A Visa chargeback is what happens when a customer sidesteps your store’s return policy and goes straight to their bank to force a refund. The bank reverses the transaction, pulling the money right back out of your account. For you as a Shopify merchant, it’s not just a lost sale—it's a direct hit to your revenue, plus a penalty fee for your trouble.

Why Your Revenue Is Disappearing to Visa Chargebacks

That sinking feeling when a 'notification of chargeback' email lands in your inbox is all too familiar. It feels like a punch to the gut. One minute you have a completed sale, and the next, money is being yanked from your bank account—often weeks after you’ve already shipped the product. You are not alone in this fight.

The scale of this problem is staggering. Chargeback fraud makes up a whopping 75% of all Visa chargebacks, costing merchants over $170 billion in annual losses in the US alone. What’s worse? "Friendly fraud" is the main driver, accounting for 61% of all Visa chargebacks that started as legitimate purchases.

This isn't some abstract number—it's real money pulled straight from your bottom line, turning satisfied customers into accidental villains who hit 'dispute' on a whim.

But here’s the good news: you don't have to write these off as a cost of doing business. There's a clear path to getting your money back and protecting your store for good.

A Visa Chargeback at a Glance

At its core, a Visa chargeback involves a few key players and stages. Getting a handle on who's who is the first step toward building a winning defense.

Here’s a quick breakdown of the moving parts:

| Component | What It Means for Your Store |

|---|---|

| Cardholder | Your customer who kicks off the dispute with their bank. |

| Issuing Bank | The customer's bank (like Chase or Bank of America) that files the chargeback for them. |

| Acquiring Bank | Your bank or payment processor (like Shopify Payments) that gets hit with the dispute. |

| Merchant | You. The one who has to prove the charge was legitimate or lose the money. |

| Representment | The process where you submit evidence to fight the chargeback and prove your case. |

Grasping these roles helps clarify exactly what you're up against every time a dispute notice arrives.

Most merchants try to fight these disputes manually, but it's a confusing, time-consuming process that rarely works. You're up against tight deadlines and a mountain of complex banking rules. That’s where automation becomes a true game-changer.

At ChargePay, we’ve helped thousands of Shopify merchants just like you by fully automating the entire dispute process. Our AI gets to work the second a chargeback hits, analyzing the reason code and submitting a perfectly crafted evidence package.

The results speak for themselves:

- An impressive 92.4% win rate across all disputes.

- Over 100,000 chargebacks handled.

- More than $2.8 million in revenue recovered for our merchants.

This guide will walk you through everything you need to know about a Visa chargeback, from how the process works to building an airtight defense. Before we dive in, you might also want to check out our complete guide to chargeback prevention strategies.

Understanding the True Cost of a Visa Chargeback

When you get a Visa chargeback, it's easy to think of it as just a simple refund. But it's not. Think of it as a customer forcing a refund through their bank, sidestepping you and your store's return policy entirely. This single action triggers a formal dispute process, and the fallout goes way beyond just losing the money from that one sale.

Every chargeback sets off a chain reaction that costs you both time and money. There are a few key players you need to know:

- The Cardholder: This is your customer, the one who kicked off the dispute.

- The Issuer: The customer’s bank, which files the chargeback for them.

- The Acquirer: Your bank or payment processor (like Shopify Payments) that has to handle the dispute from your end.

- The Merchant: That’s you, the store owner now tasked with proving the transaction was legitimate.

Getting a handle on these roles is important, because once the ball gets rolling, you’re on the hook for a lot more than just the original sale amount.

The Hidden Financial Drain

The first hit you'll feel is the lost revenue from the sale itself. But the financial bleeding doesn't stop there. For every single chargeback, your acquiring bank slaps you with a non-refundable chargeback fee.

This fee usually lands somewhere between $15 and $100, and you have to pay it whether you win or lose the dispute. If you want to dig deeper into this specific cost, you can learn more about chargeback fees in our detailed guide.

Let's put that in perspective. Imagine you sell a $50 product. A chargeback comes through, and that $50 is gone. Then, your acquirer tacks on a $25 fee. Suddenly, you're out $75 plus the cost of the product you already shipped. If you get just 10 of these a month, that's an extra $250 in fees alone, on top of the $500 in lost sales. For a growing store, those numbers add up fast.

