Receiving that American Express dispute notification can really throw you for a loop. It's easy to feel a jolt of anxiety, but it’s not a final judgment. Think of it as the start of a conversation between you, your customer, and Amex. Your biggest advantage is knowing the rules of that conversation.

The very first thing you need to do? Check your American Express dispute status. Staying on top of it is the key to resolving things quickly and efficiently.

What Your Amex Dispute Status Really Means

When an Amex dispute email lands in your inbox, it's natural to feel a bit of uncertainty. But that notification isn't a verdict—it's just a heads-up that a customer has questioned a transaction. Your best bet is to stay calm and organized, because these initial stages are usually just a request for more information.

Understanding the First Steps

The process often kicks off with an 'Inquiry' or a 'Retrieval Request.' This is not a formal chargeback. It’s simply Amex, on behalf of the cardholder, asking for more details about a charge. At this stage, no money has been taken from your account.

This is your chance to provide basic transaction info—like a receipt or order confirmation—to clear up any confusion before it gets more serious. If you want to dive deeper into the nuts and bolts of how these differ, check out our detailed guide on disputes and chargebacks.

A formal 'Chargeback,' however, is a different beast. Seeing this status means the funds have been temporarily pulled from your account and given back to the customer while the investigation is underway.

A proactive and organized approach is your best defense. Viewing each dispute not as a loss, but as a chance to present your side of the story, can dramatically shift the outcome in your favor.

To give you a clearer picture, here’s a quick rundown of the main stages you'll encounter.

Key Amex Dispute Stages at a Glance

Going through the American Express dispute process is much easier when you know what each stage means for you. This table breaks down the journey from the moment a cardholder raises a question to the final decision.

Understanding these phases helps you anticipate what’s next and prepare the right response at the right time.

Why Your Response Matters

How quickly you respond and the quality of your evidence are everything. Ignoring an inquiry will almost always lead to it becoming a chargeback, making it much tougher to win.

By regularly checking your American Express dispute status in your merchant portal or payment processor's dashboard, you can stay ahead of deadlines and on top of the process.

With this foundation, you can shift from feeling reactive and uncertain to being in a confident position of control. When you know what each status means, you can take the right actions, protect your revenue, and keep your merchant account in good standing.

How to Check Your Dispute Status Step by Step

Getting a dispute notification is just the first domino to fall. The real work—and where you can start to take back control—is in actively tracking its progress. Thankfully, checking your American Express dispute status is pretty straightforward once you know where to look.

You'll have one of two primary places to check, and your business setup will determine which one is your main source of truth.

Your Direct American Express Merchant Account

If you have a direct merchant account with American Express, their online portal is your mission control. This dashboard is built to give you a complete picture of everything happening with your transactions, and that absolutely includes disputes.

Here’s the simple process:

- Log In: Head over to your American Express merchant account online.

- Navigate to Disputes: Look for a tab or section labeled "Disputes," "Chargebacks," or sometimes "Cases." The exact name might differ slightly, but it’s almost always easy to spot on your main dashboard.

- Find the Specific Case: You can usually search for the dispute using the case number, transaction details, or cardholder info.

- Review the Status: Once you click into the case, you’ll see its current status—like "Information Requested" or "In Progress"—along with any critical deadlines for submitting your evidence.

Checking Through Your Payment Processor

For a lot of businesses, especially in e-commerce, you won't be dealing with Amex directly. Instead, you'll manage disputes right where you manage your payments: through your processor. Platforms like Shopify, Stripe, or PayPal serve as the middleman, so their dashboards are where you’ll find all the details.

The process is very similar across platforms:

- For Shopify Merchants: Log into your admin panel, go to Orders, and use the Chargebacks and inquiries filter. This will pull up all your active cases.

- For Stripe Users: Inside your Stripe Dashboard, click on the Payments section and then select Disputes. Every case will be listed there with its current status and what you need to do next.

