An Address Verification System (AVS) is a simple but powerful tool that springs into action the moment a customer hits "buy" on your website. Think of it as a quick, automated security check that helps shield your business from payment fraud.

What Are Address Verification Systems, Anyway?

Picture AVS as a digital bouncer for your online store. It's your first line of defense, working in the blink of an eye to vet a credit card transaction before it's even approved.

The whole process is refreshingly simple. When a customer types their billing address into your checkout form, AVS instantly sends that information to the card-issuing bank. The bank then compares the numbers in the street address and the ZIP code to what it has on file. This isn't about making sure a package gets to the right doorstep; it's purely a security check to help confirm the person making the purchase is the legitimate cardholder.

Why This Matters for Your Business

Every online merchant knows the sting of a chargeback. They drain your revenue, eat up your time, and can seriously damage your standing with payment processors. This is exactly where an address verification system proves its worth. By flagging a transaction with a mismatched address before you finalize it, AVS lets you stop potential fraud right at the door.

This quick check has a direct impact on your bottom line by:

- Reducing Fraudulent Transactions: It makes it much harder for a thief with stolen card details to complete a purchase.

- Cutting Down on Chargebacks: Fewer fraudulent sales mean fewer "unauthorized transaction" chargebacks filed against your business.

- Protecting Your Revenue: By blocking these losses, you hold onto more of the money you've rightfully earned.

A common mix-up is thinking AVS verifies the shipping address. In reality, its only job is to check the billing address for payment authorization. It's a small distinction, but it's critical for understanding its role in your overall security setup.

The Growing Need for AVS

The importance of these systems is only growing. As e-commerce continues to boom, so does the attention it gets from fraudsters. In fact, the global Address Verification Software market is projected to rocket from USD 6.65 billion in 2023 to USD 12.1 billion by 2032.

North America currently accounts for about 37% of this market, largely because the massive volume of online sales in the US and Canada demands strong tools to clamp down on fraud and prevent delivery issues. For a deeper dive, check out this detailed report on the address verification market.

Putting a solid AVS strategy in place isn't just a technical tweak; it's a foundational layer of trust and security for your business. Understanding how AVS works is the first step, and you can learn more about how it fits into a broader strategy in our guide to AVS fraud prevention.

