Chargebacks are not a side issue for Shopify stores. They are a revenue leak that keeps draining cash after the order is shipped, support has moved on, and inventory is gone.

The frustrating part is that many disputes are not classic stolen-card fraud. A large share comes from real customers disputing legitimate purchases, late complaints, confusion over descriptors, or buyers who go straight to the bank instead of talking to you first. That is why chargeback protection matters. Done right, it protects margin, lowers operational stress, and gives you a repeatable way to recover revenue that would otherwise be written off.

Your Store Is Leaking Money Through Chargebacks

For e-commerce merchants, chargebacks are projected to cost the industry a significant amount in future years. Friendly fraud constitutes a large majority of all chargebacks globally. In recent years, many millions of chargebacks have been filed, with merchants winning only 45% of disputes on average according to Chargeback.io's chargeback statistics.

That is why a single dispute never feels small.

You lose the order revenue. You often lose the product. You still absorb the operational time. Then you get hit with fees on top. If you want a quick breakdown of those extra costs, this explanation of a chargeback fee is worth reading.

Why this hurts Shopify stores more than expected

Shopify merchants move fast. You are managing product launches, fulfillment delays, subscription issues, ad spend, returns, and customer support. Chargebacks land in the middle of all that with strict deadlines and a burden of proof that sits on you.

Manual handling usually breaks down in one of three places:

- Evidence is incomplete: The order receipt is easy to find, but delivery proof, tracking events, customer emails, and prior order history are scattered.

- Responses are weak: A generic reply does not match the dispute reason code.

- Deadlines get missed: The dispute sits in an inbox until it is too late to build a solid case.

Every lost dispute is not just a refund. It is a second loss layered on top of the first one.

A lot of store owners accept this as part of online commerce. That is the mistake.

Strong chargeback protection turns disputes into a process instead of a fire drill. The return comes from recovering revenue you already earned and from stopping your team from wasting time on low-win manual work.

What a better system changes

The stores that handle chargebacks well do not rely on a single fraud filter and hope for the best. They put two systems in place.

First, they prevent avoidable disputes before checkout and after purchase. Second, they fight invalid disputes with documentation that fits what banks review.

That combination matters because prevention alone does not recover money once a dispute is filed.

What Chargeback Protection Means

Most store owners hear "chargeback protection" and think of fraud software. That is only part of it.

A practical definition is simpler. Chargeback protection is the set of tools and workflows that either stop a dispute from happening or help you win after it happens. If one half is missing, you still lose money.

A useful way to think about it is this: one team stands at the front door checking risky orders, and another team handles the legal paperwork after a dispute shows up.

For a broader merchant-side view, this overview of merchant chargeback protection covers the same split in practical terms.

Prevention blocks problems before they mature

Prevention is your first layer.

This includes checks at checkout, cleaner billing descriptors, better customer communication, and post-purchase workflows that reduce confusion before a cardholder calls the bank. Basic fraud tools are helpful here. So are order review rules for suspicious activity.

Prevention works well against straightforward payment fraud and preventable merchant mistakes. It also helps when customers do not recognize a charge or cannot find a support path.

What prevention does not do well is recover already-lost revenue. Once the bank opens a dispute, you are in a different game.

Representment recovers revenue after a dispute is filed

Representment is the formal process of responding to a chargeback with evidence. Most merchants struggle with this aspect. The bank does not care that you "know" the customer received the order. It wants proof that matches the reason code and card network rules. That can mean transaction details, fulfillment evidence, delivery confirmation, customer communication logs, account history, usage records, and timelines that show the purchase was legitimate.

A weak representment case usually sounds like this:

- Customer ordered

- Product shipped

- Merchant believes the claim is false

That is not enough.

A strong case ties evidence directly to the dispute type. If the claim is unauthorized, you need records that support authorized use. If the claim is item not received, you need shipment and delivery evidence. If the claim is canceled recurring billing, you need subscription and cancellation records.

Why you need both

A prevention-only setup leaves money on the table. A representment-only setup means you are fighting too many disputes that could have been avoided.