- For PayPal Sellers: Log in and make your way to the Resolution Center. This is PayPal's dedicated hub for all claims and chargebacks that need your attention.

No matter which platform you use, the goal is the same: find that dispute and get a clear read on where it stands. It can also be helpful to see the process from the other side; our guide on how to dispute a charge with American Express from a customer's view provides some great context.

Staying on top of these statuses is absolutely critical. While Amex chargebacks happen a bit less frequently (0.65%) than with Visa or Mastercard, they often involve higher stakes. The average Amex dispute is around $200, and with merchant win rates sitting at a tough 28%, every single response you make has to count. You can get more insights on how Amex chargebacks affect merchants over at clearlypayments.com.

Decoding Common Amex Dispute Status Codes

When you log in to check your American Express dispute status, you're going to see a few key phrases pop up again and again. These aren't just random labels; they're signals telling you exactly what’s happening with your case and, more importantly, what you need to do next.

Think of them as a simple decoder ring for the dispute process. Getting a handle on these codes is the difference between feeling in control and feeling completely lost.

Let's break down the most common ones you'll run into.

Common Amex Dispute Status Codes and What They Mean

As you go through the dispute portal, you'll find that Amex uses specific language to communicate the stage of the investigation. While it might seem a bit formal, each status is a clear directive. Here’s a quick rundown of the codes you'll see most often, what they actually mean, and what your immediate next move should be.

Understanding these statuses turns a confusing process into a series of clear, manageable steps. It allows you to respond at the right time with the right information, which is critical for protecting your revenue.

Your Call to Action: Information Requested

When you see an "Information Requested" status, this is your moment. It means Amex is asking for your side of the story, and this is your single best opportunity to submit compelling evidence to prove the charge is legitimate.

Ignoring this is the biggest mistake you can make. This isn't a suggestion; it's a direct request. Failing to respond pretty much guarantees you'll lose the dispute by default.

The Waiting Game: In Progress or Under Review

Once you’ve sent in your evidence, the status will usually flip to "In Progress" or "Under Review." This is the waiting phase. It simply means American Express has your documentation, and their team is doing the legwork of investigating the claim.

You don't need to do anything here. Just hang tight and keep an eye on the portal for any changes. It's rare, but they might ask for more information at this stage.

The status codes are more than just updates; they are strategic prompts. 'Information Requested' is your cue to build your case, while 'In Progress' is a signal to wait patiently as the process unfolds.

The timeline for the review can vary quite a bit, which is why having a good grasp of the different American Express chargeback time limits can help you set realistic expectations.

The Final Verdict: Resolved or Closed

This is it—the end of the road. A "Resolved" or "Closed" status means a final decision has been made. But you'll need to read the fine print to see how it ended.

It will always come with a final clarification:

- Resolved – In Your Favor (or similar wording): Fantastic news, you won! Your evidence was convincing, the chargeback was reversed, and the funds are heading back to your account.

- Resolved – For Cardholder (or similar wording): This is the outcome no one wants. It means you lost the dispute, your evidence wasn't strong enough, and the funds will stay with the customer.

Knowing what each American Express dispute status means helps you stay one step ahead. You can transform a confusing, reactive process into a series of clear, proactive steps, giving you the best shot at protecting your hard-earned revenue.

How to Build a Winning Dispute Response

Knowing your American Express dispute status is just the start—winning the dispute is what actually protects your bottom line. This all comes down to your representment, which is the evidence you submit to prove the charge was legitimate. The trick to crafting a compelling response isn't about arguing; it's about presenting clear, undeniable facts that make it easy for an Amex reviewer to see things your way.

Think of it like you're building a case for a judge. You need to organize your evidence logically and tell a simple, truthful story about what happened during the transaction. Your goal is to leave absolutely no room for doubt.

Gathering Your Core Evidence

Every dispute is a little different, but the kind of evidence American Express looks for is pretty consistent. The real key is to make sure your evidence directly addresses the customer's specific claim. Start by pulling together every document related to that order.

