Think of 3D Secure as your online store's digital bouncer. It's an extra security checkpoint that happens in a flash when a customer pays, where their own bank quickly confirms it's really them making the purchase. For you, this simple step is a powerful way to stop fraud in its tracks.

What Is 3D Secure Authentication?

Picture a customer in a brick-and-mortar shop using their debit card. The cashier hands them the keypad, and they punch in their PIN. That quick action proves they're the real cardholder, protecting both the customer and the store from a bogus transaction. 3D Secure brings that same level of confidence to your online checkout.

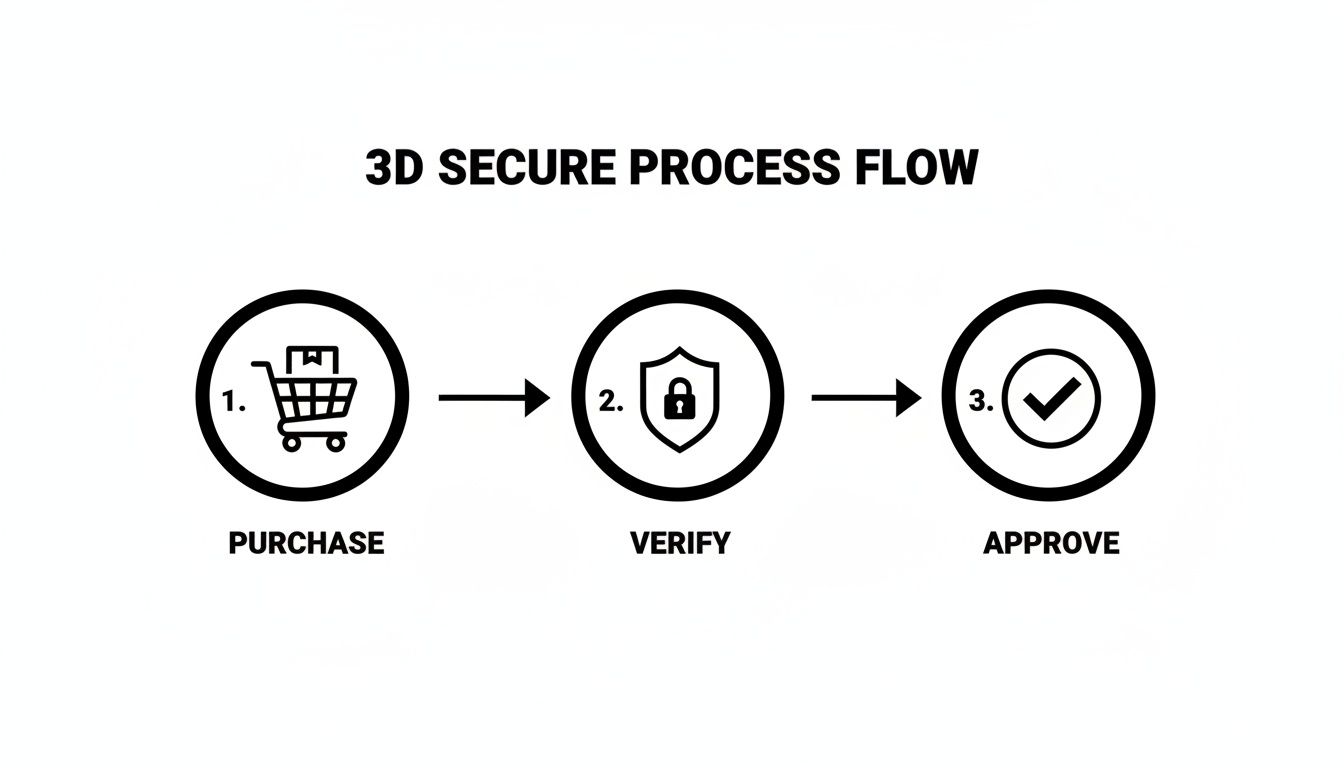

When a shopper hits "buy," 3D Secure springs into action, creating a secure link between your website, the payment network (like Visa or Mastercard), and the customer’s bank. This all happens in seconds. For most legitimate transactions, the check is completely invisible—what we call "frictionless." The system crunches a bunch of data points behind the scenes and gives the thumbs-up without the customer having to lift a finger.

But what if something seems a little off? That's when the system triggers a "challenge."

Think of it like a friendly security guard asking to see some ID. The customer’s bank might just ask for a quick confirmation, like entering a one-time code sent to their phone or using their fingerprint in their banking app.