For most established Shopify stores, the hard truth is this: friendly fraud and customer-led disputes make representment essential. Prevention reduces volume. Representment recovers revenue from the disputes that still arrive.

Good chargeback protection does not ask you to choose one side. It keeps bad orders out and builds strong cases for the good orders that get disputed anyway.

That is the baseline. Everything else is execution.

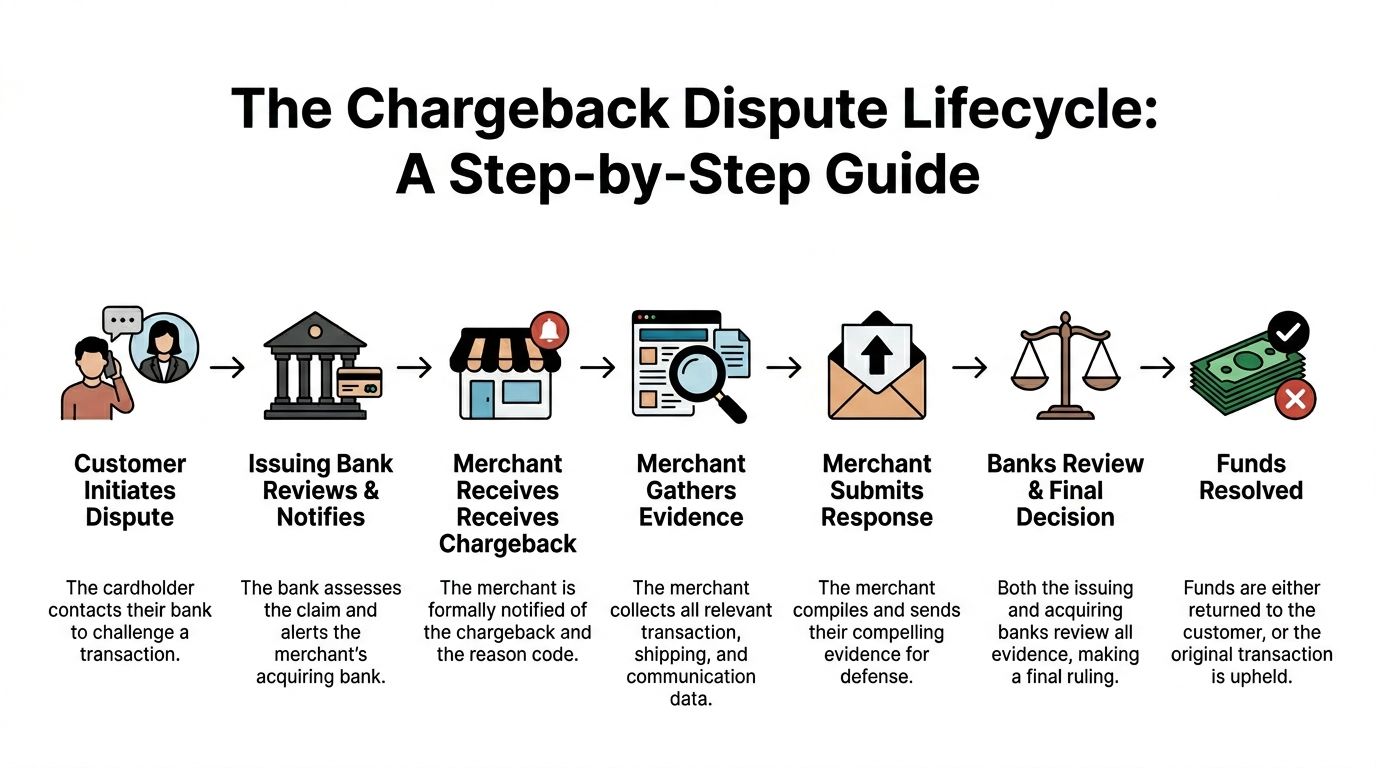

The Chargeback Dispute Lifecycle Explained

A chargeback starts with a customer action, but it quickly turns into a bank-driven workflow with strict timing and very little room for error.

Once the cardholder contacts their bank, funds may be pulled from your side while the dispute is reviewed. Then the notice lands with your processor or in your dashboard, and the clock starts. At that point, speed matters almost as much as evidence quality.