Here’s your essential evidence checklist:

- Order and Payment Confirmation: Grab screenshots or records from your system that show the order was placed and the payment went through successfully.

- Proof of Delivery: For any "product not received" claim, this is non-negotiable. A shipping confirmation with a tracking number showing the item was delivered to the correct address is your single strongest piece of evidence.

- Customer Communication: Any emails, chat logs, or support tickets between you and the customer can provide critical context. This is especially powerful if it shows a happy customer or proves you tried to resolve their issue.

- Product or Service Descriptions: If the dispute is for "not as described," include screenshots of the product page the customer ordered from. This proves that what you delivered was exactly what they saw.

Presenting this information clearly is half the battle. For merchants, mastering the art of a strong dispute response is a critical skill. It’s a similar mindset needed to craft a winning Plan of Action, as detailed in this practical, step-by-step reinstatement guide for Amazon accounts.

Structuring Your Response for Impact

Once you have your documents, the next step is to package them persuasively. Don't just dump a folder of random files on the reviewer. Instead, write a clear, concise rebuttal letter that walks them through your evidence, piece by piece. If you need a good starting point, this example of a rebuttal letter can help guide you.

A winning response is built on clarity, not volume. Focus on providing irrefutable proof that directly counters the cardholder's claim, making the reviewer's decision as simple as possible.

Winning these disputes is about more than just getting back the money from one sale. It directly impacts your bottom line by helping you avoid some pretty costly fees. For instance, American Express has an Excessive Chargeback Fee policy that hits merchants whose chargeback ratio goes over 1% for three months in a row.

If your ratio stays above that mark, you'll get slapped with a $25 fee for every single chargeback over that threshold. With merchant win rates for Amex disputes hovering at a challenging 28%, every piece of evidence counts. Being meticulous and organized gives you the best possible shot at keeping both your revenue and your good standing.

You’ve done the hard work. You’ve gathered your documents, built a rock-solid case, and finally hit “submit” on your dispute response. So, what’s next? This is the part where the ball leaves your court and lands squarely with the American Express review team. Knowing what happens now is crucial for managing both your expectations and your cash flow.

Once your evidence is in their hands, the American Express dispute status will usually switch to something like "In Progress" or "Under Review." This kicks off the waiting game. An Amex specialist will now meticulously comb through all the information—from both you and the cardholder—to make a final call.

The Amex Review Period

This review process isn't instant. Amex-specific disputes can take around 45 days on average to resolve, which can feel like an eternity when your revenue is tied up. During this time, it’s a good idea to keep an eye on your merchant portal for any updates, but you generally don’t need to do anything else unless Amex reaches out for more information.

Getting a handle on these timelines is more important than ever. With global chargeback volumes expected to rocket to 337 million by 2026, the heat is on for merchants everywhere. It's a massive financial drain, and you can get a clearer picture of the impact by checking out this detailed breakdown of chargeback statistics.

