Global network tokenized transactions are projected to reach 574 billion by 2029, and Visa says tokens can produce a 30% reduction in online fraud plus a 4.6% lift in global authorization rates compared with raw card numbers, according to Juniper Research. That should get every Shopify merchant’s attention.

Most store owners hear “tokenization in payments” and file it under technical security stuff. That’s a mistake. This is a revenue topic. It affects fraud exposure, checkout trust, approval rates, and how much damage a breach can do to your business.

It also has one major limit that many payment guides gloss over. Tokenization helps protect card data, but it doesn’t stop a customer from filing a chargeback after a legitimate purchase. If you sell on Shopify, you need to understand both sides: what tokenization solves, and what it leaves untouched.

What Is Payment Tokenization in Simple Terms

Think of a customer’s card number like a master key to a building. If someone steals it, they can open far too many doors. Tokenization swaps that master key for a valet key. The valet key works for one specific purpose, but it can’t open every door.

That replacement value is the token.

What gets replaced

When a customer enters their card at checkout, the sensitive card number isn’t meant to stay in your systems. Instead, a token stands in for it. That token can be used to process a payment, save a card for future orders, or run a subscription, but it isn’t the original card number.

If a criminal gets the token, they don’t get the original payment data. That’s the core benefit. Tokenization isn’t just hiding the card number. It’s replacing it with something that has no useful value on its own.

Practical rule: If your store never keeps raw card data, a payment data breach becomes far less damaging.

This is why tokenization in payments has become the normal setup for modern ecommerce. Merchants want fewer fraud problems, less sensitive data exposure, and more confidence that one security mistake won’t turn into a much larger mess.

Why this matters to a Shopify merchant

For a Shopify store owner, the question isn’t “Is tokenization technically elegant?” The key question is, “Does it protect revenue?”

Yes, in several ways. It lowers the risk attached to stored card data. It supports safer repeat purchases. It helps card networks and issuers verify transactions more safely. And, as noted earlier, token-based transactions can improve approvals and reduce online fraud through network tokenization.

You can also think of tokenization as part of a bigger shift in how digital ownership and digital value are handled. If you’re curious how the same replacement concept shows up outside card payments, this overview of Gold Tokenization gives a helpful parallel.

The simple takeaway

If you remember one thing, remember this: tokenization lets your store use payment data without carrying the full risk of storing original data.

That doesn’t solve every payment problem. But it’s a major upgrade over handling raw card numbers, and it’s one of the reasons secure ecommerce checkout works the way it does now.