This extra step is designed to be a piece of cake for real customers but a brick wall for fraudsters trying to use stolen card details. It's a smart way to add serious protection without creating a frustrating checkout experience. You can see a real-world example of this in our guide to Mastercard's SecureCode and how it fits into the payment puzzle.

Let's quickly break down what 3D Secure really means for your store.

3D Secure At A Glance For Merchants

This table shows how 3D Secure isn't just a technical feature; it's a core part of protecting your business's finances and reputation.

The Most Important Benefit: Liability Shift

Beyond just blocking fraudulent payments, 3D Secure delivers a game-changing financial advantage for merchants: the liability shift.

Normally, in the world of e-commerce, you're the one left holding the bag for fraudulent chargebacks. If a stolen card is used at your store, that loss comes straight out of your pocket.

But when a transaction is successfully authenticated with 3D Secure, the tables turn. The financial responsibility for that transaction often shifts from you, the merchant, back to the card-issuing bank. This means if a customer later claims the purchase was fraud, it’s the bank—not your business—that has to cover the loss.

This makes 3D Secure more than just a security measure; it's a powerful financial shield that directly protects your bottom line. By using it, you can dramatically cut your losses from the most common types of e-commerce fraud and process more orders with total confidence.

The Evolution from 3DS1 to Smart 3DS2

The early days of e-commerce security were a bit like the Wild West. The first version of 3D Secure, known as 3DS1, was a major step forward, but it often felt clumsy and heavy-handed. It was designed to stop fraud, but its methods often stopped legitimate customers in their tracks.

Imagine your customer is excited to finally buy something from your store. They've filled their cart, entered their shipping info, and are ready to pay. But right after they hit that final button, they're abruptly redirected to a completely different, often poorly designed, bank webpage. This page would demand a static password they probably set up years ago and have long since forgotten.

This jarring interruption completely shattered the checkout flow. Confused and often suspicious of the strange pop-up, many customers would simply give up and close the tab. This user experience was a certified conversion killer.

The Problem with the Old Way

The biggest flaw with 3DS1 was its one-size-fits-all approach. It treated every single transaction with the same high level of suspicion, forcing good, honest customers through an awkward and frustrating verification process.

This created a real dilemma for merchants: enable 3DS1 for better fraud protection and liability coverage, or disable it to avoid losing sales from abandoned carts? It was a tough choice nobody wanted to make.

The impact was huge. Studies showed that the friction from early 3DS1 protocols caused 25-35% of shoppers to abandon their carts. That's a massive amount of lost revenue, all because of a clunky security step.

This simple flow is what modern 3D Secure aims for—a quick, seamless process that protects everyone without the old friction.

The Smart Solution: 3DS2

This is where 3D Secure 2 (3DS2) completely changed the game. Instead of being a blunt instrument, 3DS2 is a smart, surgical tool. It works silently in the background, acting like an intelligent risk analyst for every single transaction.

Think of 3DS2 as a silent security guard who knows all the regular customers by name. It lets them pass through without a second glance but politely asks for ID from anyone who looks unfamiliar or suspicious.

Instead of interrupting every purchase, 3DS2 analyzes over 100 different data points in real-time. This includes information like:

- The customer's device ID

- Their transaction history with your store

- The shipping and billing addresses

- The total value of the purchase

Based on all this rich data, the system instantly calculates a risk score. For the vast majority of transactions—typically 80-90%—the risk is low. These purchases are approved immediately in what’s called a "frictionless flow." Your customer experiences nothing but a smooth, fast checkout.

Only when the system flags a transaction as high-risk does it trigger a "challenge." But even this step is modern and user-friendly. No more forgotten passwords. Instead, the challenge might be a quick fingerprint scan on a phone, facial recognition, or a one-time code sent via text message. It's fast, secure, and familiar to today's shoppers.

Comparing 3DS1 vs 3DS2 From A Merchant's View

For merchants, the shift from 3DS1 to 3DS2 isn't just a small update; it's a fundamental change in how security and customer experience work together. The old way often forced you to choose between safety and sales, while the new way lets you have both.

Here’s a quick breakdown of the key differences that matter to your business:

Essentially, 3DS2 fixed everything that was broken with 3DS1. It understands that you can't treat every customer like a criminal and that a smooth checkout is just as important as a secure one.

This intelligent, risk-based approach is at the core of modern e-commerce fraud prevention best practices. It allows you to secure your sales without sacrificing the customer experience. By telling the difference between your loyal customers and potential threats, 3DS2 provides powerful protection that actually helps, rather than hurts, your bottom line.

