Think of an acquiring bank as your business’s financial wingman. This is the institution that handles all the credit and debit card payments your customers make, making sure the money from a sale actually lands safely in your bank account.

They’re the ones who give you a merchant account, which is the special key you need to unlock the ability to accept card payments in the first place.

Your Business Partner in Payments

Every time a customer hits "buy" on your website, a whole flurry of activity kicks off behind the scenes—all in a matter of seconds. The acquiring bank, sometimes called an acquirer or merchant bank, is the star of that show, working entirely on your behalf as the merchant.

Let's say you run a popular online coffee shop. A customer orders a bag of your signature espresso blend and enters their card details. It's your acquiring bank that grabs that payment information, securely sends it through the system to get the green light, and ultimately brings the money home to you. Its loyalty is to your business, not the customer.

This role is absolutely essential to how we shop today. To give you an idea of the scale, the global payments industry was projected to handle around 3.6 trillion card transactions in 2025. That mind-boggling number is only possible because of the quiet, consistent work of acquiring banks.

The Core Jobs of an Acquiring Bank

So, what does your acquiring bank really do for you on a daily basis? It boils down to a few critical jobs:

- Giving You a Merchant Account: This is the special bank account that’s set up to receive funds from card transactions. No merchant account, no card payments. Simple as that.

- Connecting You to Card Networks: The acquirer is your official link to the big players like Visa, Mastercard, and American Express. It’s what lets you route a transaction request to the right place for approval.

- Handling the Money (Settlement): Once a purchase is approved, the acquirer is responsible for pulling the funds from the customer’s bank and depositing them into your merchant account.

It's easy to get the players in the payment world mixed up. An acquirer is different from a payment processor, which is more focused on the technical side of securely transmitting the transaction data. While they work hand-in-hand, their roles are distinct. To get a clearer picture, check out our detailed guide on payment processors vs. acquiring banks.

Tracing a Single Card Payment from Start to Finish

Ever wondered what really happens in the few seconds between a customer clicking "Buy Now" and getting that satisfying order confirmation? It’s not magic. It’s a high-speed data relay race involving a whole cast of characters, and your acquiring bank is right in the thick of it.

Let's follow the money—or at least, the data that represents it—on a typical online purchase. Imagine a customer finds the perfect pair of sneakers on your e-commerce store, enters their card details, and hits submit. That click kicks off a carefully choreographed journey for their payment information.

The whole process breaks down into two main phases: authorization (the initial "yes or no" check) and settlement (when the money actually changes hands).

The Authorization Journey

The first leg of the trip is all about getting the green light. It’s a rapid-fire security check to confirm the customer is legit and has the funds to cover the purchase.

Payment Gateway: First up, your website's payment gateway snags the customer's card info, encrypts it for safety, and securely hands it off to your acquiring bank.

Acquiring Bank: Your acquirer takes the handoff and immediately routes the request to the correct card network, like Visa or Mastercard. Think of it as your trusted messenger, officially kicking off the approval process.

Card Network: The card network acts like a switchboard, instantly forwarding the request to the customer's issuing bank (the bank that actually issued their credit card).

Issuing Bank: This is where the real decision happens. In a split second, the issuer runs a gauntlet of checks. Is there enough credit or funds available? Has the card been reported stolen? Does this purchase fit the customer's usual spending pattern?

The Response: The issuing bank sends back a simple approval or decline code. That message zips all the way back through the card network to your acquiring bank, which then passes the verdict to your payment gateway. Finally, your website tells the customer "Order Confirmed!" or "Payment Declined."

Believe it or not, this entire round trip usually takes less than two seconds. To really get into the weeds, check out our guide on how credit card transactions work from top to bottom.

The Settlement Process

Just because a transaction is authorized doesn't mean the cash is in your account. Not yet, anyway. That part comes later, during settlement, which usually takes a day or two.

