When a customer disputes a charge on their credit card, it kicks off a formal process that can feel confusing and, frankly, a little unfair. It’s designed as a safety net for consumers, giving them a way to challenge a transaction and get their money back from their bank.

This process, better known as a chargeback, is a complex dance between the customer's bank, your bank, and you, the merchant—all to figure out if a charge was legitimate. For any business accepting cards, getting a handle on this journey is step one in protecting your bottom line.

What Is the Credit Card Dispute Process?

If you've ever been blindsided by a chargeback notice, you're not alone. It's easy to think of it as just a simple refund, but it's much more than that.

The best way to think about the credit card dispute process is as a formal, multi-step conversation between banks. It’s a conversation your customer started, and it puts your money right in the middle of it all.

This system was originally created to make people feel safe using credit cards. It gave them protection against outright fraud or from merchants who didn't hold up their end of the bargain. While that’s still the goal, the boom in e-commerce has made things a lot trickier for businesses. A simple customer complaint can now trigger a formal financial dispute that yanks funds directly from your account before you even get a chance to tell your side of the story.

The Key Players in Every Dispute

To fight a dispute and win, you first need to know who you're dealing with. Each player has a specific and crucial role in how things shake out.

- The Cardholder: This is your customer. They made the purchase and are now telling their bank something is wrong with the charge.

- The Issuing Bank: This is the cardholder’s bank (think Chase, Bank of America, Capital One). They’re the ones who issued the credit card, and they are the customer's first point of contact. Their main job here is to protect their customer.

- The Acquiring Bank: This is your bank, sometimes called the merchant bank. They give you the merchant account you need to take card payments. Their job is to act as the middleman between you and the issuing bank.

- The Card Network: These are the big names like Visa, Mastercard, and American Express. The networks are the referees—they set the rulebook that all the banks have to follow during a dispute.

When a customer files a dispute, the issuing bank gives them a provisional credit. At the same time, they pull those funds from your acquiring bank, which then takes the money straight from your merchant account. This all happens almost instantly.

At this point, the burden of proof shifts entirely to you. You, the merchant, are now responsible for providing compelling evidence to prove the transaction was valid. This formal response process is known as representment.

Understanding these roles is everything. It explains why the money disappears so fast and why your response has to go through the right channels to even be considered. For a deeper look into how it all kicks off, you can learn more about what a bank chargeback is and the first few steps. Without this basic knowledge, you're flying blind when a dispute notice lands, and that puts your revenue at serious risk.