This walkthrough of the card dispute process is useful if you want the merchant-side version of each handoff.

What usually happens in a real dispute

A customer sees a charge and files a complaint with the issuer.

The issuing bank reviews the claim at a high level and sends the dispute into the card network flow. Your acquiring bank or payment provider then passes the case to you, usually with a reason code and a deadline. That reason code shapes what evidence has a chance of working.

Now your team has to collect the right records quickly. That often includes:

- Order data: Items purchased, timestamp, amount, billing details

- Fulfillment records: Tracking, carrier scans, delivery confirmation

- Customer communication: Emails, tickets, chat logs, refund requests

- Account behavior: Login history, prior purchases, usage signals where available

If the package was delivered, that helps. If the product was digital, the evidence needs to show access, account ownership, or usage records. If the customer previously contacted support, the timeline matters.

Then you submit a response. The banks review it. Funds either stay reversed or come back.

Where merchants lose

The process sounds manageable until you try to do it at volume.

The evidence lives in different systems. Shopify has some of it. Your help desk has another part. The carrier has shipping events. Your subscription or login platform may hold the rest. Pulling all of that together manually is slow.

There is also a quality problem. A lot of responses are true but not persuasive. Banks do not reward effort. They reward documentation that answers the exact claim.

How 3D Secure changes the starting point

One tool can improve the dispute lifecycle before the dispute even begins. 3D Secure 2.0 shifts liability for certain fraudulent transactions from merchants to issuers through stronger authentication, and evidence from Visa and Mastercard rules shows 3DS 2.0 cuts chargeback rates by up to 70% for card-not-present disputes according to AlphaComm's write-up on chargeback protection.

That matters because it changes the kind of evidence available later.

When authentication data exists, the issuer has more to review during representment. In some unauthorized claims, that gives the merchant a much stronger position than a plain card-not-present transaction with no extra verification trail.

If you sell online and rely heavily on card payments, enabling 3DS 2.0 through your gateway is one of the cleaner ways to improve chargeback protection at the transaction level.

It will not solve every dispute type. It does not fix item quality complaints or subscription confusion. But it can reduce exposure where unauthorized claims are common.

Prevention vs Representment Which Strategy Wins

If you only had budget or attention for one side of chargeback protection, where would the return be better?

For most Shopify stores with steady order volume, representment usually produces the clearer financial return, while basic prevention provides support around it. That is because prevention can lower future dispute volume, but representment is the only thing that can recover money from disputes already filed, especially the customer-led ones that slip past checkout checks.

Where prevention earns its keep

Prevention is still worth doing.

Address checks, CVV checks, 3DS through supported gateways, clean descriptors, clear refund policies, and fast support all reduce avoidable disputes. They are especially useful against obvious fraud and confusion-based complaints.

But prevention has trade-offs:

- It can reject good customers: Overly aggressive filters create false declines.

- It cannot reverse a filed dispute: Once the bank opens the case, your fraud rule is irrelevant.

- It struggles with friendly fraud: A legitimate customer can pass every fraud check and still file a chargeback later.

That last point is the biggest limitation for established stores. Many disputes come from completed, fulfilled orders that looked fine at checkout.

Why representment carries more weight

Representment deals with the disputes prevention cannot stop.

It is how you recover revenue from customers who received the item, used the service, forgot the subscription, or skipped your support team and went directly to their bank. It is also where process quality matters most. Good representment is not about arguing harder. It is about assembling evidence faster and matching it to the bank's framework.

Manual representment can work if you have a small store and low dispute volume. Past that, it starts eating time fast.

Here is the practical difference.

Manual vs Automated Chargeback Representment

| Task | Manual Effort (You) | Automated Effort (ChargePay) |

|---|---|---|

| Find dispute notice | Monitor processor emails and dashboards | System detects and tracks incoming disputes |

| Gather order records | Pull data from Shopify manually | Pulls order data automatically |

| Collect shipping proof | Check carrier portals one by one | Compiles fulfillment evidence into the case |

| Match evidence to reason code | Interpret reason code yourself | Builds the response around the dispute type |

| Write rebuttal | Draft custom response under time pressure | Generates a structured response for submission |

| Meet deadlines | Set reminders and hope nothing slips | Submits before deadlines and monitors status |

| Track outcomes | Update spreadsheets manually | Tracks recoveries and case outcomes in one place |

That table is why representment often wins the ROI argument.

