When a customer says they want to "dispute a transaction," they’re not just asking for their money back. They've formally gone to their bank to reverse a charge, claiming it was wrong, unauthorized, or even fraudulent.

This single act kicks off a formal investigation by the bank, putting the funds in question on hold. While it’s a vital protection tool for consumers, for you—the merchant—it’s the start of a complicated and potentially expensive process.

What It Really Means to Dispute a Transaction

Let's get one thing straight: when a customer disputes a transaction, they are intentionally bypassing you. They're going straight to their bank and essentially saying, "I don't believe I should have to pay for this."

Think of it less like a customer service request and more like a mini-court case for that specific purchase. The banks suddenly become the judge and jury, and you're now on the defense.

This simple complaint triggers a formal process that pulls in a few key players:

- The Cardholder: The customer who started the whole thing.

- The Issuing Bank: The customer's bank. They review the claim and often pull the money back from you temporarily.

- The Acquiring Bank: Your business bank. They get the dispute notice and pass the bad news on to you.

- The Merchant: That's you. You now have to decide whether to eat the cost or fight back.

The Critical Difference from a Refund

Understanding what a dispute truly means starts with seeing how it’s completely different from a refund. A refund is a conversation between you and your customer. They contact you, you agree to return their money, and you handle it privately. It's a customer service moment.

A dispute, however, immediately escalates the problem to the banking level. The moment it's filed, it becomes an official financial claim governed by strict card network rules. It's no longer just between you and the customer. You can dive deeper into the nuts and bolts in our guide to what is a bank chargeback.

To make it crystal clear, let's break down the key differences.

Refund Request vs. Transaction Dispute Key Differences

This table shows a quick comparison to help you understand the critical distinctions between a customer asking for a refund and filing a formal dispute.

As you can see, a dispute is a much more serious event with far greater consequences than a simple refund request.

A dispute isn't just a reversed payment; it's a formal challenge to the legitimacy of a transaction. For merchants, this means more than just lost revenue—it involves additional bank fees, administrative work, and a potential negative mark on your merchant account health.