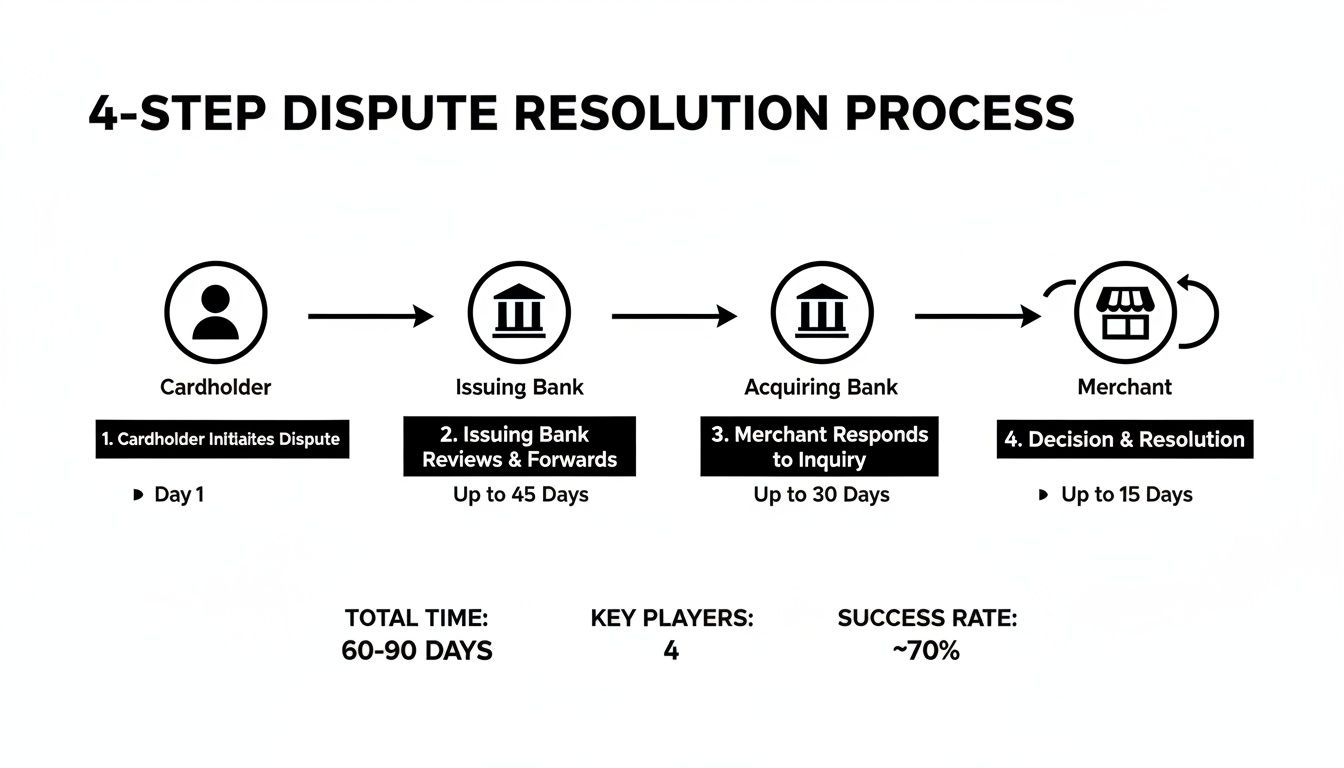

The Complete Lifecycle of a Chargeback

A chargeback isn't a single, isolated event; it's a structured journey with distinct stages and strict deadlines. Getting this lifecycle wrong is one of the fastest ways to lose a dispute by default. Think of it like a domino effect—one step directly triggers the next, and the clock is always ticking on your response time.

The whole process kicks off the moment a cardholder contacts their bank to question a charge. That single action sets in motion a formal chain of events that pulls funds directly from your account, often before you're even aware there’s a problem.

This flowchart gives you a bird's-eye view of the four main stages, showing how a single customer action ropes in their bank, your bank, and you.

As you can see, the process moves in a straight line, but it puts you, the merchant, on the defensive from the get-go. You’re left reacting to moves already made by the cardholder and the banks.

Here's a quick look at how these stages and timelines break down in practice.

Chargeback Dispute Stages and Timelines

This table summarizes the key stages in the credit card dispute process, outlining what happens at each step and the typical timeframes you'll have to act.

Understanding these windows is critical—missing a deadline means an automatic loss, no matter how strong your evidence is.

Stage 1: The Initial Dispute and First Chargeback

It all starts with the cardholder. For any number of reasons—from genuine fraud to just not recognizing a charge—they call their issuing bank to dispute a transaction. The bank takes a look at the claim and, if it seems valid under the card network's rules, files a formal chargeback.

This is what we call the "First Chargeback" stage. The issuing bank immediately gives a provisional credit back to their customer. At the same time, they claw the funds back from your acquiring bank, which then debits the money straight from your merchant account, along with a separate chargeback fee.

At this point, the money is gone from your account. You receive a notification, and the clock starts on your deadline to respond. This is your one and only chance to present your side of the story.

This reality highlights a massive pain point for merchants. Global chargeback volumes are projected to rocket up by 41% between 2023 and 2026. For e-commerce businesses, this is expected to cost the industry a staggering $33.79 billion in 2025 alone, with U.S. merchants losing an average of $4.61 for every single dollar of fraud. You can discover more insights about these chargeback stats on Chargebacks911.com.

