Losing money to chargebacks is a frustrating reality for any Shopify store owner. The key to stopping that drain isn't a secret—it's understanding chargeback reason codes.

Think of these codes as a short note from the card network (like Visa or Mastercard) that explains exactly why a customer disputed a charge. It could be fraud, a problem with fulfillment, or just a simple processing error. Unlocking what they mean is the first step to getting your money back.

Decoding the Blueprint to Winning Disputes

For Shopify merchants, these codes are more than just technical jargon; they’re your roadmap to protecting your bottom line. Ignoring them is like trying to solve a puzzle with half the pieces missing. Each code tells a story about what went wrong with a transaction and gives you a direct path to fighting back the right way.

Here at ChargePay, we've been in the trenches, handling over 100,000 disputes and getting back more than $2.8 million for merchants just like you. Our experience has shown us one thing: winning starts with knowing exactly why you lost the money in the first place.

Why Every Code Matters

Every single chargeback that hits your account comes with a specific alphanumeric code assigned by the customer's bank. This code dictates the entire dispute process, from the evidence you need to submit to the deadlines you have to meet. If you get this part wrong, you're looking at an automatic loss.

For instance, a "Fraud" code requires a totally different set of evidence (like AVS/CVV matches and IP logs) than a "Product Not Received" code, which is all about proving delivery. If you treat them the same, you’re just throwing money away.

When you translate these cryptic codes into clear, actionable steps, you turn a confusing problem into a real opportunity. This is the first step toward building a solid representment case and replicating our 92.4% win rate.

Getting a handle on the different reasons for a chargeback is absolutely fundamental. Without this knowledge, you’re flying blind.

To get started, it helps to see how these codes are grouped. Here’s a quick breakdown of the four main categories you’ll run into.

Quick Lookup for Chargeback Code Categories

| Category | What It Means for Your Store | Common Shopify Example |

|---|---|---|

| Fraud | A transaction made with a stolen card or without the cardholder's permission. | A large order for high-demand electronics is placed with a credit card that was just reported stolen. |

| Authorization | An issue with the transaction's approval process itself. | Your system accidentally charged a customer twice for the same order (a duplicate charge). |

| Processing Errors | A mistake made during the transaction, often by the merchant or payment processor. | A customer was promised a refund, but it was never processed, so they filed a chargeback to get their money. |

| Consumer Disputes | The customer has an issue with the product, service, or delivery. This is the most common category. | A customer claims the custom t-shirt they received was a different color than what was shown on your product page. |

Knowing which bucket a dispute falls into immediately tells you what kind of fight you're in for and what evidence will matter most to the bank.

Turning Codes into Cash Recovery

When you really get what these codes mean, you can start making smart moves:

- Gather the right evidence: Stop wasting time digging up documents the bank doesn't care about. Submit exactly what the specific code requires.

- Spot troubling patterns: Are you seeing a lot of "Not as Described" codes? It might be a sign that you need to beef up your product descriptions or take better photos.

- Fight friendly fraud: Pinpoint customers who claim "fraud" after their package has been delivered, and build a powerful case with delivery proof and order details.

Ultimately, mastering chargeback reason codes is about shifting from a defensive, reactive position to a proactive, revenue-recovering one. This guide will give you the tools to do exactly that.

To put this whole process on autopilot, you can install ChargePay from the Shopify App Store. We're rated 4.9 stars and are proud to hold the exclusive Built for Shopify badge.

Visa and Mastercard Reason Codes Explained

Let's get straight to it. This is your playbook for decoding and fighting the most common chargebacks from Visa and Mastercard. Forget generic advice—we’re giving you a specific, evidence-based action plan for every code. This isn't just theory; it's the exact knowledge we've used to handle over 100,000 disputes and claw back $2.8 million for Shopify merchants just like you.

Think of this as your go-to reference guide for the moment a dispute hits your dashboard. We'll cut through the banking jargon and show you exactly what documents you need to gather to win.