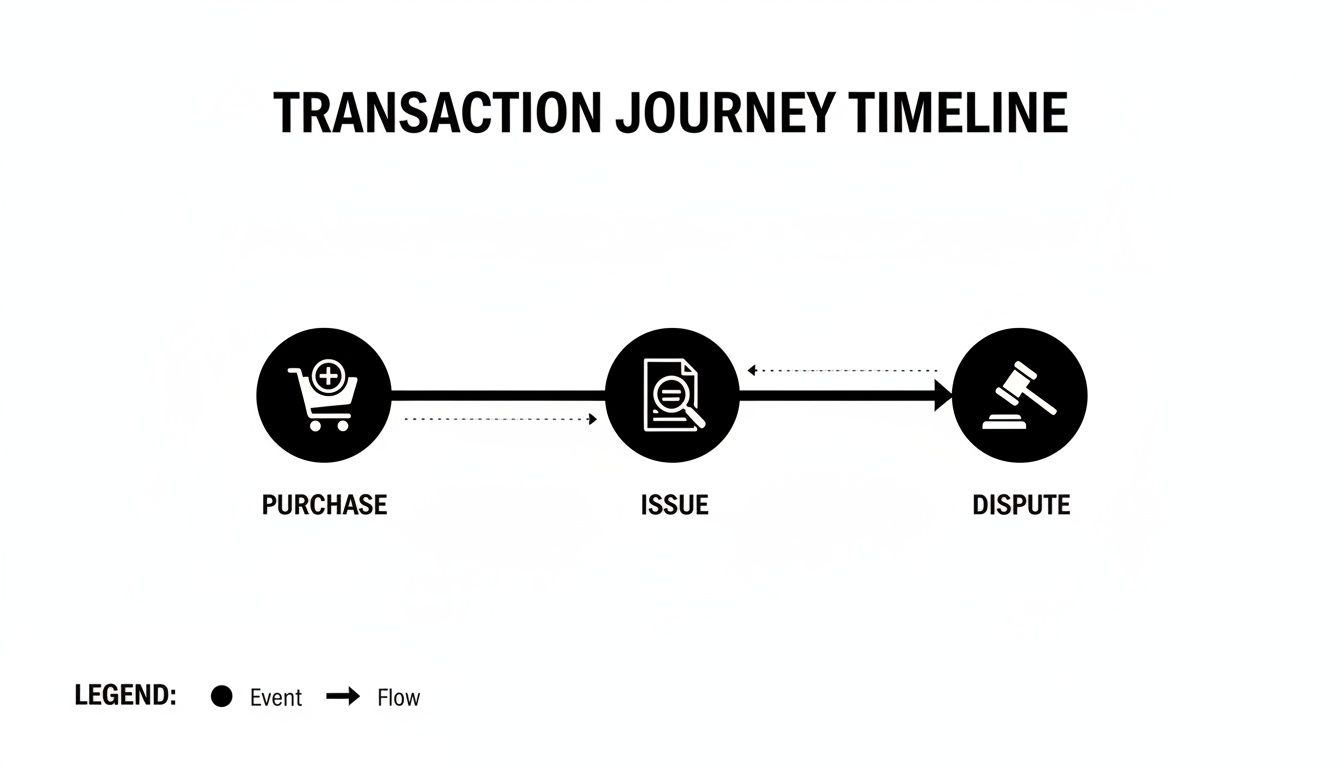

The Journey of a Disputed Transaction

So, what happens the moment a customer decides to dispute a transaction? It’s not an instant refund. Instead, it kicks off a formal, multi-stage process governed by the card networks (like Visa or Mastercard). Understanding this journey is key to knowing when and how you can defend your sale.

The whole thing starts when the cardholder contacts their bank—the issuing bank—to question a charge. They’ll explain why they believe the charge is incorrect, and the bank opens a formal investigation. This is the starting pistol for the entire dispute lifecycle.

From there, the issuing bank reviews the claim. If it seems valid on the surface, they issue a temporary credit to the customer. At the same time, the funds are pulled from your merchant account, and you get hit with a non-refundable dispute fee. This fee can be anywhere from $15 to over $100, and you pay it regardless of who wins.

From Notification to Representment

Thankfully, you aren't left in the dark. Your bank—the acquiring bank—will notify you of the dispute and provide a reason code that explains the customer’s claim. This is where the clock starts ticking for you. You typically have a tight window, often just 20 to 45 days, to respond.

This response process is called representment. Think of it as your one and only chance to present your side of the story and prove the transaction was legitimate. You'll need to gather and submit compelling evidence to make your case. For a more detailed look at what happens during this phase, you can explore the full card dispute process.

This timeline shows just how quickly a simple purchase can escalate into a formal dispute.

As you can see, the journey from a customer having an issue to filing a dispute is often a short one, putting the pressure on you to act fast.

The Final Decision and Its Impact

Once you submit your evidence, the issuing bank reviews everything—both your documents and the customer's original claim. They act as the final judge and make the call.

- If you win: The temporary credit is taken back from the customer's account, and the funds are returned to you. Phew.

- If you lose: The customer keeps the credit, meaning you've lost the sale revenue plus the non-refundable dispute fee.

This entire journey can take anywhere from a few weeks to several months, leaving your revenue in limbo. It’s a drawn-out process that really highlights why understanding what a disputed transaction means is so critical for your bottom line.

Why Good Customers Dispute Valid Charges

When a customer files a dispute, it’s natural to jump to conclusions—maybe a stolen card or a scammer trying to get a free product. And while those things definitely happen, the reality is often much simpler. Many disputes come from good, honest customers who are simply confused or frustrated.

A lot of these issues boil down to a simple misunderstanding. Picture this: a customer checks their credit card statement and sees a charge from a business name they don't recognize. Panic sets in, and they assume it’s fraud. Or, maybe they forgot about that subscription they signed up for months ago. When the renewal charge hits, disputing it feels like a quicker fix than trying to figure out how to cancel.