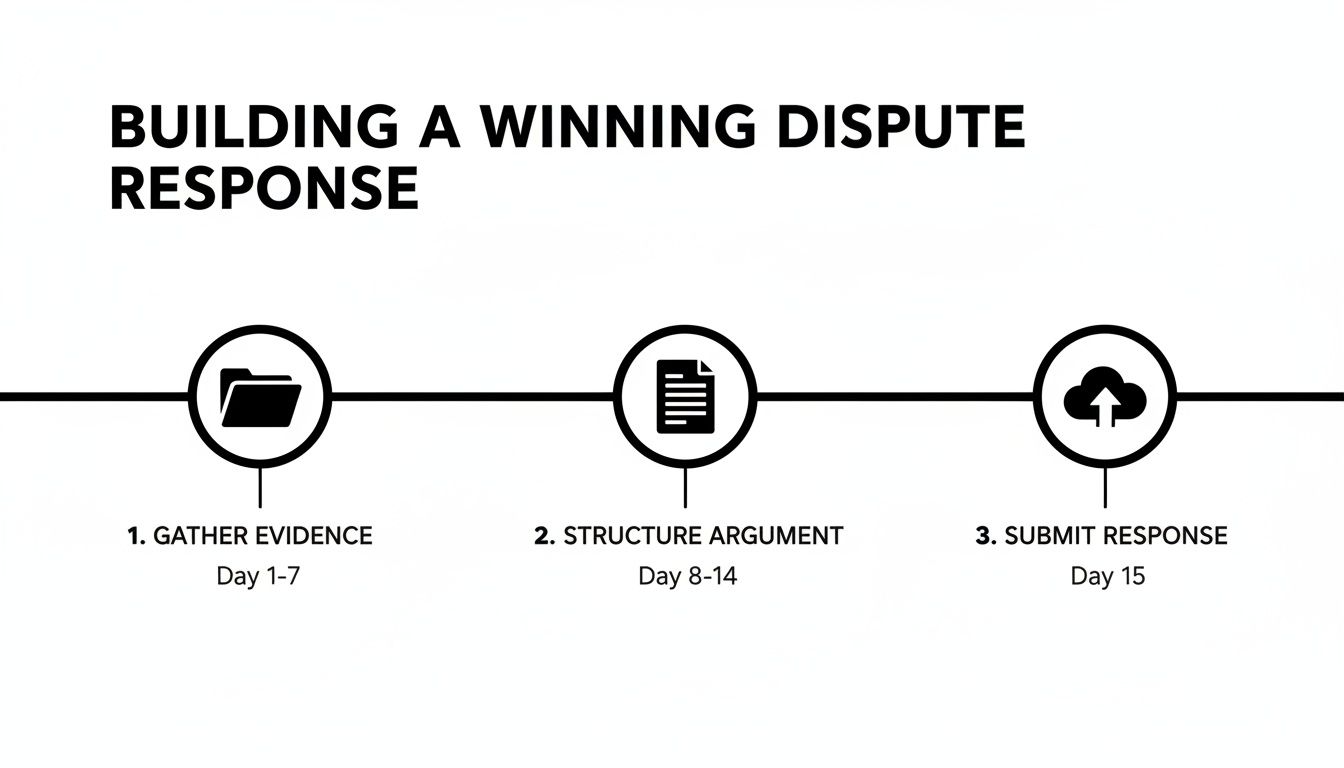

Here’s a simple, effective workflow for pulling your evidence together before you hit submit.

Stick to a structured approach—gather, structure, and submit. It ensures your response is clear, compelling, and easy for the Amex reviewer to digest.

The Final Decision and What It Means

After the review is complete, the dispute status will update one last time to show the final outcome. It will fall into one of two buckets:

- Resolved in Your Favor: This is what you’re hoping for. It means your evidence was strong enough to convince Amex to reverse the chargeback. The funds that were temporarily pulled from your account will be returned.

- Resolved for Cardholder: This means you lost the dispute. Your evidence wasn't enough to overturn the cardholder's claim, and the funds will stay with them for good.

The final resolution is a critical learning moment. A win confirms your processes are solid, while a loss offers a chance to identify gaps in your evidence collection for next time.

In some rare cases, a cardholder might try to open a second chargeback on the same transaction, a process known as arbitration. This escalates the whole thing and comes with extra fees. But if you won the first round with solid evidence, it's pretty unlikely to happen. By understanding these potential outcomes, you'll be better prepared for whatever the final American Express dispute status reveals.

How to Automate Your Dispute Management

Let's be real. Manually checking every single American Express dispute status, digging up evidence, and writing custom responses is a huge time sink. It’s the kind of work that pulls you away from what you should be doing—growing your business. But what if you could put that entire process on autopilot?

