Let's be honest, "presentment" is one of those industry terms that sounds way more complicated than it actually is. For any merchant, it really boils down to two key things. First, it's the everyday, behind-the-scenes action of sending a customer's transaction to their bank to get paid. Easy enough.

But the second meaning? That’s the one you really need to care about. When a customer files a chargeback, your presentment is your chance to fight back. It’s the collection of evidence you present to prove the sale was legitimate so you can get your money back.

Understanding the Two Sides of Presentment

When you hear the word "presentment," it can feel like insider jargon, but it breaks down into two straightforward ideas that directly impact your daily operations and, more importantly, your bottom line. Getting a handle on both is the first step toward protecting the revenue you've worked so hard to earn.

The first meaning of presentment is pretty routine. It’s the initial process where your payment processor "presents" a customer’s transaction details to their bank to collect the funds. For most businesses, especially those on powerful e-commerce platforms like Shopify, this is completely automated. You make a sale, the system does its thing, and the money shows up. It happens thousands of times a day without a hitch.

Why the Second Meaning Matters More

The second, and far more critical, meaning of presentment kicks in when a transaction goes sideways. A customer disputes a charge, their bank initiates a bank chargeback, and suddenly, the funds are yanked from your account.

This is where your presentment becomes your defense. It's your formal, evidence-backed response to the bank, proving the charge was valid and you held up your end of the deal.

Think of it like this: a chargeback is the prosecution's opening statement claiming you're at fault. Your presentment is your defense attorney's case, complete with receipts, shipping confirmations, and customer emails as hard evidence.

To help you keep these two concepts straight, here’s a quick breakdown:

The Two Sides of Presentment

This process of defending yourself is becoming more important than ever. With global chargeback cases projected to soar to 337 million by 2025, the financial pressure on merchants is immense. Successfully presenting your case is your primary weapon for recovering lost funds in this tough situation. Understanding the mechanics of a chargeback is the first step to building a winning defense.

