If you're an online merchant, you've probably learned the hard way that chargebacks are more than just lost sales. They’re a multi-layered threat to your bottom line, and having a plan isn't just a good idea—it's essential for survival.

Protecting your business means more than just fighting disputes as they come in. It’s about preventing them from ever happening in the first place and having a rock-solid system to manage the ones that inevitably slip through.

Understanding the Real Cost of Chargebacks

It’s easy to look at a chargeback as a simple reversed transaction. A customer disputes a charge, you lose the sale, and you move on. But that’s only the tip of the iceberg. The real financial damage runs much, much deeper.

Every single time a chargeback hits your account, you're not just refunding the sale. You're also slapped with a separate chargeback fee from your payment processor. These fees can sting, usually falling somewhere between $20 and $100 per incident. For a deeper dive, check out our guide on what a chargeback fee is and how it works.

Add to that the fact that you’ve also lost the merchandise you shipped and the money you spent on shipping. All of a sudden, a single dispute has a ripple effect, costing you far more than the original order value.

The Different Faces of Chargebacks

Not all chargebacks are the same. They generally fall into a few key categories, and understanding the difference is absolutely critical if you want to build an effective defense.

- Criminal Fraud: This is the one we all think of first—a stolen credit card used for a purchase. It’s straight-up theft. While your fraud filters will catch a lot of these, some will always get through the cracks.

- Merchant Error: These are the "oops" moments that happen on your end. Maybe you shipped the wrong size, a product arrived damaged, or your billing descriptor was so generic the customer had no idea who charged them. The good news? These are almost entirely preventable with better internal processes.

- Friendly Fraud: This is easily the most frustrating and fastest-growing category. Here, a legitimate customer buys something, receives it, and then files a chargeback. It could be buyer's remorse, confusion about your return policy, or, unfortunately, someone trying to get something for free.

The rise of "friendly fraud" is a massive headache for online businesses. Reports now show that a staggering 72% of merchants have seen an increase in these cases, where perfectly legitimate transactions are disputed by the cardholder.

Why Chargebacks Are on the Rise

The explosion of e-commerce has made card-not-present (CNP) transactions the new normal, which naturally opens the door for more disputes. It's a big number, but global chargeback cases are projected to hit 337 million by 2025.

This surge is fueled by evolving consumer habits and the expectation for instant, frictionless everything. In this environment, a proactive chargeback plan isn't optional anymore. It's a core part of running a sustainable online business.

This is why a robust strategy isn't just about damage control. It's about protecting your revenue, keeping your payment processor happy, and making sure your business can actually thrive without being bled dry by hidden fees and operational nightmares.

Building Your Proactive Prevention Plan

The easiest chargeback to win is the one that never happens. I've seen it time and time again: merchants who shift from a reactive "firefighting" mode to a proactive mindset completely change their business. It’s all about building a strong defense that stops disputes before they even have a chance to start.

This means shoring up your checkout process and getting your internal policies ironed out. The goal is simple: remove the common triggers for disputes, whether it's customer confusion, mismatched expectations, or just being an easy target for fraudsters.

Fortify Your Checkout Process

Think of your checkout page as the front line in your battle against chargebacks. This is where you can deploy some powerful—yet surprisingly simple—fraud detection tools that screen transactions in real time. They're your digital gatekeepers.

Here are the non-negotiables I recommend to every merchant:

- CVV Checks: Always, always require the three- or four-digit security code from the back of the card. It’s a basic but effective step to confirm the customer actually has the card in their hand.

- Address Verification Service (AVS): This tool is your best friend. It checks the billing address the customer enters against the one the card issuer has on file. Any mismatch is a major red flag for potential fraud.

- 3D Secure (e.g., Verified by Visa, Mastercard SecureCode): This adds an extra authentication step, often a password or a one-time code sent to the cardholder's phone. It's a fantastic deterrent against unauthorized card use.

Putting these tools in place creates just enough friction to stop fraudsters in their tracks, all while keeping the checkout experience smooth for your legitimate customers. They are foundational to any solid prevention strategy. For a deeper dive, you can explore our complete guide on chargeback prevention tactics.

Communication Is Your Best Ally

Beyond the tech, clear and consistent communication is one of your most effective weapons against disputes—especially the tricky "friendly fraud" kind. So many chargebacks happen simply because a customer is confused, surprised by a charge, or can't get a quick answer to a problem.

A customer who can easily contact you is far less likely to file a chargeback. Make your customer service contact information—email, phone number, and live chat—impossible to miss. It should be on every page of your site, especially on order confirmation and shipping notification emails.