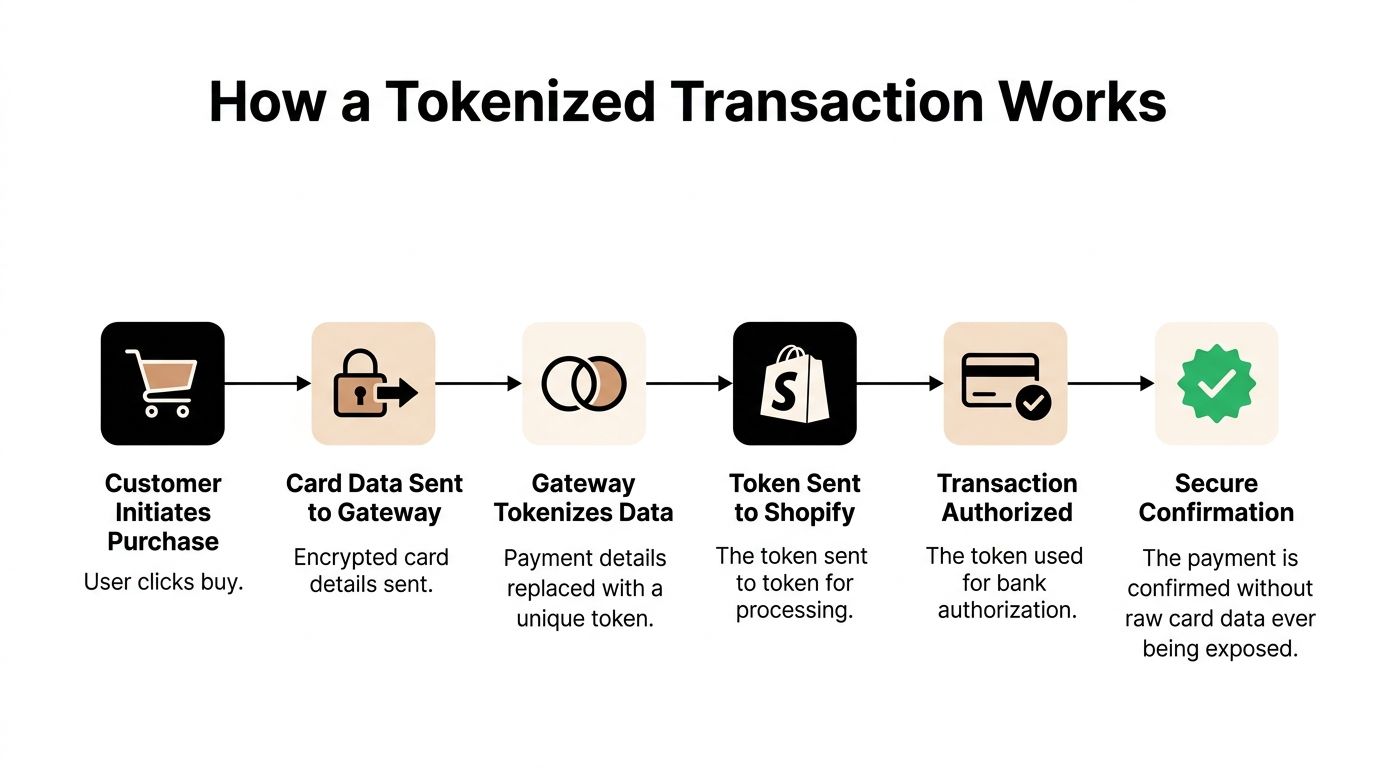

How a Tokenized Transaction Actually Works

The flow is less mysterious than it sounds. A tokenized payment follows a clear chain of events between your customer, your checkout, your payment gateway, the card network, and the bank.

This visual makes the sequence easier to follow.

The payment flow step by step

The customer starts checkout

A shopper enters card details on your Shopify store or uses a saved payment method.The payment system requests a token

The card details go through the payment setup so a token service provider can create an EMV Payment Token.The actual card number is stored securely elsewhere

The original Primary Account Number, often shortened to PAN, is kept by the token service provider or network. Your store should only deal with the token.A cryptogram is created for the transaction

This acts as an added proof layer tied to that payment event.The token moves through authorization

Your acquirer and the network route the tokenized transaction for issuer approval.The issuer approves or declines

Actual card details can be matched securely in the background without exposing them to your store systems.

What merchants usually get confused about

A lot of merchants assume the token is just a scrambled version of the card number. It isn’t. Stripe explains that the token is a unique EMV Payment Token with no mathematical link to the original card number, and this approach can reduce PCI DSS scope by as much as 80-90% because you no longer store or transmit sensitive cardholder data, as covered in Stripe’s payment tokenization explainer.

That distinction matters. If there’s no mathematical link, stealing the token doesn’t help an attacker reconstruct the original PAN.

The safest card number for your store is the one your systems never have to keep.

Where Shopify fits in

If you use Shopify Payments or another mainstream gateway, much of this happens behind the scenes. You don’t need to manually build tokenization infrastructure. But you do need to understand who does what, especially when you’re troubleshooting declines, dealing with stored cards, or reviewing your PCI exposure.

If you want a quick refresher on the roles of gateways, processors, and acquirers, ChargePay’s guide to what a payment processor is helps connect the moving parts.

The revenue angle

For a merchant, the operational value is simple. The less sensitive card data you touch, the less liability sits on your side. That reduces breach risk and narrows the amount of payment data your business has to protect directly.

Tokenization also supports recurring billing and stored card experiences without forcing customers to re-enter details every time. That convenience matters for repeat purchase businesses, subscription brands, and stores trying to remove checkout friction without opening up bigger security risks.

Tokenization vs Encryption What Merchants Must Know

Merchants mix these up all the time. They’re related, but they are not the same thing.

Encryption protects data by scrambling it so only someone with the right key can read it.

Tokenization protects data by replacing it with a different value.

