High-risk credit card processing is a special service for businesses that payment processors see as having a higher chance of chargebacks or fraud. Getting this label isn't a judgment on how good your business is—it's a financial risk assessment based on your industry, how you sell, or your past processing history. Because of this, you’ll face stricter terms and higher fees than standard merchants.

What It Really Means to Be a High Risk Merchant

Being labeled 'high risk' can feel like a penalty, but what does it actually mean for your day-to-day operations? It’s not just about paying a little extra. It fundamentally changes how payment providers view and interact with your business.

Think of it this way: a payment processor is a bit like a bank evaluating someone for a loan. A borrower with a steady, predictable job and a long credit history is a safe bet—low-risk. But a freelance artist with a fluctuating income? That’s more of an unknown. The bank might still offer them a loan, but they'll almost certainly charge a higher interest rate to protect their investment.

High Risk vs. Low Risk Merchants at a Glance

This table breaks down the key differences you'll run into. It’s a quick snapshot of why the two account types are treated so differently.

As you can see, running a high-risk account involves more oversight and higher costs, all designed to lessen the processor's risk.

Why You Face Tougher Terms

Processors see high-risk merchants through this same lens. Your business model—maybe you rely on recurring billing, sell high-ticket items, or operate in a heavily regulated industry—presents a greater financial risk to them, mostly from chargebacks.

A chargeback is a transaction reversal kicked off by a customer's bank. For processors, every single one means lost revenue, administrative headaches, and potential fines from card networks like Visa and Mastercard.

Because of this heightened risk, processors put safeguards in place that directly affect you:

- Higher Processing Fees: This is the most obvious one. Your transaction rates will be noticeably higher to compensate the processor for taking on more risk.

- Stricter Account Monitoring: Expect every transaction to be under a microscope. Processors will be watching carefully for any signs of fraud or unusual activity.

- Rolling Reserves: The processor might hold back a percentage of your revenue (typically 5-10%) in a non-interest-bearing account. This acts as their financial cushion against future chargebacks.

Trying to navigate this world can be incredibly frustrating, especially when your main focus is just growing your business. The constant threat of an account hold or sudden termination only adds to the stress.

But, as you’ll learn in our deep dive on what makes a merchant high risk, this label isn't a dead end. Not even close. With the right knowledge and strategies, you can manage these challenges and build a stable, profitable operation. This guide will give you the practical steps to do exactly that.

Why Your Business Was Flagged as High Risk

Getting slapped with a "high-risk" label can feel personal, but it’s rarely a random judgment call. Payment processors and their banking partners aren't trying to critique your business model; they're running a risk calculation. At the end of the day, it's all about protecting themselves from financial loss.

To get out of the high-risk category (or at least manage it), you first have to understand their perspective. The reasons you’ve been flagged almost always boil down to two things: the industry you're in or the way your specific business operates.

Industry-Wide Risk Factors

Some industries are automatically viewed with a bit more caution. It has nothing to do with you personally and everything to do with historical data from thousands of businesses just like yours. From a processor's point of view, these sectors are simply more likely to generate customer disputes, fraud, and chargebacks.

Here are a few of the usual suspects that raise an immediate flag:

- Subscription and Recurring Billing: Think SaaS products or monthly subscription boxes. The risk here is that customers forget they signed up, lose interest, or don't feel they’re getting their money's worth. This often leads to "friendly fraud," where a legitimate customer disputes a charge they simply don't recognize or no longer want.

- High-Ticket Sales: Selling expensive items like jewelry, electronics, or furniture is inherently riskier. A single chargeback on a $3,000 sofa is a much bigger financial blow to the processor than one on a $30 t-shirt.

- Highly Regulated Industries: If you're in a business like CBD, supplements, travel, or adult entertainment, you’re navigating a minefield of legal and regulatory scrutiny. Rules can change overnight, making your venture seem unstable in the eyes of a cautious processor.

If you operate in one of these spaces, you're likely starting with a high-risk label right out of the gate. But your industry is only part of the story.

