The Address Verification System, often just called AVS, is a simple but powerful tool that fights fraud by checking if a customer's billing address matches the one their bank has on file. Think of it as a quick, automated ID check for online purchases.

What Is the Address Verification System?

Imagine AVS as a digital bouncer for your online store. Every time a customer tries to buy something without their physical card present—what we call a card-not-present (CNP) transaction—AVS steps in to do a quick check.

It takes the numbers from the billing address (the street number and ZIP code) and asks the customer's bank, "Hey, does this look right to you?"

This all happens in a blink of an eye. The bank sends back a simple code telling you if it was a perfect match, a partial match, or a total miss. This isn't just a fancy feature; it's your first line of defense against fraudsters who might have stolen a credit card number but probably don't know the cardholder's exact billing address.

Why AVS Matters for E-commerce

The big card networks rolled out AVS back in the 1990s to deal with the growing problem of fraud in mail-order and phone-order sales. Today, it’s more critical than ever. With online and other CNP sales now making up a whopping 63% of all merchant transactions worldwide, it's no surprise that most payment disputes start right here. If you want to dive deeper, Mastercard's 2025 report has some great insights on the true cost of chargebacks.

The system works by sending the address details through a payment processor to the bank that issued the card. The bank then does the check and reports back.

Think of it this way: AVS doesn’t catch every single fraud attempt, but it creates a pretty big hurdle. It filters out the most common, low-effort fraud attempts, saving you a ton of time, money, and the headaches that come with chargebacks.

This check is a key part of e-commerce security. It helps confirm that the person making the purchase is very likely the legitimate owner of the card, creating a safer experience for both you and your customers.

The AVS Journey From Checkout to Approval

Ever wondered what really happens in those few seconds after a customer clicks "Buy Now"? It's not magic, but a rapid-fire security check happening behind the scenes. The Address Verification System, or AVS, plays a starring role in this process, protecting your business from potential fraud.

Think of it like a lightning-fast game of telephone. The moment your customer enters their payment details and hits submit, it kicks off a chain reaction. That information doesn't just sit on your website; it travels across the internet and back in just a couple of seconds.

Following the Data Trail

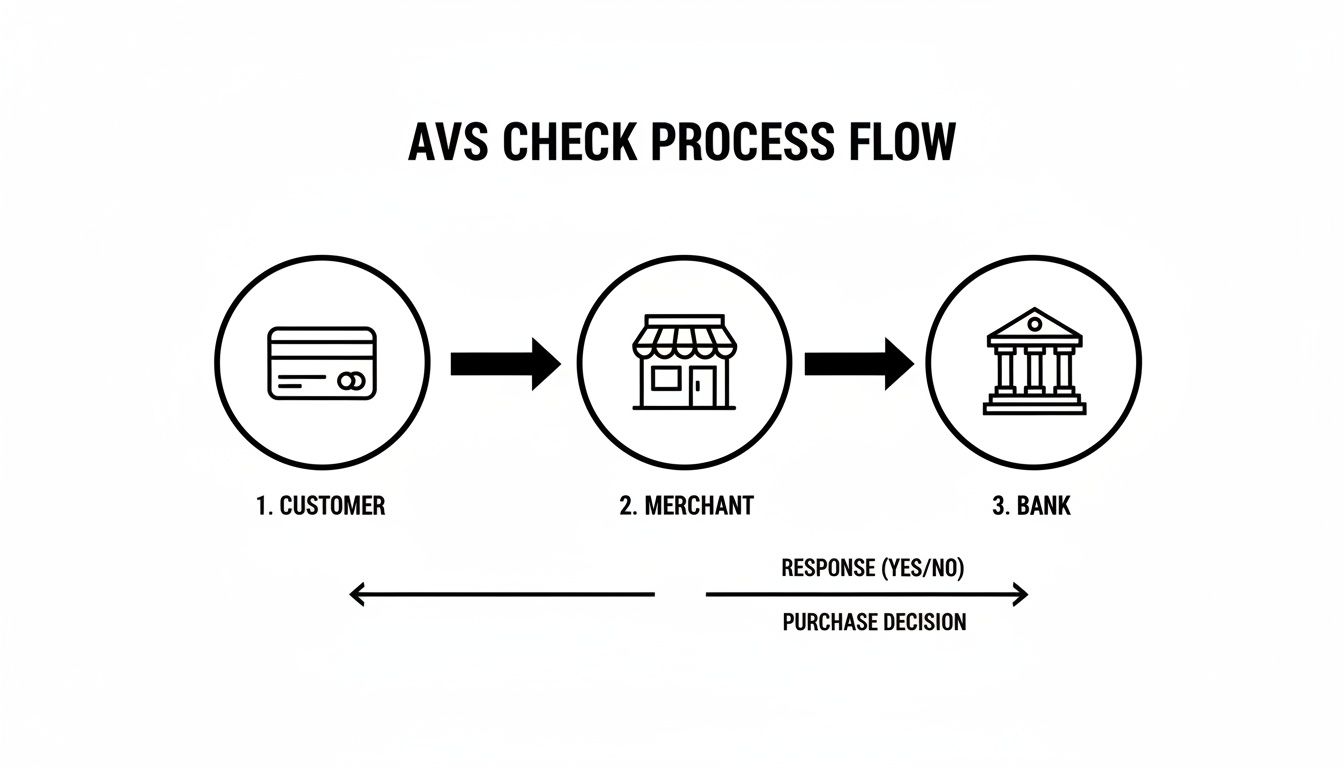

The entire AVS journey unfolds in a precise sequence, zipping from the customer's browser all the way to their bank and then back to your store. This flow is designed to verify the address information securely before the transaction gets the final green light.