That sounds like a small difference. In practice, it changes your risk profile.

The simplest way to think about it

Encryption is like locking a paper with sensitive information in a safe. The information still exists inside. If someone gets the safe open and finds the key, they can read it.

Tokenization is like replacing that paper with a claim ticket. The ticket points to the actual item somewhere else, but the ticket itself doesn’t reveal the original information.

That’s why merchants often prefer tokenization for stored payment details. It reduces the value of stolen data.

Tokenization vs Encryption at a Glance

| Aspect | Encryption | Tokenization |

|---|---|---|

| What happens to the original data | It stays the same, but becomes unreadable without a key | It gets replaced with a separate token |

| If stolen | Attackers may still target keys or decryption paths | Tokens are generally useless on their own |

| Typical merchant concern | Protecting data in storage or transit | Avoiding storage of sensitive card data in the first place |

| PCI impact | Sensitive data may still remain in scope | Scope can be reduced because raw card data is removed from merchant systems |

| Best fit | Broad data security use cases | Payment credentials, stored cards, recurring billing |

Not all tokenization works the same way

Worldpay distinguishes between vault-based and vault-less tokenization in its explanation of how tokenization works. In vault-based models, the original card number sits in a secure central vault. In vault-less models, tokens are generated without relying on one central storage point. Worldpay also notes that both methods render stolen data “useless to fraudsters,” and some benchmarks show a 40-50% reduction in fraud for card-on-file scenarios.

That’s useful for stores with saved cards, subscriptions, and repeat buyers.

Merchant takeaway: Encryption helps protect sensitive data. Tokenization helps remove it from your environment.

If you want a deeper breakdown of where each method fits, ChargePay’s comparison of tokenization vs encryption is worth reading.

Why this matters for chargebacks

Encryption mainly answers a security question. Tokenization answers a security and storage question. Neither one, by itself, answers the question that matters after a dispute lands in your dashboard: Can you prove the charge was valid?

That’s where merchants need to separate payment security from dispute management.

The Real-World Benefits for Your Shopify Store

Payment tokenization is growing for a reason. The global market for payment tokenization was valued at $2.1 billion in 2024 and is forecast to grow because it addresses practical business problems, according to Market Intelo’s tokenization market report. The same report notes that up to 18% of online carts are abandoned due to payment trust issues.

That trust gap shows up at checkout every day.

Benefit one: less breach exposure

If your store isn’t storing raw card numbers, there’s less sensitive payment data for attackers to target through your environment. That lowers the blast radius of a security incident.

For a Shopify merchant, this matters beyond compliance checkboxes. A payment data incident can trigger customer distrust, extra operational work, and a lot of cleanup that has nothing to do with selling products.

Benefit two: smoother PCI compliance

Merchants often dread PCI DSS because it feels technical and time-consuming. Tokenization helps by moving sensitive cardholder data away from your systems.

That means less direct handling of high-risk payment information. Less handling usually means less complexity.

Benefit three: better checkout trust

Customers don’t see the word “tokenization” at checkout, but they feel the result. They’re more willing to complete a purchase when payment feels secure and familiar.

That matters because hesitation at the payment step is expensive. If trust issues are causing cart abandonment, reducing perceived risk can help recover otherwise lost orders.

Benefit four: easier repeat purchases

Saved cards, subscriptions, and one-click style reorders all work better when the card details are stored as tokens rather than raw account numbers. Customers get convenience. You get less exposure.

This is especially helpful for brands with repeat buying patterns, from supplements to beauty to replacement products.

Why this matters in a Shopify stack

Shopify gives merchants strong payment infrastructure, but store setup still matters. If you’re evaluating the broader fit of Shopify for your business, this analysis on Is Shopify the right choice for your e-commerce business is a helpful complement to the payment side of the discussion.

For fraud controls around checkout, order review, and customer behavior, ChargePay also has a practical guide to Shopify fraud prevention.

Security that helps checkout performance is better than security that only adds friction.

The short version is this. Tokenization in payments is good for protection, good for trust, and good for removing risk from stored card data. Those are real business benefits, not just backend technical upgrades.

Why Tokenization Does Not Stop Friendly Fraud Chargebacks

Many merchants often get blindsided.

