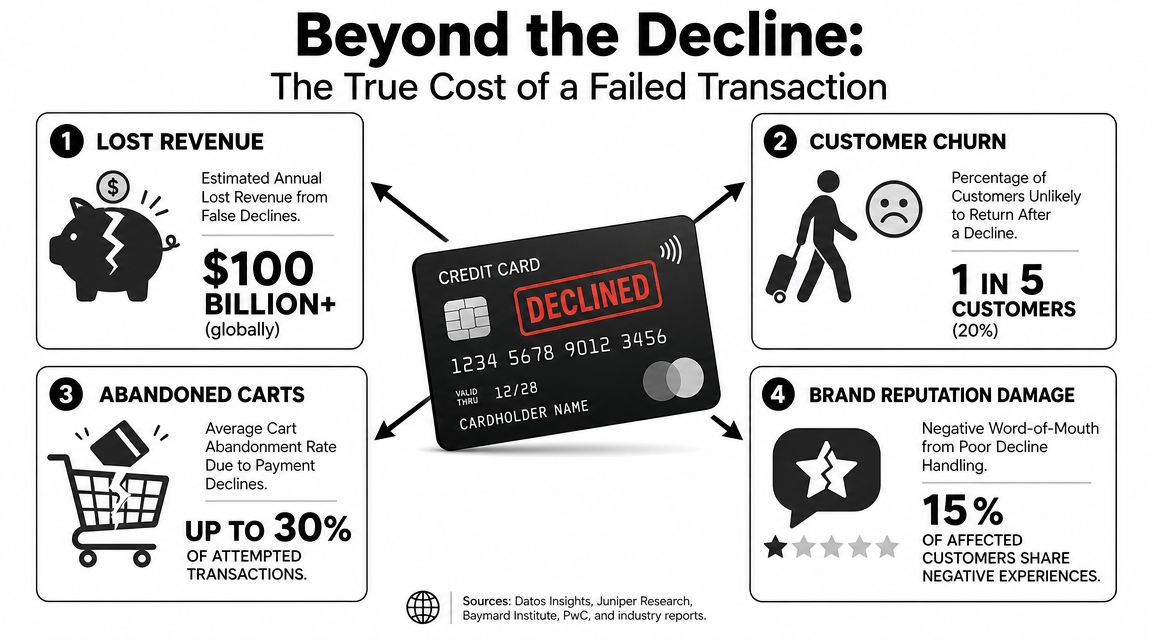

Issuer declines cost more than one order. They trigger a chain most Shopify merchants know too well: the customer hits an error, leaves checkout, emails support, retries in frustration, and comes back later as a dispute risk.

That is why treating a decline like a simple payment failure is a mistake. It sits at the intersection of conversion, fraud screening, customer experience, and chargeback prevention. If your team only looks at whether the payment went through, you miss the bigger loss.

A shopper does not care whether the problem came from the bank, your gateway, or an overly strict risk setting. They care that your checkout failed. Once that trust breaks, recovery gets expensive.

You need to read declines as an early warning signal. Some point to bank-side issues. Others expose checkout friction, weak retry logic, or settings that block legitimate buyers. If you need a quick refresher on who handles what in the payment flow, this breakdown of issuer vs acquirer responsibilities is a useful place to start.

Handle declines well and you save revenue before it turns into support load and disputes. Handle them poorly and one failed payment becomes the first domino in a much more expensive chain.

Why Card Issuer Declined Is More Than Just a Failed Order

A card issuer decline is rarely a one-order problem. For a Shopify store, it often starts a chain reaction: the customer loses confidence, support tickets go up, retries get messy, and a preventable checkout failure turns into churn or a dispute later.

When shoppers see card issuer declined, they do not separate bank logic from gateway rules or your fraud settings. They blame the checkout. That is the part you control, and that is why this issue deserves operator attention, not just a payment-status label.

The decline is the first warning sign

An issuer decline happens after the customer has already made it through product selection, cart, and checkout. You already paid to bring that shopper in. If the payment fails at the last step, the wasted ad spend is only the first hit.

The bigger problem is what the decline reveals. Sometimes the bank is blocking the charge for reasons on the cardholder side. Sometimes your setup is making recovery harder than it should. If you want a clearer view of who owns which part of the payment flow, this guide to issuer and acquirer responsibilities in card payments is a useful reference.

Here is the practical takeaway. A decline is not just a payment event. It is an operational signal that something in your revenue flow needs attention.

The cost shows up in more places than revenue

Store owners usually count the lost order and move on. That is too narrow.

