So, you’ve run into an issue with a purchase and the merchant isn't helping. What's next? This is where the chargeback process comes in, but it’s important to know it’s your last line of defense, not your first move.

Before you even think about calling your bank, you absolutely must try to sort things out with the merchant directly. Think of it as a mandatory first step. Your credit card issuer will expect you to have done this, and skipping it is one of the quickest ways to get your dispute shut down before it even starts.

When is a Chargeback the Right Call?

Most businesses would rather give you a refund than deal with the headache and fees of a chargeback, so they’re usually willing to work with you. But when they dig in their heels or just plain ignore you, that’s your green light.

Filing a chargeback isn't just lodging a complaint. You're kicking off a formal investigation backed by heavyweights like Visa or Mastercard to get your money back. It's a powerful tool when used correctly.

Do You Have a Valid Reason to File?

Not every frustrating purchase qualifies for a chargeback. You need a legitimate, recognized reason for your bank to take your case seriously. If you just changed your mind or have a minor complaint, a chargeback probably isn't the way to go.

Here are the classic situations where a chargeback is completely justified:

- Fraudulent Charges: This is the most obvious one. You check your statement and see a charge from a company you've never heard of for something you definitely didn't buy.

- Product Not as Described: The boots you ordered arrived, but they're the wrong color, a cheap knock-off instead of the brand advertised, or missing the steel toe you needed.

- Damaged or Defective Goods: That new gadget arrived with a cracked screen, or it just stopped working a week later, and the seller is refusing to help.

- Services Never Delivered: You paid a contractor for a job they never finished or signed up for a monthly subscription that never activated.

- Billing Goofs: You were double-charged for a single item, charged the wrong amount, or are still being billed for a service you cancelled months ago.

A chargeback does more than just get your money back. It’s a tool that holds businesses accountable and protects you from fraud. When a direct conversation goes nowhere, it’s your right to take the next step.

To help you decide, here’s a quick table breaking down common scenarios.

Quick Guide: Is a Chargeback Your Best Option?

This table should make it clear: the first step is almost always trying to resolve it with the business.

One of the most clear-cut cases for a chargeback is fraud. A fraud detection agent at a bank deals with these situations constantly. For a complete rundown of all the scenarios that qualify, check out the valid reasons for a chargeback in our detailed guide.

As more of our shopping moves online, disputes are on the rise. Industry reports suggest global chargeback cases could swell to 261 million in 2025 and hit 324 million by 2028. It's a growing issue, making it more important than ever for you to know your rights and how the process works.

Gathering Evidence to Build a Strong Case

Winning a chargeback really boils down to one thing: telling a clear, believable story to your bank. And every good story needs proof. Without solid evidence, it's just your word against the merchant's, which is rarely enough to get your money back.

Think of yourself as a detective building a case. Your goal is to assemble a file so compelling that the bank has no choice but to rule in your favor. The more organized and persuasive your evidence is, the faster the person reviewing it can grasp the situation and side with you.

