You log into Shopify, see a dispute for Item Not as Described, and your first reaction is usually the same: “That's ridiculous. The product is fine.”

Sometimes you're right. Sometimes the customer is gaming the system. But a lot of chargebacks start earlier, with a blurry product photo, a missing size detail, a return policy that's hard to find, or a cancellation flow that creates friction. By the time the dispute hits your dashboard, the legal issue has already turned into a payment problem.

That's the part most merchants miss. Consumer protection laws don't sit in some distant legal file. They show up as lost revenue, higher dispute volume, weaker evidence, and more refunds forced through card networks. We've seen the same pattern across store audits and dispute reviews. If your catalog data is messy, your evidence will be messy too. That's why disciplined product data work, including AI-driven data quality steps, matters well beyond merchandising.

You also need to understand the direct cost of each dispute, not just the order value. If you haven't looked closely at the real impact of a chargeback fee, do that. It changes how you think about prevention.

Why Consumer Protection Laws Matter for Your Bottom Line

A chargeback rarely starts at the bank.

It usually starts on your site. A shopper thinks the product looked different in the photos. They expected delivery by a certain date because your shipping copy implied it. They thought a subscription would be easy to cancel, but the path was buried. They saw one price on the product page and a higher total at checkout.

The revenue problem is bigger than the legal problem

When merchants hear “consumer protection laws,” they think lawsuits, regulators, and paperwork. That's too narrow. For a Shopify store, the first impact is operational:

- More disputes because buyers feel misled or trapped

- Weaker representment evidence because your own store records don't clearly support your position

- Higher refund pressure because support can't point to clean, customer-facing disclosures

- More friendly fraud opportunities because ambiguity gives bad actors a better story

Practical rule: If a reasonable customer can misunderstand your page, a bank reviewer can too.

That's why this topic matters. The dispute team can't fix what the storefront broke. If your product page, checkout, and policy stack create confusion, your payment processor becomes the cleanup crew, and you pay for it.

Compliance gives you evidence, not just protection

Good compliance does two jobs at once.

First, it lowers the odds of a dispute. Second, it creates the exact evidence you need when a dispute still happens. Clear product descriptions, visible delivery estimates, timestamped consent, accessible cancellation terms, and documented customer communication all strengthen your position.

Think of compliance as an evidence system. Not a legal memo. Not a checkbox exercise. An evidence system.

If your store says one thing, your order confirmation says another, and your support team improvises the rest, you're handing the customer the better narrative. Banks often decide on narratives backed by records. You need the cleaner record.

