A chargeback for fraud is the financial equivalent of a rug being pulled out from under you. It’s a forced payment reversal kicked off by a customer’s bank because the cardholder claims they never authorized the purchase. Essentially, a sale you thought was complete gets undone, and the money is yanked right back out of your business account.

What a Fraud Chargeback Really Means for Your Business

Picture this: you get an email notification about a "chargeback for fraud" on a recent sale. It’s a gut-punch for any merchant. Your first thought is probably that some criminal with a stolen credit card hit your store. And while that’s definitely a possibility, the story is often a bit more complicated.

This alert means a customer has contacted their bank and flat-out denied making a purchase from you. The bank, whose main job is to protect its cardholder, immediately reverses the payment. The funds are gone from your account while they sort things out. Now you're out the product and the payment for it.

The Two Faces of Fraud Chargebacks

Not all fraud claims are the same, and knowing the difference is your first line of defense. You'll generally run into two main types:

- True Criminal Fraud: This is the classic scenario. A thief gets their hands on stolen credit card information and uses it to buy something from your store. In this case, the real cardholder is a victim, and the chargeback is doing exactly what it was designed to do.

- Friendly Fraud: This one is much murkier. It happens when a legitimate customer buys something but later disputes the charge, claiming it was fraudulent. Sometimes it's an honest mistake—they forgot about the purchase or don't recognize your business name on their statement. Other times, it's done intentionally to get a free product.

No matter the reason, the immediate hit to your business is identical. The money vanishes, and you're thrown into a dispute process that drains your time and energy. You can get ahead of this by learning more about the different kinds of chargeback fraud and what causes them.

A chargeback for fraud isn't just about a single lost sale. It triggers a cascade of hidden costs, including non-refundable processing fees, steep chargeback penalties from your payment processor, and the valuable time you spend gathering evidence to fight the claim.

These disputes do more than just sting your bank account. A high chargeback rate can seriously damage your standing with payment processors. This can lead to higher processing fees or, in a worst-case scenario, losing your merchant account entirely. It's a real headache that pulls you away from what you should be doing: growing your business.

The Real Reasons You Are Getting Fraud Chargebacks

When you see a chargeback for fraud, it's natural to picture a shadowy criminal somewhere making off with stolen goods. And sometimes, that's exactly what's happening. But more often than not, the story behind a fraud chargeback is a lot more complicated.

Think of yourself as a detective. Every chargeback has a backstory, and it’s your job to figure out what really went down. Digging into the "why" is the only way to build a real defense and, more importantly, stop these disputes from happening again.

Most of the time, these cases fall into one of three main categories.

The Clear-Cut Case of Criminal Fraud

This is the one that fits the classic definition of fraud. A thief gets their hands on someone's credit card details—maybe from a data breach, a phishing email, or just plain old theft—and uses that info to buy something from your store.

Later on, the real cardholder checks their statement, sees a charge they definitely didn't make, and immediately calls their bank. The bank sees a legitimate victim of theft and, in almost every case, will side with their customer. It's frustrating for you, but it’s the system working as intended to protect consumers. These chargebacks are the toughest to win because the transaction was genuinely unauthorized.

The Murky World of Friendly Fraud

Here’s where things get messy. Friendly fraud is when a real customer makes a purchase but disputes the charge later on. It’s not always malicious—sometimes, it’s just a simple mistake. A customer might not recognize your store's name on their statement, or maybe they just forgot about the purchase entirely.

A classic example is a teenager using their parent’s card for an online game. The parent sees an unfamiliar charge, assumes the worst, and reports it as fraud without realizing who made the purchase. This is accidental friendly fraud.

But there’s a darker side to this. A lot of consumers are now filing fraud chargebacks on purpose just to get their money back while keeping the product. This tactic, often called "chargeback abuse" or "cyber-shoplifting," has exploded into a massive problem for online sellers.

The surprising truth is that "friendly fraud" is no longer a minor issue. It now accounts for a staggering 45% to 75% of all merchant disputes globally, making it a dominant threat.

