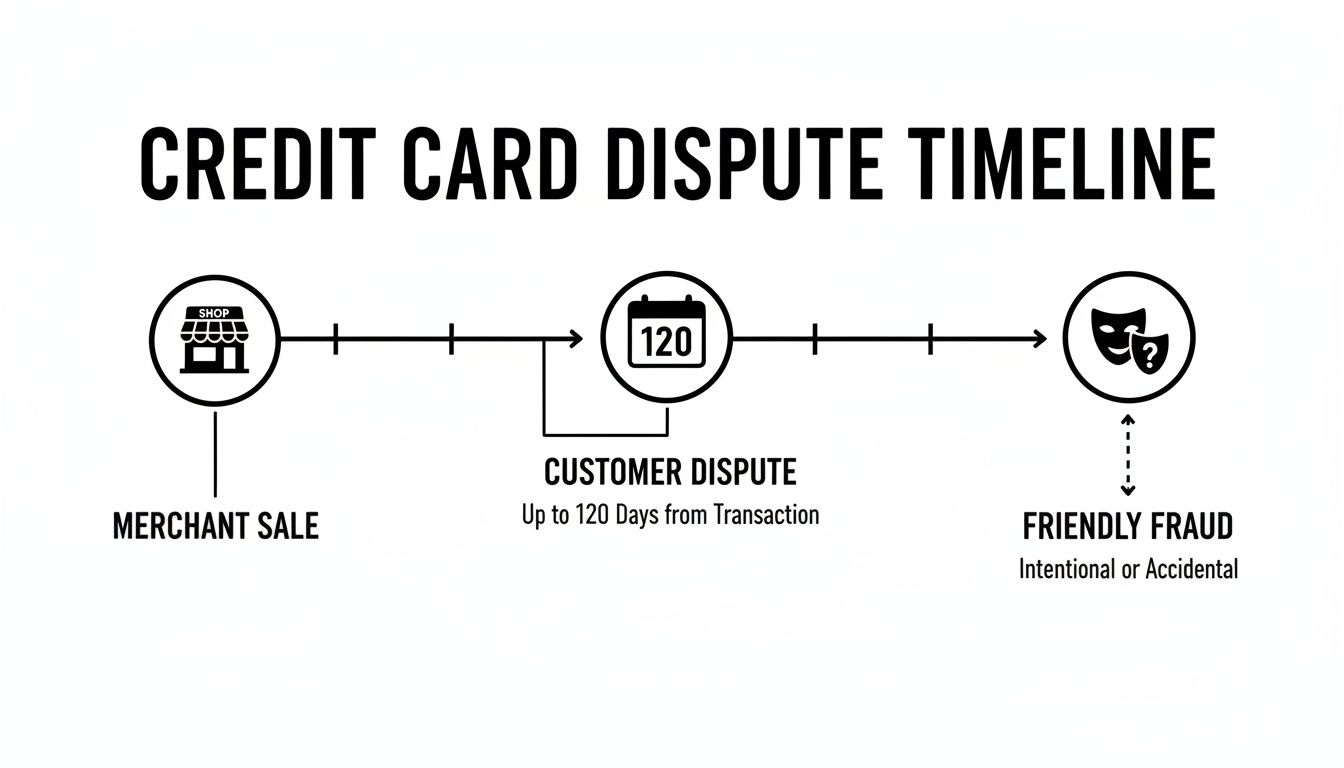

When a customer disputes a charge, it's easy to think there's just one deadline. In reality, the credit card dispute time limit isn't a single clock—it's two completely different ones. For the person who made the purchase, the window to file a dispute is wide open, often for as long as 120 days. But for you, the merchant, the clock starts ticking furiously, giving you a tiny fraction of that time to respond and defend the sale.

The Two Clocks of a Credit Card Dispute

Picture this: you're running your Shopify store, an order comes through, you ship it out, and you mentally mark the sale as complete. But then, months down the road, a chargeback notice materializes out of nowhere, yanking that revenue straight out of your bank account.

This is a classic scenario where merchants get trapped between two wildly different timelines. It’s a setup that puts your bottom line at a serious disadvantage.

On one side, you have the customer's clock. It ticks along slowly, giving them all the time in the world. On the other side is the merchant's clock—a frantic countdown timer that demands your immediate attention.

The Customer's Generous Timeline

Card networks are built to protect consumers, and that means giving them plenty of runway to reconsider a purchase or flag an issue. Think about it: a customer could buy a seasonal product, use it for its intended purpose, and then two months later, decide they don't want it anymore. In many cases, they can still file a dispute, leaving you to deal with the fallout long after you've forgotten the transaction.

