Account takeover can turn into a chargeback fast. For Shopify stores, the financial hit usually shows up after the fraudster is already inside a real customer account, using saved payment details and a trusted order history to place orders that look legitimate enough to ship.

That is what makes ATO a revenue problem, not just an account security problem. One compromised login can lead to lost merchandise, a dispute from the legitimate customer, chargeback fees, and support time spent cleaning up an order your team thought was safe.

ChargePay sees that pattern every day across 200K+ cases and $10.8M+ recovered for merchants, with a 92.4% win rate on disputes. But recovery is the back end of the problem. The better outcome is preventing the order from becoming a dispute in the first place.

The practical goal is simple: treat account takeover prevention as part of your chargeback prevention strategy for Shopify stores, because every blocked hijacked login is one less fraudulent order that can turn into lost revenue. That means tightening login controls, watching for risky account changes, and giving support teams a clear response path before a compromised account turns into a shipped order and a chargeback.

Why Account Takeover Is a Chargeback Problem in Disguise

Unauthorized transactions are one of the most common reasons cardholders dispute e-commerce purchases. In Shopify, account takeover often sits underneath that claim. What looks like a normal repeat purchase can become a chargeback because the order came from a hijacked customer account, not from the customer.

That distinction matters to your margin. A fraudster who gets into a shopper's account is starting with an advantage your checkout already trusts. They may have access to saved cards, stored addresses, loyalty points, and a buying pattern that helps the order pass basic fraud checks. By the time the customer notices, the package may already be out the door and the dispute clock has started.

A common pattern after compromise is account detail changes, especially email or phone updates that keep the customer from seeing alerts or resetting access quickly. For a merchant, that delay is expensive. It gives the attacker time to place orders, reroute shipments, or make account changes that complicate your evidence later.

Practical rule: Treat account takeover as an order risk and a chargeback risk, not only a login risk.

That is why ATO belongs inside your broader chargeback prevention strategy for Shopify stores. The revenue chain is straightforward:

- A legitimate account gets compromised

- The fraudster uses stored trust to place an order

- The customer notices after fulfillment or after a card statement posts

- The issuer receives an unauthorized transaction claim

- Your store absorbs lost goods, fees, and dispute work

Why merchants miss it

Commonly, store owners look for classic card fraud signals such as a first-time buyer, mismatched billing and shipping, a throwaway email, or an unusually large basket. Those checks still matter, but ATO often slips past them because the transaction arrives wrapped in account history your store recognizes.

The order can look clean on the surface. Same customer profile. Same saved card. Familiar order cadence. Sometimes the only early clues are subtle, like a recent password reset, a new device, an updated phone number, or a shipping change that appears right before checkout.

That is also why stronger login controls have a direct financial payoff. Following multi-factor authentication best practices does more than protect accounts. It reduces the number of fraudulent orders that turn into unauthorized chargebacks.

The business view

ATO creates costs well beyond the order amount. Support teams handle the complaint. Operations may need to intercept fulfillment or deal with reships. Your team has to pull logs, account changes, and order details fast enough to respond to the dispute. Even if you identify the problem quickly, the time drain is real and the margin loss is usually larger than merchants expect.

For Shopify brands, preventing account takeover protects revenue twice. It stops bad orders before inventory leaves the warehouse, and it cuts the chargebacks, fees, and customer trust damage that follow once a compromised account is used successfully.

Fortify Your Shopify Store Login

Every stolen login that reaches checkout can turn into lost inventory, dispute fees, and an unauthorized chargeback. That makes login security a revenue control, not just an IT task.

For Shopify stores, the login page is often the first place to stop a chargeback that has not happened yet. If an attacker cannot get into a customer account, they cannot use saved cards, stored addresses, loyalty points, or order history to make a fraudulent order look legitimate. That matters because orders placed through real customer accounts are harder to catch later in the flow and harder to defend once the cardholder disputes them.

Stop relying on passwords alone

Passwords still fail in predictable ways. Customers reuse them across sites. Old breaches keep feeding credential-stuffing attacks. Bots test those credentials at a scale no manual review team can match.

Adding MFA helps, but the method matters. SMS codes add some protection, yet they are weaker than authenticator apps or passkeys and can create support friction if customers lose access to a phone number. The practical goal is to add stronger verification where the account value is high and the attack risk is real. A useful companion resource on rollout and policy decisions is this guide to multi-factor authentication best practices, especially if your team is deciding what to require for staff accounts versus customer logins.