This isn't happening in a vacuum. Social media is full of so-called "refund hacks" that teach people how to game the system. In fact, a shocking 34% of consumers who've committed this kind of fraud learned how to do it on TikTok. All this has added up to a massive $15 billion in fraudulent chargeback losses for businesses like yours. You can explore more about these chargeback statistics and how they impact merchants to see the full picture.

To help you spot what you're up against, here's a quick breakdown of the most common reasons these disputes pop up.

Table: Common Causes of Fraud Chargebacks

As you can see, the reasons are all over the map. Getting a handle on which type you're dealing with is the first step toward a solution.

Simple Merchant Errors That Cause Disputes

Finally, we have the chargebacks you have the most direct control over. Sometimes, a dispute gets labeled as fraud, but it was actually triggered by a simple mistake in your own process.

Here are a few common slip-ups that can lead to a fraud chargeback:

- Confusing Billing Descriptors: If the name on your customer's credit card statement doesn't clearly match your store name, they might hit the panic button and report it as fraud.

- Poor Communication: When you don't send order confirmations or shipping updates, customers can get nervous. A nervous customer is much more likely to cancel the payment through their bank.

- Unexpected or Delayed Shipping: If an order takes way longer to arrive than you promised, a customer might assume they've been scammed and file a chargeback to get their money back.

By looking closely at the reason behind each dispute, you can start to connect the dots. Pinpointing whether you're dealing with a thief, a confused customer, or a flaw in your own system is the key to lowering your chargeback rate and protecting your bottom line.