The Risk of High-Risk Monitoring Programs

This is where things get really serious. Visa keeps a close watch on merchants and their acquiring banks through programs like the Visa Acquirer Monitoring Program (VAMP). This program tracks your dispute-to-transaction ratio. If your store racks up too many chargebacks, you risk getting flagged as "high-risk."

Starting in October 2025, Visa's enforcement of VAMP gets even stricter. Merchants with a dispute ratio above 1.5% could be looking at severe penalties that go far beyond standard fees.

Being placed in a monitoring program like VAMP can set off a cascade of other problems:

- Heavier Fines: You’ll face escalating penalties for every new dispute you get.

- Increased Scrutiny: Your acquirer might start placing holds on your funds or require you to keep a cash reserve.

- Account Termination: In a worst-case scenario, your payment processor could shut down your merchant account completely, leaving you unable to accept credit card payments at all.

Ignoring a Visa chargeback is never an option. Each one is a black mark against your business's health. Managing them proactively isn't just about getting sales back; it's about protecting your very ability to do business. This is why having an automated system in your corner is so critical. At ChargePay, we’ve recovered over $2.8 million for merchants by fighting every single dispute, making sure their businesses stay healthy and profitable.

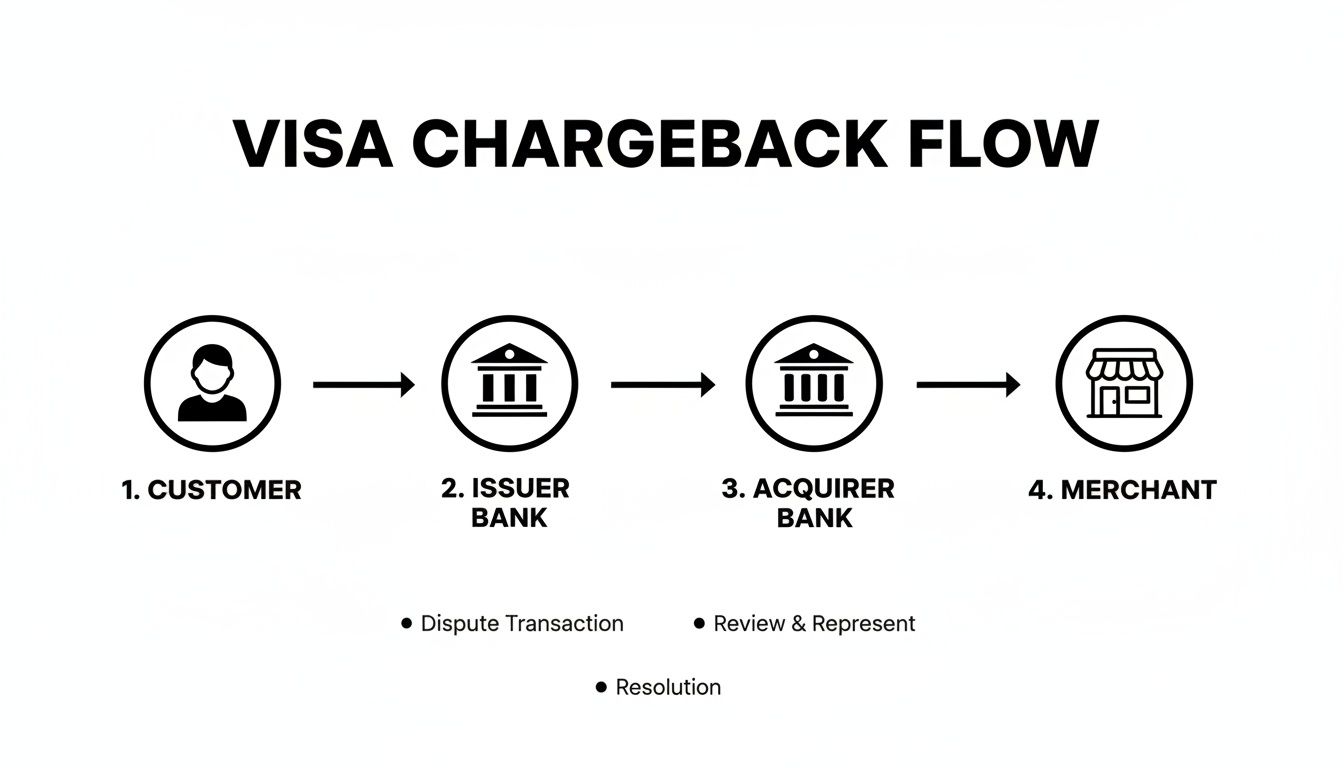

Navigating the Visa Chargeback Process and Deadlines

When that first Visa chargeback alert lands in your inbox, it can feel like you’ve been thrown into a maze with no map. The whole process is confusing, the terms sound like a foreign language, and there’s a clock ticking somewhere in the background. But getting a handle on the journey a dispute takes is the first step to getting back in control.

The system that governs all of this is Visa’s Claims Resolution (VCR) framework, and it's built for speed. The problem? That speed often works against you, the merchant. As e-commerce has exploded, so have Visa chargebacks. We're seeing global volumes rocket from 238 million and heading toward an estimated 337 million by 2026—that’s a massive 42% jump. For store owners, this means more dispute alerts, more headaches, and more revenue at risk.

This chart breaks down the typical path a Visa chargeback takes, showing how a simple customer complaint travels all the way to your store.

As you can see, by the time you even get the notification, the dispute has already made its way through the customer's bank (the Issuer) and your bank (the Acquirer). Each of those stops eats away at your precious time to respond.

The Stages of a Visa Chargeback

The VCR process isn’t just one single event; it's more like a conversation between banks, with your money caught in the middle. Knowing what happens at each stage helps you figure out what’s coming next so you can build your defense.

Here’s a simple play-by-play of the journey:

Initial Dispute (Inquiry): The moment your customer calls their bank to question a charge, the clock starts. Their bank reviews the claim and decides if it’s worth moving forward. You probably don't even know this is happening yet.

The Dispute Case: If the customer's bank agrees with them, they file an official dispute. Your bank gets notified, the money is pulled from your account, and you finally receive that dreaded chargeback alert. This is when your window to act officially opens.

Representment (Your Fightback): This is your one shot to prove the charge was valid. You need to pull together all your compelling evidence—things like proof of delivery, AVS/CVV results, and any customer emails—and submit it in what’s called a "representment" package. This is where most merchants stumble, either by sending in weak evidence or just missing the deadline completely.

A missed deadline is an automatic loss. There are no do-overs or extensions. Visa's rules are incredibly strict, and once that window slams shut, the money is gone for good.

This is exactly why we designed ChargePay to be fully automated. Our AI platform has already recovered over $2.8 million for Shopify merchants by making sure every dispute is answered right away with a perfectly built evidence package, long before any deadlines are even close.

The All-Important Deadlines

In a chargeback fight, time is everything. Visa gives the banks involved about 20 to 30 days to sort out a dispute. But that's the timeline for the entire process. By the time the news trickles down to you, your actual response window is way shorter.

You often only have 7-14 days to get your evidence together and respond.

This tight deadline is a massive headache for busy store owners. You have to drop what you’re doing to hunt down order details, find tracking numbers, and pull Shopify data, all while trying to run your business. It's the perfect recipe for missed deadlines and lost sales. If you want a deeper look into these timelines, you can read our complete guide on the Visa chargeback time limit.

Ultimately, getting through the Visa chargeback process means being proactive and organized. Every step has its own rules, and every day that goes by lowers your chances of winning. This is the core problem ChargePay was built to solve—we handle the entire messy workflow for you, turning a manual, stressful task into a problem that's solved on autopilot.

How to Decode Visa Reason Codes for Your Defense

When you get hit with a Visa chargeback, the notification comes with a numeric reason code. At first glance, these codes can look like a confusing jumble of numbers, but they’re actually Visa’s way of telling you why the customer disputed the charge in the first place.

Learning to decode them is the first real step in building a solid defense. Think of a reason code as the playbook for your dispute. It tells you exactly what kind of evidence you need to gather to fight back effectively and win. Instead of getting bogged down by a long list of codes, you can simplify things by grouping them into four main categories that cover nearly every dispute a merchant will face.

