That sinking feeling when you spot a weird charge on your Cash App? It's awful. But the good news is you have options. You can either ask for a refund right from the person who received the money or file a formal dispute with Cash App. Figuring out which path to take is the most important first step in getting your money back.

Your First Move When a Cash App Payment Goes Wrong

We’ve all felt that jolt of panic after hitting "send" on a payment that just doesn't feel right. The speed of Cash App is a blessing, but it can also be a curse when things go wrong, whether it's an honest mistake or outright fraud. What you do in those first few moments really matters.

First things first, you need to understand your two main choices: a refund request and a formal dispute. They sound similar, but they're completely different tools for different situations.

Refund Request vs Formal Dispute

A refund request is your best bet for simple, honest mistakes. Maybe you sent cash to the wrong $Cashtag by accident, or you paid a friend back twice for dinner. In these scenarios, you're just asking the other person to be a good sport and send the money back. It's the friendly, low-conflict approach that works best when there's trust involved.

A formal dispute, however, is for the serious stuff. This is the route you take for suspected fraud, an unauthorized charge you don't recognize, or if you've been scammed by a seller. When you file a dispute, you're officially asking Cash App's team to step in, investigate the transaction, and make a judgment call.

The key difference is who's in control. With a refund, the recipient has all the power to say yes or no. With a dispute, Cash App investigates the evidence and makes the final decision.

To make this crystal clear, let's look at the key differences side-by-side.

Dispute vs Refund Request What's the Difference?

Let's say you bought concert tickets from someone on social media, sent the money via Cash App, and then they ghosted you. A refund request here is probably a waste of time—they already have your money and aren't likely to give it back. This is a textbook case for a formal dispute. You'll need to gather your evidence and present your case directly to Cash App.

To get a better handle on the entire process, you can learn more about the Cash App chargeback process and how it’s designed to protect you.

So, your first move really does set the tone. If it's a simple mix-up with someone you know, start with a refund request. But if you smell a rat or see a charge you didn't make, don't hesitate—go straight to filing an official dispute to get the ball rolling.

A Practical Walkthrough of Filing Your Dispute in the App

Knowing you need to file a dispute is one thing; actually finding the right buttons inside the Cash App interface is another. It can feel like you're searching for a needle in a haystack if you don't know exactly where to look.

Let's walk through the specific clicks you need to make to get your claim officially filed.

The process kicks off in your activity feed, which is the clock icon at the bottom right of your screen. This is where every single transaction lives, so your first task is to scroll through and pinpoint the specific payment that’s causing the problem.

Navigating to the Right Transaction

Once you’ve tracked down the suspicious charge, tap on it to open the full transaction details. This screen shows you the recipient, the amount, and the date—all the basic info.

Look to the top right corner. See those three little dots (...)? That's your gateway to the support options.

Tap those dots, and a menu will pop up from the bottom. You'll see a few choices, including one labeled "Need Help & Cash App Support." That's the one you want.

Don't get distracted by the big "Refund" button you see on the main transaction screen. If you're dealing with fraud or an unauthorized payment, asking a scammer for a refund is a dead end. You need to dig deeper into the support menu to file a formal dispute.

After you select the support option, Cash App will give you a list of potential issues. Your job is to pick the one that best describes what happened.

Choosing the Correct Dispute Reason

This next screen is critical. Getting it right helps Cash App route your problem correctly from the get-go. You'll likely see options like these:

- "I sent this payment to the wrong person." This is for simple mistakes, not for scams or fraud.

- "This was an unauthorized purchase." Pick this if you didn't make or approve the transaction at all.

- "I was scammed." This is your choice if you were tricked into sending money for something that never materialized.

Be honest and pick the most accurate reason. For instance, if you bought concert tickets from a seller who then vanished, that’s a scam. If a charge pops up from a store you've never even heard of, it's probably an unauthorized purchase. Making the right choice here really does set the stage for a smoother investigation.