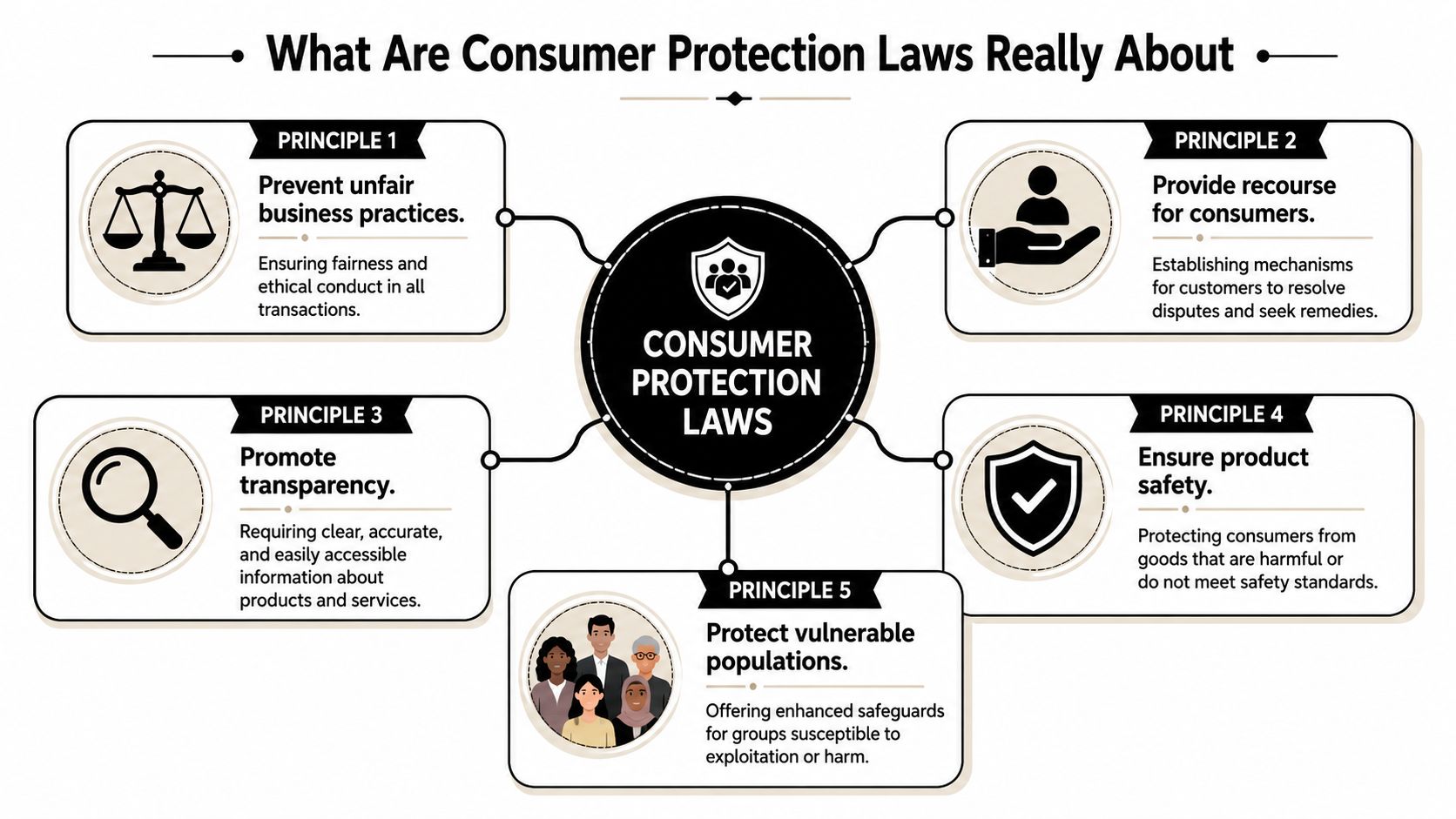

What Are Consumer Protection Laws Really About

Most consumer protection laws boil down to five plain-English rules. Don't confuse people. Don't hide the ball. Don't overpromise. Protect customer data. Give people a fair path to fix problems.

The legal framework in the U.S. has been built over time, starting with the Federal Trade Commission Act of 1914, then expanding through laws such as the Fair Credit Reporting Act (1970), Fair Debt Collection Practices Act (1977), Telephone Consumer Protection Act (1991), and CAN-SPAM Act (2003), as outlined in this overview of key U.S. consumer protection laws.

Transparency

If a customer has to hunt for fees, subscription terms, auto-renewal language, or delivery conditions, your store has a transparency problem.

In e-commerce, transparency means the customer can see the important terms before they pay. That includes pricing, recurring billing, return conditions, shipping costs, and material limitations. Hidden terms often become disputes over unauthorized charges or cancellation.

If you sell subscriptions, study how the FTC Negative Option Rule affects Shopify merchants. This is one of the fastest ways a legitimate business creates unnecessary chargeback risk.

Accuracy

Your product page is a promise. If the item arrives and the customer thinks the promise was wrong, accuracy becomes a dispute issue.

That includes:

- Images that match the actual product

- Descriptions that match size, color, material, function, and compatibility

- Claims that stay inside what you can support

- Delivery statements that don't imply a timeline you can't control

A lot of Item Not as Described disputes are really accuracy failures with a payment label attached.

Fairness and redress

Fairness is the broad idea behind rules against deceptive or unfair practices. Redress is what happens when something goes wrong. The customer needs a reasonable path to contact you, cancel where appropriate, request a refund when your policy allows it, or resolve a defect.

If support is slow, policies are vague, and checkout copy is aggressive, customers stop negotiating with you and start calling their bank.

Privacy and safety

For a Shopify merchant, privacy isn't abstract. If you collect customer data, you need to say what you're doing and follow through. If you sell sensitive or age-restricted products, your safeguards matter. If you market to families or children, scrutiny increases.

The common thread across all five principles is simple: the customer should understand the transaction, receive what you promised, and have a fair way to fix a problem. When that breaks down, chargebacks follow.