The Four Main Categories of Visa Chargebacks

Most of the disputes you'll ever see fall neatly into one of these buckets. Just by knowing the category, you can immediately grasp the core of the customer's claim and start pulling together the right proof.

Here are the four key categories:

- Fraud: The customer is claiming they never authorized the transaction.

- Authorization: There was a hiccup with how the payment was approved by the bank.

- Processing Errors: Something went wrong on the technical side of the transaction.

- Consumer Disputes: The customer has an issue with the product or service itself.

Each one of these requires a totally different approach. For example, fighting a fraud claim is all about proving the legitimate cardholder made the purchase. But when you’re fighting a consumer dispute, it’s all about proving you delivered exactly what you promised.

Fraud Codes: The Ones That Hurt Most

This is, by a long shot, the most common type of Visa chargeback you'll come across. These disputes pop up whenever a cardholder says a transaction wasn't made by them.

The code you'll see most often is 10.4: Other Fraud – Card-Absent Environment. This is the catch-all code for pretty much any online transaction the customer claims they didn't make. To win this fight, you have to prove the actual, legitimate cardholder was behind the keyboard when the order was placed.

Your evidence should include things like:

- AVS and CVV match results from your order details.

- IP address data that shows the order was placed from a location that makes sense for the customer.

- Past order history from the same customer, especially if they used the same card or shipping address before.

This is also where "friendly fraud" becomes a massive headache. Friendly fraud—when a legitimate customer disputes a valid charge—is a silent killer for merchants. It now makes up a staggering 45% of all global disputes and is the fastest-growing type of fraud out there. Projections even warn of a 40% rise in these cases by 2026, which will only turn up the heat on store owners. For a deeper look, you can discover more insights about chargeback fraud trends on expertsure.com.

Consumer Dispute Codes: When a Customer Is Unhappy

These disputes aren't about fraud. They’re all about a customer's dissatisfaction with their order. The most common code here is 13.1: Goods or Services Not Received, where the customer is simply claiming their order never showed up.

This is one of the most winnable chargeback types for merchants, but only if you have your documentation in order. Proof of delivery is non-negotiable here.

To win a "Goods Not Received" dispute, your evidence package has to contain:

- A valid tracking number that shows the package was successfully delivered to the customer’s address.

- The name of the shipping carrier you used.

- Proof of delivery confirmation, like a signature or a photo of the package at their door.

Another frequent one is 13.3: Not as Described or Defective Merchandise. Here, the customer claims the product they received is different from what they saw on your store or that it arrived damaged. To fight this, you need to prove your product page was accurate and you sent what was ordered. Screenshots of your product page, detailed descriptions, and any emails or chats with the customer about the item are your best friends here. If you want to dive deeper into these claims, you can learn more about the top reasons for a chargeback in our detailed article.

The table below breaks down some of the most common reason codes you'll see and gives you a clear checklist of the evidence you need to gather for each.

Common Visa Reason Codes and How to Fight Them

| Reason Code Category | Example Code | What It Means | Required Evidence to Win |

|---|---|---|---|

| Fraud | 10.4: Card-Absent Fraud | The cardholder claims they didn't authorize the online transaction. | • AVS & CVV match results • Geolocation/IP address data • Previous order history with the same customer |

| Consumer Dispute | 13.1: Goods Not Received | The customer claims their order never arrived. | • Valid tracking number showing delivery • Shipping carrier name • Proof of delivery confirmation (signature, photo) |

| Consumer Dispute | 13.3: Not as Described | The item received doesn't match the product description or was defective. | • Screenshots of the product page • Product descriptions & photos • Customer service emails or chats |

| Processing Error | 12.6: Duplicate Processing | The customer was charged more than once for the same transaction. | • Transaction logs showing a single charge • Proof of a refund for any duplicate charges |

Having this cheat sheet helps you quickly identify what you're up against and what you need to do to build a strong case.

Of course, understanding these codes is a huge step, but manually matching evidence to codes for every single dispute is a massive time sink. This is exactly where an automated solution like ChargePay gives you a serious advantage. Our platform instantly analyzes the reason code the moment a dispute lands and automatically pulls the precise evidence needed from Shopify to build a winning case—all before you even have to lift a finger. With over 100,000 disputes handled, we know exactly what it takes to win each type of claim.