Staff accounts should be locked down first. A compromised admin login can do far more damage than a single customer takeover because it can expose orders, refunds, apps, and store settings in one session.

Use risk-based friction instead of blanket friction

The right login setup does not challenge every customer the same way. It adds checks when the session looks wrong.

Good triggers include:

- New device or browser: The customer signs in from a setup your store has not seen before.

- Unusual location: The login originates from a country or region that does not fit prior behavior.

- High attempt volume: One account or many accounts receive repeated login attempts in a short period.

- Sensitive account changes: The session tries to update email, phone, password, or default shipping details soon after login.

This approach protects conversion. Real customers with familiar patterns move through quickly. Higher-risk sessions get extra verification before a fraudster can place an order that becomes a chargeback a week later.

Add anti-automation at the login layer

Many ATO attacks are automated, so the login page needs controls that slow scripts down before they become successful sessions.

Start with the basics:

- Rate limiting on repeated login attempts

- Bot detection that separates human traffic from automated abuse

- Device and browser checks to identify repeated attack infrastructure

- Alerts when failed logins or suspicious login patterns spike

These controls pay off beyond security. They reduce the number of compromised accounts that make it into checkout, which means fewer fraudulent orders to review, fewer support escalations, and fewer disputes tied to saved payment methods. If you are reviewing your broader stack, connect login controls with your Shopify fraud prevention controls so account abuse and checkout abuse are handled as part of the same revenue protection system.

Choose controls your team can actually maintain

Merchants often overbuy tools and underuse them. A simpler setup that your team monitors every week is usually better than an advanced stack no one tunes.

| Approach | What it does well | Where it falls short |

|---|---|---|

| Password-only login | Low friction for customers | Weak against reused or stolen credentials |

| SMS MFA | Improves account protection | Can be bypassed through phone-related attacks and adds recovery issues |

| Authenticator app or passkey | Stronger proof the user is legitimate | Requires customer setup and support planning |

| Bot controls plus adaptive checks | Stops scale and applies friction where risk is higher | Needs ongoing review so false positives do not hurt conversion |

If you only make one change here, strengthen MFA for admins and high-risk customer logins, then monitor login abuse like a fraud signal tied directly to future chargebacks.

Here's a short walkthrough on why the login layer matters and what stronger account protection looks like in practice:

Spot Trouble Before It Becomes a Chargeback

Many successful account takeovers are detected only after the attacker is already inside the account. For a Shopify store, that delay is expensive. By the time the customer notices, the order may have shipped, the refund request may be open, and the dispute can be days away.

For chargebacks, post-login behavior is often the primary warning layer.

Proofpoint notes in its account takeover fraud reference that attackers increasingly exploit the post-login phase. That matches what shows up in e-commerce losses. A fraudster does not need to brute-force checkout if they can log in, change account details, and place an order that looks like normal customer activity.

How account takeover turns into revenue loss

A typical sequence is simple. Stolen credentials get the attacker into a real customer account. They change the email address or phone number, update shipping details, and place an order with a saved card or trusted profile.

At that point, the payment can look legitimate enough to pass basic checkout screening.

Then the legitimate customer reports the order as unauthorized. You lose the product, absorb fulfillment costs, spend time on support, and face a fraudulent chargeback that started as an account abuse problem.