Stage 2: Representment – Your Chance to Respond

Once you get that chargeback notification, you enter the representment stage. This is your official opportunity to "re-present" the transaction to the issuing bank, armed with compelling evidence to prove the charge was legitimate.

You'll need to pull together a rebuttal package with documents that directly counter the customer's claim. The exact evidence you need depends on the reason for the dispute, but it almost always includes things like:

- Proof of delivery, such as shipping confirmations or tracking numbers.

- Order details and any records of customer communication.

- AVS and CVV match results from the original transaction.

- IP address logs and device information for online orders.

Your acquiring bank reviews your evidence package before passing it along to the issuing bank. Timeliness is everything here; response windows are typically between 20 and 45 days, and they vary by card network. If you want to dive deeper into the specific rules, our guide on the Visa chargeback process is a great place to start.

Stage 3: The Issuer's Decision

After your evidence is submitted, the issuing bank plays judge. They weigh your documentation against the cardholder’s original claim and make the final call. There are only two ways it can go:

- Dispute Reversed (You Win): If your evidence is solid, the bank reverses the chargeback. The funds are returned to your merchant account, but you usually have to eat the cost of that initial chargeback fee.

- Dispute Upheld (You Lose): If the bank decides your evidence isn't strong enough or sides with the cardholder, the chargeback stands. The provisional credit they gave the customer becomes permanent, and for you, the case is closed.

Stage 4: Escalation to Arbitration

What if you lose at representment but are absolutely certain the chargeback is bogus? You have one last, final option: arbitration. This is where you appeal the decision directly to the card network (like Visa or Mastercard) to act as the ultimate referee.

Be warned, though: arbitration is an expensive, high-stakes gamble. Both you and the issuing bank have to pay hefty fees just to enter the ring, and the loser is on the hook for all of them—we’re talking hundreds of dollars. Because of the steep costs and low success rates for merchants, this move is typically reserved for very high-value disputes where the evidence is absolutely airtight.

Why Customers File Disputes in the First Place

To stop disputes from happening, you first have to get inside your customer's head. It’s tempting to write off every chargeback as a case of blatant fraud, but the reality is usually a lot more nuanced. Most disputes actually fall into just a handful of categories, and each one needs a different approach.

Think of it like being a detective at a crime scene. You can't just assume what happened; you have to look for clues. Pinpointing the root cause of a dispute helps you find the weak spots in your own process—the leaky pipes in your business—and patch them up for good.

The Three Main Reasons for Disputes

While the banks have dozens of specific "reason codes" they can assign to a chargeback, almost every single one boils down to one of three core problems: true fraud, merchant error, or friendly fraud. Knowing the difference is everything when it comes to building a defense that actually works.

True Fraud: This one is exactly what it sounds like. A criminal gets their hands on a legitimate cardholder's details and goes on a shopping spree. In this case, both you and the customer are victims of a crime, and the cardholder is completely justified in disputing the charge. Fighting these is a losing battle because the real customer never authorized the purchase.

Merchant Error: This category covers any slip-ups on your end. Maybe you accidentally double-billed a customer for a subscription, sent the wrong size shirt, or your return policy was buried in fine print. These are painful, but the good news is they are entirely preventable with better internal processes and clearer communication.

Friendly Fraud: Here’s where things get tricky. Friendly fraud is the most frustrating—and fastest-growing—type of dispute. It’s when a customer disputes a legitimate charge that they or someone in their household actually made. It's not always malicious; sometimes it’s just a case of forgetfulness, confusion, or even convenience.

The rise of friendly fraud shows a massive shift in how people handle transaction problems. They now see their bank as the quickest, easiest way to get their money back, often skipping the merchant entirely.

This isn't just a hunch; the data backs it up. Consumers are prioritizing convenience over everything else. A recent study found that a jaw-dropping 76% of cardholders would rather go straight to their bank to dispute a charge than contact the merchant first. What's more, nearly half of them admit they don't even bother reaching out. You can dig into these findings from the 2025 Cardholder Dispute Index on Financial IT.