Building an Airtight Case to Win Your Chargeback

When a Visa chargeback lands on your desk, it’s easy to feel like you’ve already lost. But here’s the thing: it’s not an automatic loss. You get one shot to fight back in a process called representment. This is your moment to submit a package of compelling evidence that proves the transaction was totally legit, directly taking on the customer's claim.

Your goal is to build a case so solid and thorough that it leaves no room for doubt.

Think of yourself as a detective on a case. The chargeback reason code tells you the nature of the alleged "crime" (like "Goods Not Received"), and it’s your job to present undeniable proof that your side of the story is the truth. A weak, thrown-together response is a guaranteed loss. A strong one, however, can get your money right back where it belongs.

Start with a Powerful Rebuttal Letter

Your rebuttal letter is the cover sheet for your evidence package, and first impressions matter. It's a short, professional summary of your case that explains exactly why the chargeback is invalid. This isn't the place to get emotional or tell a long-winded story; it needs to be direct, factual, and incredibly easy for a busy bank agent to scan.

Your letter should clearly lay out:

- The key transaction details (order number, date, amount).

- The specific chargeback reason code you're fighting.

- A quick summary of the evidence you've included and how it proves the charge is valid.

For example, if the claim is "Goods Not Received" (Reason Code 13.1), your letter should immediately point to the attached proof of delivery and tracking number. You want to make the reviewer's job as simple as possible.

The Essential Evidence Checklist

A strong rebuttal letter is just the opening act. The real power of your representment comes from the rock-solid evidence you provide. Honestly, this is where many Shopify merchants stumble, especially with those tight deadlines breathing down their necks. To build an airtight case and seriously boost your odds of winning, keeping meticulous records through effective bookkeeping for Shopify store owners is absolutely critical.

Here is the essential evidence you need to start gathering to win a Visa chargeback:

1. Proof of Delivery

This is a non-negotiable must-have for any "product not received" claim. You have to show the item arrived at the exact address the customer gave you.

- Tracking Number: Include the number from a major carrier like USPS, FedEx, or UPS.

- Delivery Confirmation: Get a screenshot from the carrier’s website showing the "Delivered" status, complete with the date, time, and city/state.

- Delivery Photos or Signatures: If you have one, this is knockout evidence. A photo of the package on the customer's doorstep or a signature on file is incredibly difficult for anyone to dispute.

2. AVS and CVV Match Results

This evidence is your best friend when fighting fraud claims (like Reason Code 10.4). It shows you took the right steps to verify the cardholder when they made the purchase.

- AVS (Address Verification System): A "match" confirms the billing address the customer typed in matches the address their bank has on file.

- CVV (Card Verification Value): A "match" proves the customer had the physical card, or at least knew the 3- or 4-digit security code on the back.

You can find this data right in your Shopify order details. Getting a full match on both AVS and CVV is powerful proof that the legitimate cardholder authorized the transaction.

3. Customer Communication Logs

Any conversation you've had with the customer can help build your case. These records can show their intent and completely dismantle claims of dissatisfaction or non-receipt.

- Emails and Contact Forms: Include any messages where the customer asks about the product, confirms their shipping address, or talks about their order.

- Live Chat Transcripts: Transcripts from your Shopify chat app can prove you provided support or that the customer was fully aware of the purchase.

- Social Media DMs: If a customer slid into your DMs on Instagram or Facebook, a screenshot of that conversation can be surprisingly valuable evidence.

4. IP Address and Geolocation Data

This bit of tech data helps connect the person who placed the order to the cardholder's location. You can find it in your Shopify order analysis. An IP address that matches the customer's billing or shipping city adds a strong layer of proof, especially for fraud claims.

Pulling all of this together manually for every single dispute is a massive time-suck—time you should be spending growing your business. That’s why at ChargePay, we built an AI that does all the heavy lifting for you. Our system, trusted by thousands of Shopify merchants, automatically pulls every piece of relevant evidence from your store, assembles it into a winning response, and submits it for you. We've recovered over $2.8 million for our users this way, proving automation is the key to winning consistently.

Automate Your Chargeback Wins with AI

After walking through the nitty-gritty of building a case—from decoding reason codes to hunting down every last piece of evidence—it's pretty clear that fighting a Visa chargeback yourself is more than just hard work. It's a massive time-suck that just won't work as your store grows.