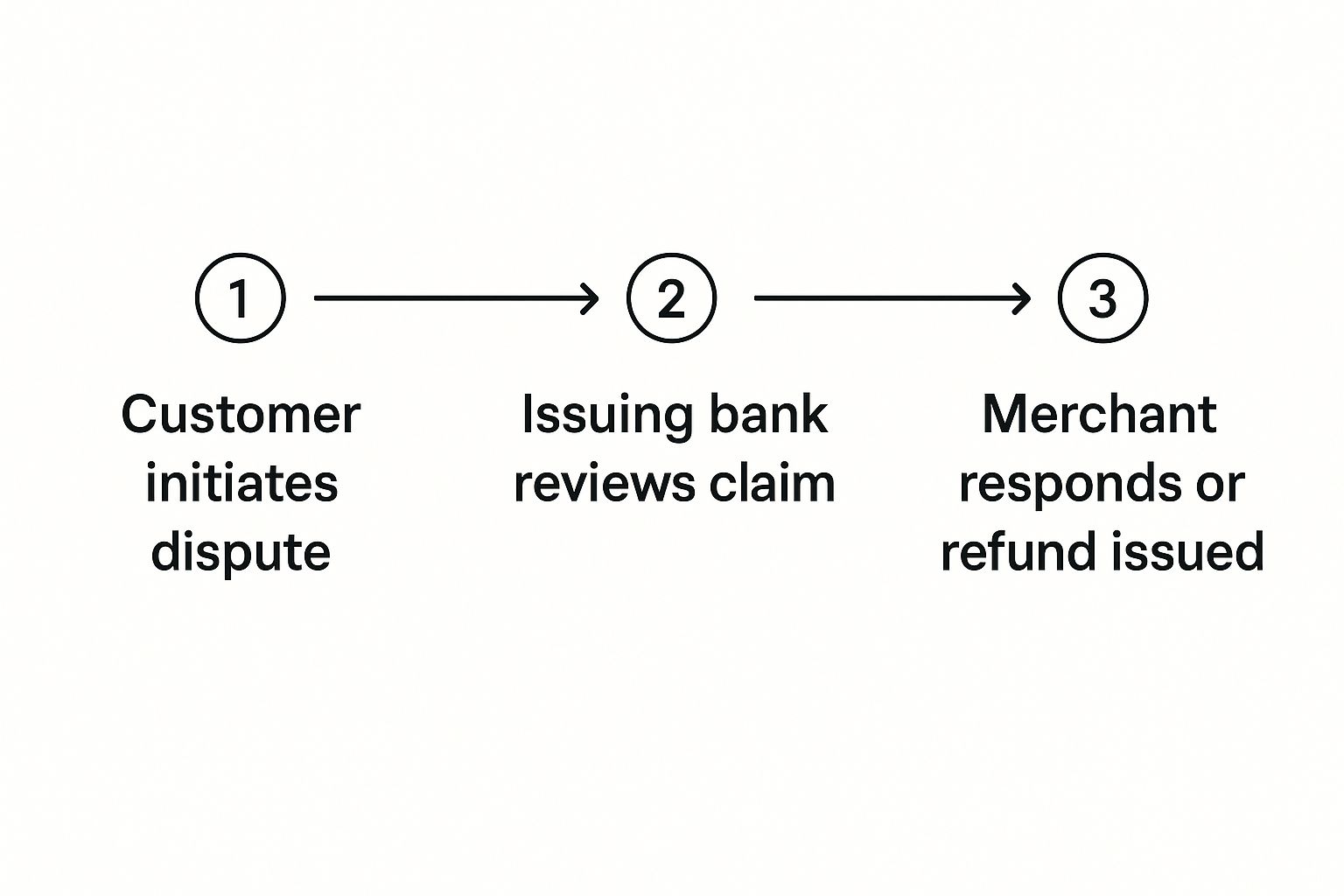

This chart gives you a quick visual of the dispute lifecycle.

Notice how the moment a dispute is initiated, the bank gets involved. That's when things get complicated and costly. Your goal is to intercept that customer's issue before they even think about calling their bank.

Set Crystal-Clear Expectations

Ambiguity is the enemy of a low chargeback rate. Period. You need to make absolutely sure your customers know exactly what they're buying and what to expect after they click that purchase button.

Focus on locking down these key areas:

- Detailed Product Descriptions: Go beyond the basics. Include dimensions, materials, care instructions—anything a customer might need to know. High-quality photos and videos from multiple angles are a must. A great resource for this is this guide on ecommerce product page optimization.

- Transparent Policies: Your shipping, return, and refund policies should be easy to find and written in plain English. Ditch the legal jargon that could confuse or intimidate customers.

