Fraud isn't a side expense anymore. It's a margin killer hiding inside orders that look normal, customers who sound believable, and disputes that arrive weeks after you already shipped the product.

The number that should reset how you think about this is $12.5 billion in reported consumer fraud losses in 2024, up 25% year over year according to the FTC loss data summarized by Fraud.org. For Shopify merchants, that doesn't stay in the abstract. It turns into unauthorized orders, “item not received” claims, bank disputes, lost inventory, fulfillment waste, and chargeback fees.

If you're running a store, your job isn't to memorize every fraud label. Your job is to understand which payment fraud trends show up as specific customer claims and dispute reason codes, then tighten your process before those orders turn into losses.

Why Fraud Is Costing You More Than You Think

Fraud costs more than the order value you lose. It hits your margin from five directions at once: lost inventory, outbound shipping, reversed revenue, team time, and dispute fees. If you've ever wondered what a chargeback fee does to your margin, start there. That fee lands after the product is gone and the sale has already been pulled back.

The headline number understates the problem

Reported consumer fraud losses reached $12.5 billion in 2024, up 25% year over year and 558% from $1.9 billion five years earlier, while the FTC estimate adjusted for underreporting puts true scam losses at $196 billion. The same summary says only 2% to 6.7% of victims report losses, which means official totals likely miss a large share of fraud across payment channels, wallets, apps, and transfers, as noted earlier.

This is significant because fraud pressure does not stay neatly inside card payments. It shows up in account takeovers, manipulated customers, false “item not received” claims, and disputes that banks sort into reason codes your team has to answer.

For a Shopify merchant, that is the bridge that matters. A broad fraud trend turns into a daily operational problem when it lands as fraudulent transaction, product not received, or credit not processed on a chargeback notice. If you only track the top-line dispute count, you miss the pattern driving the losses.

Practical rule: Review fraud by reason code and customer claim, not just by total chargebacks.

What this looks like inside a Shopify business

A bad order rarely looks bad at first. It can pass AVS, use a real card, ship to a plausible address, and come in at an order value high enough to hurt but low enough to avoid a manual review trigger.

Then the costs stack up fast:

- Inventory loss: You shipped a real item to a fraudster, mule, or reshipper.

- Fulfillment waste: You paid pick, pack, and postage on revenue that will not stay booked.

- Support time: Your team has to pull tracking, order logs, device data, and customer emails.

- Chargeback fees: The processor debits another fee while the case is still being argued.

- Misread trends: Repeated “friendly fraud” claims can look like random complaints instead of a preventable pattern tied to specific products, shipping methods, or customer segments.

That last point is where stores lose money for months. If a wave of “unauthorized” or “item not received” claims keeps hitting the same SKUs or fulfillment flow, you do not have a customer service issue. You have a fraud control issue with a clear chargeback footprint.

ChargePay's role here is operational, not theoretical. It has recovered $10.8M+ for merchants and handled 200K+ cases. That scale shows what many Shopify teams learn too late. Fraud is recurring, process-driven, and expensive when nobody maps each trend to the claim types and reason codes showing up in the dispute queue.

The Top 5 Payment Fraud Trends Hitting Shopify Stores

Fraud does not hit Shopify merchants evenly. It hits the stores with weak review rules, fast fulfillment, and no habit of tying disputes back to the order patterns that caused them.

That is why you should track fraud trends by the customer claim they create. A vague “fraud problem” does not help you fix operations. A spike in “unauthorized” claims, “item not received” complaints, or “not as described” disputes does.

AI-powered friendly fraud

This trend costs real money because the order often looks legitimate from start to finish. The customer may use their own card, receive the product, and then file a dispute with a polished, believable story written faster and better than most support teams can answer.

On Shopify, this usually lands as the claims you already know:

- “I never got it” despite confirmed delivery

- “This transaction was unauthorized” after a family member used the card

- “The item was not as described” when the actual goal is a refund without a return

Treat these as chargeback patterns, not random complaints. If one product line or shipping method keeps producing the same claims, fix that flow first.

Account takeover attacks

Account takeover is dangerous because it borrows trust you already built. The fraudster logs into a real customer account, uses saved payment details or an established profile, and places an order that looks safer than it is.

The result is usually an unauthorized transaction dispute, but the operational clues show up earlier:

- Address changes right before checkout

- Expedited shipping on an older customer account

- Multiple failed logins before one successful purchase

- A post-delivery message from the genuine customer saying they never placed the order

If you want the underlying pattern, this guide to card-not-present fraud explains why so many ATO losses still end up as standard remote-payment disputes.