Common Visa Chargeback Reason Codes and How to Beat Them

Visa sorts its reason codes into four buckets—Fraud, Authorization, Processing Errors, and Consumer Disputes. We're going to zero in on the ones that hit Shopify stores the hardest.

Visa Code 10.4: Other Fraud, Card-Absent Environment

- What it means: This is the classic "I didn't authorize this online purchase" claim. It’s a favorite for both real fraud (stolen cards) and friendly fraud, where a legitimate customer wants their money back for free.

- Your Action Plan: Your mission is to prove the real cardholder made the purchase. You need to pull together compelling evidence like AVS/CVV match results, IP address logs that match the shipping city, and any customer emails or past order history. If you used 3D Secure, that’s your silver bullet.

Visa Code 13.1: Merchandise/Services Not Received

- What it means: The customer is claiming they paid, but the product never arrived. This is a huge headache for e-commerce merchants, especially when you're at the mercy of shipping carriers.

- Your Action Plan: This one is all about proving delivery. Your absolute best evidence is a proof of delivery document with a signature, showing an address that matches what's on the order. Clear, legible tracking info from the carrier showing the "Delivered" status is non-negotiable.

Globally, 'Product or Service Not Received' is one of the most common reasons for a chargeback, and it's expected to be a huge part of the projected 261 million global chargebacks in 2025. On their own, merchants typically win only about 30% of these disputes. In contrast, ChargePay’s AI automates evidence packages with signed proofs of delivery and tracking data to hit a 92.4% win rate for our merchants.

Common Mastercard Chargeback Reason Codes and How to Beat Them

Mastercard uses four-digit codes, but the reasons behind them are pretty much the same as Visa's. Here are the two you absolutely have to know.

Mastercard Code 4837: No Cardholder Authorization

- What it means: Just like Visa's 10.4, this code pops up when the cardholder says they never authorized the transaction. It's a go-to for friendly fraud.

- Your Action Plan: You have to build a case proving the purchase was legit. Combine transaction data showing AVS and CVV matches with the IP address of the device used for the purchase. If that IP address is in the same city as the cardholder’s billing or shipping address, you’ve got a strong rebuttal. A history of previous, undisputed orders from that same customer is also incredibly powerful.

When you're fighting a 'No Authorization' claim, you have to think like a detective. You're connecting the dots between the digital footprint (IP address, device ID) and the physical delivery address to prove to the bank that the real cardholder was involved.

Mastercard Code 4853: Cardholder Dispute

- What it means: This is a broad "consumer dispute" category. For Shopify merchants, it usually breaks down into two claims: "Merchandise Not as Described" or "Defective Merchandise." Basically, the customer is saying the product wasn't what they expected.

- Your Action Plan: Your product page is your best friend here. Submit crystal-clear screenshots of the product description, images, and any size or material specs from your store at the time of the purchase. Pair this with your shipping policy and any pre-purchase chats to prove you set clear expectations from the start.

Navigating the rules for each card network can get complicated. For a deeper dive into Visa's specific rules and timelines, you can check out our detailed guide on the Visa chargeback process.

Winning chargebacks comes down to providing the right evidence for the right reason code, every single time. It's a repetitive, detail-heavy task—which makes it perfect for AI. If you're tired of losing revenue, install ChargePay from the Shopify App Store. We're a Built for Shopify app with a 4.9-star rating, ready to put our 92.4% win rate to work for you.

Handling Amex and Discover Chargeback Codes

While you're probably seeing Visa and Mastercard disputes most often, you absolutely cannot sleep on chargebacks from American Express and Discover. It's a classic mistake. These card networks play by their own rules, with unique reason codes and evidence requirements. Ignoring these differences is like throwing revenue away.

Here at ChargePay, we've seen it all. After managing over 100,000 disputes and clawing back $2.8 million for merchants, we know that success comes from understanding the specific playbook for each card network—not just the big two. Let's break down what you need to know to fight and win Amex and Discover disputes.

American Express Chargeback Codes

American Express has a reputation for putting its cardholders first. This means they often lean towards the customer unless you hit them with undeniable, rock-solid proof. Their reason codes are a mix of letters and numbers.