- Clear Billing Descriptors: Make sure the name that shows up on your customer's credit card statement is instantly recognizable. A generic or confusing descriptor like "SP WEBSERVICES" is a top reason for "I don't recognize this charge" disputes. Use your store name, not a holding company name.

To help you get a handle on this, here’s a quick-reference table summarizing the key tactics.

Key Chargeback Prevention Tactics at a Glance

This table breaks down some essential prevention measures and how they directly protect your business from different types of disputes.

By building this proactive framework, you create an environment where fraudulent transactions are harder to complete and legitimate customers have fewer reasons to file a dispute in the first place. This foundation isn't just about saving money on chargebacks; it's about building a more resilient and profitable business.

Spotting Red Flags After the Sale

Even with the best fraud prevention tools at checkout, some sketchy orders are bound to slip through. That window of time right after a customer hits 'buy' is your last chance to catch something fishy before you ship the product.

Think of this as your second line of defense. It’s a quick, manual review of orders that just don't feel right. A solid chargeback protection strategy doesn’t end when the payment goes through; it keeps going until that package is on the truck.

Common Transactional Red Flags

Your order queue is a goldmine of data if you know what to look for. Over time, you’ll develop a sixth sense for spotting unusual patterns that can save you a fortune. While one red flag might not mean much, a few of them together should definitely make you pause.

Here are some of the classic signs that an order might be fraudulent:

- Mismatched Addresses: This is fraud detection 101. When the billing address is in New York but the shipping address is in California, it’s worth a closer look. Drastically different locations, especially different countries, are a major warning sign.

- Unusually Large First-Time Orders: A brand-new customer dropping a massive order way above your average ticket price? That's suspicious. Fraudsters using stolen cards often try to max them out quickly before they get shut down.

- A Flurry of Rapid Orders: Watch out for multiple orders to the same address using different credit cards, all placed in a short time frame. This often means someone is burning through a list of stolen card numbers to see which ones work.

- Odd Email Addresses: An email like

j8f7d9s0a@email.comor one from a known disposable email service should raise your eyebrows. Real customers usually have an email that includes their name or something recognizable.

When you're reviewing orders, trust your gut. If a transaction just feels 'off'—maybe the items they bought make no sense together or the customer's name doesn't match their email—it’s always better to hold the shipment and verify.

The Power of Post-Purchase Communication

While you’re on the hunt for fraud, don’t forget that clear communication with all your customers is one of the best ways to prevent chargebacks—especially the "friendly fraud" kind. A lot of the time, a customer initiates a chargeback because they’re confused or just impatient.

Good communication reassures legitimate buyers and can spook fraudsters who prefer to stay under the radar.

Building Trust After the Transaction

A few simple, automated emails can make all the difference in stopping buyer’s remorse from turning into a dispute. It's all about managing expectations and building trust from the get-go.

- Immediate Order Confirmation: The moment an order is placed, fire off a detailed confirmation email. It needs to include the order number, a full list of items, the total cost, and the shipping address. This gives the customer a chance to catch any mistakes right away.

- Clear Shipping Updates: Send another email as soon as the package ships, and make sure it has the tracking number. This simple step proactively answers the dreaded "Where is my order?" question before the customer even thinks to ask their bank.

These small touches reinforce that you’re a legitimate, professional business. It’s often the stores with poor post-sale communication that become easy targets for opportunistic disputes. To learn more about this common problem, check out our deep dive on friendly fraud. By keeping your customers in the loop, you shut down a whole category of preventable chargebacks.

How to Fight and Win Chargeback Disputes

When that chargeback notification lands in your inbox, it's easy to feel your stomach drop. It’s frustrating, and it can feel like you’re powerless. But just accepting the loss isn't your only move. With the right game plan, you can fight back and win—and you absolutely should.

Think of it like you're building a legal case. The bank acts as the judge, and your job is to lay out such clear, compelling evidence that they have no choice but to rule in your favor. This isn't about getting into an argument; it's about presenting undeniable facts that shut down the dispute.

And make no mistake, this is a skill you need to master. Projections show the sheer volume of chargebacks is set to climb from 261 million in 2025 to a staggering 324 million by 2028. That's a 24% jump in just three years, mostly fueled by the endless growth of online shopping. Knowing how to fight back is more critical than ever. You can see more on these trends in these chargeback statistics and what they mean for merchants.

Gather Your Evidence Like a Detective

The moment a dispute is filed, a timer starts. You typically only have a few weeks to respond, so you need to act fast. Your first and most important step is to gather every single piece of information tied to that transaction.