This long window is just a fact of life for e-commerce merchants. Major players like Visa and Mastercard set a standard 120-day time limit for most consumer disputes. This gives buyers more than enough time to change their minds, whether it’s due to simple buyer's remorse, a delivery issue, or even friendly fraud—which, by the way, is behind a shocking 75% of all chargebacks. Getting a handle on these timelines is your first step to building a solid defense, as experts break down in analyses on chargeback time limits.

The Merchant's High-Pressure Deadline

While your customer had months to kick off the dispute, you get a sliver of that time to fight back. Once a chargeback is filed, your window to scramble for evidence—like order details, shipping confirmations, and any customer emails—and build a convincing response is painfully short.

This mismatch in timing creates the perfect storm for lost revenue, especially from friendly fraud. You can learn more about the initial steps of this process by understanding the differences between retrieval requests vs chargebacks.

The core challenge for any merchant is managing this asymmetry. The system gives cardholders a four-month grace period to change their minds, but it often gives you just a few weeks to prove your case. Without a plan, you're set up to fail.

Comparing Dispute Timelines for Merchants and Customers

When it comes to the credit card dispute time limit, not all clocks are created equal. The system essentially creates two completely different timelines—a long, generous one for the customer and a much faster, more demanding one for the merchant.

For a cardholder, the window to file a dispute can stretch for months. This gives them plenty of time to spot a problem, have second thoughts about a purchase, or even commit friendly fraud. But for you, the merchant, the moment that dispute notification arrives, it’s a frantic race against the clock.

The Widening Gap Between Buyer and Seller

Think of it like a relay race where your customer gets a massive head start. They can take their sweet time deciding whether to even begin running, but once they hand off that baton (by filing the dispute), you have to sprint to the finish line with a mountain of evidence.

This fundamental imbalance puts you at a significant disadvantage from the very beginning.

This timeline below really brings the journey to life, showing how a simple sale can turn into a dispute months down the road, highlighting just how long a customer can wait before taking action.

The key takeaway is simple: the long customer dispute window directly opens the door to friendly fraud, where legitimate transactions are disputed long after the fact.

Consumer vs Merchant Dispute Timelines: A Quick Comparison

To truly grasp the pressure you're under, let's put some numbers to it.

The moment a chargeback hits your account, the clock starts ticking—and it ticks fast. You generally have just 20 to 45 days to build your case and respond, depending on the card network. For example, you get 30 days for Visa, 45 days for Mastercard, and a mere 20 days for American Express. If the dispute gets escalated, that window can shrink to just 7-10 days.

Now, compare that to the customer's timeline, which often extends to 120 days and can even go up to 540 days for certain Visa reason codes. It’s a classic case of asymmetry, and it’s a merchant’s nightmare.

This table breaks down that stark contrast, showing just how little time you have to act compared to your customer.

As you can see, the difference is dramatic. While a customer has months, you have mere weeks—sometimes less—to gather compelling evidence and submit a winning response. Miss that short deadline, and it’s an automatic loss. No questions asked.

To dive deeper into the full chargeback lifecycle, check out our guide on how long chargebacks take to resolve. This is why having a system ready to go isn't just helpful; it’s essential for survival.

How Card Network Rules Change the Deadlines

That "120-day rule" you hear about? It's a great starting point, but it's far from the whole story. The real credit card dispute time limit is more like a maze than a straight line, with rules that shift depending on the card network—Visa, Mastercard, American Express, or Discover—and the specific reason for the chargeback.

Thinking every dispute follows the same clock is a costly mistake. Each network has its own playbook, and you have to know the differences to protect your revenue. One network might give you 45 days to respond, while another gives you just 20. Those details matter. A lot.

This isn't just about small print; the rules can dramatically change how long a customer has to file a dispute and how you must respond. A simple "product not as described" claim has a different timeline than a "non-delivery of services" claim, and each network treats them uniquely.

Visa and Mastercard Nuances

Visa and Mastercard might be the two biggest players, but they don’t operate identically. While both often start with a 120-day baseline for the consumer, the exceptions are where merchants really get into trouble.

For instance, Visa’s rules can be surprisingly flexible for the cardholder. For certain issues, like goods or services promised for a future date (think a pre-ordered product or tickets to an event months away), the dispute clock doesn’t even start ticking until that expected date passes. In some cases, like non-delivery, the time limit can stretch up to a staggering 540 days from the original transaction.