Code C08: Goods/Services Not Received. This is the Amex version of the classic "item not received" claim. The customer is simply saying they paid for something, but it never showed up.

How to Fight It: Your whole case hinges on definitive proof of delivery. You need to provide a shipping confirmation that clearly shows the full delivery address, the delivery date, and a signature if you have one. That delivery address must be an exact match to the one on the order. No exceptions.

Code C31: Goods/Services Not as Described. With this one, the customer is claiming the product is way different from what they saw on your Shopify store. Maybe it looks different, it's the wrong size, or it's just defective.

How to Fight It: Your product page is your best friend here. Get crystal-clear screenshots of the product description, all the images, and any material or sizing details from when the order was placed. If you have any emails or chats with the customer clarifying details about the product, include those too. You have to prove to the bank that you set the customer's expectations perfectly.

Discover Chargeback Codes

Discover also has its own system. The reasons for the disputes are familiar, but the codes and what you need to prove are different. For a really deep dive, you can check out our complete guide to Discover Card chargeback rules.

- Code RG: Non-Receipt of Goods or Services. Just like Amex's C08, the cardholder claims their order is missing in action. This is a super common one for e-commerce stores.

- How to Fight It: Your job is to provide the full tracking history from a reliable carrier showing that "Delivered" status. The most critical part? Making sure the tracking info clearly shows the delivery address matches the one on the customer's order. Any small difference here is an easy way to lose the dispute.

Getting the nuances between card networks right is a full-time job. A "Not Received" claim from Amex might need slightly different evidence than the same claim with Discover. It's that level of detail that makes the difference between our 92.4% win rate and the industry average.

Trying to fight all these disputes by hand is a massive time-sink. For every single one, you have to figure out the code, understand its specific rules, dig up the right evidence, and get it all submitted before a tight deadline.

This is exactly where automation becomes a lifesaver. ChargePay's AI instantly knows the reason code from any card network. It automatically pulls the correct data from your Shopify store and puts together the perfect evidence packet for you. If you're tired of the guesswork and ready to start winning, install ChargePay from the Shopify App Store. Our 4.9-star rating and Built for Shopify badge show we’re a partner that merchants like you trust.

How to Build a Winning Representment Case

Just knowing the chargeback reason code is only half the battle. How you fight back is what actually gets your money back. Think of building a solid representment case as translating that reason code into a story that proves the bank should reverse the dispute. It’s a methodical process, not guesswork.

This isn’t some theory, either. It’s the exact method our AI uses to hit a 92.4% success rate for the Shopify merchants we protect. We’ve used this blueprint to recover over $2.8 million across more than 100,000 disputes.