A declined payment can push a ready-to-buy customer out of the session. It can trigger a support conversation your team cannot resolve because the bank made the final call. It can also train the customer to mistrust future billing attempts, especially if you run subscriptions, preorders, or post-purchase upsells.

That mistrust is expensive.

If a shopper retries multiple times and still gets blocked, frustration rises fast. Some abandon. Some contact support. Some forget the original failure, then dispute a later successful charge because the experience already felt off. The decline was the first domino.

Why this matters for Shopify operators

Too many brands treat issuer declines as background payment noise. That is a mistake. If your decline handling is weak, you are spending acquisition dollars to create failed checkouts, extra support work, and future chargeback risk.

Treat declines like part of revenue protection. Review patterns by card type, issuer response, product line, and traffic source. Tighten customer messaging. Fix avoidable checkout friction. Stop retrying blindly.

The goal is simple. Recover the good orders, avoid making bad retries worse, and keep one failed authorization from turning into a lost customer and a dispute later.

Soft Declines vs Hard Declines What Your Gateway Is Saying

Your gateway is giving you a diagnosis, not just a red light. Read it correctly and you recover more orders. Read it poorly and you turn one failed authorization into repeat checkout failures, annoyed customers, and avoidable dispute risk later.

A soft decline means the transaction might still go through after the customer or issuer fixes something. A hard decline means the card should not be retried in its current state. That distinction should control your next move.

The expensive mistake is treating every decline the same.

The split that matters

Some issuer responses point to a temporary block. The customer may need to confirm a purchase, free up available credit, retry with corrected details, or complete an authentication step. Those are soft declines.

Others are dead ends. Expired card. Invalid account number. Lost or stolen card. Closed account. Those are hard declines, and retrying them is sloppy operations.

Stripe explains this well in its decline code reference. One takeaway stands out: a large share of declines come from insufficient funds, not fraud. That matters because a good customer with a timing or balance issue should get a recovery path, not the same treatment as a stolen card response.

Common decline codes and merchant actions

| Decline Code | Meaning | Type | Recommended Action |

|---|---|---|---|

| 05 Do Not Honor | Issuer refused the transaction without a clear reason | Soft or unclear | Ask the customer to contact their bank or use another payment method. Do not keep retrying the same authorization. |

| 51 Insufficient Funds | Customer does not have enough available funds or credit | Soft | Let the customer choose when to retry. Offer another card or wallet right away. |

| 54 Expired Card | Card on file is no longer valid | Hard | Request updated card details. Do not retry the same card. |

| 14 Invalid Card Number | Card details are incorrect or no longer usable | Hard | Ask the customer to re-enter payment details or use a different card. |

| Lost or Stolen Card response | Issuer blocked the card for security | Hard | Stop immediately. Ask for another payment method. |

| Authentication required | Extra verification is needed | Soft | Send the customer through the proper authentication flow, then retry once through that flow. |

What Shopify merchants usually get wrong

First, they let subscription tools or billing apps retry declines with no real logic. That trains issuers to distrust your traffic and creates a bad customer experience fast.

Second, they hide behind useless messaging. “Payment failed” does nothing. Tell the shopper what to do next: contact the bank, check card details, use another payment method, or complete identity verification.

Third, they miss the chargeback angle. A customer who gets blocked three times and then finally sees a later charge is more likely to contact support angry, or dispute the charge because the payment history already feels messy. The decline was the first domino.

If you see issuer responses tied to extra verification, clean up your authentication flow and review how 3D Secure authentication works. It will not rescue hard declines, but it does help recover the orders that only need issuer confidence to approve.

Your Immediate Troubleshooting Playbook for Declined Cards

Every issuer decline can trigger three costs at once. You lose the order, you frustrate the customer, and you increase the odds that a messy retry or delayed charge turns into a dispute later. Treat the first failed authorization like a risk event, not a checkout glitch.

The right response in the first hour is simple. Check your own setup, contact the customer with a clear next step, and retry only when the reason supports it. That is how you recover revenue without creating chargeback bait.

Check your Shopify and payment settings first

Start with your side of the stack before you blame the issuer.

Look at Shopify checkout settings, gateway rules, fraud apps, and any custom logic that can block a good order before the bank ever gets a fair shot at approving it. Stores with tight filters often create their own decline problem, especially on mobile, high-value orders, gift shipments, and international traffic.

Use this checklist:

- Review AVS mismatch handling. If you auto-reject every mismatch, you will block legitimate customers. Revisit your settings with this guide to AVS address verification.

- Check CVV rules. Requiring CVV is fine. Rejecting every exception with no fallback costs sales.