A Step-by-Step Look at the Chargeback Process

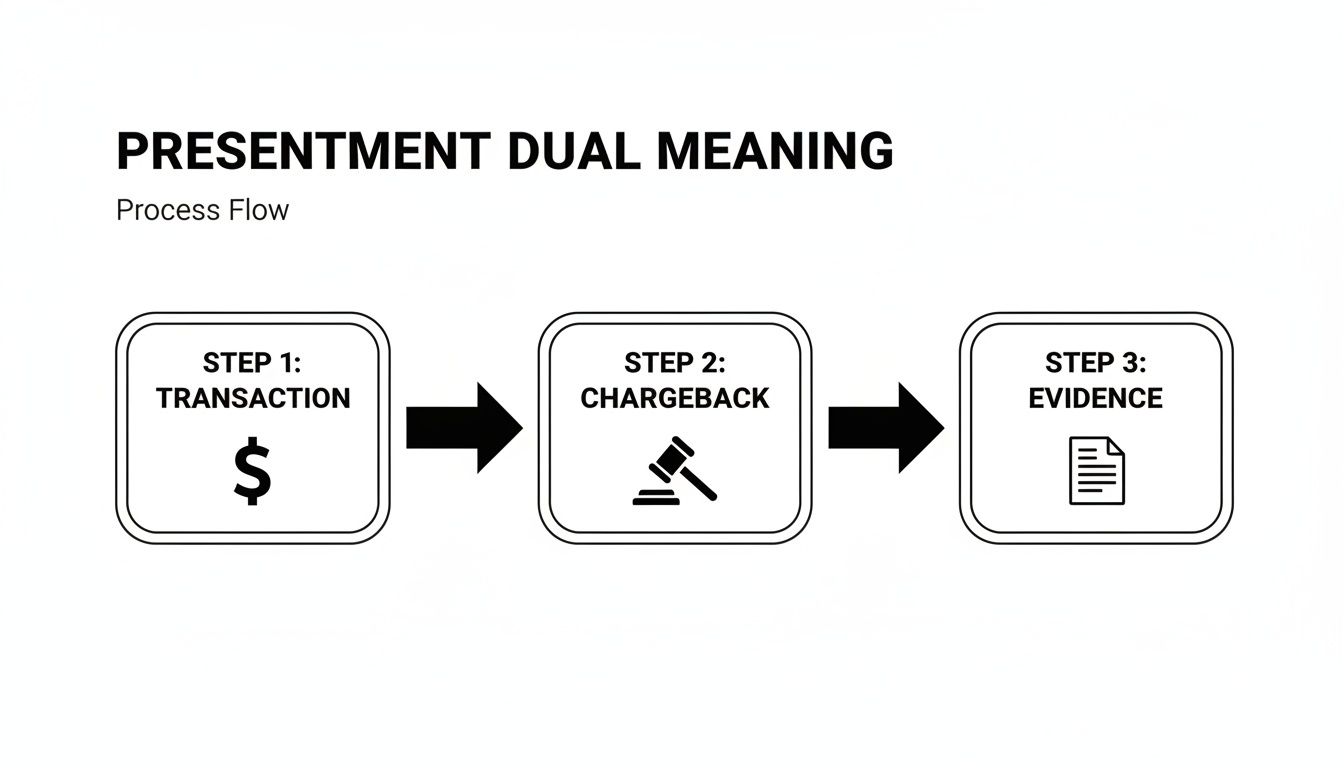

To really get what presentment means in a dispute, it helps to see where it slots into the bigger picture. The whole chargeback system can feel like a tangled mess, but it actually follows a pretty clear path. Think of it as a relay race where the baton gets passed from the customer, to their bank, and finally to you.

It all starts with a simple transaction—a customer buys something from you. But then, days or even weeks later, they decide to dispute the charge and call their bank. That's the starting gun. The customer's bank takes a look at the claim, and if it seems plausible, they kick off the chargeback and pull the funds right out of your account.

That’s when you get a notification about the dispute, which officially starts the clock on your response time. This is your window to take action.

The Merchant's Turn to Respond

This is exactly where your presentment comes into play. It’s your turn to step up to the plate. You gather up all your evidence—things like shipping confirmations, any emails you exchanged with the customer, and transaction details—and submit it to the bank. This whole package of proof is your presentment.

The flow chart below breaks down how this works, from the initial transaction to you submitting your evidence.

As you can see, a straightforward sale can quickly turn into a formal dispute. Your evidence-based presentment is the key to turning the situation around.

Unpacking the Timeline

Getting the sequence of events down is crucial because the deadlines are no joke. For a complete picture of the entire process, it's a good idea to understand what is a chargeback in banking, from its inner workings to protective strategies. Once that chargeback notification hits your inbox, you typically have between 7 and 45 days to respond, depending on the card network.

Here’s how the steps usually unfold:

- Initial Transaction: The customer makes a purchase.

- Customer Dispute: The cardholder calls their issuing bank to question the charge.

- Chargeback Initiated: The issuing bank files the chargeback, and the funds are temporarily taken from your merchant account.

- Merchant Notification: You get a formal heads-up about the dispute from your acquiring bank or payment processor.

- Evidence Submission (Presentment): You pull together and send in your compelling evidence to fight the chargeback.

This five-step process is the standard playbook for almost every dispute. If you miss your window in step five, it's an automatic loss. That makes your presentment the single most important action you can take.

Once you’ve submitted your evidence, the issuing bank reviews everything from both sides and makes the final call. If you win, the funds are returned to you. To get more comfortable with these stages, check out our guide on the complete card dispute process. Knowing this workflow inside and out demystifies the whole system and puts you in a much stronger position to protect your revenue.

Building Your Case with the Right Evidence

When that chargeback notification hits your inbox, the game changes. From that moment on, the single most important factor determining whether you win or lose is the quality of your evidence. A strong presentment is more than just dumping a few documents on the bank; it’s about telling a clear, undeniable story that proves the transaction was legitimate.

Think of yourself as a detective building a case. Every piece of data you gather helps paint a complete picture for the issuing bank, leaving them with no room for doubt.

For any dispute, some evidence is always a good starting point. This includes the basics, like the transaction amount, date, and time, plus a clear description of what was purchased. These foundational details set the stage for the more specific proof you’ll need to win.

Tailoring Evidence to the Claim

Here's where merchants often stumble: you can't use a one-size-fits-all approach. The key to a successful presentment is tailoring your evidence to the specific reason for the chargeback. A claim of an "unauthorized transaction" demands a completely different set of proofs than a claim that the "product was not received." Generic responses are a fast track to losing.

Let's say a customer claims they never authorized the payment. Your mission is to prove they were the one who clicked "buy." This is where their digital fingerprints become your best friend.

- IP Address: Show that the order was placed from an IP address matching the customer's known location or their past order history.