Your goal here is to paint a complete picture of a legitimate, fulfilled order. Don't leave anything out, no matter how small it might seem.

Here’s the essential evidence you need to pull together immediately:

- Transaction Details: The basics—order date, exact amount, and the authorization approval code.

- Customer Information: Grab the customer's name, email, and the IP address they used at checkout.

- Proof of Delivery: This is the big one. It's non-negotiable. You need shipping confirmation with a tracking number that shows the item was delivered to the address the customer provided. If you have signature confirmation, that's even better.

- Communication Records: Dig up any and all emails, live chat transcripts, or support tickets between you and the customer. This can prove you addressed their concerns, or even better, that they never bothered to contact you before filing the dispute.

- Product & Policy Proof: Include a copy of the product description from your site and a link to your return and shipping policies. This directly counters claims like "item not as described" or that your terms were hidden.

This collection of evidence is the foundation of your entire defense. A well-organized file is what separates a rushed, weak response from a powerful, convincing case that wins.

Write a Powerful Rebuttal Letter

Your rebuttal letter is your one and only chance to speak directly to the bank investigator reviewing the case. Keep it professional, to the point, and focused strictly on the facts. Don't let emotion or frustration creep in; let the evidence do the talking.

Start by clearly stating you are disputing the chargeback. Then, get straight to the point: you need to directly address the specific reason code provided with the dispute. For example, if the code is for "Product Not Received," your entire response should be laser-focused on proving delivery.

Your rebuttal letter isn’t a place for storytelling. It's a formal, fact-based document. Structure it with clear headings and bullet points to make it incredibly easy for the bank employee to scan and understand your key points in seconds.

A strong rebuttal letter follows a simple, clear structure:

- Introduction: State the case number, transaction details, and that you are challenging the dispute.

- Addressing the Reason Code: Explain why the chargeback is invalid, tying it directly back to the reason code.

- Presenting Evidence: Systematically list the evidence you've attached. Make it easy for them (e.g., "See Exhibit A: Proof of Delivery," "See Exhibit B: Customer Email Correspondence").

- Conclusion: Briefly summarize why the charge was legitimate and formally request that the chargeback be reversed.

This structured approach makes your argument easy to follow and infinitely more persuasive.

Understanding Deadlines and Reason Codes

Every chargeback comes with two critical pieces of information you absolutely cannot ignore: the response deadline and the reason code. If you miss that deadline, it's an automatic loss. Period. It doesn't matter how solid your evidence is.

Reason codes are the bank’s shorthand for why the customer filed the dispute. Each card network (Visa, Mastercard, Amex) has its own set of codes, but they usually fall into a few buckets: fraud, authorization problems, or product/service issues. Understanding the code is your key to victory, because it tells you exactly what kind of evidence you need to provide to win.

Fighting chargebacks is a learned skill, but it’s an essential part of effective merchant protection from chargeback. Every dispute you win sends a clear message that your business is not an easy target. For more advanced strategies on this, you can check out our detailed guide on improving your chargeback dispute management.

Using Automation for Smarter Chargeback Management

Let's be honest: fighting every single chargeback by hand is a losing battle, especially as your business grows. The whole process of digging up evidence, writing rebuttals, and racing against tight deadlines is a massive drain on your time and resources. That's time you should be spending on growth, not just damage control.

As you scale, the sheer volume of disputes can become overwhelming. This is the point where automation shifts from a "nice-to-have" to a core part of your defense strategy. It's all about working smarter, not harder, to protect your bottom line.

Specialized software can completely flip the script on how you handle disputes. These tools are built to take over the tedious, repetitive tasks that bog down your team, all while improving your accuracy and win rate. It’s a fundamental shift in how you approach merchant protection from chargeback.

The Real Benefits of Automated Dispute Management

Moving away from manual processes isn't just about saving time; it's about getting better results. Automated systems are designed to navigate the complex, rule-based world of chargeback representment with a level of precision that's nearly impossible to achieve by hand.

Think about the advantages:

- Boosted Win Rates: The best systems analyze data from thousands of past disputes to craft the most effective rebuttal for each specific reason code. They know exactly what evidence the banks want to see and how to present it for the best chance of success.

- Reclaimed Time and Resources: Imagine freeing up your team from hours of digging through order histories and writing letters. Automation handles the heavy lifting, allowing your staff to focus on customer service and business growth.

- Error-Free Submissions: Missing a deadline or submitting incomplete evidence means an automatic loss. Automation ensures every response is submitted correctly and on time, every single time.

This isn't just theory. For a solid foundation on how these systems work, understanding workflow automation is a great starting point. It shows how structured, automated processes can eliminate human error and drive efficiency.