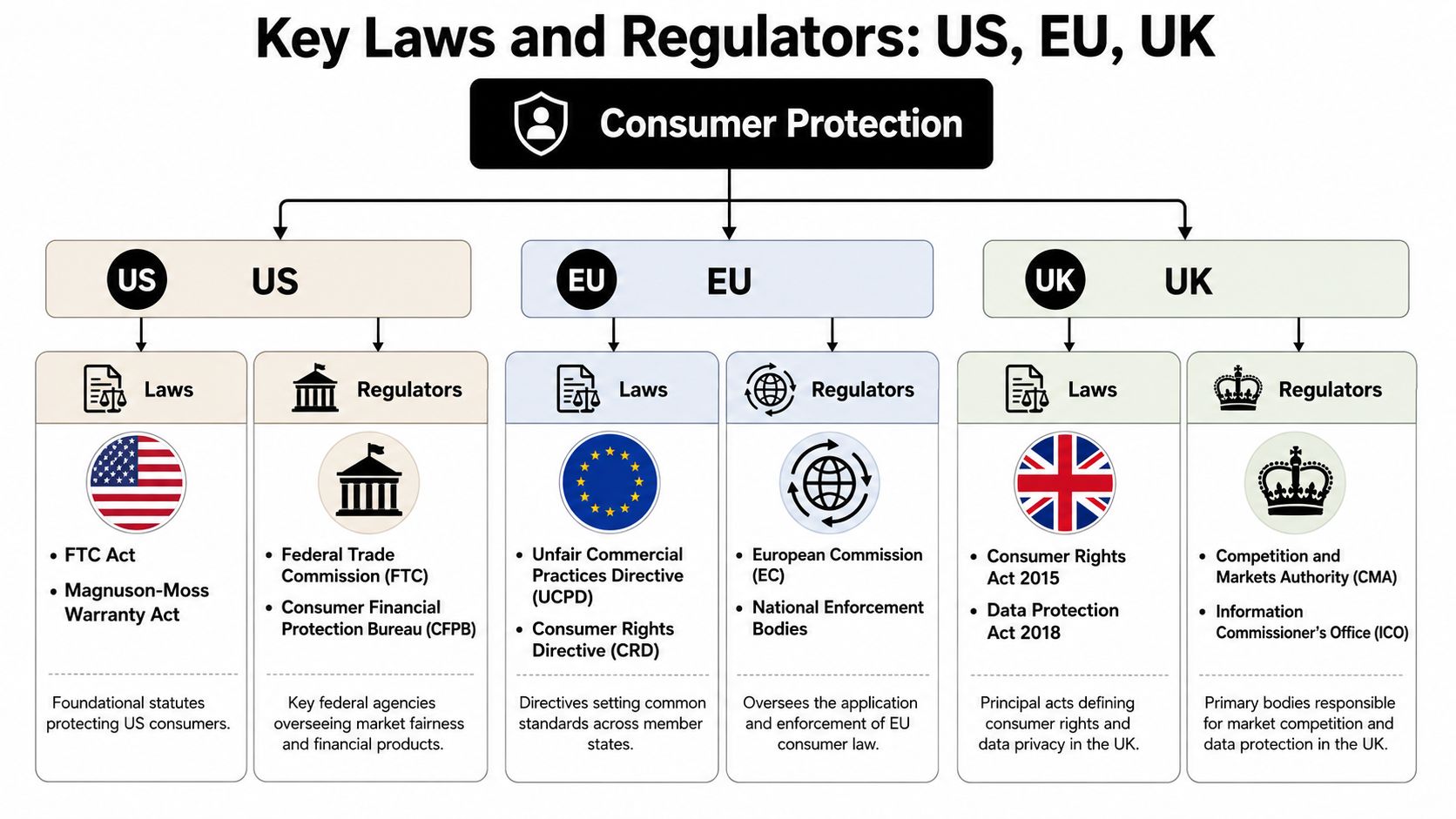

Key Laws and Regulators in the US, EU, and UK

You don't need to become a lawyer for every market you sell into. You do need a working map of who enforces what, and which rules can turn into refunds, chargebacks, or enforcement headaches.

United States

In the U.S., the Federal Trade Commission matters because it polices unfair and deceptive conduct. That isn't narrow. It can touch advertising claims, billing flows, consent, cancellation, privacy promises, and post-purchase practices.

The FTC says it enforces federal competition and consumer protection laws against anticompetitive, deceptive, and unfair practices. The stakes are real. One FTC-cited settlement required Shutterstock to pay $35 million over allegations involving charges without informed consent and making cancellation difficult, according to the FTC's consumer protection enforcement overview.