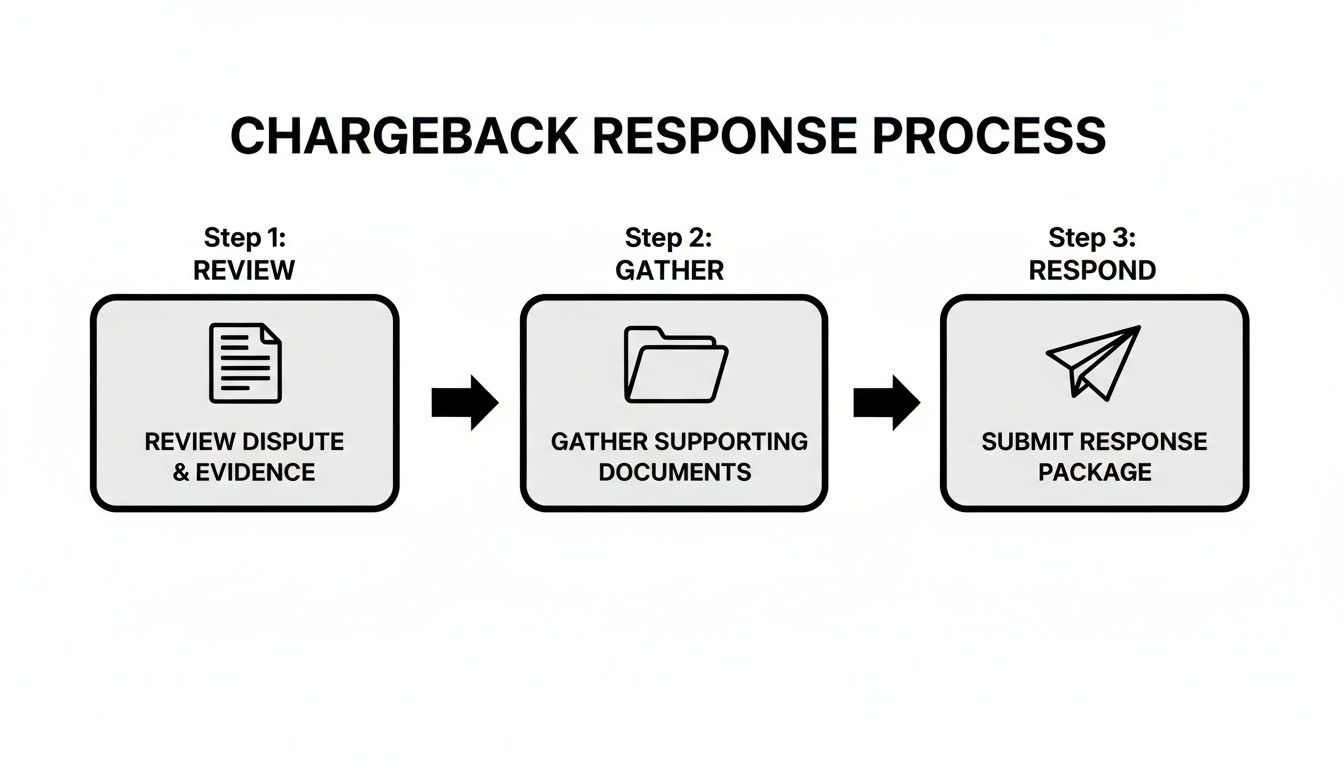

Your Step-by-Step Response Blueprint

Every time a chargeback lands in your account, you have to move fast, but you also have to be organized. A winning response always breaks down into three simple phases. Each step builds on the last, creating an undeniable argument against the customer’s claim.

This is the basic path from getting a chargeback notice to submitting a response that wins.

This workflow—review, gather, and respond—is the foundation for turning a lost sale back into recovered revenue.

Following this structure makes sure you're hitting the specific chargeback reason code with the right evidence, which seriously bumps up your chances of winning. It's all about being precise.

Writing a Rebuttal Letter That Gets Results

Your rebuttal letter is your one shot to tell your side of the story directly to the issuing bank. It has to be clear, straight to the point, and use the evidence you gathered to tear down the customer’s claim. A messy or confusing letter will get tossed aside in seconds.

Your letter should always do three things:

- Get straight to the point: Start by saying you're disputing the chargeback and list the key transaction details.

- Tackle the claim head-on: Use the reason code to directly refute what the customer is claiming. If it’s a "Product Not Received" dispute, your first line should be about how the product was delivered, pointing to your proof.

- Summarize your proof: Briefly list the documents you’ve attached, like "tracking confirmation showing delivery to the cardholder's address" or "AVS and CVV match data from the transaction."

A great rebuttal letter connects the dots for the bank reviewer. It doesn't just hand them a pile of evidence; it explains why that evidence makes the chargeback invalid. That narrative is what gets you a fast, favorable decision.

For example, if you're fighting friendly fraud, you could write something like: "The cardholder is claiming this transaction was unauthorized (Code 10.4). However, our evidence shows a successful AVS and CVV match, and the IP address from the order geolocates to the same city as the shipping address. This proves the legitimate cardholder made the purchase."

This whole process of fighting back is called chargeback representment. If you want to get even deeper into crafting your arguments, check out our full guide on chargeback representment strategies.

Or, you could just let us do it for you. Install ChargePay from the Shopify App Store, and our AI will automatically build and send winning dispute responses for you. With a 4.9-star rating and the Built for Shopify badge, you can trust us to have your back.