Here’s a simple visual of how that AVS process flows from checkout to the bank's response.

As the diagram shows, the request travels from your site to the payment gateway, then to the card network, and finally to the issuing bank where the actual check happens.

The core of the AVS check is surprisingly simple: the customer’s bank compares the numeric parts of the street address and ZIP code entered at checkout with what it has on file. It then sends back a single-letter response code.

This whole round trip—from your customer confirming their purchase to you getting the bank's verdict—is incredibly fast. It has to be. The process is designed to be almost invisible to the customer, preventing any frustrating delays that might cause them to leave.

A smooth AVS check is also a key piece of the puzzle to reduce shopping cart abandonment. By making sure your checkout process is seamless, you keep legitimate customers happy. This split-second verification is a tiny step in the customer's journey but a massive leap for your store's security.

How to Read AVS Response Codes

When you submit a transaction, the Address Verification System pings the customer's bank and spits back a single-letter code. Think of these AVS codes as traffic signals for your fraud-prevention strategy—they tell you whether to stop, slow down, or proceed with confidence.

Knowing how to translate these technical responses into smart business decisions is what separates seasoned merchants from the rest.

To keep things simple, we can sort these AVS codes into three buckets: green light, yellow light, and red light. This quick mental model helps you instantly gauge the risk level of an order.

Green Light: Full Match

A green light is exactly what it sounds like—the best possible outcome. It means the numeric parts of the street address and the ZIP code the customer entered are a perfect match for what their bank has on file.

- Code Y or F: You have a full match. Both the street address numbers and the 5-digit ZIP code are correct.

For most online stores, this is an automatic green light to approve the order. It’s a strong signal that the person placing the order is the legitimate cardholder.

Yellow Light: Partial Match

A yellow light code is your cue to slow down and take a closer look. These codes mean one piece of the address matched, but the other didn’t. This happens all the time and isn’t an automatic sign of fraud.

For instance, a customer might have just moved and updated their ZIP code with the bank but forgot to change the street address. Or maybe they’re shipping a gift to a friend and got the billing and shipping addresses mixed up during checkout.

These partial matches require a bit of judgment. The most common yellow light codes you’ll see are:

- Code A: The street address numbers match, but the ZIP code is wrong.

- Code W or Z: The 5-digit ZIP code matches, but the street address numbers are off.

These transactions usually need a bit more investigation. You can dig deeper into interpreting these more nuanced signals in our full guide to credit card AVS codes.

Red Light: No Match or System Error

Finally, a red light code is a major warning sign. These codes flag high-risk situations where you should probably hit the brakes and decline the transaction. They pop up when nothing matches or when the system couldn't process the check.

- Code N: No match. Neither the street address nor the ZIP code matches what the bank has. This is a massive red flag for fraud.

- Code U: Unavailable. This usually means the card-issuing bank doesn’t support AVS, which is common with international cards.

- Code R: Retry. The AVS system was temporarily unavailable. You can simply ask the customer to try entering their information again.

A Merchant's Guide to Common AVS Codes

Feeling a little overwhelmed by the alphabet soup of AVS responses? Don't be. Most of the time, you'll only encounter a handful of these codes.

Use this quick reference table to understand the most frequent AVS responses and figure out your next move.

Think of these codes not as rigid rules but as valuable pieces of data. When combined with other fraud signals—like CVV match results, IP location, and order size—they give you a much clearer picture of who you're dealing with.

Using AVS Signals to Make Smarter Decisions

Getting an AVS response code back from the bank is just the first step. The real magic happens when you use that signal as part of a bigger fraud prevention strategy, not just as a simple yes/no switch for every order.

A single AVS match or mismatch rarely tells you the whole story. To make smarter decisions, you have to look at the AVS result alongside other important clues. Think of yourself as a detective piecing together the evidence for each transaction.

For example, a partial AVS match on its own might not be a huge deal. But what if it’s paired with a failed CVV check, it's a high-value order, and the shipping address is thousands of miles from the billing address? All of a sudden, that small yellow flag starts to look like a massive red one.

Building Your Rule-Based Defense

Most modern payment gateways let you create custom rules that automatically handle transactions based on these combined signals. This is how you build a balanced defense that catches fraudsters without frustrating legitimate customers who just made a typo.

You can set up rules to:

- Automatically approve transactions that have a full AVS and CVV match. No need to second-guess the good ones.