The more disputes you get, the more expensive manual work becomes. The cost is not just payroll time. It is missed deadlines, weak cases, and the mental load of switching between ops, support, and bank paperwork.

The right answer is not either-or

The highest-value setup usually looks like this:

- Use prevention for the front end: checkout controls, customer communication, post-purchase clarity

- Use representment for the back end: evidence, deadlines, issuer-facing responses

- Audit what causes disputes: fraud, confusion, fulfillment issues, recurring billing complaints

Here, chargeback protection stops being theoretical and starts becoming operational.

One practical option for Shopify stores is ChargePay's chargeback representment workflow, which focuses on automated dispute fighting rather than asking merchants to manage another dashboard by hand.

Prevention reduces the number of fires. Representment recovers money from the fires that still happen.

If your store already has disputes coming in every month, that distinction matters more than any generic fraud promise.

How AI Automates Winning Chargeback Disputes

Automation matters because chargebacks are repetitive, deadline-driven, and document-heavy. Those are exactly the conditions where manual work fails first.

AI-based chargeback protection is useful when it does three jobs well: gather evidence, shape the response around the dispute type, and submit on time without waiting for someone on your team to intervene.

According to Kount's chargeback analysis, platforms using predictive analytics and machine learning reduce chargeback losses by up to 80% for merchants, and financial institutions spend an average of $9.08 to $10.32 processing each dispute, which is one reason automation keeps gaining ground.

Automated evidence gathering

The first gain is speed.

When a dispute hits, the system can pull the evidence most merchants would otherwise collect by hand. That may include the order timeline, billing and shipping details, tracking events, customer communication, and prior order history tied to the customer profile.

That sounds simple until you do it manually across multiple tools.

With AI, the value is not just faster collection. It is consistency. Cases do not get weaker because someone forgot to include a delivery scan or missed an email thread that showed the customer already acknowledged receipt.

Intelligent response writing

A useful chargeback response is not a generic statement. It has to fit the reason code.

AI can map the available evidence to the claim and build a response that is organized, relevant, and bank-readable. That is much better than copying a template into every dispute regardless of whether the complaint is unauthorized use, item not received, or service cancellation.

The best systems also remove weak arguments. That matters because overloading a case with unrelated screenshots does not help. It can make the file harder to review.

For a deeper look at that workflow, this guide to automated chargeback and dispute management using AI breaks down how evidence collection and submission can be handled without manual case assembly.

Submission and tracking

Many stores lose chargebacks before the bank even reviews the substance.

They lose because the deadline passed. Or because the response was uploaded in the wrong place. Or because nobody followed the case after submission.

AI helps by keeping the process moving. It submits on schedule, tracks status changes, and keeps records tied to the case outcome.

This short video shows what that kind of workflow looks like in practice.

What this means for a Shopify team

For a Shopify merchant, the practical upside is straightforward:

- Less admin work: Your team is not chasing data across tools

- Fewer avoidable losses: Deadlines and missing files stop killing cases

- Better recovery discipline: Every dispute gets a structured response instead of ad hoc effort

This alters the economics. A merchant who handles disputes manually pays in staff time whether they win or lose. An automated workflow makes the effort more predictable and usually much lighter.

Choosing Your Chargeback Protection Partner

The wrong provider can make chargeback protection more expensive without making it more effective. Guarantee-style products often sound reassuring at first but then narrow coverage in the fine print. A lot of merchants do not discover the exclusions until a claim is denied.

According to Kount's guide on preventing chargebacks, many providers exclude merchant errors or non-fraud reasons, some cap protection, and manual responses may still be required. The same source notes that only 40 to 60% of "guaranteed" cases are reimbursed because of those restrictions.

What to check before you install anything

Start with the business model.

If a provider charges on every transaction or every approved order, ask what happens when the dispute reason falls outside coverage. If they only reimburse certain fraud cases, that is not full chargeback protection. It is selective reimbursement.