How AVS Works Behind The Scenes

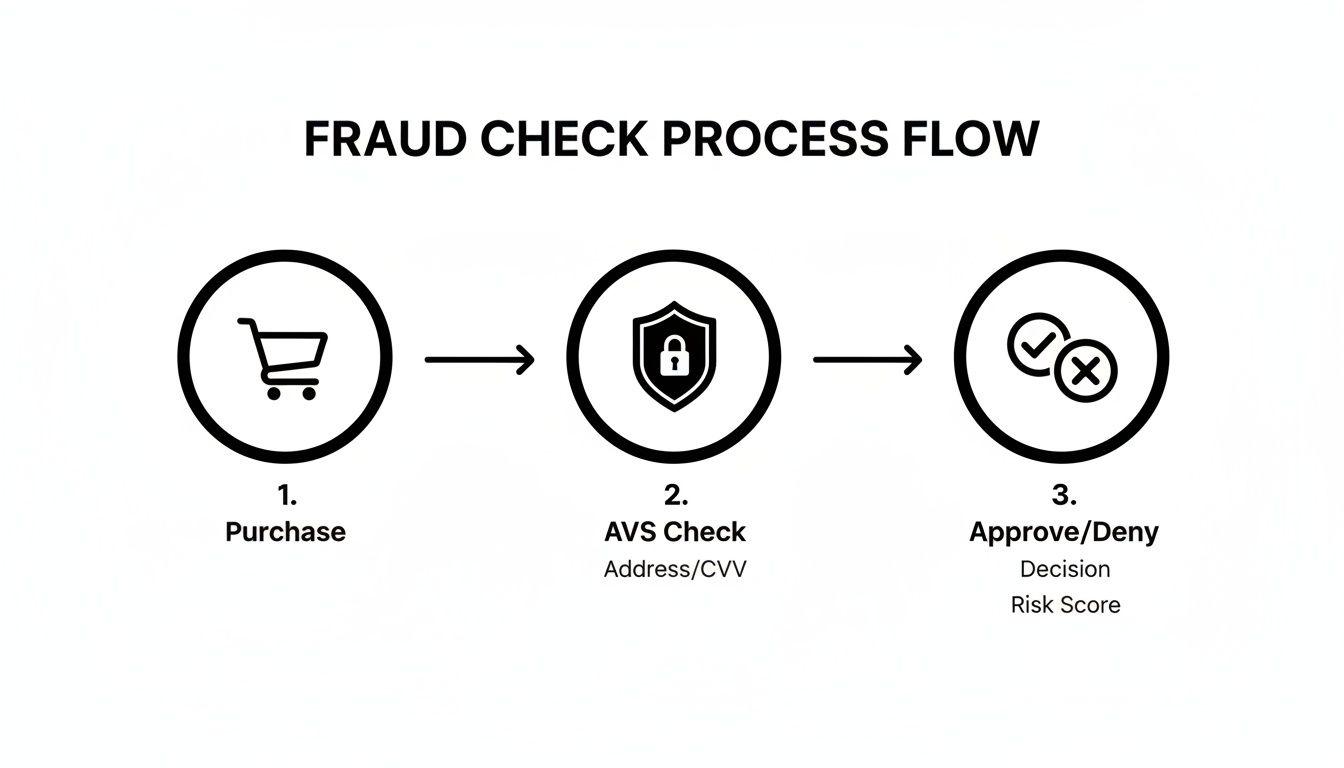

Ever wondered what actually happens in those few seconds between a customer hitting “buy” and their order being confirmed? Let's pull back the curtain on how an address verification system works. You don’t need to be a tech wizard to get it—the whole process is surprisingly simple and lightning-fast.

When a customer fills out their credit card details and billing address, your payment gateway—whether it's Stripe, PayPal, or another provider—jumps into action. It cleverly isolates just the numerical parts of the address: the street number (like the "123" in "123 Main St") and the ZIP code.

That’s it. Just those two numbers get sent over to the bank that issued the customer's credit card. The street name, city, and other details are ignored for this specific check, which is what makes the whole thing happen in the blink of an eye.

This diagram breaks down the basic fraud check from purchase to the final decision.

As you can see, the AVS check is a quick, automated step that helps your system decide whether to give a transaction the green light or stop it in its tracks.

The Bank's Role In The AVS Check

Once the customer’s bank receives the street number and ZIP code, it does a quick side-by-side comparison. It checks those numbers against the official billing address it has on file for that credit card. Simple as that.

Based on what it finds, the bank pings back a single-letter AVS response code to your payment gateway. Think of this code as a simple signal—not a detailed report, but a quick "yes," "no," or "maybe."

Your payment gateway then takes that code and acts based on the rules you've set up. For instance, you can tell your system to automatically reject any transaction with a total mismatch but maybe flag partial matches for a quick manual review. This single-letter code is what makes address verification systems such a powerful, real-time filter against fraud.

Decoding Common AVS Response Codes

Getting familiar with these codes is a game-changer for any merchant. While there are a bunch of them, you'll likely only see a handful on a regular basis. Knowing what they mean helps you tighten up your fraud settings without accidentally blocking legitimate customers.

The AVS code is a recommendation, not a command. It’s a data point to help you make a smarter decision, but you're still in the driver's seat when it comes to deciding what to do with a match, mismatch, or partial match.

Here’s a quick reference guide to help you understand what the most common AVS response codes from your payment processor actually mean.

Ultimately, these codes give you the intel you need to configure your payment gateway to fight fraud effectively while still giving your real customers a smooth checkout experience.

The Real Benefits and Limitations of AVS

Address verification systems are a fantastic first line of defense for any online store. Think of AVS as a quick, effective bouncer at the door of your checkout process. It’s a low-cost fraud filter that works in real-time to protect your revenue from some of the most common types of fraud.

But like any security tool, it's not a magic bullet. You have to be realistic about what it does well and where it falls short. Understanding this balance is the key to building a smarter, more complete defense against fraud without accidentally turning away good customers.

Let's break down the genuine pros and the very real cons.

The Upside: What AVS Does Brilliantly

The best thing about AVS is its speed and simplicity. It gives you an instant check that helps stop obvious fraud before it ever becomes a problem, which translates into some significant wins for your business.