This is where an automated solution comes in, offering a much smarter and more efficient way to handle disputes. Instead of constantly reacting to notifications and scrambling for documents, you can have a system that proactively manages everything for you from start to finish.

Let AI Handle the Heavy Lifting

This is exactly where a tool like ChargePay shines. It uses artificial intelligence to completely take over your dispute management workflow. The second a dispute lands in your account, the system kicks into gear, automatically generating a compelling, evidence-backed response in real time.

This approach accomplishes two huge things:

- It saves you countless hours of mind-numbing administrative work.

- It can significantly improve your win rate by leveraging data-driven arguments that are tailored to win.

Automation transforms dispute management from a reactive, time-consuming chore into a proactive, revenue-recovering asset. It lets you fight every dispute without lifting a finger, protecting your bottom line while you focus on your customers.

For businesses running on platforms like Shopify or Stripe, the integration is completely seamless. The system just works quietly in the background, fighting to recover revenue you might have otherwise written off as a loss. You can find more details in our complete guide to automated chargeback and dispute management using AI.

From Manual Effort to Automatic Wins

Imagine this: no more logging into different portals just to check a status. No more digging through old emails for proof of delivery. An automated system does all of that for you, pulling the necessary data—like order details, shipping confirmations, and customer history—to build the strongest possible case on your behalf.

This frees you and your team up to focus on the bigger picture, like marketing campaigns and new product development. By letting technology handle these repetitive tasks, you turn a frustrating cost center into an efficient, automated part of your operations. It’s all about working smarter, not harder, to protect your hard-earned revenue.

Got Questions? We’ve Got Answers.

When you're dealing with disputes, a lot of questions can pop up. Getting straight answers is the best way to feel confident you're handling things correctly. Here are some of the most common things merchants ask us about the American Express dispute status and what it all means.

How Long Does an American Express Dispute Take to Resolve?

This is the big one, right? The timeline for an Amex dispute can be a bit of a moving target, but you can generally expect the whole process to take around 45 to 90 days from start to finish.

The most critical part for you, the merchant, is that initial response window. It's short—often just 20 days. Once you've submitted your evidence, Amex takes over to review the case, and that can take several weeks. If things get complicated or head toward arbitration, the clock keeps ticking. The key takeaway? Act fast and keep a close eye on the status in your merchant portal so you don’t miss any deadlines.

Can a Customer Reopen a Closed Amex Dispute?

Generally, when a dispute is closed in your favor, that's the end of it. It’s considered final. However, there’s a small catch: a cardholder can escalate the issue to pre-arbitration if they come back with new, compelling evidence that wasn't part of the initial case.

While it doesn't happen often, the fact that it can happen is exactly why you need to put your best foot forward the first time. A rock-solid, comprehensive evidence bundle during your initial representment is your best defense against the dispute coming back to haunt you.

On the flip side, if you lose the initial chargeback, you usually have the option to escalate to arbitration yourself. Just remember that this path comes with extra fees and more complexity, so you’ll need to do a quick cost-benefit analysis to see if it’s worth it.

What Is the Difference Between an Inquiry and a Chargeback?

Understanding this distinction can save you a world of hurt. An 'inquiry' (sometimes called a retrieval request) is just a preliminary check-in. Amex is simply asking for a bit more information about a transaction on behalf of the cardholder.

At the inquiry stage, no money is pulled from your account. It's your golden opportunity to clear up a customer's confusion with simple proof of purchase, like a receipt or shipping confirmation. A 'chargeback,' on the other hand, is the real deal. It’s a formal dispute, and the funds are immediately taken from your account. You then have to fight to get that money back by proving the charge was legitimate. Responding to inquiries quickly and thoroughly is the best way to stop them from turning into damaging chargebacks in the first place.

Stop wasting time and losing revenue to manual dispute management. ChargePay uses AI to automate the entire process, recovering up to 80% of your lost funds without you lifting a finger. See how it works at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)