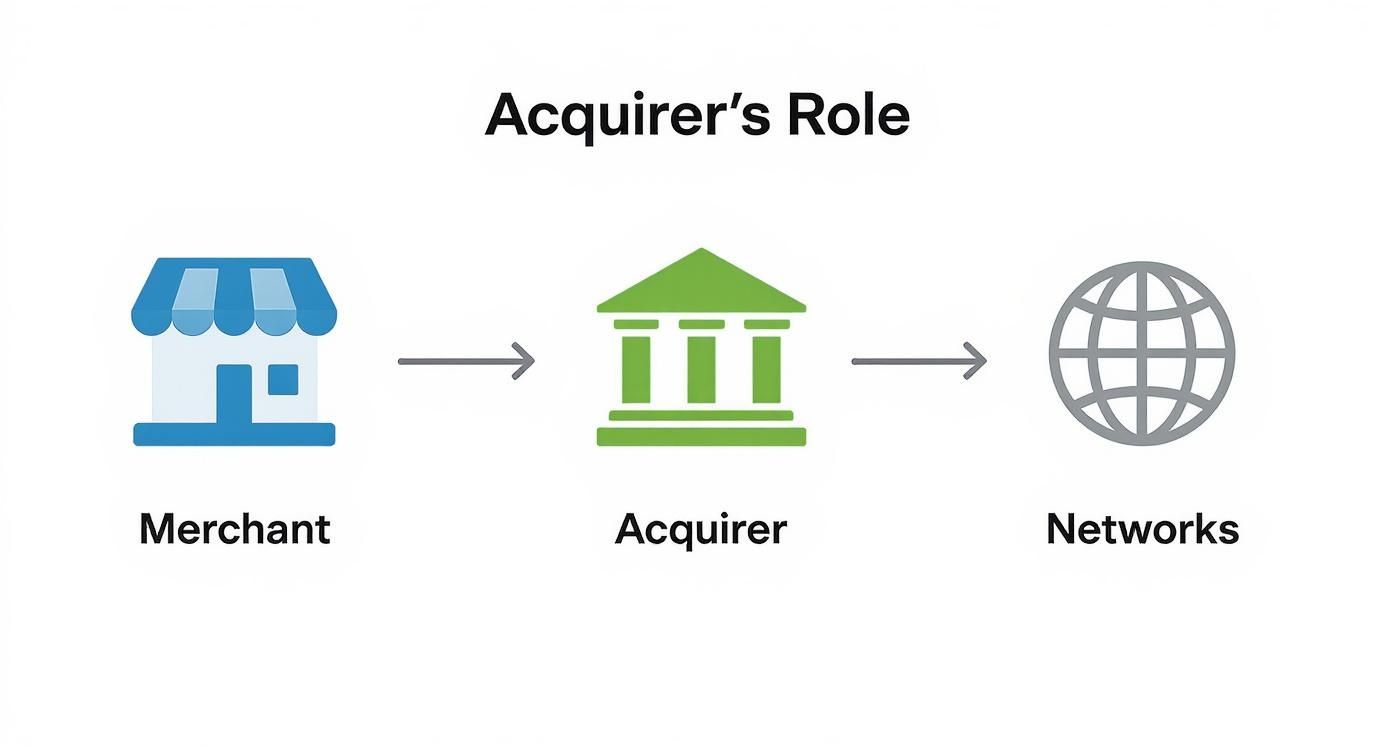

The infographic below really simplifies how your business plugs into the wider world of payments, with the acquiring bank sitting right in the middle as your essential link.

This visual drives home the point: the acquiring bank is your bridge. It connects your storefront to the massive card networks that make global e-commerce possible.

At the end of each business day, your system will send a batch of all your approved transactions to your acquirer. The acquirer then does the legwork of collecting the funds from all the different issuing banks involved and deposits one lump sum (minus their fees, of course) into your merchant account. This is when the sale is truly complete.