Here’s where it really shines:

- Reduced Chargebacks: This is the big one. By flagging transactions where the billing address numbers don't match up, you make it much harder for someone with stolen card details to buy something. Fewer fraudulent transactions mean fewer chargebacks related to unauthorized card use, which directly protects your bottom line.

- Low-Cost Security: For most merchants, AVS is just a standard feature that comes with their payment processor. There are no extra fees or complicated software to install, making it one of the most cost-effective security measures you can possibly implement.

- Real-Time Decisions: The AVS check happens in the blink of an eye—literally milliseconds. This speed means you can block a sketchy transaction instantly without adding any friction or delay to the checkout process for your legitimate customers.

- Increased Customer Trust: Your customers might not know what "AVS" stands for, but they definitely know what a professional, secure checkout process feels like. This small security step helps build confidence and contributes to a trustworthy brand image.

At the end of the day, these systems are excellent at catching unsophisticated fraud—the kind where a thief only has the card number, expiration date, and CVV. But relying on it alone is a mistake that can leave your business exposed.

The Downside: Where AVS Can Fall Short

While AVS is a powerful tool, it has some critical limitations that every merchant needs to get their head around. If you ignore them, you're looking at lost sales and a false sense of security.

The system's single biggest weakness? It only checks the numerical parts of an address—the street number and the ZIP code. It completely ignores the street name, city, and state.

This means a fraudster who knows the correct house number and ZIP code but enters the wrong street name could still get a partial AVS match. Depending on how your gateway is configured, that fraudulent transaction might just slip right through.

Another major challenge is its spotty global reach. Address verification systems are most reliable in the United States, the United Kingdom, and Canada, where the banking infrastructure fully supports it. Once you go outside of those regions, support can be patchy or completely nonexistent.

This creates a couple of big headaches for businesses with an international customer base:

- False Declines: When an international bank doesn't support AVS, it often returns a "System Unavailable" or "Not Supported" code. If your fraud rules are too strict, you might automatically decline these transactions, frustrating perfectly good customers and costing you sales.

- Inability to Verify: For those same international orders, you lose AVS as a security signal entirely. You can't use it to gauge the transaction's risk, forcing you to rely on other fraud prevention tools to make a decision.

These limitations are exactly why AVS should never be your only defense. For any business handling card-not-present sales, it's absolutely vital to layer AVS with other security measures to create a truly robust and intelligent protection strategy.

Setting Up AVS on Your E-Commerce Platform

If you're running your store on a major platform like Shopify or using processors like Stripe or PayPal, I've got some good news. The basic Address Verification System (AVS) is almost always built-in and running from day one. You don’t need to install a thing to get started.

But the real magic isn't just having AVS—it's in fine-tuning the settings to fit your store's unique risk profile. This is where you transform AVS from a simple background check into an active, strategic part of your defense.

By adjusting how your store reacts to different AVS response codes—like a perfect match, a partial match, or a complete miss—you create a much smarter filter. The goal is to walk that fine line between blocking obvious fraudsters and making sure your legitimate customers can check out without a hitch.

Finding and Customizing Your AVS Settings

Most payment gateways tuck their AVS settings away in a fraud prevention or risk management dashboard. While the exact location can vary, you're usually looking for a section labeled "Rules," "Filters," or "Protection Settings." This is your command center for telling the system what to do with AVS responses.

For instance, you can set up simple but powerful rules:

- Always Accept: Greenlight any transaction with a full address and ZIP code match (AVS code 'Y').

- Always Decline: Automatically block any transaction where nothing matches (AVS code 'N').

- Flag for Review: This is the crucial one. Set transactions with partial matches (like codes 'A' or 'Z') aside for a quick manual look.

That last option is your secret weapon. A partial match isn’t an automatic red flag for fraud. It could just be a loyal customer typing their address in a hurry. By flagging these orders instead of instantly rejecting them, you give yourself the chance to save a sale you might have otherwise lost.

Tailoring Rules to Your Business

There’s no "best" way to configure your AVS rules—it all depends on your business. What you sell, who your customers are, and your personal comfort level with risk all play a role. A one-size-fits-all approach is a recipe for either letting fraud slip through or frustrating good customers.

Think of your AVS settings as dials you can turn up or down, not a switch you just flip on. The idea is to create a dynamic defense that protects your revenue without killing the customer experience.