- Audit fraud apps and manual rules. If two or three tools are screening the same order, you can end up declining good customers twice.

- Compare declines by device. Mobile checkouts produce more typos and less patience.

- Review billing descriptor clarity. If the customer does not recognize your charge later, today's decline problem can become tomorrow's chargeback.

One more point. If your team cannot quickly see which declines came from issuer logic versus your own filters, fix reporting first. You cannot reduce declines if you keep mixing bank rejections with merchant-side blocks.

Send better customer messages

Decline recovery usually fails because the message is lazy.

A generic “payment failed” message forces the customer to guess. Good customers abandon. Frustrated customers try the same card five times. Some come back later angry because they see a pending charge and assume you billed them incorrectly. That is how a decline starts the chain reaction.

Tell the shopper exactly what to do next. Keep it short. Give options.

Customer email for a likely soft decline

Subject: Your order is almost completeHi [First Name],

Your bank did not approve the payment for your order. This usually means the card needs verification or one detail needs to be checked.Please try again with the same card after reviewing the details, use a different card, or choose a digital wallet. If it still fails, contact your bank and ask them to approve the purchase.

We saved your cart here: [cart link]

Customer email for a likely hard decline

Subject: Please update your payment methodHi [First Name],

We could not complete your order because the card was declined by the issuing bank. The fastest fix is to place the order again with a different card or update your payment details.If you want help, reply to this email and our team will assist.

Clear beats clever.

Retry only with a reason

Retries need rules. Random retries waste auth attempts, train issuers to distrust your traffic, and create confusion when a customer sees multiple attempts or a delayed capture.

Use a simple operating standard:

- Retry soft declines only after something changed. The customer corrected details, completed verification, switched cards, or called the bank.

- Do not retry hard declines on autopilot.

- Log the issuer response code so you can find patterns by card type, device, country, or product line.

- Keep proof of customer authorization for any later retry in a saved-card or recurring flow.

This protects revenue and reduces downstream risk. A customer who sees repeated failed attempts and then a later successful charge is more likely to contact support upset, request a refund, or file a dispute because the payment history already looks sloppy.

What to do in the first 60 minutes

Use this order of operations:

- First 10 minutes: Check the decline code, payment method, device type, and whether any fraud rule or checkout setting blocked the transaction.

- Next: Classify it as soft, hard, or unclear.

- Then: Contact the customer with one clear action. Re-enter details, complete verification, call the bank, or use another payment method.

- After that: Retry once if the customer took action or the decline reason supports another attempt.

- Finally: Tag the order in Shopify and note what happened so your team can track whether the failed payment later turned into a support issue, refund request, or chargeback.

The goal is not to push every payment through. The goal is to stop the chain reaction early, recover the orders you should recover, and avoid creating a bigger loss later.