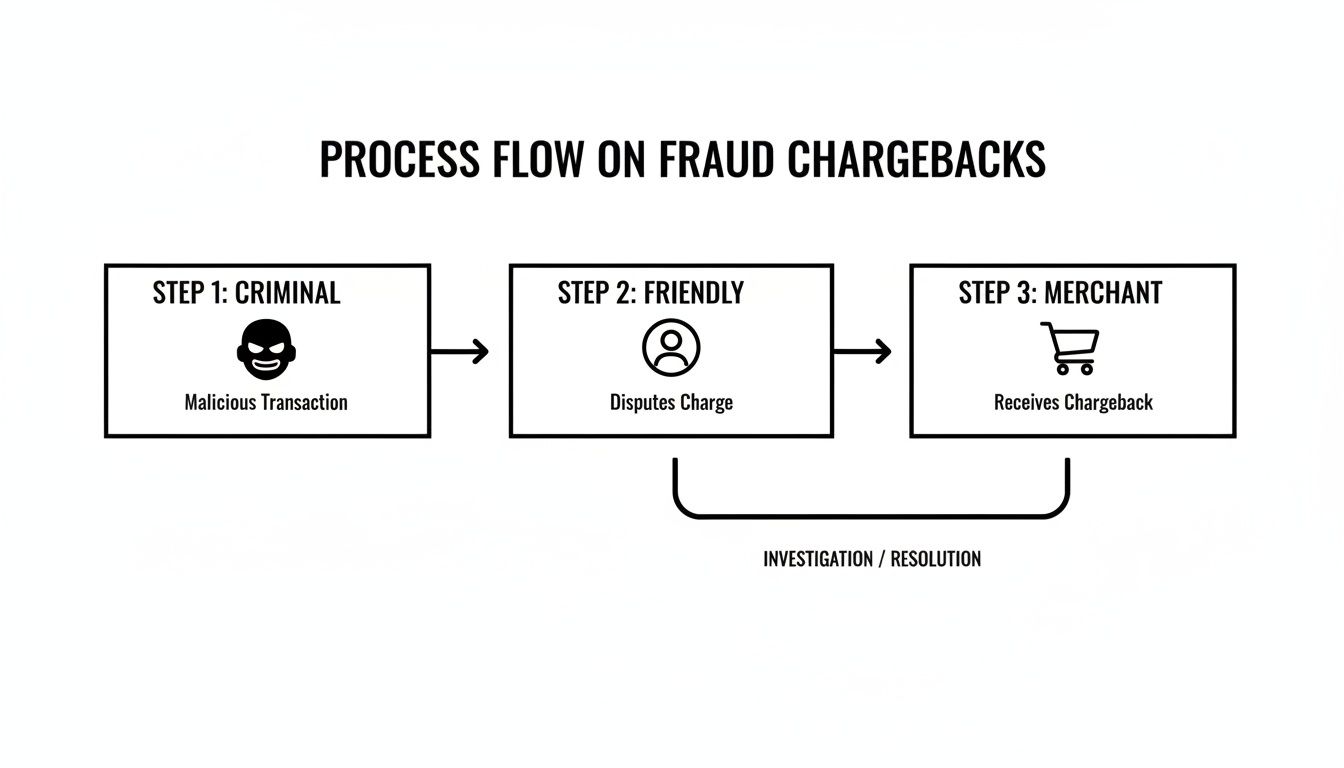

How to Fight a Chargeback for Fraud Step by Step

Getting hit with a chargeback for fraud notification feels personal, but it’s not a fight you have to lose on principle. The dispute process is really just a structured conversation with the customer's bank, and your job is to lay out a clear, logical case showing the transaction was legitimate.

Instead of panicking or just writing it off as a loss, you need a solid game plan you can use every time. Following a step-by-step process removes the emotion and guesswork, giving you the best shot at getting your money back.

This flowchart breaks down the typical paths a fraud chargeback can take, from clear-cut criminal fraud to friendly fraud and simple merchant errors.

Knowing where the dispute likely came from helps you zero in on the exact evidence you’ll need to build a winning response.

Step 1: Analyze the Chargeback Immediately

The moment that notification lands, the clock starts ticking. Most payment processors give you a very tight window to respond—sometimes only a few days. Don’t let it sit.

First thing's first: find the reason code. This code, assigned by the credit card company, gives you a hint about why the customer is disputing the charge. Even if it’s a generic "fraud" code, it’s the starting point for your investigation.

Next, pull up all the transaction details. Look at the customer's name, what they bought, the shipping address, and the total amount. Does anything seem off? This initial once-over will guide your evidence gathering.

Step 2: Gather Your Compelling Evidence

Okay, it’s time to build your case. Your entire goal is to collect every scrap of information that ties the real cardholder to this specific purchase. You’re essentially looking for proof that directly contradicts their claim of an "unauthorized transaction."

Break down your evidence into a few key piles:

- Customer & Order Information: This is the basic stuff—the customer’s name, email, and billing address. Make sure you also grab screenshots of the order confirmation and any emails you’ve traded.

- Transaction Authorization: This part is huge. You need to show that security checks were passed, like a positive AVS (Address Verification System) match or a correct CVV (Card Verification Value) entry.

- Shipping & Delivery Proof: If you shipped a physical product, this is your ace in the hole. Get that tracking number and a screenshot from the carrier’s website showing the delivery confirmation. It needs to show the item was delivered to the customer's address on file.

The heart of your defense is proving a direct link between the person who owns the credit card and the person who got the goods. Every piece of data that strengthens this connection is a point in your favor.

Don't overlook the digital trail, either. If the customer logged into an account on your site, include their account creation date and login history. If they checked a box agreeing to your terms of service, document that, too. For a deeper dive, our guide on chargeback representment covers more advanced tactics.

Step 3: Craft a Professional Rebuttal Letter

With all your evidence lined up, the last step is writing a clean, concise rebuttal letter. This letter is your formal response to the bank, so keep it professional and easy to follow. Ditch the emotional language and just stick to the facts.

Think of it as the cover letter for your evidence package. Start by identifying the transaction and stating clearly that you are disputing the chargeback. From there, walk the bank representative through your evidence piece by piece.

A simple, logical structure works best:

- Introduction: State the transaction date, amount, and customer's name. Clearly say you are challenging the fraud claim.