Common Triggers for Friendly Fraud

Since friendly fraud is where you can make the biggest impact, let's zoom in on what sets it off. A classic trigger is an unclear billing descriptor. A customer scans their credit card statement and sees a charge from "SP*WEBSERVICES" instead of "Your Awesome Brand Name," assumes it's fraud, and immediately calls their bank.

Another common scenario involves family members. A teenager makes an in-app purchase on their parent's phone, or a spouse orders something from a new online store. The cardholder sees the charge, doesn't recognize it, and files a dispute without a second thought. Our guide on the top reasons for a chargeback breaks down even more of these situations.

By simply addressing these small points of confusion, you can eliminate a huge chunk of disputes before they ever happen.

When a chargeback notice lands in your inbox, it feels less like a customer service issue and more like an accusation. You've got one shot—and one shot only—to prove the transaction was legitimate and get your money back. This is called representment, and it's all about building an airtight, evidence-backed case.

Think of yourself as a detective. Your job is to assemble all the clues from the original purchase and present them in a way that tells a clear, undeniable story. The bank reviewing your case wasn't there; they only have the customer's version of events. Your representment package is your opportunity to give them yours.

The key is realizing that a one-size-fits-all approach just doesn’t cut it. The evidence you submit has to directly counter why the customer filed the dispute in the first place. You have to tailor your response to the specific claim.

Matching Your Evidence to the Dispute Reason

Let’s get practical. If a customer claims they never received their order, an invoice is useless. It proves they bought something, not that it arrived. You need to provide evidence that directly addresses their "product not received" claim.

Here’s a quick reference guide for lining up your evidence with the most common dispute types.

Essential Evidence by Dispute Type

The type of proof you need changes dramatically depending on the customer's claim. Submitting irrelevant documents just creates noise and weakens your case. This table breaks down what you should focus on for the most common chargeback reasons.

This targeted approach shows the bank you’ve done your homework. It immediately makes your case more compelling because you're directly refuting the claim with hard data, not just generic transaction info.

Your Essential Evidence Checklist

No matter the specific reason, some documents are just fundamental to building a solid case. Think of these as the foundation of your argument. Without them, even the strongest claim can fall flat.

Your representment package should always aim to include:

- Order and Transaction Details: The invoice showing what was purchased, the amount, the date, and the time.

- Authorization Data: AVS (Address Verification Service) and CVV results are critical. They show you took steps to verify the cardholder at checkout.

- IP Address Logs: The IP address where the order was placed, which can often be matched to the cardholder’s billing address location.

- Customer Communications: Any emails, chat logs, or support tickets between you and the customer. This is gold for proving they were happy with the purchase or acknowledged receiving it.

- Proof of Delivery: For physical goods, this is non-negotiable. A tracking number from a reputable carrier showing the item was delivered to the correct address is often the single most powerful piece of evidence you can provide.

The goal isn't just to dump a folder of documents on the bank. It's to construct a narrative that leaves no room for doubt. Each piece of evidence should add another layer to your story, proving the transaction was valid, authorized, and fulfilled as promised.

Crafting the Rebuttal Letter

All this powerful evidence needs a cover sheet to tie it all together: the rebuttal letter. This letter summarizes your case, explains the attached evidence, and directly refutes the customer’s claim in a few concise paragraphs. If you're not sure where to start, you can find guidance on how to structure an example of a rebuttal letter to make sure you hit all the key points.

A well-organized representment package dramatically increases your chances of winning back your revenue. It tells the bank you're a diligent merchant who takes this process seriously, which helps build credibility for this case and any future ones.

The True Cost of a Chargeback on Your Business

When a chargeback notification lands in your inbox, your eyes probably go straight to the lost sale amount. A $50 order? Okay, you think, I'm out $50. But that's just the tip of the iceberg. The real financial damage runs much, much deeper and can quietly bleed your business dry.

First, the original transaction amount is yanked from your account. No surprise there. But the hits keep coming. You also lose the non-refundable processing fees you paid just to make that sale happen in the first place.