Business-Specific Red Flags

Even if you’re in a "safe" industry, your own operational track record can land you in the high-risk bucket. This is where processors put your business practices and financial health under a microscope to see how you run things day-to-day.

It’s a lot like your personal credit score—your past behavior predicts your future reliability. For merchants, your processing history serves the same purpose. To really get into the weeds on how these financial institutions think, our guide on what is an acquiring bank breaks down how they assess and manage risk.

The most common operational triggers include:

- High Chargeback Ratio: This is the big one. If more than 1% of your transactions consistently end up as chargebacks, you're almost guaranteed to be classified as high-risk. It’s a massive red flag that signals potential issues with your product, customer service, or fraud prevention.

- Poor Personal Credit of the Owner: For new businesses without much of a processing history, underwriters will often pull the owner's personal credit score. A low score can suggest financial instability, which makes the processor nervous about taking you on.

- International Sales Volume: Selling to customers in countries known for higher rates of e-commerce fraud automatically dials up your risk profile. Processors pay close attention to geographic data when predicting the likelihood of fraudulent payments.

A processor's main goal is to avoid financial loss. Every red flag, whether it’s your industry or your chargeback rate, is seen as a potential threat to their bottom line.

Getting a handle on your business's financial health, sometimes with the help of a Credit Repair Executive Assistant, is key to addressing the core problems that get you flagged. Once you know whether the risk is coming from your industry or your operations, you can build a smart strategy to improve your standing and secure better processing terms.

The True Financial Impact of a High-Risk Label

Getting slapped with a "high-risk" label isn't just a bit of administrative paperwork. It’s a constant, significant financial drag on your business. We're not talking about a few extra cents per transaction, either. This label triggers a chain reaction of costly consequences that directly eat into your profitability, choke your cash flow, and can even threaten your ability to operate at all.

Let’s pull back the curtain on the real-world costs. The gap between standard and high-risk processing isn't a small step—it's a chasm. Getting a handle on these financial pressures is the first, most critical step toward getting them under control.

Sharply Higher Processing Fees

The first and most immediate hit comes straight to your bottom line: processing fees. While a low-risk merchant might be paying around 2.9% + 30¢ for a typical transaction, a high-risk business can easily see rates jump to 4% to 6%, and sometimes even higher. On paper, a couple of percentage points might not seem like a big deal, but it adds up frighteningly fast.

Let's say your e-commerce store is pulling in $50,000 in monthly sales.

- Low-Risk Scenario: At a 2.9% rate, you’d pay $1,450 in processing fees.

- High-Risk Scenario: At a 5% rate, that fee skyrockets to $2,500.

That’s an extra $1,050 disappearing from your revenue every single month. Over a year, you're looking at $12,600 gone. This isn't just another business expense; it's a direct erosion of your hard-earned profit, all because of that high-risk label. You're then forced into a tough spot: either raise your prices and risk losing customers or just live with thinner margins.

The Cash Flow Squeeze of Rolling Reserves

On top of the higher fees, processors have another tool to shield themselves: the rolling reserve. For many business owners, this is one of the most frustrating parts of high-risk credit card processing to deal with. A rolling reserve is basically a forced savings account that your processor controls, not you.

Here’s how it works: the processor withholds a percentage of your daily sales—usually 5-10%—for a set period, often around 180 days. The money isn't gone for good, but it's completely locked away from you. It acts as the processor’s insurance policy against any future chargebacks you might get.

Think of it like a security deposit for an apartment. You’ll probably get it back down the road—assuming no issues—but you absolutely can’t use it to pay this month’s rent. It directly handcuffs your ability to buy inventory, make payroll, or fund a marketing campaign.

If your business brings in $50,000 a month and your processor slaps a 10% rolling reserve on you for six months, that’s $5,000 of your own money being held back every single month. After half a year, a jaw-dropping $30,000 of your revenue is sitting in limbo, severely restricting your operational cash flow.

The High Cost of Intense Chargeback Scrutiny

Chargebacks are a headache for any merchant. But for a high-risk business, they’re a five-alarm fire. Processors watch your chargeback ratio—the percentage of transactions disputed by customers—like a hawk. Even a small spike can unleash devastating consequences.