- Flag for manual review if there's a partial AVS match but the CVV is correct. It’s worth a second look.

- Automatically decline any order where AVS, CVV, and IP location checks all come back negative.

This layered approach is a core part of effective transaction monitoring solutions. It helps you automate the easy decisions and focus your attention where it's truly needed.

The goal is to create a smart filter, not a brick wall. Your rules should be flexible enough to account for common customer mistakes while being tough on the clear signs of fraud.

Manually reviewing every partial match is expensive and time-consuming, which is why many merchants just write off low-value disputes. In fact, about 16% of chargebacks are never even contested for this very reason. With chargeback losses projected to hit a staggering $41.69 billion by 2028, merchants are increasingly turning to automated platforms that combine AVS signals with other data to fight back more effectively.

When AVS Is Not Enough

While the Address Verification System is a fantastic first line of defense, it’s not a silver bullet. You have to understand its blind spots to build a security strategy that actually protects your business without accidentally turning away good customers.

AVS can be a bit blunt. For instance, a simple typo when a customer is rushing to enter their address can trigger a mismatch, leading to a "false decline" where you reject a perfectly legitimate order. It's an easy mistake to make.

Customers who have recently moved might also get flagged if they haven't gotten around to updating their billing info with their bank. These situations show exactly why leaning on AVS alone can be a risky move.

Handling International Transactions

The biggest challenge with AVS is that it’s not a global system. It works like a charm in the US, UK, and Canada, but support gets patchy pretty much everywhere else.

Many international banks just don't participate. This means you’ll often get a "U for Unavailable" response code, which tells you absolutely nothing about how risky the transaction is.

When you're selling to customers outside these core regions, you need other tools in your belt. A layered defense is the name of the game here. For these orders, you should lean more heavily on other signals:

- CVV Match: Always, always require the 3-digit (or 4-digit for Amex) security code from the back of the card. A correct CVV is a strong sign that the customer physically has the card in their hand.

- 3D Secure: This adds an extra authentication step at checkout, like a one-time password sent to the cardholder's phone. To get the full rundown, check out our guide on what is 3-D Secure authentication.

Building a Stronger Defense

When AVS data just isn't giving you the full picture, integrating with comprehensive identity verification software solutions can add a much-needed deeper layer of security.

The bottom line is that AVS is a powerful signal, but it's just one piece of the puzzle. It’s most effective when used as part of a broader strategy that considers multiple data points.

By understanding where AVS falls short, you can prepare for those scenarios. You’ll be able to build a smarter, more resilient fraud prevention system that protects your revenue and keeps your customers happy, no matter where they are in the world.

Got Questions About AVS? We've Got Answers.

Even once you get the hang of AVS, some real-world questions always pop up when you start putting it into practice. Let's walk through a few of the most common ones so you can sharpen your fraud strategy and use the Address Verification System like a pro.

Does a Full AVS Match Guarantee a Sale Is Legitimate?

Not exactly. A full AVS match is a great sign, but it's not a silver bullet. Think about it: if a fraudster has managed to steal a complete set of card details—and that includes the billing address—they can still sail right through the check.

A perfect AVS match just confirms the numbers in the address line up with what the bank has on file. It doesn't actually verify the person making the purchase. This is exactly why AVS should be just one piece of your security puzzle. You should always use it with other checks like CVV verification, IP geolocation, and even a quick look at the order size to get a fuller, more accurate picture of the risk involved.

How Should I Handle AVS for International Orders?

This is a big one. AVS support gets pretty spotty once you go outside of the US, UK, and Canada. As a result, you’ll frequently see a "not supported" response code for international orders. This code doesn't mean the transaction is a scam; it just means the check couldn't happen.

For your international customers, it’s smart to ease up on how much weight you give the AVS result. Instead, shift your focus to other security signals that work better across borders.

- CVV Match: This is non-negotiable. Always require the security code on the back of the card.

- 3D Secure: Using systems like Visa Secure adds a much stronger authentication step that has wide support internationally.

By adjusting your approach for international sales, you can cut down on false declines and stop turning away good customers just because their bank doesn't support AVS. It’s a simple shift that helps you grow your global sales safely.

Can I Customize My AVS Rules?

You bet. Most payment platforms you’re already using—like Stripe, PayPal, and Shopify Payments—let you set up your own AVS rules right in their fraud prevention settings. This kind of control is vital for striking the right balance between tight security and a smooth customer experience.

For instance, you could create a rule that automatically blocks any transaction where the ZIP code is a mismatch. Or, you could have another rule that just flags an order for a quick manual review if there's only a partial match on the address. Jump into your payment gateway’s dashboard and see what options you have. Tweaking these settings helps you build a smarter, more effective defense against fraud that’s tailored to your business.

Stop losing revenue to fraudulent chargebacks. ChargePay uses AI to automate the entire dispute process, recovering up to 80% of your lost funds without any manual work. Protect your business today.

.svg)

.svg)

.svg)

.svg)