How 3D Secure Shifts Chargeback Liability

If you run an online store, "liability shift" is one of the most important concepts you'll ever learn. It’s not just payment jargon; it's a rule that directly protects your bottom line. Think of 3D Secure as more than a security gate—it’s a financial shield for your business.

Normally, when a customer files a chargeback claiming fraud, the card networks almost always side with them. The burden falls squarely on you. You're out the money from the sale, you've lost the product you shipped, and you get slapped with a painful chargeback fee. It's a triple-whammy.

But when a transaction is successfully authenticated with 3D Secure, the tables turn completely.

The liability for that fraudulent transaction "shifts" from you, the merchant, to the card-issuing bank (the customer's bank). Essentially, the bank is on the hook because their system verified the cardholder. Once 3DS gives the green light, the bank assumes the financial risk.

This is the core benefit of using modern payment security. If a fraudster uses a stolen card but the purchase is authenticated through 3D Secure, you’re generally protected from the financial fallout of that specific fraud claim.

Seeing the Financial Impact in Action

Let's look at a real-world example. Imagine a crook gets their hands on stolen credit card details and tries to make a $500 purchase from two different online stores.

Scenario 1: The Store Without 3D Secure

The fraudster breezes through checkout. The payment is approved without any extra checks. A few weeks later, the actual cardholder spots the charge, reports it as fraud, and files a chargeback.

- The Result: The merchant is in a tough spot. They have to refund the $500, they’re out the cost of the product, and they get hit with a chargeback fee (usually $15-$25). The total loss is easily over $500.

Scenario 2: The Store With 3D Secure

The same fraudster tries the same $500 purchase. This time, 3D Secure activates. The customer's bank flags the transaction as potentially risky and prompts for a one-time code sent to the real cardholder's phone. The fraudster doesn’t have it.

- The Result: The transaction is blocked before any money changes hands. The merchant loses nothing.

- Even Better: In the rare case that a sophisticated fraudster somehow passed the authentication, the liability shift would still protect the merchant. The chargeback becomes the bank's problem, not yours.

This shows that 3D Secure isn't just about stopping fraud—it's about making sure you don't pay the price when it slips through. For merchants everywhere, especially those dealing with high-volume platforms, this is critical for avoiding headaches like Amazon chargeback disputes.

What the Liability Shift Does and Doesn't Cover

It's really important to know that the liability shift isn't a silver bullet. It only applies to specific situations.

This protection is designed for chargebacks filed for fraud-related reasons. These typically include:

- Stolen Card Fraud: When a transaction is made with lost or stolen credit card information.

- "I Don't Recognize This" Claims: When a cardholder insists they didn't authorize a purchase (which can sometimes be friendly fraud).

However, the liability shift will not protect you from chargebacks related to service or product issues. You're still responsible for disputes like:

- Product not as described

- Item was never delivered

- Subscription was canceled but I was still charged

- A refund was promised but never processed

For these types of chargebacks, the responsibility is still yours to prove you held up your end of the deal. 3D Secure is your best defense against fraud, but you still need solid fulfillment and customer service to handle everything else. For a deeper dive into protecting your business, check out our complete guide to Stripe chargeback protection.

Navigating Global Rules Like PSD2 and SCA

If you sell to customers in Europe, you've probably heard about a specific set of rules meant to make online payments safer. This isn't just about ticking a compliance box; it's about making sure your European customers can actually complete their purchases without a hitch. The big one you need to know is the Payment Services Directive 2, or PSD2 for short.

Think of PSD2 as the rulebook for all electronic payments happening within the European Economic Area (EEA). But for e-commerce stores, the most important chapter in that book is a requirement called Strong Customer Authentication (SCA).

SCA is pretty much what it sounds like. It mandates a stronger, multi-step way for customers to prove they are who they say they are during most online checkouts. This rule was put in place to tackle the growing problem of online fraud, making it much tougher for criminals to use stolen credit card details successfully.

What Strong Customer Authentication Really Means

Under SCA, a payment has to be verified with at least two of these three things:

- Something the customer knows: A password or a PIN.

- Something the customer has: Usually their smartphone, used to get a one-time code or an app notification.

- Something the customer is: Biometrics, like a fingerprint or a quick face scan.