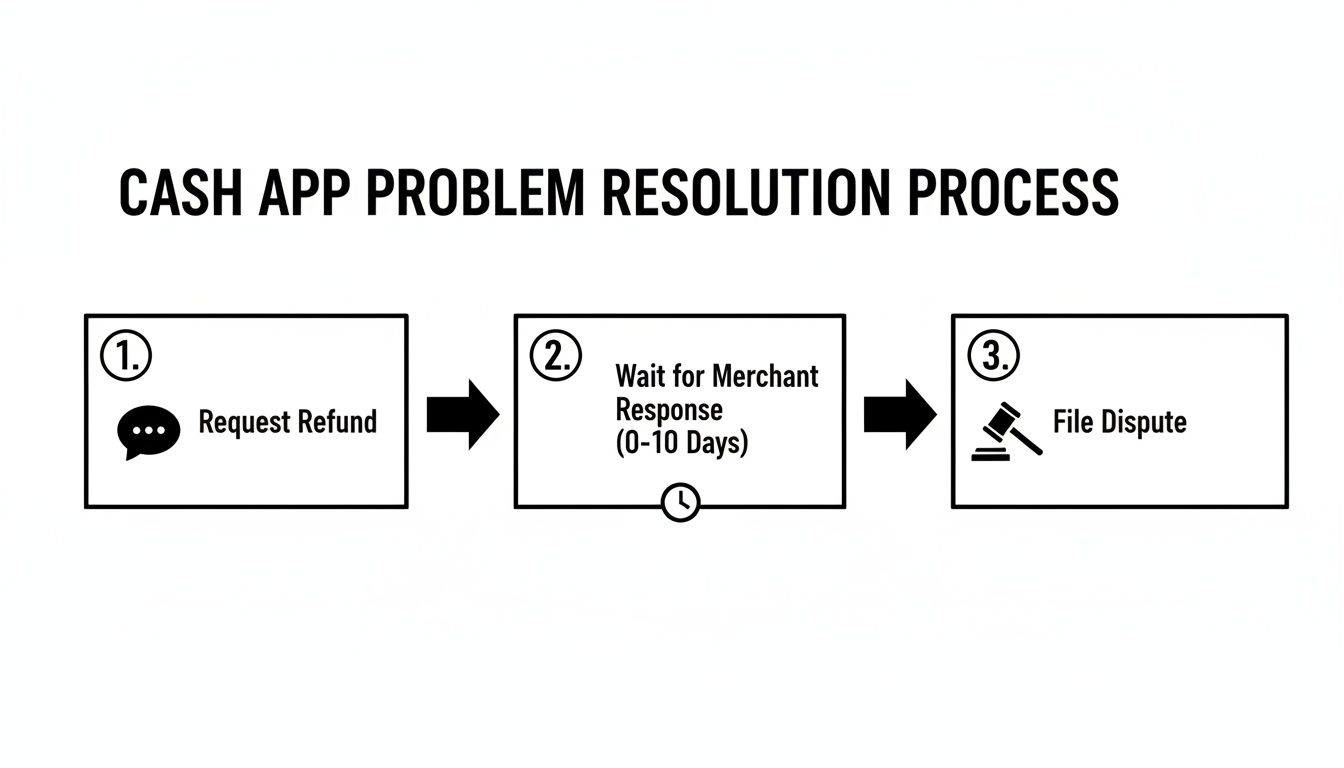

This visual guide breaks down the basic flow, from spotting a problem to filing that formal dispute.

As the flowchart shows, your first decision is between a simple refund request and a more serious dispute. It's all about guiding you down the right path based on what actually happened.

Finally, Cash App will ask for more details. This is your chance to briefly and clearly explain the situation. Stick to the facts: what were you supposed to get, why is the transaction fraudulent, and what communication (if any) did you have? Once you hit submit, your dispute is officially on the record.

While this process is specific to Cash App, you can learn more about the general principles of how to dispute a transaction for a broader understanding.

What to Do When Cash App Denies Your Dispute

That sinking feeling when you get a notification from Cash App saying your dispute was denied is all too common. It feels like hitting a dead end, but trust me, it’s not over. It just means you need to change your strategy and take your case to a higher authority.

Before you throw in the towel on Cash App support, it’s worth one more try. A denial isn't always the final word. You can reply directly to their email, maybe with some new evidence you’ve found or just by re-explaining your side of the story more clearly. A little polite persistence can sometimes trigger a second look from a different agent.

Your Most Powerful Next Step: Go to Your Bank

If Cash App still won’t budge, it's time to go over their head. Your next and most effective move is to contact the source of the funds—your linked bank or credit card company. A lot of people don’t even know this is an option, but it's a game-changer.

What you're doing here is initiating a formal bank chargeback. If the transaction was from a debit card, this is often called a Regulation E dispute. Federal law gives you the right to dispute unauthorized electronic fund transfers, and your bank is legally required to investigate your claim.