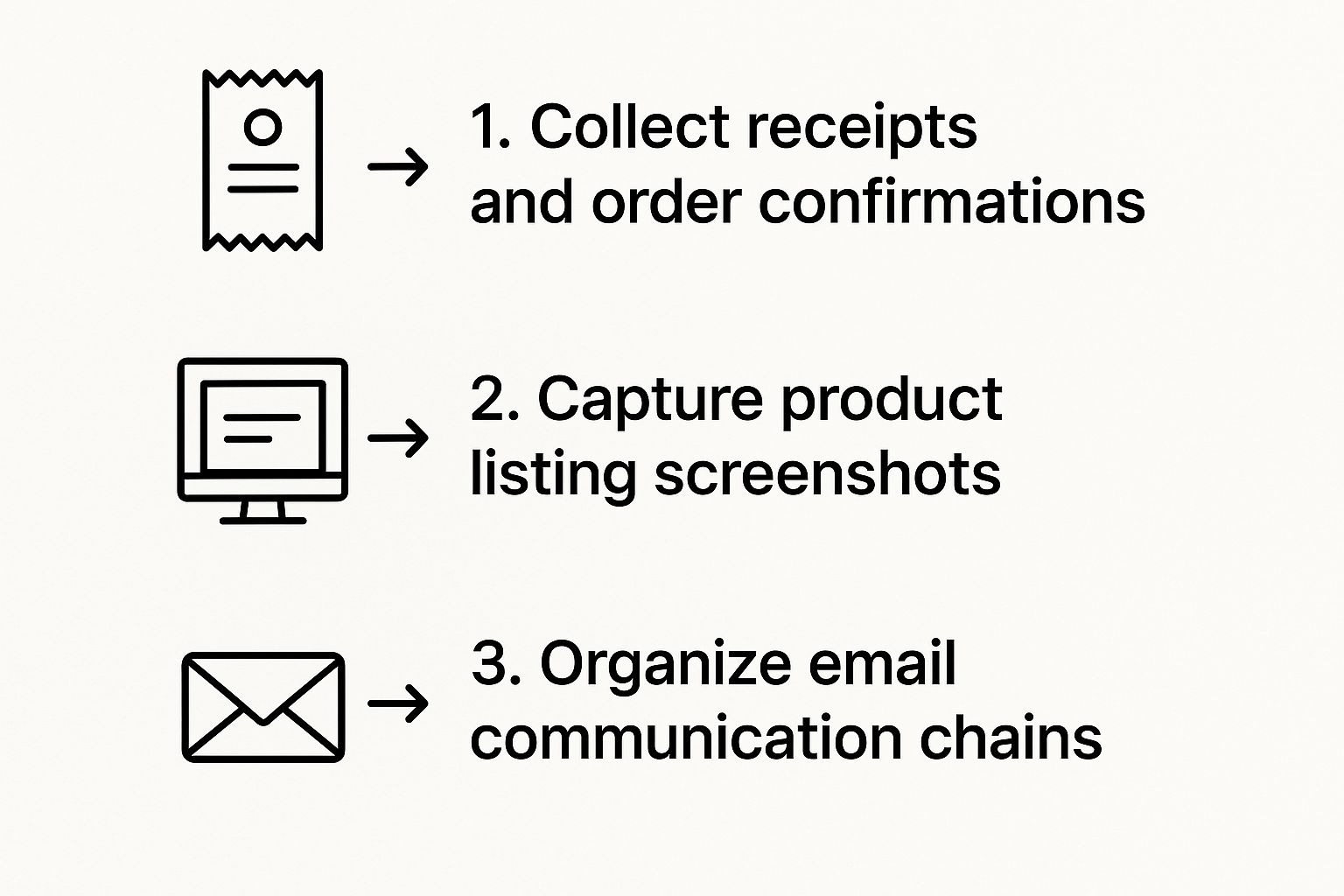

What to Collect for Your Claim

The kind of evidence you need will change depending on why you're filing the chargeback. A claim for a shattered vase is going to look a lot different than a claim for a fraudulent charge you never made.

Let's break down the must-haves for the most common situations:

- For Damaged or Defective Items: The second you open the box, start taking clear photos or videos. Get the product from multiple angles, and don't forget to document the shipping box itself if it looks beat up.

- For Items Not as Described: Your most powerful weapon here is a screenshot of the original product listing. You absolutely need to capture the description, the seller's photos, and any specific claims they made that didn't pan out.

- For Services Not Rendered: Dig up any contracts, service agreements, or work orders that spell out what was supposed to be done. If you paid a deposit for a job that never started, that invoice and your proof of payment are critical.

- For Canceled Subscriptions: The golden ticket is your cancellation confirmation email or a screenshot from your account dashboard showing the cancellation date. Your bank statement showing they charged you after that date is the final piece of the puzzle.

Here's a quick visual guide to the core documents you'll need for almost any dispute.

This simple flow covers the basic evidence you should always start with, no matter what went wrong.

Organizing Your Evidence for Success

Once you have everything, don't just dump it on the bank in a messy pile. Get it organized. Create a simple timeline of events in a Word doc or email, listing each key date and exactly what happened. For example: "Jan 5th - Ordered product. Jan 12th - Product arrived damaged. Jan 13th - Emailed seller with photos."

This organized approach makes it incredibly easy for the bank's investigator to follow along. You're not just giving them evidence; you're guiding them to the same conclusion you've already reached.

Pro Tip: I always recommend combining all your documents into a single PDF file. This keeps everything in one place, ensures nothing gets lost, and makes your case look clean and professional. Start with a brief cover letter summarizing the issue, then arrange your evidence in chronological order.

Keep in mind, this isn't a one-sided affair. The merchant gets a chance to fight back by submitting their own evidence to prove the charge was legitimate. Their response is often called a rebuttal. It’s helpful to see an example of a rebuttal letter that merchants use to get a sense of what you're up against. This gives you a peek into their process and helps you build an even stronger case from the get-go.

Getting the Official Filing Process Started

Alright, you’ve got your evidence compiled and organized. Now it’s time to officially file that chargeback. This is where you formally hand your case over to the bank. Think of it less like just filling out a form and more like submitting your final, polished report to the decision-makers.

The good news? Most banks give you a few different ways to get this done.

By far the fastest and easiest route is through your online banking portal or mobile app. Just log in, find the transaction on your statement, and look for a link that says something like "Dispute a Transaction." It’s usually right there next to the charge, making it the most direct path.