- AVS & CVV Results: Always provide proof of successful Address Verification System (AVS) and Card Verification Value (CVV) checks. A match is powerful evidence that the cardholder was physically involved.

- Customer Communications: Dig up any emails, chat logs, or support tickets where the customer discusses the purchase or a related topic.

By weaving these data points together, you create a compelling narrative that connects the cardholder directly to the transaction. It shifts the dispute from a frustrating "he said, she said" scenario to a defense backed by hard data.

Proving Delivery and Satisfaction

When the chargeback reason is "product not received," your focus shifts entirely. Now, it's all about proving successful delivery. Your shipping and fulfillment records are your star witnesses here, and you need more than a simple receipt. You have to prove the item made it all the way to the customer’s doorstep.

- Shipping Confirmation: Provide the tracking number and a direct link to the carrier’s tracking page showing the delivery status.

- Proof of Delivery: This is the gold standard. A delivery confirmation with a signature or a photo of the package at the customer's address is incredibly persuasive.

- Digital Goods: For digital products, provide server or application logs showing the customer downloaded the file, logged in to access the service, or used the software.

To help you get started, here’s a quick-glance table for some of the most common chargeback reasons. Think of it as your cheat sheet for what to grab when a dispute comes in.

Evidence Checklist for Common Chargebacks

Remember, this isn't an exhaustive list, but it's the foundation for building a rock-solid case. The more relevant details you can provide, the better your odds.

Mastering this evidence-gathering process is what separates merchants who recover revenue from those who write it off as a loss. In fact, a staggering 75% of friendly fraud cases can be successfully disputed with compelling proof. Understanding how to organize and present this evidence is your key to a better win rate. For a deeper dive, check out our full guide on how to win a credit card dispute.

The Hidden Costs of Manual Presentment

Handling chargeback presentments on your own can feel like a savvy way to sidestep extra costs. But in reality, it's often a classic case of being penny-wise and pound-foolish. The truth is that manual dispute management carries a steep, often invisible, price tag that goes far beyond the disputed amount.

The most immediate cost? Your time. Every minute you or your team spends digging through order histories, pulling up shipping confirmations, and piecing together a response is a minute not spent on growing the business. It's a frustrating diversion from the very things that actually generate revenue—marketing, product development, and customer service.

The Financial Drain of DIY Disputes

Beyond the lost hours, there are direct financial risks that can pile up fast. Chargeback deadlines are notoriously tight, and missing a single response window means an automatic loss. Submitting a weak or incomplete presentment is just as bad; it virtually guarantees the bank will side with their cardholder.

This is exactly where manual efforts tend to fall short. Without a structured process, it’s easy to overlook critical evidence, which leads directly to lower win rates and a steady drain on your revenue.

The real cost isn't just the chargeback amount. It's the lost revenue from preventable losses, the wasted payroll hours, and the missed opportunities while your team is stuck managing paperwork.

These hidden costs force businesses into tough corners. In fact, a staggering 33% of merchants admit to raising their prices just to offset the financial hit from disputes. That ultimately passes $117.46 billion in costs on to their own customers.

Automation: The Clear Advantage

This is where automated solutions completely change the game, flipping the script on manual inefficiency. Instead of just reacting to disputes as they come in, these systems proactively build and submit evidence-rich presentment cases on your behalf.

Here’s a quick look at how automation stacks up against the old-school manual approach:

The difference is night and day. Automation doesn't just save you time; it directly translates to higher recovery rates and a much healthier bottom line. For more on how this works, check out our complete guide to automated chargeback and dispute management using AI.

By taking human error and tight deadlines out of the equation, you put your business in the strongest possible position to win.

Making Presentment and Representment Clear

In the world of payments, you're going to run into two terms that sound almost identical but couldn't be more different: presentment and representment. It’s incredibly easy to mix them up, but getting the distinction right is the key to successfully navigating the chargeback process.

Let's clear up the confusion once and for all.

We've already touched on how "presentment" can be the simple, everyday act of sending a transaction to a customer's bank for payment. But when a dispute pops up, it takes on a whole new meaning. In this context, it's your evidence-backed response to a chargeback.

The Key Difference: Representment

Representment, on the other hand, is a very specific action. It’s the formal process where you re-present a transaction to the cardholder's bank after a chargeback has been filed, armed with compelling evidence to prove the charge was legitimate.