Common Causes of Legitimate Disputes

Sometimes, even with the best intentions, the problem starts on your end. A customer might be perfectly justified in filing a dispute if:

- The product arrived damaged: They received a broken item and couldn't find an easy way to start a return.

- The item wasn't as described: What showed up at their door looks nothing like the pictures online or just plain didn't meet their expectations.

- Shipping took too long: The delivery date came and went, and now they're convinced the order is lost in transit.

But perhaps the most frustrating reason is friendly fraud. This is when a customer makes a legitimate purchase, receives it, and then disputes the charge anyway. They might genuinely not recognize the charge, feel a bit of buyer's remorse, or simply find it easier to call their bank than your customer service team.

The True Cost of a Dispute

A single dispute hits your business for a lot more than just the lost revenue from that one sale. First, you get slapped with a non-refundable dispute fee from the bank, which can run anywhere from $15 to over $100—and you pay that whether you win or lose the fight. On top of that, think about the operational costs and the time your team has to spend digging up evidence to build a case.

These aren't isolated incidents; they're becoming more common. Shifting consumer habits and new fraud patterns are changing things up, with friendly fraud becoming a massive headache for merchants. In 2023, consumers filed disputes worth more than $65.2 billion, with the average cardholder filing chargebacks valued at $76.

You can read more about the latest chargeback statistics to get the full picture. Understanding what’s really behind these claims is the first step in protecting your bottom line, especially from the notoriously tricky issue of friendly fraud.

How to Build a Winning Dispute Response

Getting a dispute notice can feel like a punch to the gut. It’s easy to take it personally, but it’s really just the start of a conversation with the customer's bank—one that’s all about evidence. The key to winning is to approach it like you’re building a legal case. Your job is to prove, with cold hard facts, that the transaction was legit and you held up your end of the deal.

You have way more power in this situation than you might think. But that power hinges on being organized, professional, and fast. A sloppy, emotional, or delayed response is almost a guaranteed loss. What you need is a clear, fact-based strategy that leaves zero room for doubt.

At the end of the day, every dispute is just a customer complaint that has escalated. Learning how to effectively resolve customer complaints is a core skill for any merchant who wants to handle these situations well.

Your Evidence Checklist

The bank employee reviewing the case has no idea what happened during the sale. It’s on you to paint them a crystal-clear picture of the entire transaction from start to finish. Gathering the right evidence is, without a doubt, the most important step.

You need to pull together everything you have on the order:

- Proof of Delivery: For physical products, this is absolutely non-negotiable. Always include shipping confirmation with a tracking number showing the item was delivered to the customer's address on file.

- Customer Communications: Dig up any emails, support tickets, or chat logs. If the customer reached out before filing the dispute, you need to show that you were responsive and tried to solve their problem.

- Order and Service Records: This includes invoices, digital receipts, and the terms of service they clicked "agree" on at checkout. For digital goods, this means providing logs showing the customer downloaded the product or used the service.

A winning response is built on compelling evidence. It’s not about arguing with the customer; it’s about presenting clear, objective proof to the bank that the charge was valid. Your evidence should tell a complete and logical story of the transaction.

Crafting a Professional Rebuttal

Once all your proof is gathered, you need to package it with a professional rebuttal letter. Think of this letter as the cover sheet for your case file—it summarizes what happened and tells the bank exactly where to look in your documentation. It’s a make-or-break piece of the puzzle, and learning how to write a letter of rebuttal is crucial.

Keep it short, sweet, and stick to the facts. State the customer’s claim, then walk the bank through the evidence that proves their claim is incorrect. When you combine solid proof with a professional summary, you give yourself the absolute best shot at winning back your revenue.