If that sounds a lot like the 3D Secure process, you're spot on. 3D Secure 2 is the main technology that banks and payment processors across Europe use to meet their SCA obligations. Without it, you’re not playing by the rules. This idea of layering security is also connected to other payment protection methods, which you can explore in our guide on tokenization in payments.

To put it simply, SCA is the law, and 3D Secure 2 is the tool that helps you follow it. If you plan on selling to European shoppers, turning on 3DS2 isn't just a good idea—it's essential.

The Real-World Impact for Your Store

So, what happens if you ignore SCA? The consequences are instant and painful.

When a European customer tries to buy from your store and you don't have 3DS2 enabled, their bank is legally required to decline the transaction. It doesn’t matter if the customer is legitimate or has plenty of money in their account. The payment will fail, plain and simple.

And this isn't just a European quirk; it's a glimpse into the future of global payment security. The EEA might have been the first to enforce SCA, but other countries are quickly rolling out similar rules to cut down on fraud and protect their citizens.

By setting up 3d secure authentication correctly now, you’re doing more than just staying compliant in Europe. You’re future-proofing your business and building a checkout experience that customers everywhere will trust. You'll be ready for the next wave of security regulations, wherever they pop up.

How to Use 3D Secure on Shopify and Stripe

Getting 3D Secure up and running is probably way easier than you think, especially if your store is on a major platform like Shopify or Stripe. The good news? These guys have already done most of the heavy lifting. You don't need to be a developer or wade through lines of code to get this critical layer of fraud protection working for you.

The whole point is to have the modern, smarter version of 3D Secure authentication (3DS2) running in the background. It should protect your sales without driving legitimate customers crazy. Let's walk through how to make sure it's set up correctly on the platforms you’re already using.

Activating 3D Secure on Shopify

If you're a Shopify merchant and you’re using Shopify Payments, you're already ahead of the game. Shopify has 3D Secure 2 baked right into its native payment gateway. It’s designed to work automatically, so there isn’t a simple "on/off" switch you need to hunt down in your settings.

Instead, Shopify’s system is smart about it. It analyzes every transaction and only triggers an authentication challenge when a customer’s bank demands it for SCA compliance or when it flags a purchase as potentially high-risk. This dynamic approach means you get the benefit of the liability shift without adding friction to every single order.

The best way to confirm it’s active is to look at your checkout. As long as your checkout page is hosted by Shopify (which is the standard setup), 3D Secure is already working. There's nothing more you need to do on your end.

A common pitfall is using an older, third-party payment gateway that hasn't kept up with the times. If you've connected a legacy processor instead of Shopify Payments, it’s vital to check with that provider to confirm they support 3DS2. An outdated gateway could leave you unprotected and might even cause legitimate transactions to fail.

Using 3D Secure with Stripe

Stripe is known for its powerful, flexible payment tools, and its approach to 3D Secure is no different. Just like Shopify Payments, Stripe uses 3DS2 automatically and leans on its intelligent fraud detection system, Radar, to apply authentication dynamically.

Stripe’s logic is built to maximize your sales while crushing fraud. It won't throw up a 3D Secure challenge on every transaction, because that would absolutely kill your conversion rates. Instead, it uses machine learning to score the risk of each payment, only requesting authentication when it’s truly needed or required by regulations like SCA. For a deeper look at how these two platforms stack up, you might find our article comparing Shopify Payments vs Stripe helpful.

You can actually manage how aggressively Stripe applies 3D Secure through your Radar rules. For example, you can create a rule to:

- Request 3D Secure if a payment meets certain criteria you’ve defined as risky.

- Block payments that completely fail the 3D Secure authentication check.

- Allow payments to go through without a challenge if they seem low-risk.

This gives you a bit more granular control than Shopify, letting you fine-tune your fraud prevention strategy to match your store's specific risk level. You can find these settings in your Stripe Dashboard under Radar > Rules. By default, Stripe’s managed rules already handle this for you, but the option to customize is there if you need it. The key takeaway is that Stripe’s system is already optimized to protect you right out of the box.

When 3D Secure Is Not Enough

While 3D Secure is your single best tool for stopping card-not-present fraud, it's not a magical force field against all chargebacks. Think of it as an expert security guard at your front door, checking IDs and turning away known criminals. It’s incredibly effective at its specific job, but it can’t help you once a different kind of problem is already inside.

This is the key limitation every merchant has to wrap their head around. The liability shift from 3D Secure only protects you from disputes related to fraud. It offers zero protection against service-related chargebacks.

These are the disputes where the customer isn’t claiming fraud at all. Instead, they're unhappy with their purchase for a whole host of other reasons.