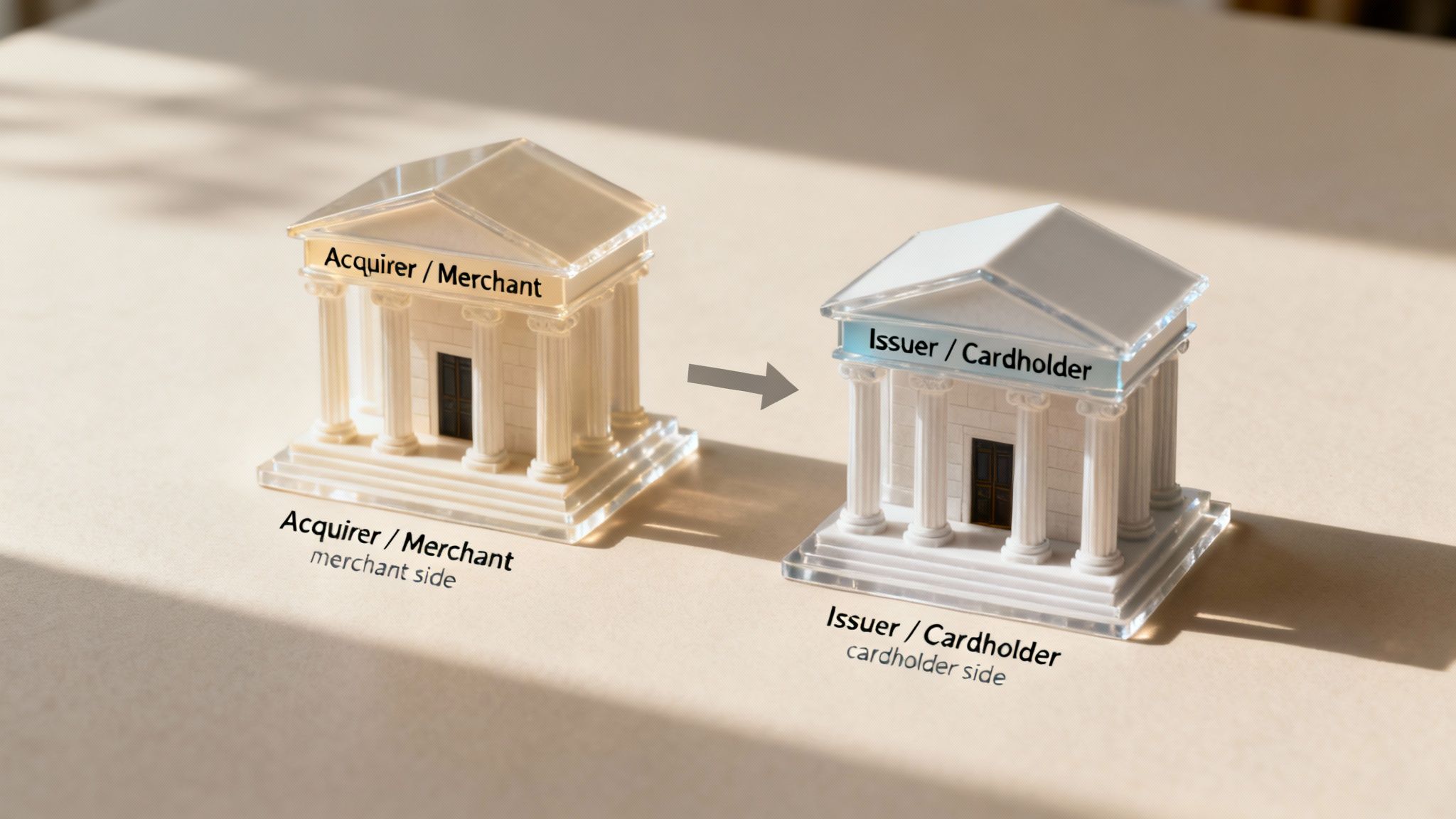

Acquiring Bank vs Issuing Bank Understanding the Difference

In every single card transaction, there are two banks working behind the scenes, each playing for a different team. It's a common point of confusion, but the difference is simple once you remember who they serve.

The acquiring bank is on your team—the merchant's. The issuing bank is on your customer's team—the cardholder's.

Think of it like a negotiation. Your acquiring bank is your agent, representing your interests to make sure you get paid. The issuing bank, on the other hand, is the customer's agent, vouching for their ability to pay and protecting their account from fraud.

They are both absolutely essential for a transaction to succeed, but their roles and responsibilities are completely separate.

Who Does What in a Transaction

When it comes to the actual payment, the issuing bank holds the power to say "yes" or "no." As soon as a payment request hits their system, the issuer checks the customer's account for sufficient funds or credit, verifies the card isn't reported stolen, and scans for any other red flags. Its main job is to authorize or decline the purchase on behalf of the cardholder.

Your acquiring bank is the facilitator in all this. It takes the transaction details from your store, routes them through the card network to the issuer, and brings the approval (or decline) message right back to you. Once a purchase is approved, the acquirer is responsible for settling the funds into your merchant account.

Key Takeaway: The issuer makes the authorization decision based on the cardholder's account status. The acquirer manages the transaction process for the merchant and makes sure the money gets collected.

A Head-to-Head Comparison

Understanding these distinct roles is crucial, especially when problems like chargebacks pop up. When a customer disputes a charge, they file it with their issuing bank. The issuer then communicates that dispute to your acquirer, who in turn notifies you. Navigating these disputes with banks becomes much easier when you know who’s responsible for each step.

To make it even clearer, let’s look at a simple breakdown of their core functions.

Acquiring Bank vs Issuing Bank at a Glance

This table puts the two roles side-by-side, so you can see exactly who handles what.