The pressure is immense because the stakes are incredibly high. Global chargeback volumes are projected to climb by 24%, jumping from 261 million in 2025 to a massive 324 million by 2028. This surge is expected to drive a 23% increase in financial losses for businesses, from $33.79 billion to $41.69 billion. With 13% of merchants already seeing chargebacks consume over 2% of their total volume, the financial strain is only getting worse.

When a processor decides your chargeback ratio is too high, they can take a few different actions:

- Account Freezes: They can instantly lock your account, cutting off access to all your funds while they conduct a review.

- Increased Reserves: They might hike up your rolling reserve percentage, putting an even tighter squeeze on your cash flow.

- Account Termination: This is the ultimate nightmare scenario. If they terminate your account, you’re left scrambling to find a new processor, which could shut down your ability to accept payments for days or even weeks.

And don't forget, every single chargeback comes with its own penalty fee, typically ranging from $25 to $100 per dispute, which you have to pay whether you win or lose. To get a full picture of these costs, our article on what is a chargeback fee breaks it all down. The financial fallout isn’t just a theoretical risk—it's a daily reality that makes managing high-risk credit card processing an absolute necessity for survival.

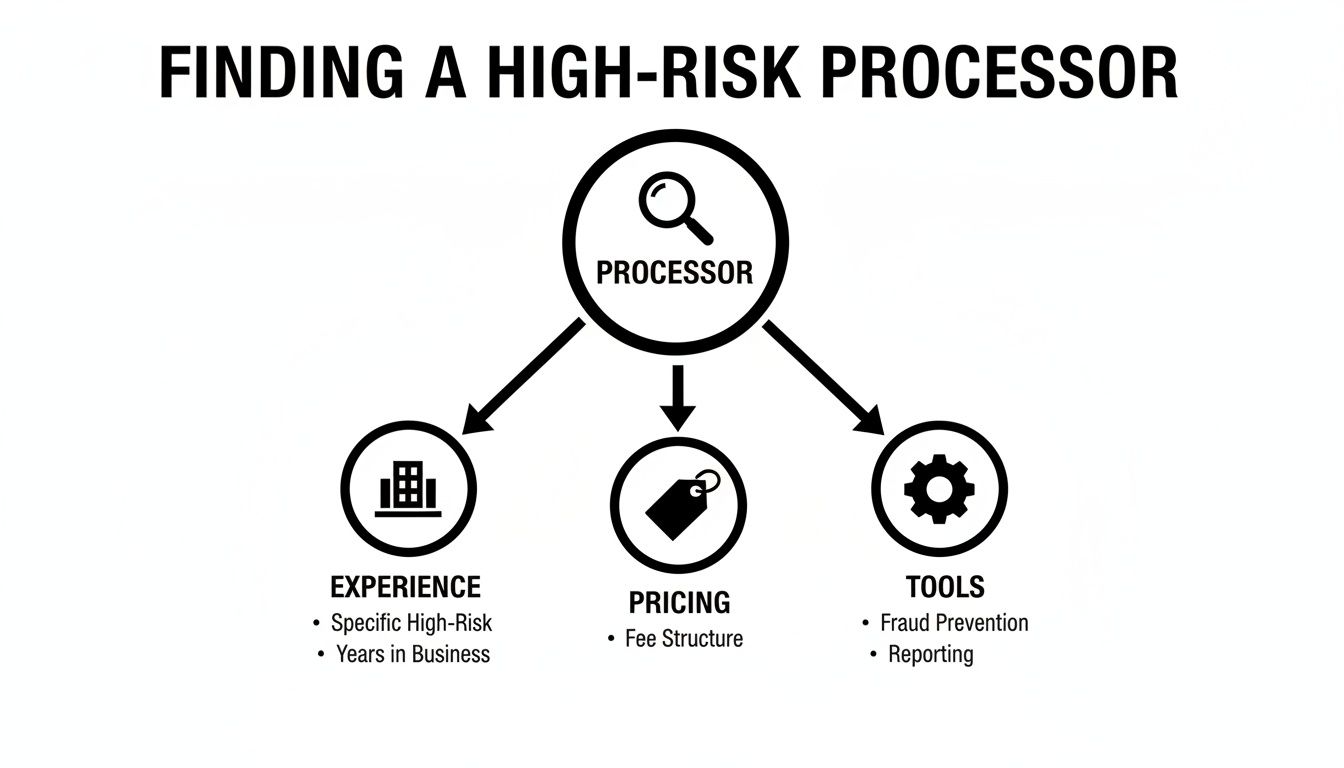

How to Find the Right High Risk Payment Processor

Choosing a partner for your high-risk credit card processing is one of the most critical decisions you'll make for your business. This isn't like picking any old service provider; you absolutely need a specialist who sees your business as an opportunity, not just a liability to be managed. Get this wrong, and you're looking at frozen funds, sudden account terminations, and a whole lot of stress you don't need.

The real goal is to find a processor that genuinely gets the quirks and challenges of your specific industry. It means you have to look past the flashy advertised rates and start digging into what they actually bring to the table.

Look for Proven Industry Experience

Your first, and most important, filter should always be industry specialization. A processor whose bread and butter is low-risk corner stores simply won't have the right experience or, crucially, the right banking relationships to support something like a CBD e-commerce shop or a subscription box service. Sure, they might approve you at first, but they're far more likely to hit the panic button and freeze your account at the first sign of trouble.

You need a partner who can confidently say "yes" to these questions:

- Do you have a solid portfolio of clients in my specific niche?

- Do you understand the common chargeback triggers and fraud patterns we're up against?

- Are your acquiring bank relationships solid and comfortable with our business model?

A processor with deep roots in your niche will offer better advice, a more stable account, and a much, much lower risk of getting shut down.

