Worried a recent purchase went sideways? You're probably wondering how long you have to act. The short answer is you generally have 90 to 120 days from the transaction date to file a chargeback.

But that window isn't set in stone. It can change depending on your card network—think Visa versus Mastercard—and the specific reason you're disputing the charge.

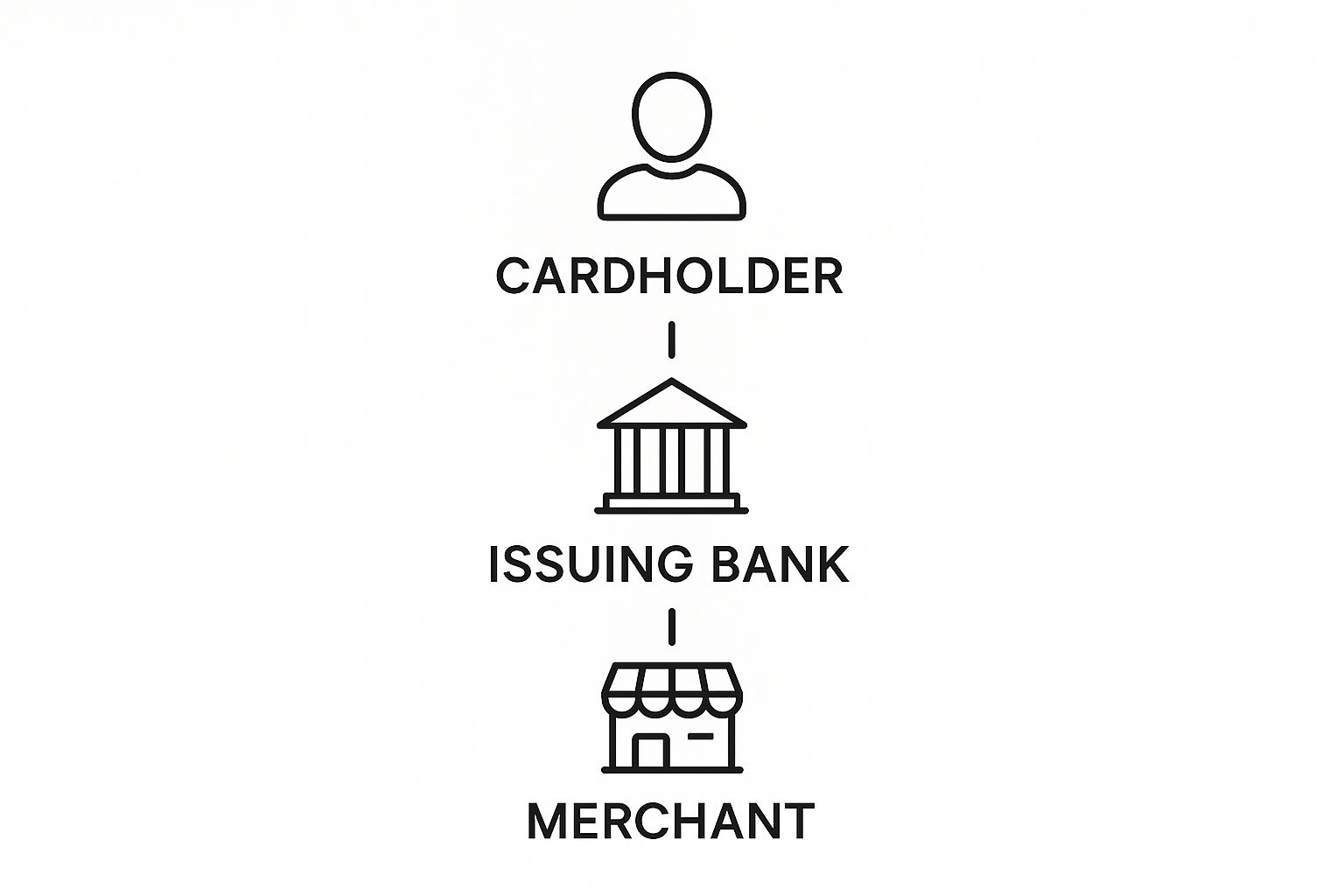

Your Quick Guide to Chargeback Deadlines

When you spot a charge you don't recognize or get a product that’s clearly not what you ordered, time is of the essence. You aren't just dealing with the seller; you're navigating a system that loops in your bank (the issuer) and the merchant's bank.