If you'd rather talk to a person, you can always call the customer service number on the back of your card. A representative can guide you through the process step-by-step, which is a big help if you're feeling unsure about any of the details. And for those who prefer a physical paper trail, filing by mail is still an option, though it’s definitely the slowest of the bunch.

Choosing the Right Reason Code

When you file, you’ll be asked to select a reason code. This is a really important step, so don't just click the first one that looks close. A reason code is simply the bank's standardized way of categorizing why you're disputing the charge. Think "Product Not Received" or "Fraudulent Transaction."

Picking the right one is critical because it tells the bank how to investigate your claim. If you got a broken product but select "Fraud," your dispute could get denied simply because it was sent down the wrong investigative path.

Here’s a quick look at the common categories you'll see:

- Fraud: Use this only for charges you absolutely did not authorize in any way, shape, or form.

- Authorization Issues: This bucket is for things like being charged after you clearly canceled a subscription.

- Processing Errors: Think duplicate charges or being billed the wrong amount for an item.

- Consumer Disputes: This is a broad category for issues like receiving a defective product, an item that's nothing like the description, or services not rendered.

Be precise. Be honest. Misrepresenting the situation, even by accident, just gives the merchant an easy opening to challenge and win the dispute.

Choosing the correct reason code is like setting the GPS for your dispute. The right code sends the investigation down the correct path, while the wrong one can get it lost from the start.

If you want to get into the nitty-gritty of how a major card network handles these, you can learn more about the Visa chargeback process and its specific codes.

Completing the Dispute Form

Whether you're doing this online or on a paper form, you need to provide a clear and concise summary of what went wrong. This is not the place for emotional rants. Stick to the facts. Use that timeline you created earlier to walk them through the events chronologically.

For example, don't write: "This seller is a total scammer and ripped me off with this piece of junk!"

Instead, try something like this:

"I ordered the product on May 1st. It was delivered on May 10th with a cracked screen (see attached photo). I contacted the merchant on May 11th to request a replacement but have received no response after three follow-up emails sent on May 12th, 14th, and 16th."

See the difference? That factual, evidence-based approach makes your claim far more credible. Upload your single, organized PDF containing all your evidence, and give everything one last look before you hit submit. Once you file, the clock starts ticking on the investigation.

What Happens After You Submit Your Claim

So, you’ve gathered your evidence, filled out the forms, and hit "submit." What now? You've essentially handed the ball to your bank, and the process kicks into gear.

The first thing you’ll likely see is a temporary credit for the disputed amount hitting your account, sometimes in just a few days. It feels like a win, but hold on—this is just a temporary refund while the bank conducts its investigation. It's not permanent... yet.

Now the spotlight turns to the merchant. They get their chance to respond to your claim in a process called representment. Typically, they have 30 to 45 days to gather their own evidence and argue that the charge was perfectly legitimate.

The Investigation Unfolds

This is where things get interesting. Your bank (the issuer) and the merchant’s bank (the acquirer) start a formal back-and-forth, reviewing the evidence from both sides. The big card networks like Visa and Mastercard set the rules for this whole dance, but they usually stay on the sidelines unless the dispute gets escalated.

Your bank is looking for a clear-cut reason to rule in your favor. If the merchant misses their deadline to respond or sends back a flimsy argument, that temporary credit becomes permanent. Case closed, you win.

Think of a chargeback less like a simple refund and more like a formal, evidence-based debate. The system is built to give both you and the merchant a fair shot to prove your case. The biggest takeaway? Be patient. A final decision can take anywhere from a few weeks to a couple of months.

Don't underestimate the merchant's motivation to fight back. Chargebacks are a huge pain for businesses. Banks charge them between $9.08 and $10.32 just to process a single claim. With global chargeback volumes projected to reach 324 million by 2028, these fees add up fast. You can dig deeper into the true cost of chargebacks and their impact on businesses on Mastercard.com.

Responding to a Merchant Challenge

What happens if the merchant comes back with a strong counter-argument? Maybe they have a delivery confirmation with a signature that looks like yours, or server logs showing you logged in and used their digital service.

If their evidence is compelling, your bank might reverse the temporary credit. You’ll get a notification explaining that the merchant has challenged your claim.

This isn’t the end of the road, so don’t panic. You usually get one more chance to respond and refute their evidence. This is where you can point out that the signature isn't yours or provide other proof to counter their claims.

This rebuttal stage is absolutely critical. If your initial evidence was solid and well-organized, your position is much stronger. It helps to understand how often merchants win chargeback disputes to get a sense of what you're up against. A well-prepared, final response can be the one thing that tips the scales in your favor.

Common Mistakes That Can Cost You the Dispute

Knowing the steps to file a chargeback is only half the story. The other half is dodging the simple mistakes that can get your claim tossed out before it even gets a serious look. I've seen countless valid disputes fail not because the claim was weak, but because of small, completely avoidable errors.