Demand Transparent Pricing and Fair Terms

Yes, high-risk processing costs more than a standard account—that's a given. But that doesn't mean you should have to put up with confusing or predatory pricing. Hidden fees, vague contract clauses, and inflexible terms are huge red flags. Any processor worth your time should be completely upfront about every single cost involved.

When you're comparing your options, make sure you get written answers to these key questions:

- What is the complete fee structure? Ask for a full rundown of transaction rates, monthly fees, PCI compliance costs, and any other charges they have.

- What are your reserve policies? You need to know if they require a rolling reserve, what that percentage is, and exactly how long they plan on holding your money.

- What are the contract terms? Aim for month-to-month agreements. Try to steer clear of long-term contracts saddled with massive early termination fees.

Honest, clear answers are the hallmark of a processor you can trust. If they're cagey or give you the runaround, it’s time to walk away.

Prioritize Powerful Fraud and Chargeback Tools

A top-tier high-risk processor does more than just move money around; they actively help you protect your revenue. Since your chargeback ratio is under a microscope, the tech they provide is incredibly important. You need a partner who offers sophisticated tools to stop fraud before it starts and to effectively fight the disputes that inevitably slip through.

When vetting a processor, remember that their tools directly impact your bottom line. Weak fraud prevention means more chargebacks, which puts your entire merchant account at risk.

Your processor should provide a layered defense system, including robust fraud filters, AVS/CVV checks, and full support for 3D Secure 2.0. Even better are the providers who integrate seamlessly with dedicated chargeback automation platforms. Having a deeper grasp of fintech payment integration strategies can really help you size up a processor's technical muscle.

Finding the right processor is an investment in your business’s stability and future. For a more detailed walkthrough, check out our complete guide on securing a high risk merchant account. By asking the right questions and prioritizing experience, transparency, and technology, you can find a true partner who will help you thrive.

Smart Strategies to Lower Your Risk and Fight Chargebacks

Getting slapped with a high-risk label isn't a death sentence for your business. Far from it. Think of it as a signal to get proactive. Instead of just reacting to problems, it’s time to build a smart defense that protects your revenue, brings down your fees over time, and shows your payment processor you’re a partner they can trust.

It all comes down to a layered approach—one that stops criminals in their tracks but also heads off those frustrating disputes from legitimate (but confused) customers. Your goal is to prove you're a diligent merchant who takes fraud and chargebacks seriously.