This visual breaks down the key players involved in every single dispute.

Seeing the whole picture helps explain why these time limits exist in the first place—they're there to keep the process moving smoothly between everyone involved.

The time limit for chargeback on credit card isn’t just a friendly suggestion; it’s a hard rule set by the card networks themselves. These deadlines are in place to protect both you and the business.

Here’s what you absolutely need to know about these critical windows:

- Standard Window: For most disputes, you're looking at a 90 to 120-day window.

- The Starting Pistol: The clock usually starts ticking on the date of the transaction or, in some cases, the date you were supposed to receive your goods or services.

- The Reason Matters: The why behind your dispute can sometimes stretch or shrink the deadline.

Chargeback Time Limits at a Glance

Each card network has its own set of rules, but they all give you a reasonable amount of time to raise a flag. The table below gives you a quick snapshot of what to expect from the major players.

Keep in mind, these are the general guidelines. There are always exceptions for unique situations, like a service you booked for a future date that didn't happen. The key is to act as soon as you spot a problem. For a deeper dive into how these time limits compare, you can find more details at justt.ai.

How Chargeback Time Limits Actually Work

Think of a chargeback deadline as a countdown timer. The most important question you need to ask is: what starts the clock? It’s not always the day you paid, and this little detail is what trips a lot of people up when figuring out the real time limit for chargeback on credit card disputes.

Let's use a real-world example. Say you bought a concert ticket way back in January for a show happening in June. Your window to file a dispute doesn’t start ticking in January. Instead, it begins after the date the concert was supposed to happen. This protects you if the event gets canceled last minute.

The same logic applies if you order something online that never shows up. The timer starts from the promised delivery date, not the day you clicked "buy."

This whole system is designed to be fair. It gives you, the customer, a reasonable amount of time to spot a problem while also protecting businesses from having to worry about ancient transactions forever. If you want to dive deeper into the basics, we've got a full guide on disputes and chargebacks that breaks it all down.

Transaction Date vs. Service Date

Getting a handle on what triggers your chargeback window is absolutely key. The rules make a clear distinction between two main starting points to keep things fair for different kinds of purchases.

The core idea is simple: the clock shouldn't start until you could have reasonably known there was a problem. You can't dispute a package that never arrived until after its expected delivery date has already passed.

Let's break down the two most common triggers:

- Transaction Date: This is the day your payment was actually processed. It’s the usual starting point for things you buy in-store or services you get on the spot.

- Service or Delivery Date: This one is for future events, ongoing services, or items being shipped to you. The countdown only begins on the date the service was supposed to happen or the item was scheduled to arrive.

This crucial difference ensures your consumer protection rights don't expire before you even have a chance to get what you paid for.

Comparing Deadlines for Visa, Mastercard, and Amex

When it comes to chargeback deadlines, you can't assume a one-size-fits-all rule. The big three—Visa, Mastercard, and American Express—each have their own playbook. Knowing these subtle differences is often the key to successfully filing a dispute.

Think of it this way: they all offer a safety net, but the ropes are tied a little differently for each one. Let's break down what you need to know.

Visa and Mastercard Deadlines

For both Visa and Mastercard, the clock is pretty generous. Cardholders typically have 120 days to get a dispute started. That countdown usually begins on the day of the transaction, or if you're waiting for a product, the expected delivery date.

But it's not always that simple. The reason for your dispute can shift the timeline a bit. For instance, issues like sneaky recurring billing errors might have a slightly different window. The main takeaway, though, is that you have a decent amount of time to spot a problem and take action.

How American Express Is Different

American Express plays by its own rules, largely because it operates as both the card issuer and the payment network. This setup gives them a much tighter grip on the whole dispute process. While they can be more flexible, their general guideline is to file a dispute within 90 days of the transaction.

