To really get a handle on chargeback fraud, you need a strategy that goes beyond just reacting to disputes. It starts with understanding how much this stuff actually costs you. We're not just talking about the lost sale—it’s a cascade of fees, wasted time, and a real threat to your relationship with payment processors.

The best defense is a good offense, which means a combination of smart checkout security, fantastic customer service, and an automated system for fighting back.

The Real Cost of Chargeback Fraud to Your Store

Chargeback fraud isn't just another expense on your P&L. It's a direct hit to your store's bottom line and can seriously mess with your ability to grow. For anyone selling online, what looks like a tiny percentage of reversed sales can quickly snowball into a major financial headache, messing with everything from your cash flow to your future plans.

The damage goes way beyond the initial transaction. Every single dispute comes with its own set of penalties that add up fast. You lose the revenue from the sale, you're out the cost of the product, and you get slapped with a non-refundable chargeback fee by your payment processor. Getting your head around the real impact of a chargeback fee is the first step to seeing the true scale of the problem.

More Than Just a Transaction Reversal

Think of it as a domino effect. One bad chargeback can lead to another, and before you know it, you're sinking valuable hours and resources into fighting disputes instead of focusing on what you do best—running your business. The stats are pretty sobering: global chargeback volumes are projected to reach a staggering 337 million cases by 2025.

This explosion is largely fueled by card-not-present (CNP) transactions, which now make up 63% of all merchant sales and are a prime target for fraudsters.

Here's a hard truth: For every dollar you lose to fraud in the U.S., the actual cost to your business is around $4.61. That figure accounts for the lost product, shipping, operational overhead, and those brutal processor fees.

The Rise of Friendly Fraud

One of the sneakiest parts of this whole issue is the boom in "friendly fraud." This isn't your classic stolen credit card scenario. This is when a legitimate customer disputes a charge they actually made.

I've seen it happen for a few common reasons:

- Buyer's Remorse: The customer regrets their purchase and decides it's just easier to file a dispute than to deal with your return process.

- Family Fraud: A family member, usually a kid, makes a purchase without permission, and the cardholder disputes it.

- Simple Forgetfulness: The customer just doesn't recognize the billing descriptor on their statement and immediately assumes it’s fraud.

But lately, something more deliberate is happening. Viral social media tutorials teaching "refund hacks" are encouraging people to cheat the system. They'll claim a product never showed up or was broken just to get their money back while keeping the item.

It's a huge problem. In fact, some studies show that an unbelievable 61% of chargebacks now fall into this friendly fraud category. That makes being proactive not just a smart business move, but an absolute necessity for survival in e-commerce today.

Fortifying Your Checkout to Stop Fraud Early

Think of your checkout page as the frontline in the war against chargeback fraud. This is your first—and best—opportunity to spot the difference between a legitimate customer and a fraudster trying to pull a fast one. A few smart, targeted tweaks here can stop a bogus transaction in its tracks, saving you a world of headaches later.

This isn't about building an impenetrable fortress that locks out good customers. It’s about adding simple, effective security layers that fraudsters absolutely hate but your real buyers will barely even notice.

The Power of Basic Verification Tools

Let's start with the essentials—the tools you probably already have but might not be using to their full potential. These are the unsung heroes of checkout security.

CVV/CVC Requirement: You know that three or four-digit code on the back of a credit card? Always require it. It's that simple. Fraudsters working with stolen card numbers often don't have the physical card, so this one little field weeds out a massive chunk of low-effort fraud.

Address Verification Service (AVS): This is another must-have. AVS checks if the billing address the customer enters matches the one their bank has on file. A complete mismatch is a huge red flag for a stolen card. Sure, a small typo can happen, but this check catches the blatant stuff.

These two checks are your first line of defense. They’re fast, automated, and create just enough friction to deter opportunistic criminals without annoying your actual customers.

Essential Checkout Fraud Prevention Tools

To get a clearer picture, here’s a quick rundown of the most common tools and what they're designed to do.

Having a mix of these tools creates a layered defense that is much harder for fraudsters to penetrate.

Stepping Up Your Security Game

Ready to get more serious? The single most powerful tool you can add is 3D Secure. This technology adds an extra authentication step where the customer has to verify their identity directly with their bank, usually with a one-time code sent to their phone.

This is a true game-changer because it shifts the liability for fraudulent chargebacks from you, the merchant, to the card-issuing bank. If a transaction is authenticated with 3D Secure, it becomes incredibly difficult for a cardholder to successfully claim they didn't authorize it. It's a powerful tool for any e-commerce store serious about fighting fraud.