Automating Your Chargeback Responses with AI

Let's be honest—manually fighting chargebacks is a full-time job you simply don't have time for. Every minute you spend digging through Shopify for evidence is a minute you're not spending on what really matters: growing your store. This is exactly where automation steps in to take the work off your plate.

This is where ChargePay completely changes the game for Shopify store owners. Our AI-powered platform automates the entire dispute process from start to finish. That means no more manual work, no missed deadlines, and no need to become an expert on every single chargeback reason code out there.

How ChargePay's AI Solves Your Chargeback Problem

The moment a chargeback hits your store, our system instantly identifies the reason code and gets right to work. It pulls all the necessary transaction data directly from Shopify—things like AVS/CVV matches, IP logs, and shipping confirmations—and builds a comprehensive, evidence-packed response tailored to that specific code.

Globally, chargebacks hit 238 million in 2023, and merchants who fight them alone only win about 30% of the time. ChargePay flips that script. Our AI handles the entire dispute lifecycle for you, generating responses that have achieved a 92.4% win rate across over 100,000 cases, recovering more than $2.8 million for merchants just like you.

We know exactly what evidence the banks need to see for each reason code because we’ve successfully handled thousands of them. Our system detects fraud patterns, compiles the perfect evidence package, and submits the response on your behalf, well before the deadline.

This means you can finally stop worrying about losing revenue to confusing chargebacks. You only pay when we win, turning a major revenue drain into a solved problem.

To learn more about how this works, you can read our complete guide to automated chargeback and dispute management using AI.

Ready to stop losing money and let AI handle the headaches? Install ChargePay from the Shopify App Store. We're proud to have a 4.9-star rating and the exclusive Built for Shopify badge.

Frequently Asked Questions About Reason Codes

Diving into the world of disputes can feel like you're trying to learn a new language, but getting a handle on chargeback reason codes is a massive step toward protecting your bottom line. Let's walk through the questions we hear most often from Shopify merchants just like you.

What Is the Most Common Chargeback Reason Code?

For Shopify stores, we consistently see two types of disputes leading the pack: 'Product Not Received' (like Visa 13.1) and 'Credit Not Processed'.

These often pop up due to simple shipping delays, a confusing return policy, or, increasingly, from friendly fraud. That’s when a customer has their item but claims it never arrived. Across the 100,000+ disputes we've managed, these are by far the most frequent headaches.

Can I Win a Chargeback with a Fraud Reason Code?

Yes, you can, and you should. This is especially true when you suspect friendly fraud is at play. To fight back against a fraud-related code like Visa 10.4 (Card-Absent Fraud), you have to hit them with compelling evidence that proves the real cardholder was behind the purchase.

Some of the best proof you can provide includes:

- AVS and CVV match data straight from your payment processor.

- IP address logs that place the order in the same city as the shipping address.

- A history of past, undisputed orders from that same customer.

How Long Do I Have to Respond to a Chargeback?

This is where things get serious. The deadlines are strict and you can't negotiate them. You’ll typically have between 20 to 45 days to respond, and the exact window depends on the card network.

If you miss that deadline, you automatically lose the dispute and the money is gone for good. It's one of the main reasons trying to handle this manually often fails—an automated system makes sure you never let a deadline slip by.

What Is Representment?

Representment is simply the official industry term for fighting a chargeback.

It’s the process where you collect and submit all your evidence to prove the customer's claim isn't valid. The goal is to convince the bank to reverse the chargeback in your favor. A winning representment case is always built around tackling the specific chargeback reason code head-on.

Don't let confusing reason codes and impossible deadlines chip away at your profits. ChargePay automates the entire representment process for you. We use AI to build winning dispute cases based on our experience recovering over $2.8 million for merchants. With our 92.4% win rate, you only pay when we win for you.

Ready to turn chargebacks into a solved problem? Install ChargePay from the Shopify App Store and let our Built for Shopify app start protecting your business today.

.svg)

.svg)

.svg)

.svg)