Since they manage the entire system themselves, Amex often has more room to bend the rules. If you're an Amex cardholder, it's worth digging into the specifics. You can get a much clearer picture by learning more about American Express chargeback time limits and how they stack up against the others.

This chart gives you a quick side-by-side look at how these timelines compare.

As you can see, even though the windows feel similar, the starting points and the fine print for each network can really matter.

The most important thing to remember is this: while the card networks set the master rules, it's your own bank that handles the dispute. Your first call should always be to them.

Navigating these deadlines isn't just for consumers; it's a fundamental part of understanding the financial services sector. And while you might have a few months to act, the pressure is really on the merchant. They usually only get 18 to 30 days to respond once you file a claim. That tight turnaround is exactly why it pays to act quickly—it keeps the process moving for everyone.

When Can the Filing Deadline Be Extended?

So, what happens if you spot a fishy charge months after the fact? Or a pricey gadget with a warranty dies long after you bought it? The standard 90 to 120-day window seems slammed shut, but don't panic—you’re not always out of luck.

In certain situations, the time limit for chargeback on credit card disputes can be extended, giving you a second chance to make things right. These extensions are basically a fairness rule built into the system, designed for scenarios where you couldn't possibly have known about the problem any sooner.

A classic example is discovering a sneaky recurring subscription you never signed up for. The clock doesn't start ticking from the very first charge. Instead, it starts from the date you finally noticed the billing error, which is often on a much later statement.

Common Scenarios for an Extension

Card networks and banks use specific "reason codes" to sort out different types of disputes, and some of these codes come with a much longer leash. If your problem fits into one of these special categories, your bank might be able to open a dispute long after the standard deadline has passed.

The real key here is proving the "discovery date." If you can show that you acted as soon as you reasonably could have found the issue, your odds of getting an extension shoot way up.

Here are a few common situations where those deadlines are often more flexible:

- Future Delivery of Goods or Services: You booked a big vacation package months in advance, but the travel company went bust a week before your trip. In this case, the chargeback clock starts on the date the service was supposed to happen, not the date you paid.

- Defective Merchandise with a Warranty: Your new laptop gives up the ghost six months into a one-year warranty. If the merchant refuses to honor their own warranty terms, you may still have grounds to file a chargeback.

- Recurring Billing Errors: You finally notice a gym membership fee on your statement—for a gym you canceled a year ago. The timeline often resets with each new incorrect charge, giving you a fresh window to dispute it.

Getting familiar with the specific chargeback laws can really help you understand your rights in these more complicated cases. At the end of the day, these extensions exist to make sure you're protected from problems that take a while to surface.

Why Acting Fast Is Your Best Strategy

Knowing the chargeback deadline is one thing, but understanding why you shouldn't wait is a whole different ball game. Procrastinating on a dispute isn't just about getting your money back; it’s about making sure the entire consumer protection system works the way it's supposed to.

When you drag your feet, you’re basically weakening your own case.

Think of it like reporting a minor fender bender. The sooner you get all the details down—pictures, notes, witness info—the clearer the evidence is. Fresh memories, easy-to-find receipts, and recent communication records make your claim much stronger and a whole lot easier for your bank to process. But if you wait weeks or even months? Details get fuzzy, and crucial evidence can disappear.

The financial stakes are climbing, too. In 2024, the average global chargeback amount hit $169.13. With industries like travel and e-commerce seeing massive spikes in disputes, the system is under more pressure than ever. You can dig into more of the eye-opening stats on these rising costs at chargeflow.io.

The Downside of Delaying Your Claim

Waiting until the last minute to dispute a charge is a risky move. It immediately puts you at a disadvantage and can turn what should be a simple process into a major headache. A delayed claim is almost always a weaker claim.

The best way to handle a dispute is to treat it with urgency. When you file promptly, you're presenting the freshest evidence, showing you're on top of things, and making it much harder for a merchant to poke holes in your story.

Here’s why jumping on it right away gives you a clear edge:

- Stronger Evidence: Your memory of what happened is sharpest right after the event. Emails, receipts, and shipping details are also much easier to track down when you haven't let time slip by.