Of course, all of this ties into fundamental payment security standards. A crucial piece of the puzzle is understanding and maintaining PCI DSS compliance, which provides the framework for handling cardholder data safely.

The goal is to build a "smart" checkout—one that intelligently assesses risk without frustrating good customers. Combining these tools creates a multi-layered defense that is tough for criminals to beat.

The Simple Fix That Stops Confused Customers

Not every chargeback is malicious. A surprising number of disputes, often called "friendly fraud," happen because of simple confusion. A customer scrolls through their bank statement, sees a charge from a business name they don’t recognize, panics, and immediately files a dispute.

Imagine your legal business name is "Global Commerce Solutions LLC," but your awesome online store is called "The Gadget Hub." If "Global Commerce Solutions LLC" is what shows up on their statement, you’re practically asking for a chargeback.

The fix is incredibly easy: Set a clear and recognizable billing descriptor. Make sure the name that appears on your customer's bank statement is the name of your store. Something like "THEGADGETHUB" or "GADGETHUB.COM" is perfect. This tiny detail can prevent countless headaches from customers who simply forgot what they bought.

Turning Customer Service Into a Prevention Tool

It might sound strange, but one of the best ways to stop chargeback fraud has nothing to do with fancy security software. It’s all about making it incredibly easy for your customers to talk to you. You'd be surprised how many disputes don't start with bad intentions, but with simple frustration.

When a customer can't find your contact info, gets a slow reply, or is baffled by your return policy, their next click is often the "dispute charge" button with their bank. By treating your customer service team as your first line of defense, you can head off these problems long before they hit your payment processor.

This strategy is more important than ever. Friendly fraud has now officially overtaken criminal fraud as the top reason for disputes. A recent Federal Reserve study showed that 61% of disputes are filed by cardholders on legitimate purchases they made themselves. In ecommerce, this has exploded—chargebacks surged a staggering 233% between Q1 and Q3 of 2025. We're seeing this driven by everything from simple buyer's remorse to "refund hack" trends blowing up on social media.

Make Yourself Impossible to Miss

First things first: plaster your contact information everywhere. Don't make people dig for it. A frustrated buyer who has to click through five pages just to find an email address is a chargeback waiting to happen.

Your goal is to make contacting you the path of least resistance. Here’s how to do it:

- Header and Footer: Your phone number and a link to your contact page should be right there in the header and footer of every single page. No exceptions.

- Order Confirmations: Drop your support email and phone number directly into your order confirmation and shipping notification emails. This is prime real estate.

- Live Chat: If you have the team to support it, a live chat widget is an absolute game-changer for solving problems in real-time before they escalate.

Being highly visible sends a clear message: "We're here and we want to help." That simple act of accessibility can de-escalate a tense situation almost instantly.

Think about it from the customer's perspective. Their bank makes it incredibly easy to dispute a charge with a single click. Your process for getting a refund or asking a question needs to be just as easy, if not easier.

Write Policies for Humans, Not Lawyers

Your return and refund policies are critical customer service documents. If they're packed with confusing legal jargon and a maze of conditions, customers will just skip them and go straight to their bank.

Your policies need to be written in plain, simple English. Use clear headings, bullet points, and straightforward language to walk people through the process. A customer should be able to figure out exactly how to return something and when they'll get their money back in under 30 seconds.

For example, instead of this:

"All merchandise returns must be postmarked within thirty (30) days of the original purchase date. All returned items must be in new and unused condition, with all original tags and labels attached."

Try this:

"Easy 30-Day Returns

Not happy with your order? No problem! You have 30 days from when you receive it to send it back. Just make sure it's unused and has the original tags."

This kind of clarity builds trust and encourages customers to work with you directly. For a deeper look at this, check out our guide on the best practices in customer service.

Respond with Speed and Empathy

When a customer does reach out, how fast you reply is everything. A quick, empathetic response can stop a chargeback dead in its tracks. Acknowledge their problem, show you get their frustration, and tell them exactly what you're doing next.

Even a simple template can work wonders:

"Hi [Customer Name], thanks for reaching out. I'm so sorry to hear you're having an issue with [Order #]. I'm looking into this for you right now and will have an update for you within [Timeframe]."

That immediate acknowledgment buys you a ton of goodwill and time. It assures the customer their problem is being handled. This kind of proactive communication is a cornerstone of any effective strategy to prevent chargeback fraud and keep your good customers happy.

How to Win Disputes with the Right Evidence

Even with the best fraud prevention in place, a bogus chargeback is bound to slip through now and then. When it does, your ability to fight back and get your money back comes down to one thing: the quality of the evidence you provide.