Then check the workload. Some tools still expect your team to gather proof of delivery, support logs, or transaction details under deadline pressure. That is not real relief. It is a thinner interface on top of the same manual process.

A practical evaluation checklist:

- Cost model: Do you pay regardless of outcome, or only when money is recovered?

- Coverage reality: Are only certain fraud cases included, while friendly fraud and merchant-side issues are excluded?

- Automation depth: Does the system build and submit responses, or does it just surface alerts?

- Shopify fit: Is it built around your platform's data and workflow, or is Shopify just another integration?

- Merchant burden: Who gathers the evidence when a dispute arrives?

- Proof of results: Can the provider point to a win rate and a real dispute history?

Why Shopify-native matters

Generic dispute software often treats the store as a data source and little more.

A Shopify-native product can pull order details, customer history, and fulfillment context more naturally. That matters because representment quality depends on evidence quality. If the app struggles to access the right records, your response quality drops.

The Built for Shopify badge is useful here because it signals closer alignment with Shopify's standards and merchant experience expectations. It does not replace due diligence, but it is a good sign.

The model that usually feels fairest

For most merchants, pay-per-win is easier to evaluate than broad guarantee language.

If the provider only gets paid when money is recovered, the incentives are clear. You are not funding a lot of covered-but-not-recovered theory. You are paying for successful outcomes.

That is also why many merchants prefer autonomous representment over insurance-style positioning. Insurance language suggests certainty. Dispute recovery is never certain. It is a process that depends on evidence, timing, and coverage details.

If you have to read pages of exclusions to figure out whether a dispute qualifies, you are not buying clarity. You are buying ambiguity.

A good partner should lower workload, fit your Shopify stack, and make the economics easy to understand.

Common Questions About Chargeback Protection

Is chargeback protection worth it if my store does not get many disputes

Usually, yes, if the pricing model does not force fixed cost onto a small dispute volume.

Low-volume stores still face the same deadlines and evidence requirements as high-volume stores. Even a handful of losses can hurt when margins are tight. The key is avoiding a setup that charges heavily before it proves value.

Is chargeback protection the same as chargeback insurance

No.

Insurance or guarantee products typically reimburse only certain approved fraud cases and often come with exclusions. Full chargeback protection should cover the operational side of prevention and dispute fighting, not just selective reimbursement language.

That difference matters because many disputes are not classic fraud claims. They involve customer behavior, confusion, fulfillment disagreements, or friendly fraud.

Will fighting disputes make my processor or bank view my store negatively

Not when the disputes are legitimate to challenge and the cases are well documented.

A disciplined representment process helps show that your store has records, fulfillment proof, and a real dispute-handling workflow. What hurts processor relationships is unmanaged dispute volume and weak operational controls.

Why do so many merchants still lose when they have a guarantee product

Because the guarantee often still depends on merchant action.

As PayPal's help documentation and related vendor practices show, merchants may need to provide proof of delivery and customer communication logs within tight 7 to 20 day deadlines, and AI-driven representment can improve outcomes by boosting success from a 20 to 30% manual win rate to over 90% according to PayPal's chargeback protection information.

If the merchant misses the deadline or cannot produce the required evidence, the promise becomes much narrower than it first appeared.

How quickly can I expect to see recovered revenue

Recovery timing depends on the card network, issuer review speed, and dispute type.

What you should expect quickly is process improvement. A strong automated setup starts collecting evidence and responding as soon as disputes arrive. Revenue recovery follows the dispute cycle, but the operational benefit begins right away because your team is no longer scrambling case by case.

What should I look for first when comparing options

Start with these three questions:

- Who does the work: your team or the platform?

- When do you pay: upfront, per transaction, or only on wins?

- Does it fit Shopify cleanly: or will it create another tool your team has to babysit?

Those answers tell you more than polished sales language.

If chargebacks are eating into your margins, install ChargePay from the Shopify App Store. It is built for Shopify, carries a 4.9-star rating, and uses a pay-per-win model so you only pay when revenue is recovered.

.svg)

.svg)

.svg)

.svg)