- Faster Resolution: It’s simple: the sooner you kick off the process, the sooner you can get your money back. Delays on your end create a domino effect, slowing down the entire investigation for everyone involved.

- Reduced Risk: Pushing up against the deadline leaves zero room for error. If you miss that window by even a single day, you could lose your right to dispute the charge for good.

At the end of the day, acting fast is the smartest way to get your money back without a fight.

A Step by Step Guide to Filing Your Claim on Time

Ready to dispute a charge but not sure where to start? Acting fast is a big deal, but following the right steps is just as crucial if you want to stay within the time limit for chargeback on credit card rules.

Think of it like building a case for a detective. The more organized you are and the better your story, the higher your chances of winning.

First things first, gather up every scrap of evidence you can find related to the purchase. This is about more than just a receipt; you're trying to paint a complete picture of what went wrong.

- Receipts and Invoices: These are your foundational proof of the transaction.

- Email Correspondence: Any emails between you and the merchant are gold, especially if you already tried to solve the problem directly with them.

- Photos or Videos: Absolutely critical for "product not as described" or "damaged goods" claims. You have to show them, not just tell them.

- Shipping Confirmations: If an item never showed up, proof of the expected delivery date is vital.

Once you have your evidence packet ready, it's time to get in touch with your credit card issuer. Don't waste time calling the merchant again—your bank is your advocate now. Most banks give you a few different ways to kick off a dispute.

Starting the Official Dispute

Usually, the fastest way to get the ball rolling is through your online banking portal. If that's not your style, you can always call the number on the back of your card or even send a formal letter.

Whichever route you take, be ready to give a clear, simple summary of the issue and let them know about the evidence you've collected.

Be specific and just stick to the facts. Clearly state why the charge is wrong, what you actually bought, and how the merchant dropped the ball.

After you file, your bank will give you a case number. Hold onto this! You'll need it to track how your dispute is progressing.

The whole process can take a while, but staying organized and hitting your deadlines gives you the best shot at getting your money back. For a deeper dive into winning strategies, check out our guide on how to win a credit card dispute. It’s packed with extra tips for building an airtight case.

Common Questions About Chargeback Time Limits

Wading through the rules for credit card chargebacks can feel like you're trying to solve a puzzle. It’s totally normal to have questions, so let’s clear up some of the most common ones people have about those all-important deadlines.

What Happens If I Miss the Chargeback Time Limit?

This is the big one. If you miss the filing deadline, your bank will almost certainly reject your dispute. It’s a hard cutoff.

Once that happens, you lose the powerful protection the chargeback process provides. Your only real option left is to try and negotiate a refund directly with the merchant. For very large amounts, you could consider legal action, but that’s a much more expensive and time-consuming road to go down.

Does the Clock Start from the Purchase Date or Delivery Date?

Great question. The answer is, it depends on what you bought. The system is designed to be fair, so the clock doesn’t start ticking until you could have reasonably known there was a problem.

- For in-store purchases or services you get right away, the time limit usually starts right there on the transaction date.

- For online orders or future events (like a concert), the clock often starts from the expected delivery date or the date the service was supposed to take place.

This little rule protects you if a package never shows up or a show gets canceled months after you bought the ticket.

Is the Deadline Different for Fraud Versus a Faulty Product?

Yes, the specific reason for your dispute can sometimes shift the time limit for chargeback on credit card claims, but that general 90 to 120-day window is a solid rule of thumb to keep in mind. Card networks use different "reason codes" for everything from fraud to a product that just isn't what was advertised.

While some of these codes might allow for an extension, it’s always best to act the second you spot an issue. The system is under more pressure than ever, especially with the boom in e-commerce and travel disputes. Globally, the average chargeback-to-transaction ratio sits around 0.60%, but sectors like travel and lodging have seen a massive 816% year-over-year jump in chargebacks. You can dig deeper into these numbers with some recent chargeback statistics.

If you have more specific questions, exploring our detailed FAQs about chargebacks can provide even more clarity.

Are you tired of manually fighting chargebacks? ChargePay uses AI to automatically generate winning dispute responses, recovering up to 80% of your lost revenue without you lifting a finger. See how it works at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)