There's a much smarter way to win.

Instead of getting tangled up in a losing battle against tight deadlines and confusing rules, you can put the entire process on autopilot. Here at ChargePay, we built our AI platform specifically for Shopify merchants to take this entire headache off your plate. We turn a stressful, manual chore into a solved problem.

How AI Turns the Tables on Chargebacks

Picture this: a chargeback alert hits your account. Instead of you scrambling to figure out what to do, our AI gets to work in an instant. It’s not just about getting a response in faster; it’s about submitting a smarter response, every single time.

Here’s how our system works for you:

- Instant Alert & Analysis: The moment a dispute lands, our AI gets the notification and immediately breaks down the reason code to understand what the customer is claiming.

- Automatic Evidence Gathering: The AI then dives straight into your Shopify data, pulling every relevant detail—tracking numbers, AVS/CVV results, IP addresses, and customer emails.

- Custom-Built Response: It assembles a perfectly formatted, custom-tailored representment package designed to fight that specific reason code. All without you lifting a finger.

- Submission Before the Clock Runs Out: The complete evidence package is sent to the bank well before the deadline, making sure you never lose a dispute just because you missed the window.

Putting AI in charge of your chargeback defense also unlocks serious workflow automation benefits, freeing you up to focus on what actually grows your business.

The Proof Is in the Numbers

You don't have to take our word for it—the results speak for themselves. We’ve automated the fight for thousands of Shopify stores, and the numbers show what's possible when you let AI do the heavy lifting.

We've successfully handled over 100,000 disputes, recovering more than $2.8 million for merchants just like you, all with a 92.4% win rate.

As a 'Built for Shopify' app with a 4.9-star rating in the Shopify App Store, ChargePay is the go-to solution for store owners who want to protect their revenue. We handle the entire dispute so you can get back to what you do best—running your business.

Don't let chargebacks drain your bank account and your time. If you want to see how this works in practice, explore our guide on automated chargeback management using AI.

Ready to stop losing money to disputes? Install ChargePay from the Shopify App Store and let our AI start winning back your hard-earned revenue today.

Frequently Asked Questions About Visa Chargebacks

Even after you've dotted all your i's and crossed all your t's, a few lingering questions about how a Visa chargeback works can pop up. Let's tackle some of the most common ones we hear from merchants just like you.

What Is the Difference Between a Visa Chargeback and a Refund?

Think of a refund as a handshake agreement. It’s a process you control, handled directly between you and your customer right in your Shopify store, based on the return policy you've set. It's a friendly resolution.

A Visa chargeback, on the other hand, is a forced reversal of funds. The customer skips talking to you entirely and goes straight to their bank to demand their money back. This drags the banks into it, slaps you with extra fees, and can really hurt your merchant account's standing.

Can I Prevent Visa Chargebacks Before They Happen?

You absolutely can, and prevention is always the smartest move you can make. You can cut down on disputes significantly by focusing on the basics:

- Using fraud filters like CVV and AVS checks.

- Making sure your shipping, return, and product policies are crystal clear.

- Offering top-notch, responsive customer service.

But when it comes to friendly fraud—where a real customer disputes a perfectly valid charge—your best bet is an intelligent system. Our AI has analyzed over 100,000 disputes, so it knows how to spot the subtle patterns of questionable claims before they blow up, protecting your revenue without turning away good customers.

How Long Do I Have to Respond to a Visa Chargeback?

On paper, the official timeline for the whole dispute process is around 20 to 30 days. But that window includes a lot of back-and-forth between the banks before the dispute even lands on your plate.

The reality for you as a Shopify merchant is a much tighter deadline. You'll likely only have 7 to 14 days to pull together all your evidence and submit a winning response. If you miss that window, it's an automatic loss. The money's gone.

This is exactly why an automated system is a game-changer. We’ve recovered over $2.8 million for merchants by making sure a perfectly built response is sent in real-time, every single time.

Stop letting chargebacks steal your revenue. ChargePay automates the entire fight for you, turning a manual headache into a solved problem. Install ChargePay from the Shopify App Store and let our AI start winning back your money today. Find out more at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)