Think of it like building a case for the issuing bank. Your job is to tell a clear, undeniable story that proves the transaction was legitimate and the customer got exactly what they paid for.

The problem? Manually digging up all this information for every single dispute is a massive time sink. It pulls you away from actually running your business and throws you into an administrative battle you never wanted. But just letting it go is like leaving cash on the table.

Gathering Your Core Evidence

When a dispute lands in your lap, the clock starts ticking. You have to move fast and pull together a compelling package of proof. The goal is to paint a complete picture of the transaction, from the second the customer clicked "buy" to the moment the package landed on their doorstep.

Here's the essential evidence you should be gathering for every single dispute:

- Customer and Order Information: This is your foundation. You need the customer's name, email, and the full order details. A quick screenshot of the order from your e-commerce platform (like Shopify) works perfectly here.

- Proof of Delivery: This is absolutely non-negotiable, especially for those "product not received" claims. You need a shipping confirmation number and, ideally, proof of delivery from the carrier showing the date, time, and delivery address. A photo of the package on the customer's porch is pure gold.

- Customer Communications: Did the customer email you before filing the dispute? Did they hop on your live chat? Any communication you have is valuable. It can show they acknowledged the purchase or were interacting with your brand after the transaction.

This basic evidence is often enough to shut down simpler cases of friendly fraud. It clearly establishes that a real order was placed and you fulfilled your end of the bargain.

Digital Fingerprints That Strengthen Your Case

To build a truly airtight case, you need to go a step further. It's all about including the digital evidence that connects the person who placed the order to the device they used. This kind of data makes it incredibly difficult for someone to falsely claim a transaction was unauthorized.

These digital data points can be the difference between winning and losing:

- IP Address: The IP address recorded at the time of purchase is a critical piece of your puzzle. If you can show it matches the customer's billing or shipping location, you've created a powerful link.

- AVS and CVV Match: Always include the results from your Address Verification Service (AVS) and CVV checks. Showing that the numbers matched is strong proof that the person making the purchase had the physical card in their hands.

- Device Information: Data about the browser, device type (like an iPhone or Android), and operating system can help establish a pattern if the customer has ordered from you before.

Presenting this layered evidence—transactional, logistical, and digital—makes your representment package far more persuasive. You're not just telling the bank the charge was valid; you're showing them why with concrete data.

Unfortunately, the sheer volume of these disputes is only getting worse. Retail e-commerce chargebacks skyrocketed by a staggering 233% between the first and third quarters of 2025 alone. As "card-not-present" sales continue to grow, this problem isn't going away.

Why Manual Evidence Collection Is Unsustainable

Now, imagine doing all of that for every dispute that comes your way. Sifting through Shopify orders, digging through carrier portals, searching for old customer emails—it's a huge operational headache. This manual grind is exactly why so many merchants just give up and write off chargebacks as a cost of doing business.

But it doesn't have to be that way. Winning a dispute is entirely possible, and with the right strategy, you can dramatically improve your success rate. For a deeper dive into building your argument, you can learn more about how to win a credit card dispute in our detailed guide.

At the end of the day, the burden of proof is on you, the merchant. Building a system to efficiently collect and present this evidence is key. This manual struggle is what leads most growing businesses to look for an automated solution that can handle the fight for them, saving precious time and recovering lost revenue.

Automating Your Defense to Save Time and Money

So far, we've walked through shoring up your checkout, putting customer service to work, and getting your evidence in order. These are all mission-critical pieces of the chargeback puzzle.

But let's be real—manually juggling all of this is a full-time job. As your store scales, it becomes completely unsustainable.

This is where automation changes the game. The right tools can take the repetitive, soul-crushing work of fighting chargebacks right off your plate. This frees you up to focus on what actually grows your business, like killer marketing campaigns and new product development.

Instead of playing defense and reacting to disputes one by one, an automated system works tirelessly for you in the background. Think of it as having an in-house expert who never sleeps, constantly monitoring for trouble and building your case.

How AI Transforms Chargeback Management

The latest advancements in AI for e-commerce are a godsend for merchants drowning in disputes. AI-powered systems can analyze thousands of data points in a split second, spotting fraudulent patterns a human would almost certainly miss.

When a dispute lands, these tools don't just send you an alert—they spring into action. They instantly plug into your sales platforms like Shopify and your payment gateways like Stripe or PayPal. From there, they automatically pull all the crucial evidence we’ve been talking about.