Synthetic identity fraud

Synthetic identity fraud is slower and more disciplined. The fraudster combines real and fake details, behaves like a normal customer for a while, then uses that trust to place a larger order.

This is the trend many merchants miss because nothing looks urgent at first. You see a few routine purchases, then a bigger order, a new shipping address, or a payment method change. Weeks later, the dispute arrives as fraudulent or unauthorized, and the order history makes your team second-guess what happened.

Watch for accounts that age dormantly, then change behavior fast.

Card-not-present fraud

CNP fraud is still the core ecommerce problem. Shopify stores sell remotely by default, so stolen card data, mismatched identity signals, and rerouted shipments remain a direct path to lost inventory and chargeback fees.

The usual claim is simple: cardholder does not recognize the transaction.

The mistake is relying on one or two checkout checks and calling the job done. AVS and CVV can help. They do not stop a determined fraudster using clean device signals, a believable email, and a shipping address that passes a quick glance. Teams focused on protecting SaaS revenue from chargebacks deal with the same issue. Remote payments create more room for abuse unless you review order context, not just payment approval.

Triangulation fraud

Triangulation fraud creates some of the most confusing cases in a Shopify store. A scammer lists your product on another marketplace, collects money from a buyer there, then uses stolen card details to buy the item from your store and ships it to that marketplace buyer.

Your team sees a normal order. The card issuer later sees an unauthorized purchase. The legitimate end customer never intended to scam you, but you still lose the product and absorb the dispute.

That is why triangulation often turns into messy unauthorized transaction claims with delivery evidence that does not fully help your case. The package reached a real person. It just did not reach the legitimate cardholder.

These five trends matter because each one maps to a claim type your Shopify team will have to answer. If you cannot connect the fraud pattern to the dispute reason showing up in your queue, you will keep treating preventable losses like isolated incidents.

How These Trends Become Costly Chargebacks

Fraud only becomes real for many merchants when the payout reverses. That's too late. By the time the dispute lands, you're no longer deciding whether to ship. You're trying to prove what happened after the fact.

Different rails create different loss patterns

The biggest mistake merchants make is treating all payment fraud as one problem. It isn't. The rail changes both the fraud pattern and who usually absorbs the loss.

The Federal Reserve found that debit card fraud was reported by 75% of financial institutions and accounted for 40% of total payments-fraud losses, according to the Federal Reserve's survey summary on rising fraud trends. That matters because your store may focus heavily on credit-card disputes while debit-linked losses and bank-side disputes continue to expand.

How the same fraud looks in your admin panel

A few common examples make this easier to spot.

| Fraud event | What you see first | What it often becomes |

|---|---|---|

| Account takeover | Existing customer account places unusual order | Unauthorized transaction dispute |

| Friendly fraud | Customer asks vague questions after delivery | Item not received or product not as described claim |

| Card-not-present fraud | New customer, mismatched signals, expedited shipping | Fraudulent transaction chargeback |

| Triangulation fraud | Normal shipping to a real address | Late unauthorized dispute from stolen cardholder |

| Bank-rail scam | Payment looks confirmed and moves fast | Recovery is limited and often outside normal chargeback flow |

If you need a broader primer on dispute categories because your team keeps seeing different bank labels for the same behavior, this breakdown of reasons for a chargeback helps map claims to underlying causes.

Here's the practical issue. Card disputes, debit disputes, ACH problems, and bank-transfer scams don't all have the same recovery path. A card chargeback often gives you a formal representment process. A real-time payment scam may leave almost no time to stop the loss once the funds move.

Later in the cycle, merchants also run into a documentation problem. The evidence that beats “item not received” is not the same evidence that beats “fraudulent transaction.” Teams that deal with subscriptions or recurring billing face a similar challenge, which is why this guide on protecting SaaS revenue from chargebacks is useful even outside SaaS. The core lesson is the same. Generic evidence loses.

This short walkthrough shows how a single order turns into a dispute event:

If you can't explain why a dispute happened, you can't build a process to stop the next one.

Key Metrics to Monitor on Your Shopify Dashboard

You don't need a massive fraud team to spot trouble. You need a few metrics that tell you when order behavior stops looking like your normal business.

The trick is not to stare at one number in isolation. Watch for combinations. AOV jumps plus rush shipping plus new-customer concentration is more meaningful than any one signal by itself.