Then, your payment processor slaps you with a separate chargeback fee. This penalty can range anywhere from $15 to $100 per dispute, and you're on the hook for it whether you win or lose. All of a sudden, that $50 loss is pushing $75 or more, wiping out the profit margin on that sale and maybe a few others, too.

Beyond the Direct Financial Hit

The costs don't stop with the transaction itself. The true cost of a chargeback is a nasty cocktail of the disputed amount, administrative fees, and the operational resources you pour into fighting it. For instance, data from the U.S. shows the average chargeback is now valued at $110—a figure that truly reflects this layered financial impact. You can read the full analysis in Mastercard's 2025 report.

This brings us to the hidden operational costs—the time and energy your team spends fighting back. Think about it: every hour spent digging through order histories, pulling shipping confirmations, and writing rebuttal letters is an hour not spent on what really matters.

Every minute your team spends on a dispute is a minute they aren't spending on growing your business, improving your products, or helping legitimate customers. This operational drain is a silent killer of productivity and focus.

Imagine just one employee spending five hours a week managing disputes. That adds up to over 250 hours a year dedicated solely to damage control instead of growth.

The Long-Term Risk to Your Merchant Account

Maybe the scariest cost of all is the long-term threat to your business’s very survival. Every single chargeback you get—win or lose—counts against your chargeback ratio. This is the percentage of your total transactions that end up as a dispute.

Card networks like Visa and Mastercard watch this ratio like hawks. If it starts creeping above their threshold (usually around 0.9%), you’re heading for serious trouble.

- You could land in a monitoring program. These programs come with hefty monthly fines and intense scrutiny of your business practices.

- Your processing fees might skyrocket. To an acquirer, a high chargeback ratio screams "risk," and they'll hike your rates to protect themselves.

- You could lose your merchant account entirely. In the worst-case scenario, your payment processor will simply cut you off, making it nearly impossible to accept credit card payments at all.

This is what makes every single chargeback, no matter how small, a direct threat. The cost isn't just one lost sale; it's a cumulative risk that can jeopardize your entire operation.

Automating Your Defense To Recover More Revenue

Trying to fight every chargeback by hand is like bailing water from a sinking boat with a coffee mug. It's slow, exhausting, and you're still going to sink. Manual responses simply can't keep up, and that means leaving a ton of your money on the table. Automation completely changes the game by taking all those repetitive, time-sucking tasks off your plate.

Imagine your system plugs directly into your Shopify, Stripe, or PayPal accounts. With ChargePay, it does just that, instantly pulling all the transaction details and customer interactions the moment a dispute hits. Your team no longer has to spend hours digging through old emails or shipping logs. Instead, the platform serves up exactly what you need to build a rock-solid representment case.

Manual dispute handling creates a few major problems:

- Sifting through hundreds of orders to find proof points can burn entire days. This bottleneck often leads to rushed, incomplete, or weak responses.

- The pressure of tight deadlines means you can easily miss the window to respond, resulting in an automatic loss. That's pure revenue down the drain.

- When your rebuttal quality is all over the place, your credibility with issuing banks takes a hit, which can lower your win rates over the long term.

How Automation Fits Into Your Workflow

The right automation tool works quietly in the background, grabbing customer data, order history, and payment logs at lightning speed. No more switching between five different apps to piece together a defense. You get one unified dashboard where every piece of evidence is organized and ready to go. It feels like having a dedicated disputes team on call 24/7.

It's a simple, three-step flow:

- Sync and Scan

It all starts by automatically connecting to your payment processor and storefront. The system harvests all the relevant records as soon as a dispute is filed. - Analyze and Assemble

Next, AI kicks in to categorize the dispute by its reason code and cherry-picks the strongest evidence for that specific claim. - Draft and Deliver

Finally, it generates a customized, professional rebuttal letter in seconds and submits it directly to your acquiring bank on your behalf.

"ChargePay customers see up to 3.5× higher win rates and recover as much as 80% of lost revenue—without lifting a finger."