Ultimately, both banks are necessary partners in the dance of digital payments. The issuer backs the customer, and the acquirer backs you. Knowing the part each one plays helps you manage your payments and protect your business more effectively.

Understanding Acquirer Fees and Merchant Risks

While the acquiring bank is your partner in payments, this partnership isn’t free. Accepting card payments comes with a variety of fees that chip away at your profit from each sale. Think of it as the cost of doing business in a world where plastic and digital wallets reign supreme.

Your acquirer bundles these charges together, often into what’s called a merchant discount rate. This isn't one single fee but rather a blend of several different costs that you pay on every single transaction. Getting a handle on these fees helps you see exactly where your money is going.

Breaking Down the Common Fees

The fees your acquiring bank charges can seem complex, but they generally fall into a few key categories. While pricing models vary, you’ll almost always encounter these core components:

- Interchange Fees: This is the big one—the largest portion of the cost. It’s a fee set by the card networks (like Visa and Mastercard) that your acquirer pays to the customer's issuing bank on every transaction.

- Card Network Fees: This is a much smaller fee that goes directly to the card networks themselves for using their infrastructure.

- Acquirer Markup: Here's where your acquirer makes their money. It’s their fee for providing the merchant account, processing the transaction, and shouldering the risk.

These components are all rolled together to create the final rate you pay. This complex fee structure is a massive part of the global payment processing market, which is projected to handle transactions worth around $157 trillion by 2025. In places like Europe, regulatory changes and new tech are driving huge growth, with the acquiring segment alone expected to generate $10–30 billion in revenue.

The Big One: Chargebacks

Beyond processing fees, the most significant risk you face as a merchant is the dreaded chargeback. This is what happens when a customer disputes a transaction with their issuing bank, which then forcibly reverses the payment right out of your account.

This isn't just a simple refund. The issuing bank claws the money back immediately, and your acquirer hits you with a separate penalty fee for the trouble. This is a critical part of understanding what is an acquiring bank; they are your first line of defense but also the enforcer of these rules. Knowing the details of the chargeback fee is non-negotiable for any merchant.

Your acquiring bank is on the hook for any funds you can’t cover, so they take chargebacks very seriously. They constantly monitor your chargeback ratio—the percentage of your transactions that result in a dispute.

If this ratio gets too high (typically above 1%), your acquirer will label your business as high-risk. This can lead to serious consequences. On top of that, merchants also face risks tied to specific platforms and their unique dispute processes, like when managing PayPal chargeback disputes.

The acquirer might start holding a portion of your funds in a reserve account, hike up your processing fees, or, in the worst-case scenario, terminate your merchant account entirely. This makes managing chargebacks not just about recovering lost sales, but about protecting your very ability to accept payments.

How to Choose the Right Acquiring Partner for Your Business

Picking an acquiring bank isn't just a box to check on your business setup list; it's a huge strategic decision. Who you choose to handle your payments can ripple through your entire operation, affecting everything from day-to-day cash flow and customer satisfaction right down to your bottom line.

Think of it less like opening a standard bank account and more like bringing on a long-term partner for your business's growth.

The best partner for you gets the unique rhythm and risks of your industry. A high-volume retail store, for example, has completely different payment needs than a SaaS company running on subscriptions. What works brilliantly for one could be a terrible fit for the other.

This is a big reason why modern payment companies like Stripe or Adyen have become so popular. They bundle acquiring services with payment processing and a whole suite of other business tools, effectively turning the choice from a traditional bank into a tech partner that’s deeply woven into how you operate.

Key Factors to Evaluate

When you start comparing options, it's easy to get tunnel vision on pricing and contract terms. And while those are definitely important, a few other factors often matter more in the long run. Asking the right questions upfront will lead you to a partner that actually helps you grow, not just one that processes transactions.

Start by digging into these critical areas:

- Industry Specialization: Does this acquirer really get your business model? An acquirer focused on e-commerce will inherently understand the nuances of online fraud and chargebacks far better than one whose main business is brick-and-mortar retail.

- Integration Capabilities: How painlessly will their system plug into the tools you already use? Your acquirer needs to play nice with your e-commerce platform (like Shopify or WooCommerce) and any other software that runs your business.

- Customer Support: When a payment fails or something breaks, you need a real human who can help, and fast. Look for partners known for responsive, helpful service—not just endless automated phone trees and ticket numbers.

It's also smart to think about the bigger picture. Consider how an acquirer fits into your entire ecosystem of tools. As one article on Unlocking Growth with a CRM with Paystack points out, seamless integration between your payment systems and other business software can be a massive unlock for efficiency.