Think of it like this:

Presentment is like handing your ticket to the cashier to buy a movie ticket. It's the first, standard exchange. Representment is like going back to the manager with your receipt and ticket stub to argue your case after someone else claimed your seat was theirs and you were kicked out.

You are literally "presenting the charge again" (re-presenting it), but this time you’re coming back with proof to back up your claim.

Why This Distinction Matters

So, why get hung up on the terminology? While many people use "presentment" and "representment" interchangeably when talking about fighting chargebacks, knowing the technical difference helps you understand exactly what stage of the fight you're in. It adds a layer of precision when you're talking with your payment processor or a dispute management service.

The initial transaction is the first presentment; your battle to reclaim the funds is the representment.

Basically, representment is the action you take to reverse a chargeback. For a deeper dive into building a winning case, our guide on chargeback representment has some fantastic insights.

This entire process is controlled by strict rules from the card networks. For example, you have a tight window to respond—usually within 30 days of the chargeback—and your evidence has to directly address the specific reason for the dispute. It’s this structure that keeps the process fair but also makes it a real challenge for merchants trying to handle it all manually.

Ultimately, a successful representment means you’ve defended the transaction, won the dispute, and recovered your revenue.

Common Questions About Presentment Answered

We’ve covered a lot of ground on what presentment means and how it shows up in your business. To wrap things up, let's go through some of the most common questions merchants have about the whole process.

Think of this as a quick-reference guide to clear up any lingering doubts so you can feel ready to handle your next dispute with confidence.

What Happens If My Presentment Is Denied?

It's a frustrating outcome, but when an issuing bank denies your initial presentment, the chargeback stands. The money stays with the customer. However, this isn't always the end of the road.

Depending on the card network’s rules, you might still have options. For Visa and Mastercard, the next step is a process called pre-arbitration. For American Express and Discover, it's called a second chargeback. Both are essentially an appeal. If that also fails, the final stage is arbitration, a formal and often expensive process where the card network itself plays judge.

Because these later stages get more complex and costly, it’s absolutely critical to put your best foot forward the first time. A strong, evidence-packed initial presentment gives you the best shot at winning outright and skipping these complicated follow-up rounds.

How Long Do I Have to Submit My Evidence?

Time is not on your side when a chargeback hits. The clock starts ticking the moment you get that dispute notification, and the deadlines are rigid. Miss the window, and you automatically lose the dispute and the revenue. No exceptions.

The exact timeframe depends on the card network (Visa, Mastercard, etc.) and the reason for the chargeback, but you typically have between 7 and 45 days to respond. This tight turnaround is one of the biggest challenges for merchants trying to manage disputes on their own. It only takes one missed email or a delay in gathering documents to lose the case.

A missed deadline is an automatic forfeit. There are no extensions or second chances, which is why having a system to track and respond to every dispute promptly is essential for protecting your bottom line.

Should I Fight Every Single Chargeback?

While the gut reaction might be to fight every dispute that comes your way, it’s not always the smartest move. The key is knowing which battles are worth fighting and which are better left alone. Let's be honest, some cases just aren't winnable.

For instance, if a chargeback is due to clear-cut "true fraud" and you have very little evidence connecting the legitimate cardholder to the purchase, your odds of winning are slim. Pouring time and resources into a lost cause can be more expensive than just accepting the loss.

This is where a little strategy goes a long way. You need to evaluate each case based on two things:

- The evidence you have: Do you have compelling proof like AVS/CVV matches, shipping confirmation with a signature, and customer communications?

- The reason for the dispute: Some chargeback reason codes are notoriously harder to fight than others.

A strategic approach means focusing your energy on the disputes you have a high probability of winning. This maximizes your return and keeps you from spinning your wheels on unwinnable cases.

When Do I Get My Money Back After Winning?

This is the question every merchant wants answered. The good news is that when you win a presentment, the funds that were provisionally taken from your account are returned to you. A successful presentment means recovered revenue.

The timing isn't instant, but it's pretty quick. Once the issuing bank confirms the win, you can typically expect to see the funds credited back to your merchant account within a few business days to a couple of weeks. This officially closes the case in your favor.

Stop letting chargebacks chip away at your profits. ChargePay uses AI to automate the entire dispute process, building and submitting winning evidence for you. Recover up to 80% of lost revenue without lifting a finger. Learn how ChargePay can protect your business today.

.svg)

.svg)

.svg)

.svg)