Benefits You Can Actually Track

Switching to an automated defense does a lot more than just save time. It lets you shift your focus from constantly fighting fires to actually optimizing your revenue recovery strategy. Best of all, you get real-time insights into how you're performing.

- Win Rate Improvement: Watch your monthly chargeback outcomes and see a consistent upward trend.

- Revenue Recovered: Monitor the exact dollar amount of funds returned to your account, often reaching 75-80% of what would have been lost.

- Team Efficiency: See the hours your team gets back and reassign them to high-impact tasks like customer support or marketing.

You can learn more about building a smoother dispute process in our complete guide to automated chargeback and dispute management using AI.

To take your dispute resolution efforts even further, consider integrating automated support tools like SupportGPT designed to help manage customer interactions and build stronger chargeback defenses from the start.

By automating evidence collection, analysis, and response generation, you turn your credit card disputes process from a cost center into a growth engine. The right tools don’t just recover lost revenue; they also strengthen your brand’s reputation with banks and customers. It's the smartest way to keep your business thriving.

ChargePay’s transparent pay-per-success model means you only pay when you win.

There are no upfront fees, making it a no-brainer for businesses of all sizes.

And getting started takes minutes, not weeks, so you can skip the implementation headaches.

Start automating today.

Got Questions About Credit Card Disputes? We've Got Answers.

When you're running a business, chargebacks can feel like a complicated mess. Let's clear up some of the most common questions merchants have so you can get a better handle on the whole process.

How Long Do I Have to Respond to a Credit Card Dispute?

You've got a limited window to fight back, and it's called the representment period. This isn't a one-size-fits-all timeline; it changes depending on the card network, but you're typically looking at 20 to 45 days.

Honestly, you need to act fast. If you let that deadline slip by, you automatically lose the dispute. The money's gone, and there's no getting it back. This is exactly why automation is such a game-changer—it ensures you never miss a deadline by getting your response in almost immediately.

What Is a Chargeback Ratio and Why Does It Matter?

Think of your chargeback ratio as a key health metric for your business. It’s pretty simple: it’s the number of chargebacks you get in a month divided by your total transactions for that same month.

Card networks like Visa and Mastercard watch this number like a hawk. If your ratio starts creeping over their threshold—which is usually around 0.9%—you're going to set off some serious alarms. Going over the limit can mean hefty fines, higher processing fees, or even losing your merchant account entirely. That could literally shut down your ability to sell online.

Your chargeback ratio is like a credit score for your business. Keeping it low shows payment processors and banks that you're a reliable, low-risk merchant they want to work with.

Can I Prevent Friendly Fraud?

You can't eliminate it completely, but you can absolutely cut it down. A lot of friendly fraud isn't malicious—it's just a customer who's confused. Your best defense? Total clarity.

Here are a few tactics that work wonders:

- Use Clear Billing Descriptors: Make sure the name on your customer's credit card statement is one they'll actually recognize. "Awesome Brand" is a million times better than a cryptic "AB*WEBSERVICES."

- Offer Top-Notch Customer Service: Make it dead simple for customers to get in touch with you. A prominent phone number or a live chat bubble can steer them toward your support team instead of their bank.

- Send Detailed Confirmations: Pack your order and shipping confirmation emails with clear details. It reassures the customer that their purchase is legitimate and on its way.

Is It Worth Fighting Small-Dollar Chargebacks?

Yes, absolutely. It might feel like a waste of time fighting over a $20 dispute, but you have to look at the bigger picture.

Fighting every single illegitimate chargeback accomplishes two huge things. First, it helps keep your chargeback ratio in a healthy range, protecting your merchant account from penalties. Second, it sends a clear signal to the banks that you're a diligent merchant who keeps careful track of every transaction. This is where automated tools really prove their worth, making it easy and cost-effective to fight every dispute, no matter how small.

Stop losing revenue to tedious manual disputes. ChargePay uses AI to automate the entire credit card disputes process, recovering up to 80% of your lost revenue for you. Start winning more chargebacks today.

.svg)

.svg)

.svg)

.svg)