Fraud KPIs for Shopify merchants

| KPI (Key Performance Indicator) | What It Measures | Potential Red Flag |

|---|---|---|

| Chargeback rate | How often completed orders turn into disputes | A sudden rise over your recent baseline or repeated disputes clustered by product, channel, or region |

| Order velocity | How many orders are placed in a short period from related signals | Multiple orders close together from the same IP, device pattern, card pattern, or shipping destination |

| Average order value movement | Whether fraudsters are testing with larger baskets or unusual product mixes | New customers placing unusually large orders, especially with expensive or easily resold items |

| Shipping method mix | Whether risky orders are leaning on speed and rerouting | More overnight or rush orders than usual, especially for first-time buyers |

| Billing and shipping mismatch rate | Whether identity signals line up | Increased mismatch volume combined with higher dispute activity |

| Refund rate by SKU or campaign | Whether customer dissatisfaction or abuse is building | One product or ad campaign generating an unusual number of refunds, complaints, or post-delivery disputes |

| Repeat customer account changes | Whether trusted accounts are being manipulated | Password resets, address edits, or contact-detail changes right before purchase |

| Manual review pass rate | Whether your team is approving too many risky orders | Orders you approved manually later become disputes at a noticeable rate |

What smart merchants actually watch

Don't just monitor totals. Segment your dashboard.

Look at disputes by product category, shipping country, payment method, and customer type. A fraud wave often starts as a small cluster that disappears inside store-wide averages.

If you pull order or pricing intelligence from outside marketplaces to compare suspicious patterns, use tools built for reliable collection. For example, teams that need structured competitive or listing data often rely on anti-bot bypass for data extraction so they can monitor suspicious resale behavior without building that plumbing from scratch.

Watch for pattern breaks, not just bad orders. Fraud usually shows up as a change in behavior before it shows up as a chargeback.

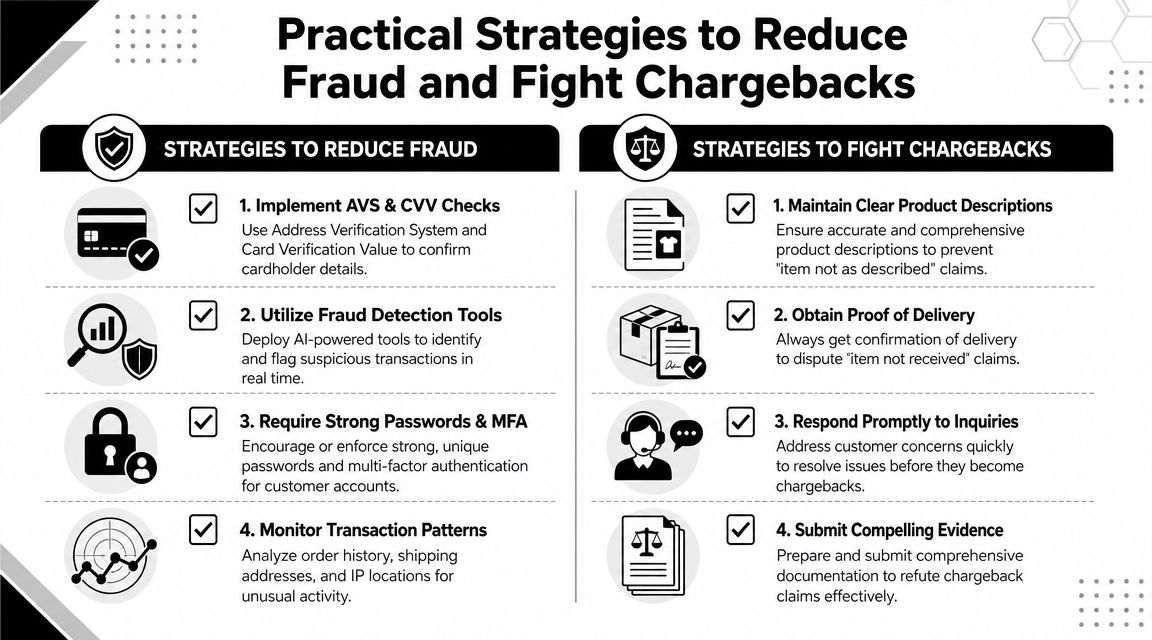

Practical Strategies to Reduce Fraud and Fight Chargebacks

Every weak handoff in your order flow becomes a chargeback opening. Fraud slips through review, fulfillment ships too fast, support misses the complaint, and then the cardholder files under the reason code that fits the story. On Shopify, that usually means the claims you see are not random. They trace back to preventable gaps in operations.