Consider creating different rules for different scenarios:

- For Low-Value Orders: You can afford to be a bit more lenient. If someone is buying a $15 t-shirt and the ZIP code matches but the street address is slightly off, is it worth killing the sale over a potential typo? Probably not.

- For High-Ticket Items: For a $1,500 laptop, you need to be much stricter. Here, you might decide to automatically reject any transaction that doesn’t have a full AVS match to avoid a costly chargeback.

This kind of flexible approach is easier to implement than ever. The global AVS market is expected to hit USD 2,500 million by 2025, largely because of the boom in e-commerce. With over 70% of US enterprises now using cloud-based tools, this technology is baked right into the platforms merchants use every day. You can read more about it in this in-depth address verification service report.

By regularly checking your AVS settings and tweaking them based on your sales data and chargeback trends, you can build a highly effective, custom security net. For Shopify merchants, mastering these tools is a key part of a strong security plan. Check out our guide on advanced Shopify fraud prevention to see how AVS fits into the bigger picture.

Building a Complete Fraud Prevention Strategy

An Address Verification System is a fantastic tool, but it should never be your only line of defense. Think of AVS as the sturdy lock on your shop’s front door—it's absolutely essential, but you wouldn't rely on it alone. For real security, you also want an alarm system, cameras, and maybe even reinforced windows.

In e-commerce, this exact same layered approach is what separates a vulnerable store from a well-protected one. By stacking different security tools together, you create a much tougher defense that is significantly harder for fraudsters to bypass. Each layer checks for different red flags, protecting your revenue from multiple angles.

Combining AVS with Other Key Tools

The goal is to build a smart, multi-layered system where each tool covers the potential blind spots of the others. When you combine AVS with other verification methods, you get a much clearer, more complete picture of whether a transaction is legitimate or not.

Here are the essential layers to add to your fraud prevention stack:

- CVV Verification: This is a non-negotiable partner to AVS. Checking the three- or four-digit Card Verification Value (CVV) helps confirm that the customer physically has the card, since this number is never supposed to be stored anywhere. A correct CVV paired with a matching AVS is a very strong signal of a legitimate purchase.

- IP Geolocation: This tool checks where in the world the order is actually being placed from by looking at the customer's IP address. If the billing address is in Ohio but the IP address is in a different country, that's a massive red flag that needs a closer look. It helps you spot those obvious geographical mismatches that scream "fraud."

- 3D Secure (3DS): For higher-risk transactions, 3D Secure adds a powerful layer of authentication. It bumps the customer over to their bank's website to enter a password or a one-time code sent to their phone. This step proves their identity directly with the bank, which is huge because it shifts the liability for fraudulent chargebacks away from you.

By combining these tools, you create a robust security net. A fraudster might have a stolen card number and a matching address, but they're far less likely to have the physical card for the CVV, be in the right location, and have access to the cardholder's banking app for 3D Secure.

The Growing Importance of a Layered Defense

The need for this kind of multi-faceted strategy is only getting more critical as e-commerce grows. The Address Verification Software market was valued at US$ 11.86 billion in 2024 and is expected to grow steadily, driven by the boom in online retail and tightening data protection rules.

As more businesses adopt these tools—especially in Europe where over 60% of companies now prioritize them for cross-border trade—fraudsters are forced to get more creative. This makes a simple, single-layered defense increasingly risky. You can learn more about these market trends and their impact on data privacy by exploring the full address verification software market report.

Ultimately, a complete strategy uses multiple tools that work together, giving you the confidence to approve good orders and the clarity to block bad ones. For more ideas on how to build out your defenses, check out our guide on e-commerce fraud prevention best practices.

Winning the Chargebacks That Still Get Through

Let's be realistic: even with the best fraud prevention tools in place, some chargebacks are still going to slip through the cracks. No system is completely foolproof. This is the moment your strategy needs to shift from pure prevention to active recovery.

While an Address Verification System is a fantastic first line of defense, blocking questionable transactions upfront, you need a different kind of tool to handle the disputes that make it past your initial defenses. This is exactly where a service like ChargePay picks up where AVS leaves off. It’s designed not just to block fraud, but to help you win the disputes you couldn't prevent, turning a potential loss into recovered revenue.

Shifting from Prevention to Recovery

Think of it this way: AVS is your proactive guard at the front gate, turning away suspicious characters before they can even get in. ChargePay is your expert legal team, ready to step in and defend your case when someone manages to sneak past and cause trouble. The two work together to create a complete revenue protection plan.