For merchants, that means this: your checkout flow, renewal disclosures, and cancellation design aren't minor UX choices. They can become evidence of whether you treated customers fairly.

A second layer in the U.S. comes from state law. Virginia's Consumer Data Protection Act is a good example because it doesn't apply to every business by default. It applies when a business either controls or processes personal data of at least 100,000 consumers in a calendar year, or at least 25,000 consumers and derives over 50% of gross revenue from selling personal data, as stated in the full text of Virginia's statute. That tells you something important. Privacy compliance often turns on scale plus monetization, not just product category.

If you want the payment-side view, this guide to chargeback laws merchants should know is worth reading after you map your market exposure.

European Union

The EU takes a more standardized approach across member states through directives. For an online seller, the practical issue is that consumer rights around disclosures, cancellation, and post-purchase remedies are more formalized than many U.S. merchants expect.

That matters when you sell cross-border. A customer who thinks they were entitled to cancel or withdraw may not argue with your support team for long. They may go straight to the issuer, platform, or local enforcement path.

United Kingdom

The UK runs on its own framework, including consumer rights and data protection rules. The key practical takeaway is that your product quality claims, refund handling, delivery promises, and data practices all need to match what UK buyers are shown before they order.

Selling internationally without market-specific terms is how stores create disputes they can't cleanly defend.

What merchants should actually do with this

Use a simple market screen:

| Market | What to check first | Chargeback risk if ignored |

|---|---|---|

| US | Billing disclosures, cancellation path, privacy promises | Unauthorized, cancelled recurring, misleading terms |

| EU | Withdrawal and disclosure requirements, delivery and returns | Services not provided, credit not processed, buyer dissatisfaction |

| UK | Product conformity, refund handling, data disclosures | Not as described, refund disputes, complaint escalation |

The legal map matters because banks, regulators, and customers don't care that your store is “just Shopify.” If you sell into their market, they'll judge the transaction by their rules.

Applying the Rules to Your Online Store

Legal theory translates into page design, app settings, and support workflows.

A compliant Shopify store usually looks boring in the right ways. Product pages are specific. Pricing is obvious. Policies are easy to find. Consent is captured cleanly. Cancellation isn't hidden behind support gymnastics.

Product pages need to do real work

Your product page should answer the questions a skeptical customer would ask after delivery, not just the ones a marketer wants to highlight before purchase.

Focus on these basics:

- Show the actual item with images that match the version shipped

- State product limitations so customers don't fill gaps with assumptions

- List dimensions, materials, compatibility, and variants in the same place the customer buys

- Avoid inflated claims that support can't defend later

If you sell supplements, electronics, cosmetics, or custom goods, this gets even more important. Small ambiguities become big disputes.

Checkout is where stores create preventable trouble

Many chargebacks start with how totals and terms appear in the last step before payment.

Your checkout should make these items obvious:

- Full price before payment. Shipping, taxes, and add-ons should be visible before the final confirmation.

- Recurring terms. If the order renews, customers must see that clearly.

- No pre-checked surprises. Upsells, insurance, warranty extras, or donations should require affirmative action.

- Policy access. Refund, shipping, and cancellation policies should be reachable without friction.

The same rule applies to data practices. The FTC says privacy promises must be honored, security should fit the sensitivity of the data, and the COPPA rule requires parental control over children's data. It also notes that state laws commonly require opt-in consent for sensitive data and give consumers rights to opt out of sale, sharing, or targeted processing. Operationally, that pushes businesses toward data minimization, explicit consent capture, and documented response workflows, as explained in the FTC's privacy and security guidance for businesses.

That's not just privacy law. It's dispute preparation. If a customer says they never agreed, your records need to show what they saw and what they accepted.

Policy pages must help customers before they help lawyers

Most store policies are written to sound formal. That's a mistake.

Write them to reduce tickets and disputes. A strong Shopify refund policy should be readable, visible, and consistent with what support does. If your support team routinely makes exceptions that your policy doesn't mention, your documentation will look unreliable in a dispute.

A policy buried in the footer and contradicted by support email isn't a defense. It's conflicting evidence.

