a calm, efficient response is crucial. That sheer volume, which you can read more about in these chargeback statistics on Chargeback.io, shows just how much risk merchants are up against every single day.

Your Three-Step Action Plan

When you get that notification about a return item chargeback, the last thing you want to do is panic. Instead, lean on a clear, automated process to get things sorted out quickly.

Automate Customer Notifications: The second a payment fails, your system should fire off a polite, non-accusatory email. This message just needs to state that their recent payment couldn't be processed and give them a secure link to update their billing info. Simple as that.

Temporarily Suspend Service: To stop the bleeding, it’s smart to automatically and temporarily pause their subscription or account access until the payment is sorted. This move protects your business and gives the customer a gentle nudge to fix their details.

Provide a Simple Resolution Path: The key is to make it incredibly easy for the customer to pay you. That notification email should take them straight to a payment page where they can pop in new card details and clear their balance in just a couple of clicks.

A well-managed response turns a potential loss into a positive customer interaction. By handling it professionally, you show that you're organized and value their business, strengthening their loyalty.

This kind of hands-off, automated approach is the core of an effective chargeback solution that protects your revenue without eating up your team's precious time.

Frequently Asked Questions

Still got a few things on your mind? You’re not alone. The whole "return item chargeback" concept can be a bit murky, so let's clear up some of the most common questions. Here are some quick, straightforward answers to get you up to speed.

Is a Return Item Chargeback the Same Thing as Friendly Fraud?

Not even close. Think of a return item chargeback as a technical glitch in the banking system—usually, it’s just a case of insufficient funds or a closed account. It’s an automated process handled entirely by the bank.

Friendly fraud, on the other hand, is a deliberate action. It's when a customer buys something, receives it, and then intentionally disputes the charge with their credit card company to get their money back. One is a simple payment failure; the other is a cardholder trying to game the system.

Can I Fight a Return Item Chargeback?

You can't really "fight" it like you would a credit card dispute. Since the reversal happened for a factual reason—the money just wasn't there—the bank’s decision is pretty much final. There isn't a formal process to challenge it.

Your best (and only) move is to reach out to the customer directly. The goal is to get them to settle the balance using a different payment method.

The key here is to shift your mindset from "disputing" to "recovering." You’re not arguing with the bank; you're working with your customer to solve a payment issue.

How Does Automation Help with These Issues?

Automation is a game-changer. Instead of having someone on your team manually track every single failed payment, modern tools can spot a return item chargeback the moment it happens.

These systems can then automatically trigger a polite notification to the customer, complete with a simple link for them to update their payment details and try again. This not only saves you countless hours but also dramatically increases your odds of recovering that lost revenue quickly.

What’s the Best Way to Tell a Customer Their Payment Failed?

The best approach is always clear, helpful, and non-accusatory. An automated email is perfect for this. It should explain that the payment couldn't be processed and give them a secure, easy way to fix it.

When you frame it as a routine technical hiccup, you preserve the customer relationship. It avoids placing blame and instead focuses on getting to a simple solution. You can also get a better handle on the different costs involved by exploring various chargeback limits and fees.

Stop losing revenue to failed payments and complex disputes. ChargePay uses AI to automate the entire chargeback recovery process, helping you win back more money without lifting a finger. Reclaim your revenue today.

.svg)

.svg)

.svg)

.svg)