- Evidence Summary: Bullet point the key pieces of evidence you're attaching. For example, "Attached you will find a positive AVS match, proof of delivery from UPS (Tracking #12345), and our email correspondence with the customer."

- Conclusion: Briefly wrap up why your evidence proves the charge was legitimate and respectfully ask that the chargeback be reversed.

Attach all your supporting documents to this letter. Make sure every file is clearly labeled so the reviewer can easily match your letter to the proof. A well-organized, evidence-backed response massively boosts your odds of winning the chargeback for fraud dispute.

Your Essential Evidence Checklist for Winning Disputes

When you're fighting a chargeback for fraud, the evidence you submit is your one and only chance to speak. A strong defense isn't about arguing; it's about presenting a clear, undeniable story that proves the transaction was legitimate.

Think about it: the bank employee reviewing your case has no idea who you are. Your job is to hand them a file so compelling it leaves no room for doubt.

It's a lot like being a detective presenting findings to a judge. Each piece of evidence builds on the last, creating an airtight case. We’ve broken this down into a simple checklist you can use every single time a dispute comes in.

Customer and Account Information

First things first, you have to prove the person who made the purchase is the person who owns the card. This collection of data establishes a digital identity and connects it directly to the order.

- Customer Details: Collect the full name, email address, and billing address provided at checkout.

- IP Address: Note the IP address used to place the order. Showing that it matches the cardholder's billing city or state is a powerful piece of evidence.

- Customer Communication: Grab screenshots of any emails, live chats, or even social media DMs you've had with the customer.

- Account History: If the customer has an account with you, show their order history and the date their account was created. A long-time customer is a lot less likely to be a fraudster.

Transaction and Order Details

Next up, you need to show the nitty-gritty of the transaction itself. This part of your evidence proves that all the proper authorization steps were taken and that the order details were crystal clear.

The core goal here is simple: connect the dots between the payment method and the specific goods or services delivered. This paperwork validates the transaction's legitimacy from start to finish.

This is where you show your work. Pull together every detail you can find.

- Order Receipt: Provide a copy of the invoice showing item descriptions, quantities, and the total amount charged.

- AVS and CVV Responses: This is critical. Show the results of your Address Verification System (AVS) and Card Verification Value (CVV) checks. A "match" or "full match" is incredibly compelling proof.

- Terms of Service Acceptance: If your customer had to check a box to agree to your terms, shipping policy, or refund policy, provide a log or screenshot of this action.

To really strengthen your case, look into tools like smart receipt solutions that can provide the kind of detailed transaction records needed to shut down disputes. A well-crafted rebuttal letter also makes a huge difference; check out our guide on creating an effective rebuttal letter template to organize your evidence effectively.

Shipping and Delivery Confirmation

For physical products, this is often the smoking gun. It’s your proof that you held up your end of the bargain and delivered the item to the exact address the customer provided.

- Tracking Number: Always provide the complete tracking number for the shipment.

- Delivery Confirmation: Include a screenshot from the carrier's website (like UPS or FedEx) showing the date, time, and address of delivery.

- Signature Confirmation (If available): If you have a signature from the recipient, it's the strongest proof you can possibly offer.

This evidence directly counters the all-too-common friendly fraud tactic where a customer claims an item just never arrived. The cost of failing here is steep. The average chargeback costs a merchant over $120 once you factor in fees and lost revenue. Even worse, for U.S. merchants, every dollar lost to fraud actually costs them $4.61 in total damages.

Proactive Strategies to Prevent Fraud Chargebacks

The best way to win a fight over a chargeback for fraud is to never have the fight in the first place. It’s a simple truth, but shifting your focus from reactive defense to proactive offense is the single most powerful way to protect your revenue and sanity. This is all about building a smarter, more secure checkout that stops fraudsters cold while giving your real customers a seamless experience.

Think of your online store like a physical one. You wouldn't leave the front door unlocked overnight, right? The same logic applies online. A few key security measures can make a world of difference.

Fortify Your Checkout Process

Your checkout page is ground zero—your first line of defense. This is where you can deploy simple, effective checks that make life much harder for criminals trying to use stolen card details. While they aren't foolproof, they are absolutely essential deterrents.