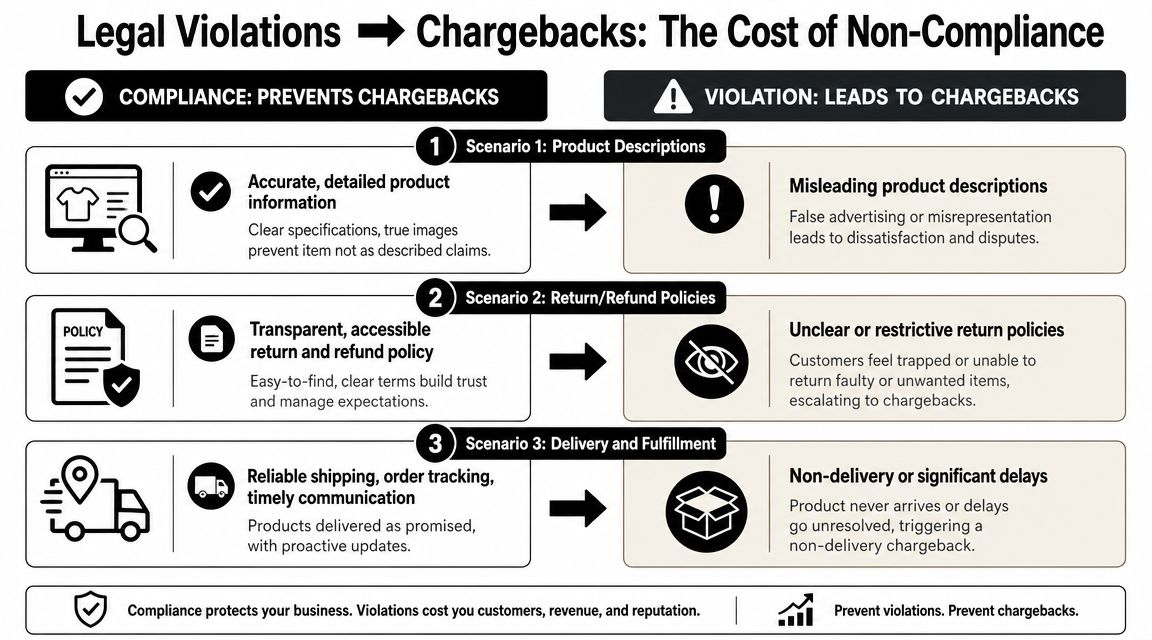

How Legal Violations Turn into Chargebacks

Most merchants treat legal compliance and chargeback management as separate problems. They aren't. The same mistake that creates customer frustration often becomes the dispute reason code.

The under-covered issue is the overlap. Broad public explainers talk about consumer rights in the abstract, but merchants need to know when a complaint turns into a refund request, a chargeback, or a fraud claim. That distinction matters because consumer protection rules in the U.S. are layered across federal and state law, and many disputes get resolved through agencies or payment networks rather than court, as explained in Cornell's overview of consumer protection laws and dispute pathways.

Case one with product descriptions

A merchant sells a jacket. The photos are heavily edited. The product page says “premium winter protection” but doesn't clarify shell thickness, insulation type, or fit. The customer receives it, thinks it's lighter than expected, and files Item Not as Described.

From the merchant's side, the jacket shipped correctly. From the bank's side, the evidence depends on what the customer was told. If the page was vague, your defense is weak.

The legal principle behind this dispute is straightforward: don't mislead buyers about what they're purchasing. In representment, that means you need:

- The exact product page shown at purchase

- Variant-specific details

- Order confirmation matching the item shipped

- Delivery proof

- Any customer acknowledgment of specs or fit guidance

Case two with subscriptions and cancellations

A customer buys a monthly product box. The renewal terms are somewhere in the footer. Cancellation requires emailing support, waiting for a reply, and following steps that aren't explained clearly. The customer gets billed again, gets angry, and disputes the charge as a cancelled recurring transaction or a service they didn't agree to continue.

That's not only a customer service failure. It's a consumer protection problem tied to consent and cancellation. If the renewal terms were not prominent and the cancellation path was unnecessarily hard, the customer's narrative gets stronger.

Here's a short explainer that frames the merchant side well:

If you sell regulated or higher-scrutiny products, the operational risk expands further. This guide on Protecting your high-risk regulated eCommerce business is useful because restricted shipping, compliance gaps, and customer misunderstandings often collide in the same dispute file.

Case three with checkout manipulation

A customer adds a product to cart. At checkout, an upsell or extra fee is included through a pre-selected option. They don't notice it, complete the purchase, then dispute the amount because the final charge exceeded what they thought they agreed to.

This type of case is brutal to defend if your checkout logs don't show clear affirmative consent. A pre-checked box might raise conversion in the short term, but it can poison your evidence later.