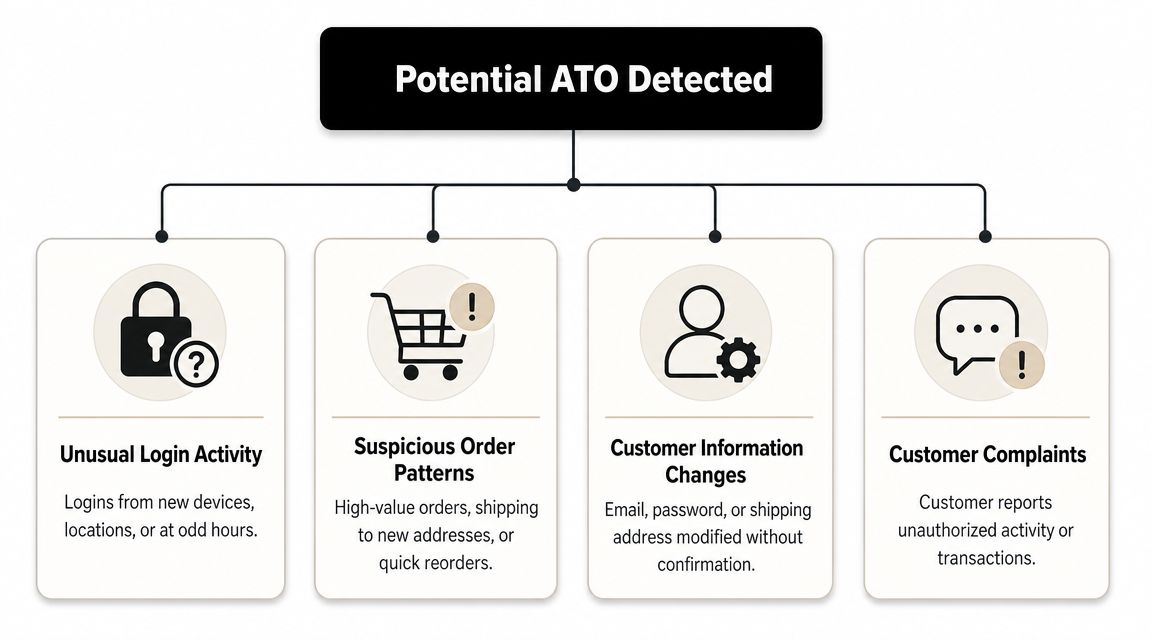

The signals that matter most

Effective detection usually comes from combining a few practical signals, not from chasing every anomaly.

Profile changes right before checkout

Email, phone, password, or shipping edits made shortly before an order should raise the risk score. Fraudsters often change these fields first to block alerts and redirect the order.A new device followed by sensitive actions

A first-time device is common. A first-time device that immediately changes credentials, adds a new address, or places a high-value order deserves extra friction or review.Order behavior that breaks the customer's pattern

A customer who usually buys low-risk items suddenly ordering expensive, easily resold products to a new address is not proof of fraud, but it is a useful signal.Customer complaints tied to account changes

“I stopped getting emails,” “my address changed,” or “I didn't place this order” are often early signs of takeover, not routine service tickets.

Connect the signals to action

The operational mistake is not missing every signal. It is seeing them in isolation.

A password reset by itself may look harmless. A new device by itself may be normal. An address change by itself may be legitimate. Stack those events together over a short window and the risk picture changes fast.

Set up a response flow your team can run every day:

| Trigger | Immediate action | Revenue impact |

|---|---|---|

| Email or phone changed | Verify the change and flag the account | Helps stop notification hijacking before an order is placed |

| New device plus profile edits | Require re-authentication or review | Reduces the chance of a compromised session placing a “good” order |

| Unusual order after account changes | Hold fulfillment briefly | Prevents shipped goods from turning into a chargeback loss |

| Customer reports unauthorized activity | Freeze sensitive actions and investigate account history | Limits repeat abuse and gives your team evidence for dispute handling |

Speed matters here. If multiple weak signals appear together, treat the account like a payment risk issue, not just a login issue.

Broader transaction monitoring solutions help by combining account events, order details, and customer behavior into one decision. That reduces the gap between “we saw something odd” and “we stopped a chargeback.”

Use support signals as fraud signals

Support teams often catch account takeover before tooling does.

A customer asking why order confirmations stopped arriving. A request to rush-ship an order after account details changed. A complaint about saved information being updated without consent. Those are all worth feeding into your fraud process.

Stores that share these signals across support, fraud review, and fulfillment stop more bad orders before shipment. That protects margin and cuts off one of the most frustrating chargeback sources, orders that looked legitimate only because the attacker used a real customer account.

Your Customer Support ATO Response Plan

Once a customer account is suspected of being compromised, speed matters. So does discipline.

Proofpoint notes that attackers increasingly exploit the post-login phase, and its research argues that focusing only on login protection is a mistake. Defenses need to monitor for unusual in-account actions, such as new forwarding rules or rapid profile changes, because a compromised session may already have passed authentication in its account takeover fraud reference.