Start with the fundamentals that every single online store should have switched on:

- Card Verification Value (CVV) Check: That little three or four-digit code on the back of a credit card is a surprisingly powerful security feature. Since thieves with stolen card numbers often don't have the physical card, requiring the CVV can stop a fraudulent transaction in its tracks.

- Address Verification System (AVS): This tool checks the billing address entered by the customer against the one the card issuer has on file. If they don't match, it’s a huge red flag that you might not be dealing with the legitimate cardholder.

These two checks are your bread and butter for preventing a chargeback for fraud. They're standard features on platforms like Shopify and PayPal, so get in there and make sure they’re enabled.

A clear, recognizable billing descriptor is one of the easiest and most overlooked ways to prevent accidental friendly fraud. If a customer sees "SPARKLETECH LLC" on their statement instead of "Sparkle Phone Cases," they might hit the panic button and file a dispute.

By making sure your descriptor matches your public brand name, you kill the confusion and drastically lower the chances of a customer mistakenly reporting a legitimate purchase as fraud.

Enhance Security with Advanced Tools

The basic checks are a great start, but today’s tricky fraud schemes call for more advanced solutions. Bringing in stronger authentication methods can seriously reduce your risk—and in some cases, even shield you from financial liability.

Implementing advanced methods like 3DS2 Liability Shift Authentication can be a game-changer. This technology adds an extra verification step, like a one-time code sent to the cardholder's phone, making it incredibly difficult for a fraudster to complete a purchase. When you use it correctly, the financial liability for fraudulent chargebacks can shift from you back to the card-issuing bank. You can find more strategies in our complete guide on chargeback fraud prevention.

You should also look into dedicated fraud detection apps or plugins. These tools are incredibly powerful, analyzing hundreds of data points for every single transaction in real-time. They’re constantly looking for suspicious patterns, such as:

- Multiple orders from different cards all shipping to the same address.

- An IP address location that is miles away from the billing address.

- An unusually large order from a brand-new customer.

These systems can automatically flag or even block high-risk orders before you ship them, saving you from an almost certain chargeback down the line.

Maintain Crystal-Clear Communication

Sometimes, a chargeback for fraud is filed simply because a customer feels left in the dark. Anxious buyers are quick to assume the worst, so keeping them informed every step of the way is a powerful prevention tool.

- Send Instant Order Confirmations: The second a purchase is made, fire off a detailed email receipt. It should include the order number, items purchased, total cost, and your store's name.

- Provide Shipping and Tracking Updates: Send another email the moment the order ships, complete with a tracking number and an estimated delivery date. This simple act reassures the customer that their product is on its way.

- Be Accessible and Responsive: Make your customer service contact info impossible to miss. A customer who can easily ask you a question is far less likely to go straight to their bank to file a dispute.

This level of communication builds trust and stops potential disputes before they even start. And with global chargeback volume projected to jump by 24% to 324 million transactions by 2028, taking these proactive steps is more critical than ever. Fortifying your business now will save you from major losses in the future.