Choosing the right processor is half the battle. You need a partner who understands your industry and gives you the tools to succeed.

A great high-risk processor does more than just move money. They equip you with the specialized tools and insider knowledge to actively manage and reduce your risk profile.

Fortifying Your First Line of Defense

First things first: you have to lock down the basics. Your top priority should be implementing fundamental fraud prevention checks right at the point of sale. These are the non-negotiables for any online business, especially if you're in a high-risk category.

Think of these tools as the locks on your front door. They won't stop a determined thief, but they’ll definitely deter the casual opportunist.

Your foundational security toolkit must include:

- Address Verification Service (AVS): This is a simple but powerful check. It confirms whether the billing address the customer entered matches what the card-issuing bank has on file. A mismatch is a classic red flag for a stolen card.

- Card Verification Value (CVV): You know that three or four-digit code on the back of a credit card? Requiring it proves the customer physically has the card, since that number isn't stored on the magnetic stripe.

- 3D Secure (e.g., Visa Secure, Mastercard Identity Check): This is a huge one. It adds an extra authentication step where the customer has to verify their identity directly with their bank, usually with a one-time code sent to their phone. It’s a game-changer for shifting fraud liability away from you and back to the issuing bank.

Putting these three tools in place creates a solid security baseline. It sends a clear message to your processor that you’re actively filtering out bogus transactions before they even hit the network.

Embracing Automation to Fight Back Smarter

Manual checks are essential, but they're not enough to keep up with modern fraud. Scammers are getting more sophisticated, and "friendly fraud"—where a real customer disputes a legitimate charge—is a massive headache for merchants. This is where AI-powered automation becomes your secret weapon.

Automated systems don't just react to fraud; they predict it. By analyzing thousands of data points in real time, they can spot suspicious patterns that a human would miss, blocking high-risk transactions before they can ever become a problem.

This proactive stance is critical in high-risk industries. For example, sectors like online gaming and crypto see an average chargeback value of $99, and first-party fraud now makes up a staggering 21% of all disputes. For merchants on platforms like Shopify or PayPal, AI-driven chargeback tools can automatically build and submit dispute responses with a 3.5x higher win-rate, recovering up to 80% of what would have been lost revenue.

Your High-Risk Merchant Survival Kit

Managing risk effectively means combining tried-and-true manual practices with the power of modern automation. This checklist breaks down the essential tools and strategies you need to protect your business and keep chargebacks under control.

By blending these approaches, you create a robust defense that not only fights chargebacks but actively prevents them from happening in the first place.

Leveraging Chargeback Automation for Revenue Recovery

Beyond just blocking fraud, today's best tools can automate the entire chargeback representment process. Let’s be honest, fighting disputes manually is a soul-crushing, time-consuming task that you often lose anyway. It means digging up evidence, writing persuasive responses, and racing against tight deadlines.

Chargeback automation platforms take all that off your plate. They plug directly into your payment processor and e-commerce store, automatically gathering all the evidence needed—shipping confirmations, customer emails, IP logs—to build a rock-solid case on your behalf.

This doesn't just save you countless hours; it dramatically boosts your win rate. These systems are programmed with the ever-changing rules of the card networks, ensuring your responses are always compelling and compliant.

For a deeper dive into building a complete defense, our guide on chargeback mitigation strategies is packed with actionable advice you can start using today. By combining foundational security with intelligent automation, you can turn chargebacks from a crippling expense into a manageable cost of doing business, all while securing your revenue and proving you're a trustworthy merchant.

It's Time to Build a More Secure, Profitable Business

We’ve walked through what it really means to get slapped with a high-risk label, dug into the reasons why it happens, and laid out some powerful ways you can take back control. If you remember one thing, make it this: being called “high-risk” isn’t a life sentence for your business. It's just another challenge that you can absolutely manage and overcome with the right game plan.

The real magic happens when you stop playing defense and start playing offense. Shifting from a reactive, manual firefighting mode to a proactive, automated one is a game-changer. When you bring in tools that fight fraud and chargebacks for you, you’re not just plugging leaks in your revenue. You’re building a more stable, predictable business from the ground up and proving to your payment processor that you’re a partner they can trust.