No more frantic searching for:

- Customer order history and contact info

- Shipping confirmations and delivery proof

- IP addresses and device fingerprints

- AVS/CVV match results

The system grabs everything it needs in an instant. This speed is a massive advantage, since the clock is always ticking on the card issuer’s deadline to submit your response.

The real power of automation is simple: it replaces manual grunt work and administrative drain with speed, accuracy, and efficiency. It lets you fight every single bogus dispute without sacrificing your own valuable time.

From Evidence to a Winning Response—Automatically

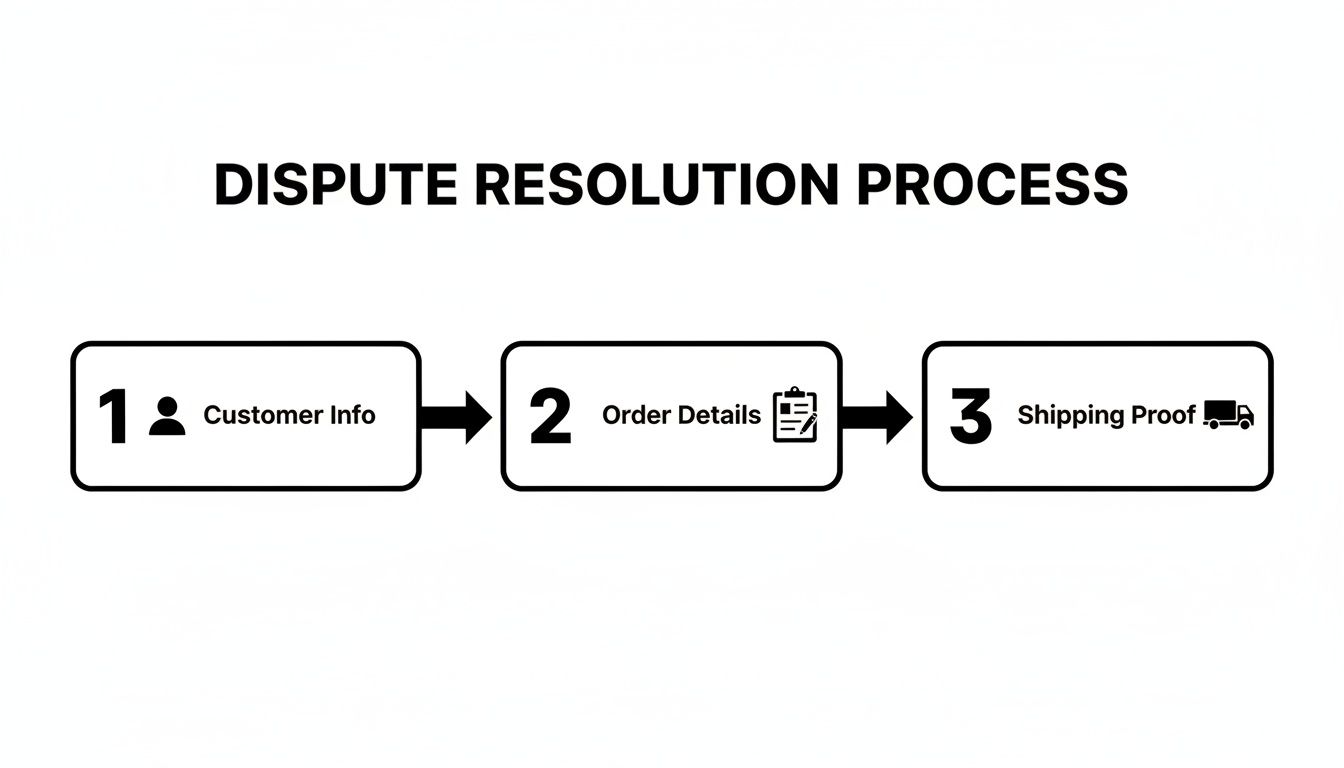

Once all the evidence is collected, the real magic begins. An intelligent system doesn't just dump a folder of screenshots on your desk. It uses that data to generate a professional, compelling dispute response, formatted exactly the way the banks need to see it.

This is a critical step. A well-structured response that tells a clear, evidence-backed story is infinitely more likely to win. Automation ensures every response is consistent, comprehensive, and submitted on time, which can have a huge impact on your win rates. Some merchants see their success rates jump by as much as 3.5 times what they could ever achieve manually.

This flowchart breaks down the essential data points an automated system pulls together to build a rock-solid case.

It all comes down to combining customer, order, and shipping details to create an undeniable foundation for your dispute.

The Tangible Benefits You Actually Care About

At the end of the day, this is all about your bottom line. Automating your chargeback defense isn't just a nice-to-have; it delivers real, measurable results that directly impact your profitability.