When a chargeback is filed against your store, fighting it manually is a slow, tedious, and often confusing process. You have to dig through order details, find shipping confirmations, and piece together every bit of evidence to prove the transaction was legitimate. This administrative burden pulls you away from what you should be doing—growing your business.

How Automation Builds a Stronger Case

This is where AI-driven automation changes the game. When a dispute hits your account, ChargePay automatically gets to work compiling all the critical evidence needed to build a winning case on your behalf.

This includes pulling key data points like:

- AVS and CVV Match Data: Showing the payment processor that you performed your due diligence at the time of the transaction.

- Order Information: Including the customer’s IP address and device details.

- Shipping Confirmations: Providing tracking numbers and delivery statuses.

- Customer Communications: Compiling any emails or support chats related to the order.

By automatically gathering this information in real-time, the system builds a comprehensive and compelling dispute response that is far more detailed than what most merchants have the time to create manually. It presents the facts clearly and professionally to the bank, significantly increasing your chances of winning.

This automated approach doesn't just save you countless hours; it recovers revenue you would have otherwise written off as a loss. It’s the safety net that ensures your business is protected from both the initial fraud attempt and the financial fallout of a dispute.

Even with robust address verification, disputes can arise from claims like "item not received." In these cases, understanding what constitutes valid proof of delivery can be a critical asset for winning chargebacks that still get through, providing the concrete evidence banks need to see.

For merchants tired of battling endless paperwork, automating the recovery process is a smart move. If you're looking for more strategies, you might be interested in our guide on how to win a credit card dispute for a deeper look at the process.

Common Questions About Address Verification

Even after you get the hang of how address verification systems work, a few questions tend to pop up in day-to-day operations. Let's tackle some of the most common ones I hear from merchants to clear up any confusion and help you put this tool to better use.

Does AVS Guarantee I Won't Get a Chargeback?

This is always the first question, and the short answer is no. While AVS is a fantastic tool for cutting down on fraud, no single system can promise a 100% guarantee against chargebacks. Think of it as a solid deadbolt on your front door—it’ll stop most opportunistic thieves, but a truly determined one might still find another way inside.

AVS is brilliant at catching fraudsters who've stolen credit card numbers but don't have the matching billing address. But it can’t do much about other kinds of disputes, like a customer claiming they never got their order or that the product wasn't what they expected. It dramatically lowers your risk, but it's just one piece of a much larger security puzzle.

Why Was My Valid International Order Declined?

This one is a common and incredibly frustrating scenario for anyone selling globally. You see an order from what looks like a perfectly legitimate international customer, but it gets declined. The culprit is almost always inconsistent support for AVS from banks outside a few key countries.

Address verification systems are most reliable in the United States, the UK, and Canada. Many banks in other parts of the world simply don't support the AVS protocol. So, when they receive an AVS check from your processor, they send back a generic code like "U" for Unavailable or "S" for Not Supported. If your fraud rules are too rigid, your system sees this as a red flag and automatically kills the transaction, creating a "false decline." This is exactly why it’s so important to have different, more lenient AVS rules for international orders—otherwise, you're just turning away good customers.

Can I Use AVS to Check Shipping Addresses?

This is a critical point that trips up a lot of merchants. The answer is a hard no. AVS is built for one job and one job only: to verify the billing address on file with the card issuer during the payment authorization process. Its whole purpose is to prevent fraud at the moment of transaction.

To make sure your packages actually get where they're supposed to go, you need a totally different tool: an address validation or address verification service (yes, the similar names are confusing!). These services check a shipping address against official postal databases, like the one from USPS, to fix typos, standardize the format, and confirm it's a real, deliverable location.

Key Takeaway: AVS secures the payment by checking the billing address. Address validation ensures accurate delivery by checking the shipping address. You really need both, but they perform two completely different jobs.

Even with a perfectly tuned AVS, some disputes are bound to slip through. When they do, ChargePay is there to handle the recovery process automatically. Our AI-driven system gathers all the crucial evidence, including AVS match data, to build and submit winning chargeback disputes for you, recovering revenue that would have otherwise been lost. Learn how ChargePay can become your automated safety net.

.svg)

.svg)

.svg)

.svg)