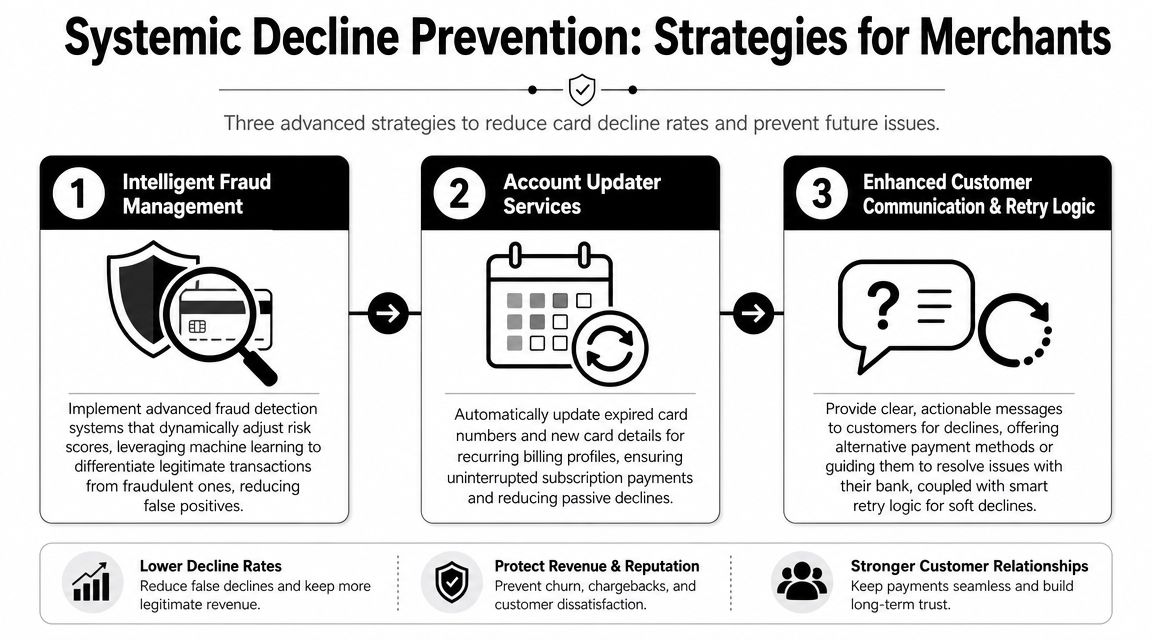

Advanced Strategies to Reduce Future Decline Rates

Fixing declines one by one is a grind. You need system changes.

A strong decline-reduction program usually combines smart routing, tokenization, and intelligent retries, according to Rapyd's guidance on improving card acceptance. The same source notes that mobile authorization rates are often 3 to 5% lower than desktop, which is a strong reason to segment analysis by device instead of looking at one blended approval rate.

Build for saved cards and recurring payments

If you run subscriptions or repeat purchases, stale card data is one of the easiest ways to lose revenue imperceptibly.

Use account updater services or network tokenization so expired, replaced, or canceled cards stay current in your billing system. That won't solve every issuer decline, but it removes a common avoidable failure in saved-card commerce.

Stop treating all traffic the same

Desktop and mobile don't behave the same. Neither do first-time buyers and repeat buyers.

A better operating model looks like this:

- Segment mobile separately. Mobile checkout friction hits harder because small input mistakes and bank prompts are more disruptive.

- Tune fraud rules by customer context. A repeat customer with a stable order pattern shouldn't hit the same threshold as a first-time risky order.

- Route intelligently when your setup allows it. If you use multiple processors or acquirers, routing logic can improve authorization outcomes.

If you want the architecture behind that approach, this overview of a payments orchestration platform is worth reading.

Tighten retries without going blind

Smart retries work. Random retries don't.

You want retry logic tied to decline type, customer behavior, and updated credentials. If your billing system keeps retrying every failure the same way, you're not optimizing. You're just repeating mistakes faster.

Better approval rates usually come from a stack of small fixes. Cleaner routing, better tokens, softer fraud rules in the right places, and customer-aware retry logic.

That's the part many merchants miss. There usually isn't one magic switch. There is a payment operation that gets sharper over time.

Connecting Declined Cards and Chargeback Prevention

A badly handled decline can become a dispute later.

That sounds backward at first. If the payment failed, how does it turn into a chargeback? Easy. The customer tries again, uses another card, gets confused by duplicate attempts, forgets the merchant name on the statement, or loses trust because the checkout felt sketchy from the start.

Decline friction creates dispute conditions

The common thread is confusion. Customers don't always separate a bank decline from a merchant problem. They remember frustration, not payment plumbing.

That's why decline handling belongs inside your chargeback prevention process. Clear checkout messaging, clean retry discipline, recognizable billing descriptors, and better fraud controls all reduce the kind of confusion that later turns into friendly fraud.

If you want a broader operational checklist on risk controls, ECORN's guide to ecommerce fraud is a useful companion read.

Aggressive retries can make things worse

This is the trap. A card gets hard declined, your systems keep pushing, and now you've got a noisy payment trail. That can trigger customer complaints, support friction, and in some cases disputes tied to authorization behavior or duplicate confusion.