Your Path Forward

Okay, so where do you go from here? The next step is turning all this information into action.

- Audit Your Defenses: Take an honest look at your current fraud and chargeback prevention. Are you still trying to catch everything by hand?

- Embrace Automation: Seriously look into solutions that can automate your dispute responses. It’s the single fastest way to boost your win rate and get your money back.

- Get Back to Growth: With a solid security system humming in the background, you can finally stop pouring all your energy into just surviving. You can get back to what actually matters—growing your business.

The goal here is to empower you. Armed with the right tools and knowledge, you can transform how your business operates, making it more resilient and leaving the constant stress of high-risk processing in the rearview mirror for good.

You have everything you need to build a more secure and profitable future. The strategies we've covered are a clear roadmap—not just for surviving in a tough environment, but for actually thriving in it. You can turn what feels like a major liability into a solid foundation for long-term success.

Frequently Asked Questions

Jumping into high-risk credit card processing can feel like you're left with more questions than answers. Let's clear up a few of the most common things merchants ask, so you can get a better handle on your account.

Can a Business Move from High Risk to Low Risk?

Yes, you absolutely can graduate from high-risk to low-risk status. But it’s not a switch you can flip overnight. Think of it like rebuilding your personal credit score—it takes time, consistency, and proving you're no longer a liability.

Processors need to see real, sustained evidence of stability before they'll even consider reclassifying your account. Typically, they're looking for:

- A Solid Processing History: At least six to twelve months of steady, predictable sales volume without any wild spikes or dips.

- A Super-Low Chargeback Ratio: You need to keep your chargeback rate consistently well below the 1% industry danger zone. This shows you have your operations under control.

- Serious Fraud Prevention: Prove you're not just reacting to problems but actively preventing them. Using tools like AVS, CVV checks, and 3D Secure is a must.

Once you’ve built this positive track record, you can reach out to your processor and ask for a review. They’ll dig into your account history, and if they agree the risk has dropped, you could be rewarded with much better rates and terms.

How Much More Are High Risk Processing Fees?

There's no sugarcoating it: high-risk processing fees are quite a bit higher than standard rates. A low-risk merchant might see rates around 2.9% + 30¢ per transaction, but a high-risk business should brace for fees anywhere from 4% to 7%, sometimes even higher.

The rate you get isn't just a number pulled out of a hat. It's a direct reflection of how much risk your specific business model brings to the processor.

Several things get factored into this price. Your industry, past chargeback history, how much you process per transaction, and even your personal credit history can all influence the final number. Essentially, the processor builds a custom risk profile just for you and prices your account to match.

What Is a Rolling Reserve and How Does It Work?

A rolling reserve is one of the most common—and sometimes confusing—parts of a high-risk merchant account. It’s basically a safety net for the processor. They hold back a small percentage of your revenue to cover potential losses from future chargebacks, kind of like a security deposit.

Here’s how it plays out in the real world:

- Let's say your processor sets a 10% rolling reserve on a 180-day rolling basis.

- On Monday, you bring in $1,000 in sales. The processor holds onto $100 (10%) and sends the remaining $900 to your bank account.

- This happens every single day. After 180 days, that first $100 held from day one is finally released back to you, while the reserve from today's sales is held.

This creates a continuous, or "rolling," fund the processor can dip into if a wave of chargebacks hits your account. It can definitely affect your cash flow, but it's a standard practice in credit card processing high risk. Getting your head around these mechanics is essential, especially as e-commerce fraud keeps climbing. In 2025, the retail e-commerce world saw a jaw-dropping 233% surge in chargeback volumes. For U.S. merchants, that translates to losing an estimated $4.61 for every $1 in chargebacks, making this kind of risk management totally non-negotiable. Learn more about the impact of rising chargebacks on retail.

Tired of losing revenue to chargebacks? ChargePay uses AI to automatically fight and win disputes for you, recovering up to 80% of lost funds without any manual work. Protect your profits and automate your chargeback management today at ChargePay.

.svg)

.svg)

.svg)

.svg)