Mastercard, on the other hand, often ties its deadlines to the "central site business date," which can add another layer of complexity if you're not familiar with it. They do, however, give merchants a slightly more generous 45-day window to respond to initial disputes, which is a small but helpful buffer compared to some others.

The key takeaway here is that the 120-day figure is just a guideline. The real deadline is dictated by the specific reason code and the card network's unique rulebook, which can stretch into hundreds of days for certain situations.

American Express and Discover Differences

American Express and Discover operate with their own sets of rules that can be even more distinct. AmEx is famous for its strong cardholder-first stance, and their dispute timelines often reflect that. They don't have a hard-and-fast limit for consumers to file a dispute, often leaving it up to issuer discretion. For merchants, though, the window is tight: just 20 days to respond.

Discover also generally sticks to a 120-day consumer window but provides a similarly short 20-day merchant response time. These shorter deadlines from AmEx and Discover mean you need to be even more prepared and act immediately when a dispute notice comes through.

To make things even more complicated, international sales bring entirely new rules into play. Europe’s Consumer Rights Directive, for example, can add 14 days post-delivery to the clock, pushing some timelines beyond 500 days and catching unsuspecting Shopify sellers in cross-border chaos. If you want to get a better handle on these intricate rules, you can find a detailed breakdown of how Visa calculates its specific time limits.

These variations create a challenging situation where what works for one dispute might not work for another. To learn more about this, discover insights about the complex web of chargeback rules at Chargebacks911.