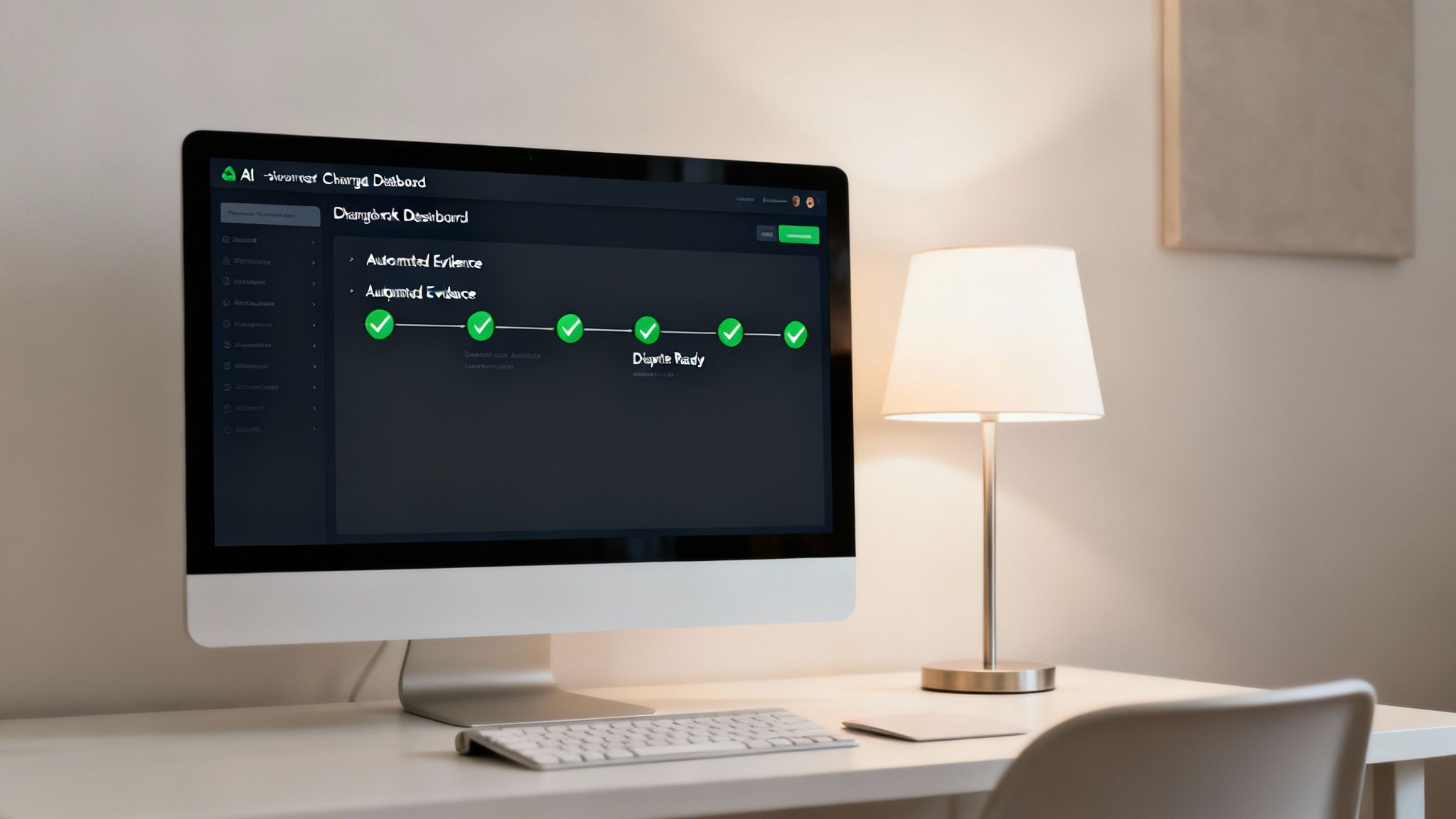

Automate Your Defense with AI-Powered Tools

Let's be honest: manually fighting every single chargeback for fraud is a massive drain on your most valuable assets—your time and your energy. It’s a slow, tedious grind of gathering evidence, writing letters, and tracking deadlines that pulls you away from what you should be doing: growing your business.

But what if you could put your entire chargeback defense on autopilot?

This is where automation and AI-powered tools come into the picture, completely changing the game for merchants. Instead of treating each dispute like a manual research project, these systems act as your dedicated chargeback specialist, working 24/7 to protect your revenue.

Think of it like having an expert detective who gets to work the instant a dispute is filed.

How AI Streamlines Your Defense

These smart platforms plug directly into your sales channels, like Shopify or PayPal, and your payment processors. When a chargeback for fraud hits your account, the system immediately springs into action without you having to lift a finger.

The process is incredibly efficient:

- Instant Analysis: The AI looks at the chargeback reason code and the original transaction data to understand exactly what kind of dispute it's dealing with.