One of the most common tripwires is just waiting too long. Banks are incredibly strict about this. You’ve typically got a window of 60 to 120 days from the transaction date to get your dispute filed. Miss that deadline, and it’s an automatic loss, no matter how solid your evidence is.

Another frequent misstep is throwing a messy pile of proof at the bank. If the person reviewing your case has to sift through a confusing jumble of screenshots and rambling emails, they're more likely to side with the merchant. Your job is to make it dead simple for them to agree with you.

Not Talking to the Merchant First

I know we've said it before, but it's worth repeating because it's the number one reason disputes get denied right out of the gate. Your bank fully expects—and often requires—you to have made a genuine effort to solve the problem directly with the business first.

Skipping this step hands the merchant an easy win. All they have to do is show the bank you never even tried to contact them, and your case is likely dead on arrival. Always, always document your attempts to communicate, even if all you get is silence.

The whole point of the chargeback system is to be a last resort when direct resolution fails. If you jump straight to a chargeback, you're signaling to the bank that you haven't used all the tools available, which seriously weakens your position.

The Pitfall of Friendly Fraud

Then we have the tricky issue of friendly fraud. This is what happens when a customer disputes a completely legitimate charge. Sometimes it's an accident, like forgetting about a recurring subscription. Other times, it’s intentional—a way to try and get something for free.

The consequences here can be a lot more severe than just losing the dispute.

- You could get blacklisted: The merchant can simply refuse to sell to you ever again.

- Your bank account could be at risk: Banks do not appreciate customers who file frivolous disputes and have been known to close accounts over it.

- It hurts everyone: Widespread friendly fraud drives up costs for businesses, which eventually get passed on to all consumers.

With the explosion of online shopping, disputes have become more common. In fact, global chargeback volumes are projected to hit 337 million by 2025. That’s a staggering 27% jump from 2022, driven mostly by card-not-present transactions. While the US has a fairly low chargeback rate of 0.47%, that still translates to a massive number of disputes.

You can dig into more of these chargeback statistics and trends at Chargeblast.com. This data really drives home why it's so critical to be absolutely certain your dispute is legitimate before you pull the trigger.

Frequently Asked Questions About Chargebacks

Even after walking through the process, a few questions always seem to pop up. Let's tackle some of the most common ones I hear to make sure you're feeling confident about your dispute.

Will a Chargeback Hurt My Credit Score?

This is a big one, and I get it completely. The good news is the short answer is no, it won't.

Filing a chargeback for a transaction on your credit card statement doesn't directly ding your credit score. Think of it as a consumer protection feature built into your card—using it isn't a black mark against your credit history.

Credit bureaus like Experian and TransUnion don't receive reports from your bank about your chargeback activity. Now, if the dispute is tied to a missed payment that led to the chargeback, that late payment itself could be reported and affect your score. But the act of filing the chargeback? That’s neutral.

What Happens if My Chargeback Is Denied?

Seeing a "denied" status on your chargeback can feel like hitting a brick wall, but it’s not always the end of the road. Your first move should be to dig into the bank's reason for the denial. Was a deadline missed? Did you not provide enough evidence?

If you have new, compelling proof you didn't include the first time around, you can often appeal the decision or even re-file the dispute. This is your chance to directly address why the initial claim was rejected. For instance, if the merchant claimed the charge was authorized, you could come back with more specific proof showing it was fraudulent.

Sometimes, the simplest path forward is to go back to the merchant one last time with the denial notice from your bank. Seeing that the bank has been involved can sometimes be the final push they need to issue a refund and avoid any more hassle.

A chargeback denial isn't a final verdict. It’s a signal to reassess your case, beef up your evidence, and try another angle if you need to.

Credit vs. Debit Card Chargebacks

The process might look similar on the surface, but there's a world of difference under the hood. When you dispute a credit card charge, the money in question is the bank's. You typically get a temporary credit while they go to bat for you, giving you significant protection under the Fair Credit Billing Act (FCBA).

With a debit card, that money comes straight out of your bank account. It's your cash that's gone. While you still have protections under the Electronic Fund Transfer Act (EFTA), you're out the money until you win the dispute. Banks can sometimes be less aggressive in fighting for you, and the timelines are often much tighter. This is exactly why using a credit card for online shopping or big-ticket items gives you a much stronger safety net.

Finally, remember that merchants face real costs when a dispute is filed against them. To get a better sense of these expenses, you can explore the details of what a chargeback fee entails and see why businesses work so hard to avoid them.

At ChargePay, we specialize in helping merchants navigate the complexities of chargeback disputes with AI-powered automation. By generating winning responses in real-time, we recover lost revenue and protect your bottom line, so you can focus on growing your business. Discover how ChargePay can transform your chargeback management.

.svg)

.svg)

.svg)

.svg)