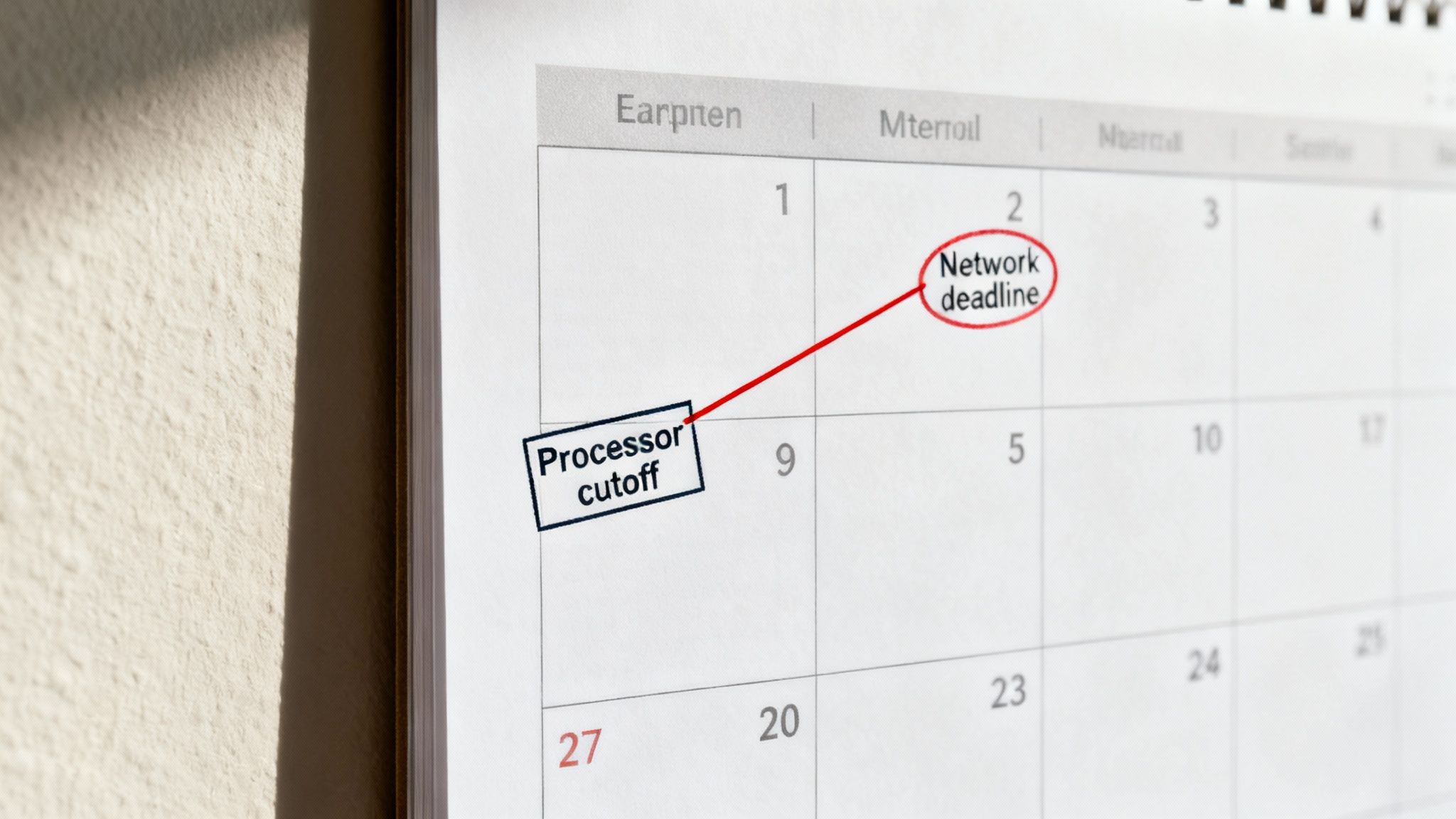

Why Your Payment Processor Gives You Less Time

If you’ve ever gotten a dispute notification from Stripe or PayPal, you’ve probably noticed something strange. The deadline they give you to respond feels incredibly tight—often way shorter than the official 30 or 45 days the card networks allow. This isn’t an error. It’s a very intentional—and necessary—buffer.

Think of your payment processor like a project manager rushing to meet a hard deadline. Their job is to take all your evidence, make sure it’s packaged perfectly according to the card network’s strict rulebook, and get it submitted before the clock runs out. To pull this off without any last-minute disasters, they build in their own internal deadline for you.

This buffer zone is their safety net. It gives them the breathing room they need to review your documents, ask for more information if something’s missing, and format everything just right. If they waited until the final day, one tiny hiccup could make them miss the official cutoff, and you’d lose the dispute automatically.

The Processor's Role as a Gatekeeper

Your payment processor is the critical go-between, connecting you to the ridiculously complex world of card networks. They’re on the hook for making sure every shred of evidence you submit meets the exact specifications for Visa, Mastercard, or whoever is involved.

This administrative cushion protects both you and them. Here’s a peek at what’s happening behind the scenes during that buffer period:

- Evidence Review: They’re checking to see if your proof—like shipping labels or customer emails—is actually clear, relevant, and compelling.

- Formatting and Submission: They take your documents and reformat them into the standardized package the network demands. It’s not just a simple upload.

- Error Correction: If there’s a problem with what you sent, this window gives them a chance to circle back with you for corrections before it’s too late.

The deadline you see in your dashboard is your deadline, not the bank’s. Missing it means your processor won't have the time to properly assemble and submit your case, guaranteeing a lost dispute before it even begins.

Understanding this is absolutely essential. When a dispute lands in your lap, you have to move fast. That clock you see is ticking down much quicker than the official one, making an immediate response your single best defense. To get a better handle on the financial tech that shapes these processes, it's worth exploring the top payment gateways for ecommerce.

For a deeper dive into their role, you can learn more about what a payment processor does and see exactly where they fit into the whole dispute ecosystem.

How Automation Helps You Beat the Clock

Trying to manage the short credit card dispute time limit by hand is a surefire recipe for lost revenue. It’s a stressful, high-stakes game of beat-the-clock that pulls you away from what you do best—actually running your business. This is exactly where automation tools come in and completely change the game.

Instead of a frantic, manual scramble to find order details, customer emails, and shipping proof, an automated system does all the heavy lifting for you. It acts like a digital detective, gathering every single piece of relevant evidence in seconds, not days. This kind of speed is absolutely critical when you’re staring down a tight 7- to 10-day deadline for escalated disputes.

Manually fighting chargebacks is like trying to put out a fire with a squirt gun. Automation gives you a fire hose, instantly assembling tailored, compelling evidence packages that give you a real fighting chance to win back your money.

With a system like ChargePay, the entire defense process becomes hands-free. You no longer have to worry about missing a deadline because you were tied up with a product launch or a customer service issue. The technology just takes over, ensuring every single response is submitted on time, every time.

Smarter Responses, Higher Win Rates

Automation does a lot more than just meet deadlines; it builds smarter, stronger cases. AI-powered tools analyze the dispute's reason code and the card network's specific rules to generate an evidence package perfectly tailored to the situation. This is a level of precision that’s nearly impossible to hit manually, especially when you're juggling multiple disputes at once.

A system built for this understands the subtle differences between a Visa "merchandise not received" claim and a Mastercard "product not as described" dispute. It knows exactly what kind of proof the bank needs to see and presents it in the exact format they require.

Here’s how it transforms your workflow:

- Instant Evidence Gathering: The system automatically pulls transaction data, shipping confirmations, delivery proof, and even customer interaction history from all your different platforms.