- Automated Evidence Collection: It then automatically pulls all the crucial evidence we’ve talked about—customer info, AVS/CVV results, shipping confirmations, and IP data—from all your connected accounts.

- Compelling Response Generation: Using all that data, the AI builds a professional, evidence-backed rebuttal letter perfectly tailored to the specific reason code.

- Timely Submission: Finally, the complete evidence package is submitted to the bank on your behalf, guaranteeing you never miss a deadline.

This isn't just about saving time; it's about building a much stronger case. AI can pinpoint and highlight the most compelling pieces of evidence, seriously boosting your chances of winning the dispute and getting your money back.

The Real-World Benefits of Automation

Switching to an automated system isn't just a minor upgrade; it has a direct, measurable impact on your bottom line and how you spend your day. For a complete look under the hood, you can check out our guide to automated chargeback management to see how this technology works in detail.

The advantages are crystal clear:

- Recover Lost Revenue: The main goal here is to win more disputes. Businesses that use AI-powered tools often see their win rates climb, turning what was once a guaranteed loss into recovered profit.

- Save Countless Hours: By getting rid of the manual work, you and your team can get hours back every single week. That's time you can put back into marketing, customer service, and product development—the stuff that actually moves the needle.

- Scale Without Fear: As your business grows, so will your chargeback volume. An automated system scales right along with you, handling hundreds of disputes just as easily as it handles one.

Ultimately, automation frees you from being a full-time dispute manager and lets you get back to being a business owner. It gives you a powerful, data-driven defense that works tirelessly to protect the revenue you've worked so hard to earn.

Got Questions About Fraud Chargebacks? Let's Unpack Them.

When you're hit with a chargeback for fraud, it’s easy to feel lost. Having direct, no-fluff answers to the most common questions can give you the clarity and confidence to tackle these situations head-on.

Can You Actually Win a Dispute Without a Signature?

Yes, absolutely. While a signature feels like the ultimate proof, you can definitely win a dispute without one, especially for digital products or less expensive physical goods. Think of it less like a single knockout punch and more like building a solid case.

Powerful evidence like a positive AVS and CVV match, an IP address that lines up with the billing address, and delivery confirmation from the carrier (even without a signature) all work together. Your goal is to paint a clear, logical picture for the bank showing the transaction was legit, using all the data points you have.

What's the Real Difference Between a Chargeback and a Refund?

A refund is a conversation between you and your customer where you agree to return their money. It's a mutual decision. A chargeback, on the other hand, is a forced reversal kicked off by the customer's bank.

A simple way to see it: a refund is a handshake, but a chargeback is a lawsuit. Refunds help protect your customer relationships and avoid extra fees. Chargebacks are adversarial by nature and always hit you with penalties and costs.

How Long Do I Have to Respond to a Chargeback?

Once a chargeback is filed, a very strict clock starts ticking. The official response window depends on the card network (like Visa or Mastercard) and is usually somewhere between 20 and 45 days.

But here's the catch: your payment processor will almost always give you a much shorter internal deadline. They need time to process your evidence and submit it correctly. The key takeaway? Act immediately. If you miss that deadline, it’s an automatic loss.

Will Fighting Chargebacks Hurt My Business?

Quite the opposite. Fighting illegitimate chargebacks is one of the most important things you can do to protect your business. Payment processors expect you to stand up for valid transactions. When you consistently fight and win disputes, it signals that you have solid fraud prevention in place.

What really hurts your business is a high chargeback ratio—that's the percentage of chargebacks compared to your total sales. Letting friendly fraud slide just inflates this number, putting your entire merchant account in jeopardy. Fighting back shows you’re a vigilant and healthy business.

Tired of watching fraudsters walk away with your revenue? ChargePay puts AI to work, automating your entire dispute process—from gathering evidence to submitting the final case. We help merchants recover up to 80% of their lost funds. Stop losing money and start winning disputes today.

.svg)

.svg)

.svg)

.svg)