A store can have strong payment security, tokenized transactions, and a reputable gateway, then still lose money to chargebacks. That’s because many disputes aren’t caused by stolen card data at all.

The blind spot

According to ACI Worldwide’s discussion of tokenization challenges, friendly fraud can comprise 40-70% of all chargebacks, and tokenization doesn’t prevent those disputes, as noted in ACI Worldwide’s PDF on the benefits and challenges of tokenization.

A customer can make a real purchase with their real card, receive the product, and still dispute the charge later.

Why? Common reasons include:

- The cardholder doesn’t recognize the descriptor and assumes the charge is unauthorized.

- The buyer forgets the purchase and disputes it with their bank.

- A family member placed the order and the cardholder didn’t know.

- The customer is unhappy after delivery and goes straight to a chargeback instead of contacting support.

- The buyer abuses the system to keep the item and claw back the payment.

What tokenization actually proves

Tokenization helps show that the payment details were handled securely. It helps reduce exposure to card data theft. It supports cleaner payment flows.

It does not prove the customer’s intent.

It does not prove satisfaction with the product.

It does not prove that the bank will side with you in a dispute.

A secure transaction can still become an expensive chargeback.

That’s the core separation merchants need to understand. Payment fraud prevention and chargeback prevention overlap, but they’re not the same system.

Why this matters for store operations

If you run a Shopify store, you already think about conversion, fulfillment, and retention. You should treat disputes the same way. Strong security tools protect the transaction before and during checkout. Chargeback strategy protects the revenue after the order is placed.

This is also why broader store quality still matters. A confusing checkout, weak order communication, vague billing descriptor, or slow support response can create disputes even if the payment itself was perfectly secure. If you’re improving your store foundation more broadly, this e-commerce website development guide is a useful reference.

For a closer look at this specific problem, ChargePay’s guide on friendly fraud breaks down why valid orders still get disputed.

The practical takeaway

Tokenization should absolutely be part of your payment setup. But don’t expect it to solve post-purchase conflict. It won’t. A token can protect card data. It can’t stop a customer from pressing the dispute button.

How to Protect Your Revenue Beyond Tokenization

Tokenization is your front-line payment security layer. Keep it. If you use Shopify Payments, Stripe, or PayPal, your setup likely already includes tokenization in some form.

That’s the starting point, not the finish line.

Build a full revenue protection stack

Merchants who want fewer losses usually need four things working together:

Secure payment handling

Use tokenized payment flows through trusted gateways so raw card data doesn’t live in your store environment.Clean checkout and billing clarity

Make your store name recognizable on statements, reduce surprise subscriptions, and set clear shipping expectations.Strong post-purchase records

Keep order confirmations, delivery details, customer communication, refund history, and any proof tied to the transaction.Dispute response systems

Have a process for identifying valid claims, spotting likely friendly fraud, and responding before issuer deadlines.

Why the last piece matters most

A lot of merchants invest in fraud prevention and then handle disputes manually. That creates a gap. Staff members scramble for screenshots, search inboxes, export tracking details, and try to write a convincing rebuttal under time pressure.

That process doesn’t scale well, especially once dispute volume rises.

Bottom line: Tokenization protects the payment credential. Chargeback prevention protects the cash from the sale.

If you want to tighten your process around alerts, evidence, and representment workflows, this ChargePay guide to chargeback prevention is a strong next read.

A better way to think about tokenization in payments

For Shopify merchants, tokenization belongs in the same mental bucket as fraud filters, clear descriptors, order tracking, support workflows, and dispute evidence. It isn’t a standalone fix. It’s one piece of a system that protects revenue at different stages of the order lifecycle.

That is the primary lesson.

Use tokenization to reduce payment data risk. Use chargeback controls to defend the sale after it happens.

If chargebacks are eating into your margins, ChargePay is built to close the gap tokenization can’t. It automatically fights disputes for Shopify merchants, detects friendly fraud, builds evidence packages, and submits responses before deadlines. ChargePay reports a 92.4% win rate across 200K+ cases and $10.8M+ recovered for merchants, with a 4.9-star Shopify App Store rating and a Built for Shopify badge. If you want automated dispute recovery on a pay-per-win model, install ChargePay from the Shopify App Store.

.svg)

.svg)

.svg)

.svg)