When you file a dispute with your bank, you're no longer playing by Cash App's internal rules. You're now protected by federal consumer protection laws, which carry a lot more weight.

This route is critical, especially considering the platform's history. In 2025, the Consumer Financial Protection Bureau (CFPB) hit Block, Inc. (Cash App's parent company) with a $175 million order for its flawed dispute resolution process. The CFPB found that Cash App was closing cases without doing a proper investigation and, in many instances, was telling users to go to their banks instead of handling the disputes themselves.

How to Start a Bank Chargeback

Getting the ball rolling with your bank is usually pretty simple. Here’s how it typically works:

- Call Your Bank's Fraud Department: The number is right on the back of your card. Alternatively, you can log into your online banking portal and look for an option like "dispute a transaction" or "report fraudulent activity."

- Give Them All the Details: Have the transaction date, the exact amount, and the recipient's info from your Cash App history ready to go.

- Explain What Happened: Let them know you made a purchase through Cash App, the charge was unauthorized (or fraudulent, or the item never arrived), and you already tried to resolve it with Cash App but were denied.

- Send Over Your Evidence: Your bank will want to see everything you've collected. This means screenshots of your chats with the seller, the denial email from Cash App, and any other proof you have.

Once you file, your bank will open its own investigation. They’ll usually issue a provisional credit for the disputed amount back into your account while they sort things out. This gives you your money back right away while the official process unfolds. To get a better sense of how this works behind the scenes, our guide on disputes and chargebacks breaks down the entire lifecycle.

For more perspective on the art of appealing platform decisions, it can be helpful to see how people navigate similar challenges with other major platforms. The core principles of detailed documentation and persistence are universal.

How Merchants Can Effectively Handle Cash App Disputes

As a merchant, seeing a customer pay with Cash App can feel like a done deal—more secure than a regular card swipe. But there’s a catch.

If that payment was funded by a linked credit or debit card, you’re still exposed to the world of traditional chargebacks. A dispute from a Cash App user will land in your payment processor's dashboard just like any other, leaving you to fight for the revenue you thought you'd secured.

Knowing how to handle these disputes from your side is essential. It's not just about losing the initial sale; it’s about the time and energy you have to pour into proving the transaction was legitimate.

Gathering Your Evidence to Fight Back

When a dispute notification pops up, you need to act fast. Your best defense is a strong offense, and that means documentation.

The goal is to assemble a rock-solid case that shows you fulfilled your end of the bargain. This process of fighting back is called representment, and its success hinges entirely on the quality of the evidence you provide.

Don't procrastinate. Start pulling together everything related to the order right away.

- Communication Records: Grab screenshots of any emails, DMs, or support tickets with the customer. These conversations can often prove they received the item or were happy with the service before the dispute.

- Proof of Delivery: For physical products, this is non-negotiable. You need shipping confirmation with a tracking number showing the package was delivered to the exact address the customer provided.

- Service Logs or Usage Data: If you sell digital goods or services, your proof lies in the data. Think login records, download timestamps, or usage reports showing the customer accessed what they paid for.

Put on your detective hat. Your job is to create an undeniable timeline of a legitimate transaction, from the moment the order was placed to the final delivery.

The number one reason merchants lose disputes is a lack of compelling evidence. Don't just send a copy of the receipt. You need to tell the complete story of the transaction, backed by clear, organized proof.

The Growing Problem of Friendly Fraud

Here's the frustrating part: many disputes don't come from stolen cards. They come from customers who knowingly dispute a valid charge. We call this friendly fraud, and it’s a massive headache for merchants. The customer gets your product, uses it, and then files a chargeback claiming they never got it or didn't authorize the purchase.

This isn't just a small issue—it's getting worse. Global chargeback volume is projected to jump by 41 percent between 2023 and 2026. Worse, in 2024, a staggering 72 percent of merchants reported an increase in friendly fraud specifically.

To fight this, your evidence has to be airtight. For instance, if a customer claims a package never showed up but your tracking information shows it was delivered and signed for, that signature is your silver bullet.

Strong documentation is your only real defense. Investing in robust chargeback protection for merchants can also give you a much-needed safety net. By preparing for these scenarios, you can dramatically improve your chances of winning and keeping your hard-earned revenue.

Automating Your Defense Against Payment Disputes

Trying to fight every single payment dispute by hand is a losing game for any business that's trying to grow. The hours you spend digging through old orders, hunting for shipping confirmations, and writing rebuttal letters really start to pile up. It pulls you away from the things that actually move your business forward.