- AI-Powered Rebuttals: It generates clear, concise rebuttal letters that directly address the specific claims made in the dispute, leaving no room for ambiguity.

- Optimized Submissions: The final evidence package is formatted and submitted according to each card network’s unique requirements, maximizing your chances of a successful representment.

By taking human error and emotional stress out of the equation, automation ensures your responses are not just timely but also strategic. Businesses using these tools often see their win rates jump significantly, recovering revenue that was previously written off as a loss. For more on this, you can learn about the benefits in this complete guide to automated chargeback and dispute management using AI.

Ultimately, automation gives you back your most valuable asset: your time. You can stop chasing paperwork and get back to growing your business, confident that your revenue is protected around the clock.

Getting a Grip on Your Dispute Timelines

Navigating credit card dispute time limits can feel like you're playing a game rigged against you. Your customer gets a pretty generous window to file a claim—often 120 days or even more. But on your end? You’re left scrambling to meet a deadline that can be as short as 20 to 45 days.

This lopsided timeline is the core challenge every merchant has to deal with. The long window for the consumer means there's plenty of time for something to go wrong, while your tiny response window demands you act perfectly, and immediately. If you miss that deadline, it's an automatic loss. The dispute is closed, and so is your claim to that revenue.

It might seem unfair, but you’re not powerless. The first step to taking back control is simply understanding these timelines. Once you know the specific rules for Visa, Mastercard, and American Express—and realize that your payment processor probably gives you even less time—you can start building a proactive defense instead of just reacting to bad news.

Shifting from Defense to Offense

The real key is to stop chasing paperwork by hand and start using tools that do the heavy lifting for you. It all boils down to a few core principles:

- Act Immediately: The second you get a dispute notification, treat it like it’s urgent. That clock is ticking down way faster than you think.

- Know the Rules: Don't just assume every dispute is the same. The evidence you need for a Visa claim might be totally different from what Amex requires.

- Embrace Automation: This is your most powerful strategy. AI-powered tools completely remove the stress of manual evidence gathering and make sure you never blow a critical deadline.

When you turn a chaotic, manual process into a smooth, automated workflow, you stop playing catch-up. You start winning back revenue and, just as importantly, you get your time back to focus on actually growing your business.

Beyond the direct credit card dispute process, understanding how to manage other financial challenges is key to controlling your dispute timelines, including the process for successfully navigating and lifting account restrictions from bounced checks.

Got Questions? We've Got Answers

Navigating the web of timelines and network rules can feel tricky. Let's clear up some of the most common questions merchants have about credit card dispute time limits.

Can A Customer Dispute A Charge After 120 Days?

Absolutely, and this is a critical point that catches a lot of merchants off guard. While 120 days feels like the standard you hear about, card networks carve out plenty of exceptions for specific situations.

Think about it this way: if a customer pre-ordered a product, the clock on their dispute window might not even start ticking until after the expected delivery date has passed, not when they first paid. For certain reason codes, like merchandise not being delivered, Visa’s time limit can stretch out to a whopping 540 days. This is exactly why holding onto detailed sales records for well over a year isn't just good practice—it's essential.

What Happens If I Miss The Merchant Response Deadline?

If you miss your deadline to respond, you automatically lose the dispute. Period. There are no extensions, no do-overs, and no second chances.

The funds are permanently handed back to the cardholder, and to add insult to injury, your payment processor will still hit you with a separate chargeback fee. This is the harsh reality of the merchant's short response window. Missing it means you’ve forfeited your revenue without ever getting the chance to tell your side of the story. It really drives home why you have to act the moment a dispute lands.

The moment a chargeback notice arrives, the clock is your biggest enemy. Missing that tight response deadline is an automatic, non-negotiable loss of both the sale amount and the chargeback fee.

How Does Automation Handle Different Time Limits?

This is where automation really shines. A good system is programmed with the specific rulebook for each card network and every reason code out there. When a dispute comes in, the software instantly knows if it's a Visa, Mastercard, or Amex claim and gets to work.

It automatically tailors the response to meet that network's unique deadlines and evidence requirements, completely removing the human error and guesswork from the equation. You no longer have to manually track dozens of different timelines. It just ensures every single response is built correctly and submitted on time, maximizing your odds of winning.

Stop losing revenue to missed deadlines. ChargePay uses AI to automate the entire dispute process, ensuring every response is timely, accurate, and optimized to win. Protect your business and recover your money today.

.svg)

.svg)

.svg)

.svg)