One of the biggest wins with automation is consistency. Whether you have one chargeback a month or one hundred, the system handles each with the same high level of detail and accuracy, ensuring nothing ever falls through the cracks.

How Automation Transforms Your Defense

So, what does an automated system actually do? It connects directly to your sales and payment platforms to streamline the entire dispute lifecycle, from the initial alert to the final resolution.

The process is pretty straightforward:

- It Gathers Evidence Automatically: The moment a chargeback is filed, the system instantly pulls all relevant data. We're talking transaction details, customer information, AVS/CVV results, shipping confirmations, and even communication logs.

- It Builds a Smart Rebuttal: Using that evidence, the software generates a powerful, well-structured rebuttal letter. It’s tailored to the specific reason code and presents your case in the format banks prefer.

- It Submits Everything for You: The complete dispute package—the rebuttal letter and all supporting evidence—is automatically submitted to the payment processor on your behalf. You barely have to lift a finger.

This end-to-end process dramatically increases the speed and effectiveness of your responses. To see how AI supercharges this, check out our complete guide to automated chargeback and dispute management using AI.

Choosing the Right Automation Solution

Not all chargeback automation tools are created equal. When you're looking at different options, you need to find features that provide true, hands-off management and deliver results you can actually see.

To put it in perspective, here’s a quick comparison of what separates a basic manual process from a truly effective automated solution.

Manual vs. Automated Chargeback Management

The table below highlights the key differences in efficiency, cost, and success rates between sticking with a manual approach and upgrading to automation.

When you're ready to make the switch, look for a solution like ChargePay that offers seamless integrations with your existing platforms (like Shopify or PayPal), real-time performance analytics, and a pricing model that aligns with your success. The right partner doesn't just manage your disputes—it becomes a profit recovery center for your business.

Your Top Chargeback Questions, Answered

Even after getting the full rundown, it's totally normal to have a few questions lingering. When it's something as important as protecting your business from chargebacks, you need total clarity. Let's tackle some of the most common questions we hear from merchants every day.

Think of this as your go-to cheat sheet to help you feel confident and ready to put what you've learned into action.

What Is a Chargeback Ratio and Why Does It Matter?

Your chargeback ratio is one of the most important health metrics for your business, plain and simple. It's calculated by dividing the number of chargebacks you get in a month by your total number of transactions that same month.

So, if you had 10 chargebacks and 1,000 transactions, your ratio is 1%.

This number is a huge deal because card networks like Visa and Mastercard use it to figure out how risky your business is. If that ratio creeps up too high—usually anything over 0.9%—you can land in a high-risk monitoring program. That means higher fees, a ton of scrutiny, and in the worst-case scenario, you could lose your merchant account entirely.

How Long Do I Have to Respond to a Chargeback?

When a dispute lands, the clock starts ticking immediately, and it doesn't wait for anyone. The response window is tight and unforgiving.

While the official window can vary a bit between card networks, you typically have somewhere between 20 and 45 days from the filing date to get your evidence submitted.

But here's the catch: many payment processors have their own, much shorter internal deadlines—sometimes as little as 7 to 10 days. They need time to process your case on their end. Miss that window, and it’s an automatic loss, no matter how solid your evidence is.

A classic mistake is putting it off. The second you get that chargeback notification, it's go-time. Start gathering your evidence right away so you can build a strong case without rushing against the deadline.

Can I Just Refund a Customer to Avoid a Chargeback?

Refunding a customer is a fantastic way to solve a problem before they file a chargeback. But once that dispute is officially in the system with their bank, a direct refund won't make it disappear.

At that point, the formal dispute process has already kicked off. You'll still get slapped with the chargeback fee, and the dispute will still count against your ratio. The only way forward is through the official channels: either you accept the dispute or you fight it with compelling evidence.

What’s the Difference Between a Chargeback and a Refund?

This is a critical distinction that trips up a lot of new merchants. Here’s how to think about it:

A Refund: This is a conversation between you and your customer. They reach out with a problem, you agree to give their money back, and you process the credit through your system. It's a voluntary part of good customer service.

A Chargeback: This is a forced reversal started by the customer's bank. The customer goes completely around you and straight to their bank to dispute the charge. It's an involuntary, often hostile process that always comes with fees and penalties for you.

Your goal should always be to create an environment where customers come to you for a refund first, making a chargeback totally unnecessary.

Ready to stop losing revenue to chargebacks and automate your defense? ChargePay uses AI to fight and win disputes for you, boosting your win rate and freeing up your time. Reclaim your revenue with hands-free automation.

.svg)

.svg)

.svg)

.svg)