Another dispute just hit your inbox. The order looked normal when it came in. The product shipped. Then the bank sided with the cardholder, and now you're out the revenue, the product, and the time it takes to fight it.

That cycle feels random when you're in it. It isn't. Most Shopify stores have patterns in the orders they lose, the evidence they fail to collect, and the disputes they could have prevented if they'd looked at fraud risk before the package went out the door.

Big-company fraud advice usually misses that reality. It talks about enterprise controls and broad governance. You need something simpler. You need to know which orders deserve scrutiny, which signals matter, and how that work lowers chargeback losses. A fraud risk assessment is just that. It's a practical way to turn your order data into decisions you can use.

Why Your Store Needs a Fraud Risk Assessment

A lot of merchants treat chargebacks like weather. Annoying, expensive, unavoidable. That mindset keeps stores stuck in reactive mode.

Fraud isn't a niche issue. The Association of Certified Fraud Examiners has long estimated that organizations lose about 5% of annual revenue to fraud, and one practical example in fraud-management guidance is that a business with $10 million in revenue could face roughly $500,000 in potential annual fraud losses if risks aren't identified and controlled, as summarized in Optro's overview of fraud risk assessment. For a Shopify store, that won't all show up as one dramatic event. It usually shows up as a steady drip of chargebacks, refunds, reshipments, and bad orders that should have been stopped earlier.

Broad fraud advice misses the merchant problem

Most fraud risk assessments are too broad for e-commerce. Guidance often focuses on internal controls and enterprise schemes, but it misses the specific risks of payment disputes by channel, product, and customer behavior. A key question for a Shopify merchant isn't just whether fraud exists. It's which disputes you're most likely to lose, and what evidence changes the outcome, as noted in Grant Thornton's guidance on strengthening fraud risk assessments.

That's why a useful fraud risk assessment for your store has to be tied to orders, not theory.

Practical rule: If your assessment doesn't help you decide whether to approve, review, cancel, refund, or fight a dispute, it's too abstract to help your store.

It changes how you react to chargebacks

When merchants say, “We get a lot of chargebacks,” they're usually describing three different problems at once:

- Bad orders getting approved: Fraud slips through because nobody connected the warning signs.

- Good orders getting weak documentation: The customer received the item, but the store can't prove enough when a dispute arrives.

- Friendly fraud getting treated like criminal fraud: The order was legitimate, but the representment package doesn't tell a clear story.

A fraud risk assessment helps separate those issues. That matters because the fix for each one is different.

If chargebacks are already hitting margins, it's worth understanding whether chargebacks hurt businesses beyond the obvious lost sale. The short answer is yes. They affect cash flow, operations, and your ability to scale cleanly.

Start by Defining Goals and Mapping Your Data

A weak fraud risk assessment usually starts with a vague goal. “Reduce fraud” sounds fine, but it won't help you build rules or review orders. You need a goal tied to a specific business problem.

A better goal sounds like this: reduce disputes on first-time customer orders for higher-priced products, or improve evidence collection for orders that tend to turn into “product not received” claims. The point is focus. If you try to assess everything at once, you'll end up with a spreadsheet nobody uses.

Pick a goal your team can act on

Before you map signals, decide what decision the assessment should improve.

Some useful examples for Shopify merchants:

- Order approval quality: Stop obviously risky orders before fulfillment.

- Manual review quality: Give your team a clear reason to hold, verify, or cancel.

- Dispute readiness: Capture stronger evidence at checkout and post-purchase.

- Channel-specific control: Separate risk by traffic source, product line, or fulfillment method.

A rigorous fraud risk assessment is typically executed in four stages: risk identification, risk and control analysis, residual risk evaluation, and risk treatment. This early work fits the risk identification stage, where you map where and how criminals could exploit your processes, according to ACAMS' fraud risk assessment guide.

Map the data you already have

Most merchants already have enough data to start. They just haven't organized it in a way that supports decisions.