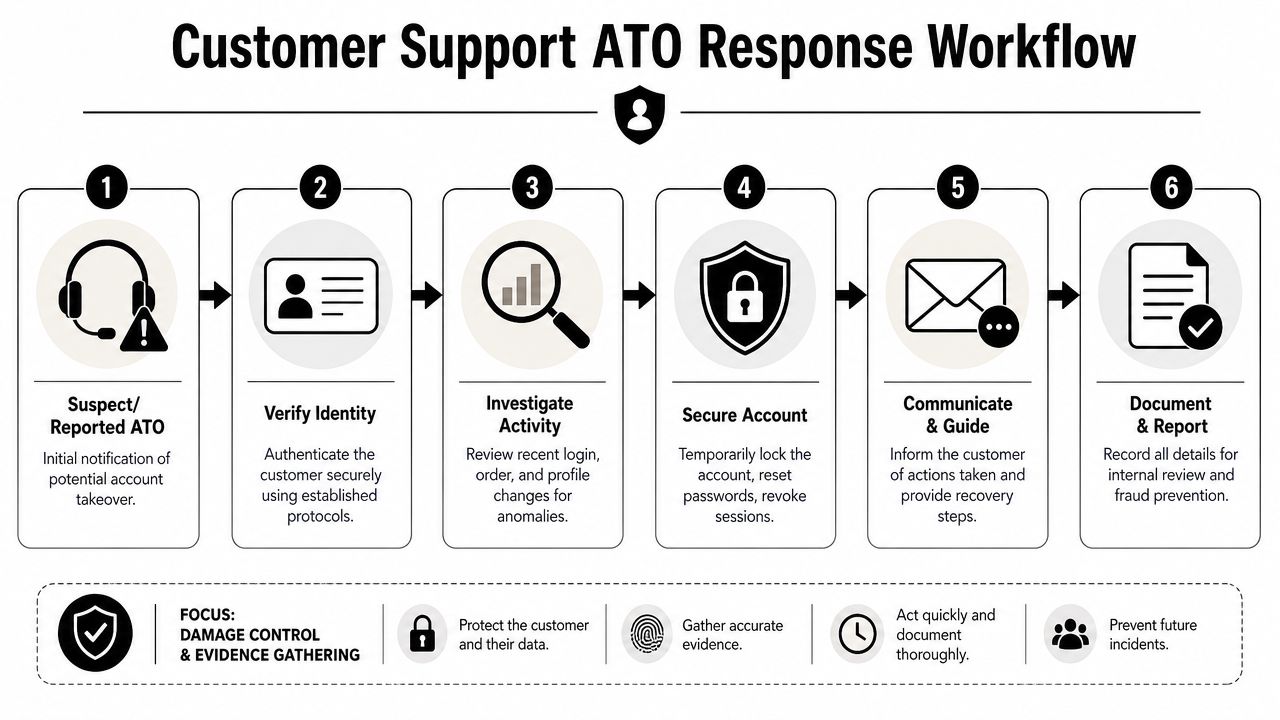

That's why customer support needs a real ATO playbook, not a loose set of ad hoc responses.

Step one is identity, not reassurance

When a customer reports suspicious activity, support should slow down just enough to verify who they're talking to. Don't rely on the same compromised channel if the email address or phone number may have been changed.

Use your established verification steps. Then move quickly.

Lock down what can still be abused

After identity checks, contain the account. The exact workflow depends on your tools, but the goals are consistent:

- Revoke active sessions

- Force a password reset

- Pause sensitive changes where possible

- Flag recent orders tied to the account

- Escalate high-risk shipments before fulfillment

Many merchants lose recoverable revenue when they focus on helping the customer log back in without stopping the order flow. A good support process protects the customer and the order queue at the same time.

Investigate the timeline

Support teams don't need to act like forensic analysts, but they do need a structured timeline.

Look for:

- Recent login changes such as a new device, fresh location, or unusual access time

- Profile edits including email, phone, password, or address changes

- Order actions like a new shipping destination, a fast reorder, or unusual cart value

- Communication anomalies such as the customer saying they stopped getting account notifications

A short internal checklist helps here more than a long policy manual.

The most useful evidence is usually chronological. What changed first, what happened next, and when did the customer notice?

Communicate like a fraud responder

Customers who've lost account access are stressed and often angry. Generic support language makes that worse.

A better response sounds like this in practice:

Acknowledge the issue clearly

Tell them you're treating it as possible unauthorized account access.State the immediate actions taken

Explain that sessions were revoked, credentials were reset, or sensitive activity was paused.Give exact next steps

Tell them how to regain access safely and what notifications to watch for.Tell them what you're reviewing

If there are recent orders under review, say so.