The Chargebacks That 3D Secure Cannot Prevent

Even with perfect 3D Secure authentication in place, you're still completely on the hook for chargebacks filed under common non-fraud reason codes. These disputes usually fall into a few key categories that every online merchant will recognize instantly.

- Product Not as Described: The customer claims the item they received looks nothing like your website's photos or description.

- Item Not Received: The shopper insists their order never arrived, even if your tracking information says it did.

- Service Canceled: A customer was charged for a subscription after they believe they already canceled it.

- Credit Not Processed: The customer returned an item but is adamant they never got their refund.

In these scenarios, the fact that you used 3D Secure is totally irrelevant. The bank sees a service dispute, not a fraud claim, and the responsibility falls right back on your shoulders. This is where a purely preventative strategy falls short and a reactive one becomes essential.

For these non-fraud disputes, you need more than a shield; you need a tool to fight back and recover your revenue. This is where a proactive chargeback recovery system becomes a crucial part of your defense.

Completing Your Defense with Automated Recovery

This is exactly where ChargePay steps in to fill the gap. While 3D Secure acts as your first line of defense to prevent fraud, ChargePay is your specialized tool to recover revenue from the service-related disputes that inevitably slip through.

ChargePay uses smart technology to automate the entire chargeback representment process. When a "product not received" or "subscription canceled" dispute hits your account, our system automatically gathers the necessary evidence—like shipping confirmations, customer service emails, and usage logs—to build a compelling, evidence-based response. We then submit it on your behalf, fighting to get your money back without you lifting a finger.

The global 3D Secure payment authentication market is projected to reach USD 2.81 billion by 2030, driven by the fight against card-not-present fraud. However, as fraud prevention gets stronger, merchants still need a powerful solution for the disputes that remain. Find out more about the growth of the 3D Secure market and see why a two-part defense is so important.

The message is simple: 3D Secure is your essential shield for fraud prevention. But for everything else, ChargePay is your automated recovery engine. Together, they create a complete defense system that protects your business from all angles, securing your revenue and letting you focus on growth.

Still Have Questions About 3D Secure?

Even after getting the basics down, you might still have a few questions about how 3D Secure plays out in the real world. Let's walk through some of the most common ones we hear from merchants to iron out any final details.

Does 3D Secure Guarantee I Win All Fraud Chargebacks?

Think of it less as a guarantee and more as your ace in the hole. While it's not an automatic win button, a successful 3D Secure authentication is the strongest piece of evidence you can possibly have in a fraud dispute.

When a transaction is authenticated with 3DS, the financial liability for that fraud shifts from you, the merchant, back to the bank that issued the card. In theory, you shouldn't even receive a fraud-related chargeback for that sale. If one does slip through by mistake, providing the 3DS data gives you an almost certain win. Just remember, it offers zero protection against non-fraud chargebacks, like "product not received."

Is 3D Secure Going to Hurt My Conversion Rate?

This is a huge—and totally valid—concern, but it’s mostly a ghost from the past. The old 3DS1 was notorious for its clunky, conversion-killing pop-ups that sent customers running for the hills. The modern 3D Secure 2 (3DS2) was built from the ground up to fix that exact problem.

Today, 3DS2 uses a "frictionless flow" for the vast majority of legitimate purchases. Your good customers won't see a single extra step. It’s only the transactions that a bank’s risk engine flags as suspicious that get "challenged" with a quick, modern verification prompt. When set up correctly, most merchants find 3DS2 has no negative impact and can even boost confidence at checkout.

The key takeaway is that modern 3DS2 prioritizes a smooth customer experience. It works silently in the background to stop fraud without getting in the way of legitimate sales.

How Do I Know if I’m Using 3DS1 or 3DS2?

It's a pretty safe bet you're on the latest version. If you set up your payment system in the last few years, you are almost certainly using the modern 3DS2 protocol.

Major payment processors like Stripe and Shopify Payments have long since upgraded their entire infrastructures. The real tell-tale sign of an outdated 3DS1 system is the dreaded redirect—where a customer is abruptly sent to a separate, clunky-looking bank page to type in a static password. If you ever see that, it’s a major red flag that you need to contact your payment provider immediately to get up to date.

While 3D Secure is your shield against fraud, it doesn't stop service-related disputes. ChargePay automates the fight against all other chargeback types, recovering revenue that 3D Secure can't protect. See how our AI-powered solution can complete your defense system at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)