Understanding the Evolving Market

The world of acquiring banks has been buzzing with consolidation lately. We're seeing massive deals, like Global Payments’ $24.25 billion acquisition of Worldpay, which shows how the major players are merging to build out their capabilities and global footprint. This trend just goes to show the intense competition and massive scale now required to serve merchants well.

For modern online businesses, managing payments often involves juggling multiple gateways and acquirers to cover different regions or payment methods. This complexity is exactly why so many merchants are now turning to specialized tools to bring some order to the chaos.

This is where having a unified system can be a game-changer. Pulling all your payment streams into a single dashboard not only simplifies your life but also gives you a much clearer picture of your revenue.

To see how this works in practice, check out our guide on the payment orchestration platform. It breaks down how you can optimize your entire payment stack, no matter which acquiring partners you end up working with.

Common Questions About Acquiring Banks

As you dig deeper into the world of payment processing, some questions always seem to surface. You get the big picture of what an acquiring bank does, but the nitty-gritty, day-to-day stuff can still feel a bit foggy.

Let's clear the air and tackle some of the most common points of confusion for business owners. This quick Q&A will give you the practical answers you need to move forward with confidence.

Can I Get a Merchant Account Without an Acquiring Bank?

In short, no. The acquiring bank is the very institution that provides you with a merchant account. Think of a merchant account as the special type of bank account you absolutely need to accept credit and debit card payments. Without an acquirer, you simply can't process card transactions.

Now, here's where it gets interesting. You might not shake hands or even exchange an email with a traditional bank yourself. Modern payment service providers (PSPs) like Stripe, PayPal, or Square have changed the game by acting as middlemen. They hold a master merchant account with their own acquiring bank and let you process payments under their umbrella as a "sub-merchant."

So, even if you don't have a direct line to the acquirer, rest assured, one is always working behind the scenes to make every single transaction happen.

Is a Payment Processor the Same as an Acquiring Bank?

Not quite, though it's an easy mistake to make since their roles can overlap and people often use the terms interchangeably. An acquiring bank is a licensed financial institution—a member of card networks like Visa and Mastercard. It’s the bank that holds your merchant account and ultimately settles the funds into your business account.

A payment processor, on the other hand, is the tech company handling the nuts and bolts of the transaction. It’s the secure pipeline that transmits payment data from your customer's card at checkout to the acquirer and the card networks.

Here’s a simple way to think about it: the acquirer is the bank, and the processor is the tech that talks to the bank. Many large players in the industry, like Adyen or Worldpay, wear both hats. They have banking licenses and processing technology, bundling everything into one neat package for merchants.

Why Would an Acquiring Bank Reject My Business Application?

It all comes down to one word: risk. Acquiring banks are on the hook financially for the transactions they process for you, especially when chargebacks roll in. If your business suddenly closes up shop or can't cover its disputes, the acquirer is left holding the bag. Because of this, they are extremely risk-averse.

An acquirer will reject your application if they feel your business is too much of a gamble. Common red flags include:

- Operating in a high-risk industry: Things like travel, subscription boxes, or health supplements are known for having much higher chargeback rates.

- A shaky credit history: If your personal or business credit is poor, it signals potential financial instability to the bank.

- A high chargeback ratio: If you have a history of excessive disputes with a previous processor, that's a massive warning sign.

- Being on the MATCH list: This is essentially a blacklist shared among acquirers for merchants whose accounts were terminated for breaking the rules. Getting on this list makes it incredibly difficult to get a new merchant account.

Ultimately, the acquirer needs to trust that your business is legitimate, financially sound, and won't bury them in disputes and fraud they'll have to pay for.

How Do Chargeback Tools Work with My Acquiring Bank?

Chargeback management tools don't replace your acquiring bank—they work right alongside it as your expert partner in the dispute process.

Here’s how it plays out: when a customer files a chargeback, their issuing bank pings your acquirer, who then forwards the dispute to you. This is where a chargeback management solution steps in to automate what is otherwise a ridiculously tedious and time-consuming process.

The tool gets to work gathering all the compelling evidence—shipping confirmations, customer emails, transaction logs, you name it—and packages it into a professional representment case. It then submits this evidence packet to your acquirer and the card networks for you. This collaboration dramatically boosts your win rate, frees up countless hours, and helps keep your chargeback ratio low, which is absolutely vital for staying in your acquiring bank's good graces.

Are chargebacks draining your time and revenue? ChargePay uses AI to automate the entire dispute process, helping you win more cases and recover lost funds without lifting a finger. See how much you can recover by visiting https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)