Process changes that save money fast

Start with fulfillment. Treat high-risk orders differently from clean repeat purchases, because shipping a bad order quickly turns a screening mistake into a lost product, a refund dispute, and a fee.

Use rules your team can follow every day:

- Pause risky orders briefly: Hold orders with recent address edits, unusual basket size, mismatched billing and shipping details, or rush shipping until someone reviews them.

- Collect stronger delivery proof: Use tracked shipping, require signatures on higher-value orders, and keep carrier scans accessible. That evidence matters when a customer claims the item never arrived.

- Tighten product-page accuracy: Clear sizing, materials, delivery expectations, and return terms make "not as described" claims harder to win.

- Respond to support tickets fast: A slow refund, replacement, or order update often turns into a chargeback filed as fraud or service-related dissatisfaction.

Social engineering is making this harder. Fraud claims are getting more polished and more believable, as noted earlier. Train support agents to log every interaction, confirm key account details before making changes, and save message history. That record can help you fight claims tied to unauthorized purchase allegations, account takeover, or friendly fraud.

Technology controls that should already be on

Skip fancy tooling you cannot configure well. Get the basics right first.

Your stack should include:

- AVS and CVV checks: These still stop low-effort stolen-card attempts and give you evidence when the cardholder later claims the transaction was unauthorized.

- Velocity rules: Block or flag repeated attempts tied to the same card, email, IP, device fingerprint, or shipping address.

- Device and behavior checks: Watch for impossible login patterns, repeated checkout retries, or account changes right before purchase.

- Account security controls: Use stronger login protections and add MFA where customer friction stays reasonable.

If you need a practical playbook, this guide to chargeback prevention for Shopify stores lays out the operational controls in plain terms.

Build better dispute evidence before you need it

Representment is won or lost before the dispute arrives. If your proof is scattered across Shopify, your help desk, and your shipping app, you will miss deadlines or submit weak evidence.

Build a record for each order that maps to the claims you are likely to face:

| Evidence type | Best use |

|---|---|

| Order confirmation details | Shows what was purchased and when |

| AVS and CVV results | Supports unauthorized transaction defenses |

| Tracking and delivery confirmation | Helps fight item not received claims |

| Customer service messages | Useful when the customer acknowledged the order or product |

| Account history and login changes | Helpful in account takeover disputes |

| Product page snapshot | Supports defense against not-as-described claims |

That bridge between fraud trend and chargeback claim matters. A rise in account takeovers becomes "I didn't authorize this purchase." Poor delivery documentation becomes "product not received." Weak product copy becomes "not as described." Organize your records around those claims, not around whatever app happens to store them.

ChargePay is a technology option for this workflow. It automates evidence gathering and dispute submission for Shopify merchants. That helps when your team knows the chargeback is invalid but cannot afford to build every case by hand.

Automate Your Defense and Recover Lost Revenue with ChargePay

By the time a dispute reaches your store, speed matters. Deadlines are short, evidence is scattered across apps, and most merchants can't justify having someone manually build representment packets all week.

That's why automation makes sense here. ChargePay handles the dispute workflow for Shopify merchants. It gathers evidence, drafts responses, and submits them before deadlines. For teams buried in disputes, that removes a lot of operational waste.

The numbers are strong. ChargePay reports a 92.4% win rate, 200K+ cases handled, and $10.8M+ recovered for merchants. It also has a 4.9-star rating in the Shopify App Store and carries the Built for Shopify badge. The pricing model is straightforward too. Pay per win means you only pay when money is recovered.

Why this matters in real operations

Most chargeback losses aren't caused by one missing screenshot. They happen because no one has time to:

- find the order timeline

- pull tracking proof

- match customer communication

- identify signs of friendly fraud

- submit a structured response before the deadline

That admin work adds up fast. If your store is already dealing with rising fraud pressure, manual dispute handling is the wrong hill to die on.

A busy merchant should focus on prevention rules, customer experience, and fulfillment controls. The dispute assembly work should be automated wherever possible.

If chargebacks are eating margin, install ChargePay from the Shopify App Store. It's built for Shopify merchants who want disputes handled automatically, without turning their ops team into a paperwork department.

.svg)

.svg)

.svg)

.svg)