First, you save countless hours. The time you and your team would have burned on administrative busywork can be poured back into activities that actually make you money.

Second, you recover revenue you thought was gone for good. By fighting and winning more disputes, you reclaim cash that was unfairly clawed back from your account. Many businesses are able to recover up to 80% of their disputed funds by taking an automated approach.

Finally, you get peace of mind. Knowing you have a robust system handling these headaches lets you operate with confidence. You no longer have to accept chargebacks as an unavoidable cost of doing business—you can actively protect your hard-earned revenue.

This hands-off approach is a cornerstone of any modern strategy to prevent chargeback fraud. If you want to dig deeper, check out our complete guide to automated chargeback and dispute management. It’s about working smarter, not harder, and using technology to defend your store effectively.

Got Questions About Chargeback Fraud? We’ve Got Answers.

Even with a solid game plan, the world of chargeback fraud can feel like a maze. We get it. Over the years, we've heard just about every question from merchants, so we’ve rounded up the most common ones to give you clear, no-nonsense answers you can use right away.

What's the Real Difference Between a Chargeback and a Refund?

This is one of the most important things to get straight. A refund is a conversation between you and your customer. They reach out, tell you what's wrong, and you agree to give them their money back. It's a direct resolution you control, and it can even be a positive touchpoint.

A chargeback, however, yanks you right out of the loop. The customer bypasses you completely and goes straight to their bank to dispute the charge. The bank then force-pulls the money from your account, kicking off a formal, often frustrating, process where you have to fight to prove the sale was legit.

Is All Chargeback Fraud Malicious?

Not at all, and this is where it gets tricky. While some fraud is absolutely intentional—think criminals using stolen credit cards—a huge portion is what we call "friendly fraud." This happens when a real customer disputes a charge they actually made.

Why would they do this? It usually comes down to a few simple reasons:

- They honestly forgot they bought something from you.

- Your business name on their statement is confusing (e.g., "SP*MERCH" instead of "Super Cool Gadgets").

- A family member used their card, and they don't recognize the charge.

- Frankly, they found it easier to call their bank than to go through your return process.

The customer's intent might not be evil, but the financial hit to your business is exactly the same. This is why every single customer interaction matters in your quest to prevent chargeback fraud.

Can I Just Blacklist Customers Who File Chargebacks?

It's a tempting thought, isn't it? But you have to tread carefully here. While you can—and should—block a customer you've confirmed is a fraudster from buying again, a blanket "blacklist everyone who disputes" policy is a bad idea. A good customer might file a chargeback because of a genuine mistake on your end.

A much smarter approach is to dig into the why. Why did the chargeback happen in the first place? Was your shipping delayed? Was your billing descriptor a mess? Fixing the root cause is a far more powerful strategy for long-term growth than simply banning shoppers.

Plus, blacklisting can backfire spectacularly if a legitimate customer gets caught in the crossfire, leading to scathing reviews and a damaged reputation.

What Is a Chargeback Ratio, and Why Should I Care?

Your chargeback ratio (or dispute rate) is simple math: the number of chargebacks you get divided by your total number of transactions in a given month. Payment networks like Visa and Mastercard watch this number like a hawk.

If your ratio creeps too high (the usual red flag is 0.9%), you’ll be labeled a "high-risk" merchant. That’s a label you really don’t want. It triggers a cascade of painful consequences:

- Higher processing fees: You'll suddenly pay more for every single transaction.

- Hefty monthly fines: The card networks can slap you with penalties until your ratio drops.

- Account termination: This is the worst-case scenario. You could lose your merchant account entirely, making it nearly impossible to accept card payments.

Keeping this ratio low isn't just good practice; it's essential for survival. Proactively fighting illegitimate disputes is one of the best ways to keep it in a healthy range.

Do I Automatically Lose Money on a Chargeback?

Not if you fight back and win. When a chargeback is filed, the money is pulled from your account immediately, but the story isn't over. You get a chance to present your side of the story with evidence—a process called representment.

If you provide a compelling case that proves the transaction was valid, you win the dispute, and the funds are returned to your account. This is precisely why having a system to capture and organize evidence is so critical. You won't get the non-refundable chargeback fee back, but recovering the full transaction amount makes a massive difference to your bottom line.

Ready to stop losing revenue to time-consuming disputes? ChargePay uses AI to automatically fight and win chargebacks for you, recovering up to 80% of lost funds without you lifting a finger. Learn how ChargePay can protect your business today.

.svg)

.svg)

.svg)

.svg)