Merchants that already invest in customer service best practices usually recover trust faster here, because the team knows how to combine empathy with process.

Document for the dispute you may face later

Every ATO response should leave a paper trail. Save the account change history, support transcript, login timeline, order details, and the actions your team took after the report.

That documentation serves two purposes. It helps you resolve the incident internally. It also gives you a factual record if the customer later disputes the purchase through their bank.

A weak response creates two losses. You lose the customer's trust, and you lose the evidence window.

From ATO Prevention to Fewer Chargebacks

Account takeover prevention is often described like a security project. For merchants, it's better understood as a margin defense project.

The reason is simple. Every blocked takeover can prevent an unauthorized order, a refund headache, and a chargeback. Even when the fraud gets through, the controls you use to detect it create the evidence you'll need later.

That link became much clearer after the early 2020s rise in industrialized ATO. Transmit Security notes that bot-driven credential stuffing helped drive a 300% jump in losses, which pushed merchants and platforms toward layered controls such as bot management, device fingerprinting, and behavioral monitoring in its analysis of the rise of account takeovers and how to prevent them. For chargebacks, that shift matters because these systems don't just block abuse. They also record context.

Prevention tools also produce dispute evidence

When a bank reviews a dispute tied to a compromised customer account, raw claims don't help much. Evidence does.

The most useful evidence often comes from the very controls you installed to prevent ATO in the first place:

| Control | What it can show in a dispute |

|---|---|

| Bot management | Login activity looked automated or abusive |

| Device fingerprinting | The purchase came from a device that didn't match the customer's normal pattern |

| Behavioral monitoring | The session behavior differed from expected account use |

| Account change logs | Email, phone, password, or address changes happened around the disputed order |

That doesn't guarantee a win in every case. But it moves you from “the cardholder says it wasn't them” to “here is the account behavior that shows the account was compromised.”

Why weak controls hurt twice

When stores underinvest in account takeover prevention, they take two hits.

First, they allow more fraudulent orders through. Second, they lose the evidence that could have clarified what happened. If you don't log account changes well, don't capture device context, and don't tie suspicious actions into one timeline, you're left arguing from fragments.

That's a bad place to be during representment.

ATO controls pay for themselves twice. Once when they stop fraud, and again when they help explain a disputed transaction.

The operational takeaway

Merchants sometimes separate fraud prevention, support, and dispute handling into unrelated tasks. They're not.

A login alert can become an order hold. An account change log can become dispute evidence. A support transcript can confirm when the customer first reported lockout. When those records connect cleanly, your team has a much stronger financial defense.

The stores that handle ATO well aren't just “more secure.” They're better at preserving revenue after an incident too.

Automate Your Defense with ChargePay

Account takeover prevention protects more than logins. It protects recoverable revenue.

Even with stronger authentication, session checks, and support controls, some compromised-account orders will still turn into disputes. At that point, the financial outcome depends on speed, documentation, and whether your team can show a clear account timeline before the deadline closes.

ChargePay helps Shopify merchants do that work without pulling staff into a manual evidence chase. It pulls together fraud signals, order details, and account activity into a dispute-ready case. You can review the workflow on the ChargePay product page.

For a Shopify operator, that matters for a simple reason. ATO losses rarely stop at the first fraudulent order. They often turn into chargebacks, lost merchandise, staff time, and higher payment risk if the pattern continues.

ChargePay reports a 92.4% win rate, has handled 200K+ cases, and has recovered $10.8M+ for merchants. The product automates the work that usually slows dispute response: collecting records, organizing account events into a usable timeline, and preparing the case before issuer deadlines create another loss.

The fit also matters. ChargePay is built for Shopify, so the workflow matches how store teams investigate order disputes. Merchants also get clear trust signals, including a 4.9-star rating and the Built for Shopify badge.

If your store is already seeing unauthorized transaction claims, suspicious account changes, or “I didn't place this order” disputes, the goal is to do more than investigate faster. The goal is to keep more revenue, reduce preventable chargeback losses, and give your team a repeatable process when ATO incidents hit.

Stop losing money to account takeover fraud and the chargebacks that follow. Install ChargePay from the Shopify App Store and let AI fight your disputes with a 92.4% win rate, 200K+ cases handled, and $10.8M+ recovered.

.svg)

.svg)

.svg)

.svg)