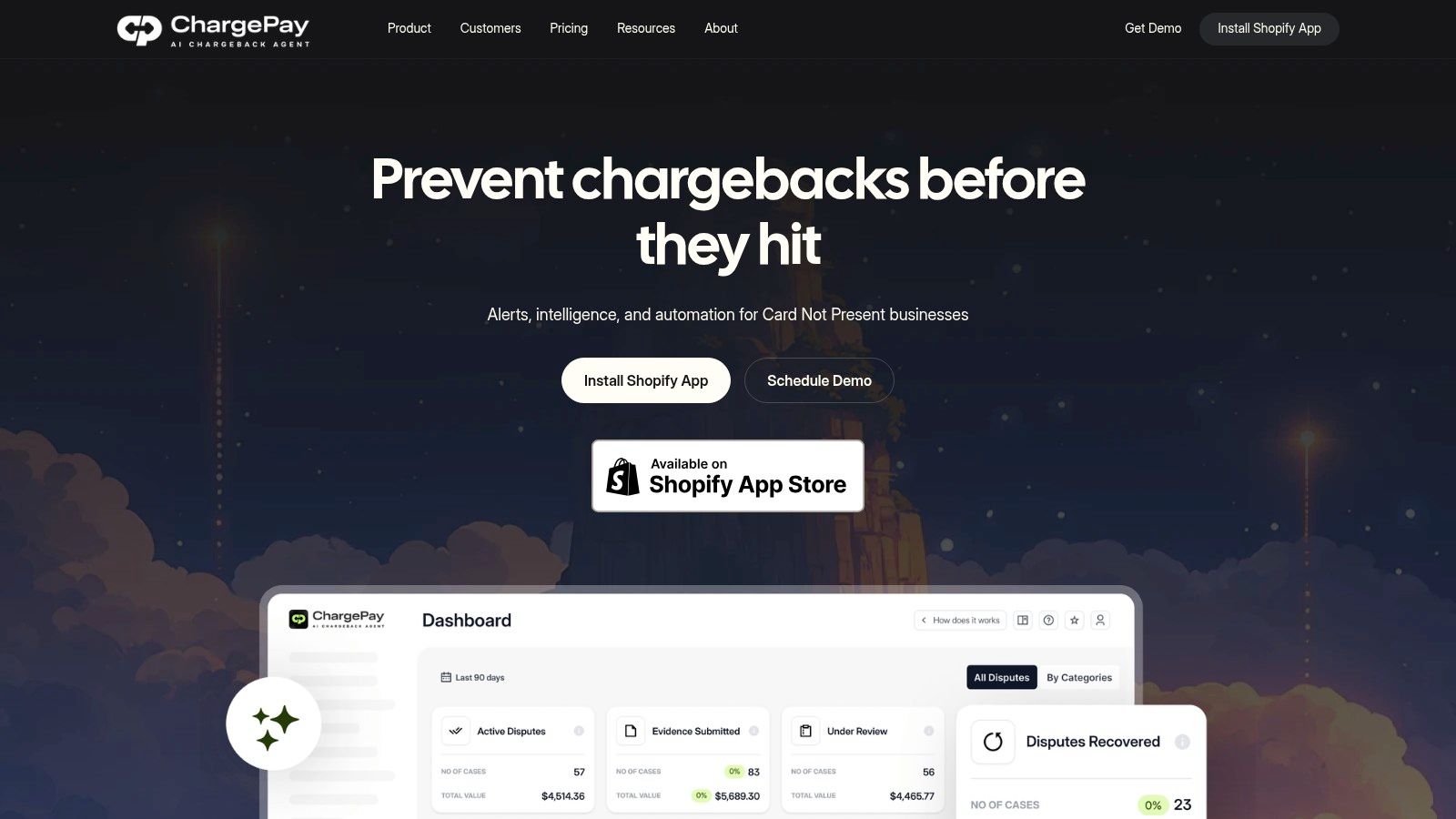

When disputes do happen, merchants need a separate layer for recovery. ChargePay is one example. It's an AI-powered Shopify app that manages chargebacks, generates representment responses, and submits evidence before deadlines. The company states a 92.4% win rate, 200K+ cases handled, and $10.8M+ recovered across merchants.

A quick product walkthrough helps if you want to see how automated dispute handling fits into the stack:

The point isn't that every decline becomes a chargeback. It's that the same sloppy processes that hurt approvals also raise dispute exposure later. Clean up declines, and you usually clean up downstream headaches too.

Stop Losing Money to Declines and Disputes

If your store keeps showing card issuer declined, don't shrug it off as normal ecommerce noise. It's costing you sales right now, and it may be setting up support issues and disputes later.

The fix is practical. Classify declines correctly. Stop retrying hard declines. Tighten customer messaging. Review fraud and AVS settings. Improve saved-card infrastructure. Segment mobile performance instead of blending it into one approval rate.

That's the operator mindset. Treat payment recovery like revenue recovery.

You also need a backstop for the disputes that still slip through. Even with cleaner checkout flows and smarter retry logic, some customers will file chargebacks. When that happens, speed and evidence matter. A manual process usually means missed deadlines, weak responses, and preventable losses.

ChargePay's positioning is straightforward: it's built for Shopify, has a 4.9-star rating, carries the Built for Shopify badge, and uses a pay-per-win model. That structure makes sense for merchants who don't want another fixed-cost app sitting on the stack while revenue leaks out.

The bigger lesson is simple. Declines and disputes aren't separate problems. They're connected failures inside the same customer journey. Fix both, and your checkout gets healthier.

Install ChargePay if you want a Shopify-focused way to stop losing money after failed payments turn into disputes. It helps merchants automate chargeback responses, recover revenue, and avoid wasting hours on manual representment.

.svg)

.svg)

.svg)

.svg)