As those dispute numbers tick upward, the manual approach just doesn't scale. Eventually, you hit a wall.

But there’s a much smarter way to protect your revenue. Instead of playing whack-a-mole with every dispute that pops up, you can put your entire defense on autopilot.

The Power of an Automated System

Imagine a system that works for you 24/7, handling disputes the second they come in. That's the whole idea behind automated chargeback management. Rather than forcing you to react to every claim, an AI-powered solution takes the entire representment process off your plate.

This tech plugs right into your payment platforms, whether you're on Shopify, Stripe, or something else. When a dispute hits—it doesn't matter if it came from a Cash App user's linked card or a traditional credit card—the system jumps into action instantly.

The real magic here is speed and intelligence. An automated system can analyze the dispute reason code, pull the most convincing evidence from your store's data, and build a solid response tailored to what banks want to see, all in a matter of seconds.

This means no more late nights scrambling to find evidence for a $50 chargeback. The automation handles it all, freeing you up to focus on growing your business.

How AI Builds a Winning Case

An automated system does more than just fill out a form; it builds a strategic defense from the ground up. It learns from thousands of past disputes to figure out exactly what kind of evidence gets results.

Here’s a peek at how it works:

- Instant Data Collection: The moment a dispute arrives, the AI grabs crucial evidence like customer IP addresses, shipping confirmations, delivery photos, and even past order history.

- Intelligent Response Generation: It then uses the dispute reason to craft a professional, data-packed rebuttal letter that’s easy for the issuing bank’s review team to understand.

- Seamless Submission: The whole evidence package is submitted directly to the payment processor on your behalf. You never have to worry about missing a deadline.

This approach doesn't just save you a ton of time—it also gives your win rate a serious boost. For any merchant, handling payment disputes well is a key piece of building a resilient risk management strategy that protects your business from all sides.

By automating your defense, you transform a reactive, time-sucking chore into a streamlined, revenue-saving machine. If you're ready to go deeper, our complete guide to automated chargeback management using AI breaks down exactly how this technology changes the game. It’s all about working smarter, not harder, to protect your bottom line.

Got Questions About Cash App Disputes? We Have Answers.

When you're trying to dispute a Cash App payment, it can feel like you're navigating a maze blindfolded. It's totally normal to have a million questions popping into your head. Let's clear up some of the most common ones so you know what to expect.

A big question is always, "How long will this take?" While a really simple, clear-cut dispute might get sorted out in about 10 business days, don't hold your breath. If your case has a few moving parts or needs more investigation, it could easily drag on for several weeks, sometimes even a couple of months.

Scams vs. Unauthorized Charges: What's the Difference?

It’s super important to know how Cash App sees different kinds of problems. An unauthorized charge is exactly what it sounds like—someone got your info and used your account without you knowing. Think of it as classic fraud, like your card details getting stolen. These cases are usually easier to win because federal laws are on your side for this kind of thing.

A scam is a whole different beast. This is when you were tricked into sending the money yourself. Maybe you thought you were buying concert tickets that turned out to be fake, or you fell for a phishing email. Because you technically authorized the payment, these disputes are much, much tougher to win.

Sadly, this kind of peer-to-peer payment fraud is blowing up. A recent Consumer Reports survey found that 12 percent of people who use P2P apps weekly have been scammed. In 2023 alone, consumers lost a staggering $210 million to these scams. You can dig deeper into their findings on P2P payment safety.

What Are My Chances of Actually Winning?

Your odds of getting your money back really boil down to your specific situation and the proof you can show.

- Unauthorized Charges: Your chances are pretty good here, especially if you can prove you didn't make the payment and you reported it right away.

- Scams: This is an uphill battle. Your best shot is if the payment was funded by a linked credit card, since that gives you another layer of protection through your bank.

- Goods Not Received: If you bought something and it never showed up, you've got a solid case. Just be ready with screenshots of your chats with the seller and proof that you never got the item.

Here's something a lot of people get wrong: you can't just "cancel" a Cash App payment once it's completed. As soon as the other person accepts the money, it's gone. Your only options are to ask them for a refund or go through the official dispute process.

At the end of the day, winning a Cash App dispute comes down to persistence and having clear, solid evidence to back up your story.

Don't let disputes drain your resources. ChargePay uses AI to automate the entire chargeback process, recovering lost revenue for you hands-free. Learn how ChargePay can boost your win rate.

.svg)

.svg)

.svg)

.svg)