Using Automation to Defend Your Revenue

As your business grows, fighting every single transaction dispute manually becomes a massive drain on your time and resources. For a lot of merchants, it feels like a losing battle, especially when you're trying to focus on, you know, actually running the business. This is where modern tools can completely change the game.

The number of global chargebacks is ballooning, with dispute volumes expected to rocket to 337 million cases by 2025. That kind of surge makes it nearly impossible for old-school manual processes to keep up, which really drives home the need for a smarter approach.

Shifting from Manual to Automatic Defense

Imagine a system that handles the entire defense process for you. Instead of you spending hours digging through sales records and customer emails, an AI-driven platform like ChargePay can analyze the dispute reason code and instantly build a powerful, evidence-backed response that's tailored to win. That's how automation solves the core problems of cost and complexity.

This dashboard gives you a glimpse of how an automated system organizes and tracks disputes, giving you a clear view of your revenue recovery efforts.

By automating this entire workflow, you can claw back that revenue and get back to what truly matters—growing your business.

The goal of automation isn’t just to fight disputes faster; it's about fighting them smarter. By using AI to assemble the most compelling evidence, you significantly increase your win rate and protect your bottom line without lifting a finger.

To get ahead of the problem, merchants can also lean on tools like dark web monitoring to spot compromised customer credentials that often lead to fraudulent transactions down the line. For a deeper dive, check out our complete guide to automated chargeback management using AI.

Frequently Asked Questions About Disputes

When you're dealing with payment processing, it's easy to get tangled up in the terminology. The phrase 'dispute a transaction' can feel a bit murky, but getting a handle on the specifics is the first step in protecting your business.

Let’s clear up some of the most common questions merchants have about the whole dispute process.

How Long Do I Have to Respond to a Dispute?

This is a big one. The clock starts ticking the second a dispute is filed, and you usually have between 20 to 45 days to respond. This window is often called the "representment period," and the exact timeline depends on the card network, like Visa or Mastercard.

Treat this as a hard deadline. If you miss it, you automatically lose the dispute. That’s why moving fast is so critical. An automated system can be a lifesaver here, ensuring you never forfeit revenue just because time ran out.

Is a Chargeback the Same Thing as a Dispute?

They're related, but they aren't the same thing. Think of it this way: a dispute is the customer’s initial claim when they question a charge on their statement. A chargeback is what happens next—it’s the actual reversal of funds from your account back to the customer's card.

The dispute is the entire process—the investigation, the back-and-forth, the argument. The chargeback is the financial gut punch that happens if you lose that argument or don't respond in time.

Can I Stop Disputes Before They Happen?

You can't stop them all—that's just the reality of doing business. But you can absolutely reduce them. The best defense is a good offense, and that means focusing on clarity and communication.

- Use clear billing descriptors: Nothing sparks a dispute faster than a charge from "XYZ SERVICES INC." on a bank statement. Make sure your business name is instantly recognizable.

- Provide amazing, easy-to-find customer service: A visible phone number or email can turn a potential dispute into a simple conversation and a refund request.

- Have a transparent refund policy: No surprises. When customers know what to expect, they're less likely to get frustrated and call their bank.

- Use fraud prevention tools: These are your front-line soldiers, stopping bad transactions before they ever have a chance to become a dispute.

Often, a little proactive communication can solve a customer's problem before they even think about involving their bank.

What if I Win the Dispute and the Customer Still Isn’t Happy?

Winning a dispute means the bank sided with your evidence. The transaction stands, the money is returned to your account, and the case is officially closed. That's a win for your bottom line.

But it doesn't magically fix the customer's feelings. They might still be upset, leave a negative review online, or vow never to shop with you again. This is exactly why prevention and great service are so important—they work to save both the sale and the long-term customer relationship. A win is great for revenue, but a happy, returning customer is better for your business.

Tired of losing revenue to complicated disputes? ChargePay uses AI to automate the entire fight for you, recovering up to 80% of lost funds without you lifting a finger. See how much you can recover with ChargePay.

.svg)

.svg)

.svg)

.svg)