Banks don't care that the extra box was technically visible. They care whether the customer clearly agreed to the final amount.

The pattern merchants should recognize

These examples look different, but they follow the same chain:

| Store mistake | Customer reaction | Chargeback outcome |

|---|---|---|

| Vague or inflated product claim | “This isn't what I ordered” | Item not as described |

| Hard-to-find cancellation path | “I cancelled or never agreed to renew” | Cancelled recurring or services not provided |

| Unchecked pricing clarity | “I was charged more than I agreed to pay” | Incorrect amount or unauthorized framing |

If you fix the original transaction design, you prevent many of these disputes before they ever reach the issuer.

Your Shopify Store Compliance Checklist

Use this as an actual audit. Open your storefront in a private browser, go from landing page to checkout, and review what a first-time buyer sees. If something is unclear to you, it's already a risk.

Product pages

- Match images to shipped reality. Don't use visuals that create a stronger impression than the item can support.

- Spell out specs. Size, material, dimensions, compatibility, scent, shade, and included accessories should be explicit.

- State limits clearly. If a product has usage restrictions, lead times, or exclusions, put them near the buy box.

- Keep variant details attached. If blue and black versions differ, the customer should see that before purchase.

Pricing and checkout

- Display the full cost upfront. Taxes, shipping, surcharges, and optional extras must appear before payment.

- Remove pre-checked add-ons. If a buyer chooses gift wrap, shipping protection, or a warranty, make them actively choose it.

- Make subscription terms obvious. Billing frequency, renewal timing, and cancellation steps should be unmissable.

- Capture consent records. Save what the buyer saw and accepted at checkout.

Policies and support

Your key policies should be visible in the footer, linked where relevant, and written in plain English.

Check these one by one:

- Refund policy. Does it say who pays return shipping, what items are excluded, and how long processing takes?

- Shipping policy. Does it separate handling time from carrier transit time?

- Cancellation policy. Can a customer understand exactly how to stop a recurring order?

- Privacy policy. Does it reflect what your apps and workflows do?

If you use AI or chat tools in sensitive workflows, read practical guidance on safely using ChatGPT in healthcare. Even if you're not in healthcare, the consent and data-handling mindset is useful when customer support touches regulated or sensitive information.

Post-purchase records

Often, many stores fall apart in disputes. They sold correctly but documented poorly.

Keep a clean record of:

- Order confirmation emails

- Tracking updates

- Delivery confirmation

- Customer support conversations

- Refund or cancellation actions

- Any replacement or resolution offered

Clean records win arguments faster than passionate explanations.

If your team can't assemble those documents quickly, your compliance problem is already a chargeback problem.

Turn Compliance into Your Best Chargeback Defense

You should stop thinking about compliance as overhead.

For a Shopify merchant, compliance is revenue protection. It reduces confusion, lowers avoidable disputes, and gives you stronger evidence when a customer still files a chargeback. That's the essential business case. Better disclosures. Better consent. Better records. Better outcomes.

There's another reason to take this seriously. Consumer protection laws don't only operate as tools for refunds or straightforward customer complaints. The Institute for Legal Reform argues that these laws can also be used as business-to-business pressure points and policy tools, including debates over whether specific consumer harm must be shown. Their analysis on the misuse of consumer protection laws to pursue policy agendas is useful because it frames enforcement as a dispute environment, not just a customer rights issue.

That matters for merchants. Even when you believe a complaint is weak, the pressure, cost, and settlement dynamics are real. Strong compliance records improve your options. Weak records force you into defensive refunds.

When a dispute does happen, your response has to connect the customer journey to the evidence. That's what chargeback representment is really about. Not generic rebuttals. A documented story showing the customer saw the terms, accepted them, received what was promised, and had a fair path to resolve the issue.

Build your store so that every lawful, honest transaction also becomes easy to defend. That's how smart merchants treat consumer protection laws. Not as a legal burden, but as a practical system for keeping more of their revenue.

Stop losing revenue to preventable disputes. ChargePay helps Shopify merchants turn strong transaction records into recovered money with a 92.4% win rate, 200K+ cases handled, and $10.8M+ recovered. It has a 4.9-star rating on the Shopify App Store, carries the Built for Shopify badge, and uses a pay-per-win model, so you only pay when money is recovered. Install ChargePay from the Shopify App Store and put your compliance evidence to work.

.svg)

.svg)

.svg)

.svg)