Use your Shopify admin, payment processor, fraud tools, and support history to pull together signals like these:

- Order basics: product, cart value, SKU mix, discount usage, shipping speed, and fulfillment timing

- Customer history: first-time or repeat buyer, prior refunds, prior disputes, account age, and email pattern

- Payment checks: AVS result, CVV result, payment method, and any gateway risk flags

- Delivery details: billing and shipping match, freight forwarder use, pickup requests, or address changes after purchase

- Behavioral clues: multiple orders close together, unusual checkout timing, mismatch between customer profile and order pattern

- Support records: delivery complaints, cancellation requests, “item not received” language, or refund pressure before a dispute

The stores that do this well don't collect more data than everyone else. They connect the data to a real decision.

If you're not already watching these signals continuously, transaction monitoring for e-commerce payments becomes useful. It helps you catch patterns across orders instead of reviewing each dispute in isolation.

Keep the first version small

Don't build a huge model on day one. Start with one product category, one payment method, or one recurring dispute type. If your store sells supplements, electronics, apparel, and subscriptions, you may find that each category produces a different fraud pattern. One blanket rule set won't fit them all.

A narrow first pass is easier to test, easier to explain, and much more likely to survive contact with actual conditions.

Build a Simple Risk Scoring Model

You don't need a complicated algorithm to run a useful fraud risk assessment. For most Shopify stores, a simple points model is enough to improve approval decisions fast.

The mistake I see most often is merchants using isolated red flags. One failed AVS check doesn't always mean fraud. One high-value order doesn't either. The signal gets stronger when you combine them into a believable story about how the order happened.

Academic research summarized by the American Accounting Association found that a story-based approach produced fraud risk assessments closer to expert judgment than a checklist alone. The study also noted that reading a fraud story caused the greatest change in the knowledge structures of novice auditors, showing why realistic scheme thinking works better than box-ticking, as discussed in the American Accounting Association summary of the story-based approach.

Score combinations, not isolated alerts

Think in patterns:

- A first-time customer buying an expensive item isn't automatically risky.

- A first-time customer buying an expensive item, with a billing and shipping mismatch, rush delivery, and poor verification results is a different story.

- A repeat customer with clean history, matching details, and normal purchase behavior deserves a very different path.

That's what your scoring model should capture.

Sample e-commerce risk scoring rules

Use a points system that reflects your store's experience. Higher points mean more review pressure.

| Risk Indicator | Description | Sample Score |

|---|---|---|

| Billing and shipping mismatch | Order details don't line up in a way your store often sees in bad disputes | 15 |

| Failed AVS or weak address verification | Payment data doesn't support the billing details strongly | 20 |

| Failed CVV or unavailable CVV result | Card verification is missing or weak | 15 |

| First-time customer with high-value order | No prior buying history and unusually expensive basket | 20 |

| Expedited shipping on risky basket | Rush fulfillment on an order with other warning signs | 10 |

| Multiple orders from the same customer in a short period | Behavior suggests testing or burst activity | 15 |

| Shipping address changed after purchase | Post-checkout changes increase delivery and dispute risk | 15 |

| Freight forwarder or pickup mismatch | Delivery setup reduces confidence in who receives the item | 10 |

| Repeat customer with clean order history | Positive signal that reduces overall concern | -15 |

| Strong verification signals across payment and address data | Multiple checks support legitimacy | -20 |

The exact scores don't matter as much as consistency. Start with a small set of rules you can explain to someone else on your team.

Decide what each score means

Your model needs a workflow behind it or it becomes decoration.

A simple setup might look like this:

- Low score: approve and fulfill normally

- Middle score: route to manual review

- High score: cancel or refund before shipment

If you're reviewing payment verification data, how AVS works in chargeback prevention is worth understanding because AVS results often matter both before fulfillment and later in dispute evidence.

What works: a modest scorecard your ops team actually follows.

What doesn't: a giant rules sheet nobody trusts, so staff override it whenever they feel pressure to ship.

Keep room for merchant judgment

A score isn't a verdict. It's a way to standardize attention.

If your team knows a particular product line attracts reseller abuse, that may matter more than a generic signal from an app. If you sell digital goods, shipping logic may matter less than account history and usage behavior. If you sell custom items, post-purchase support patterns may predict disputes better than checkout data alone.

The model should reflect your store's reality. Not someone else's template.

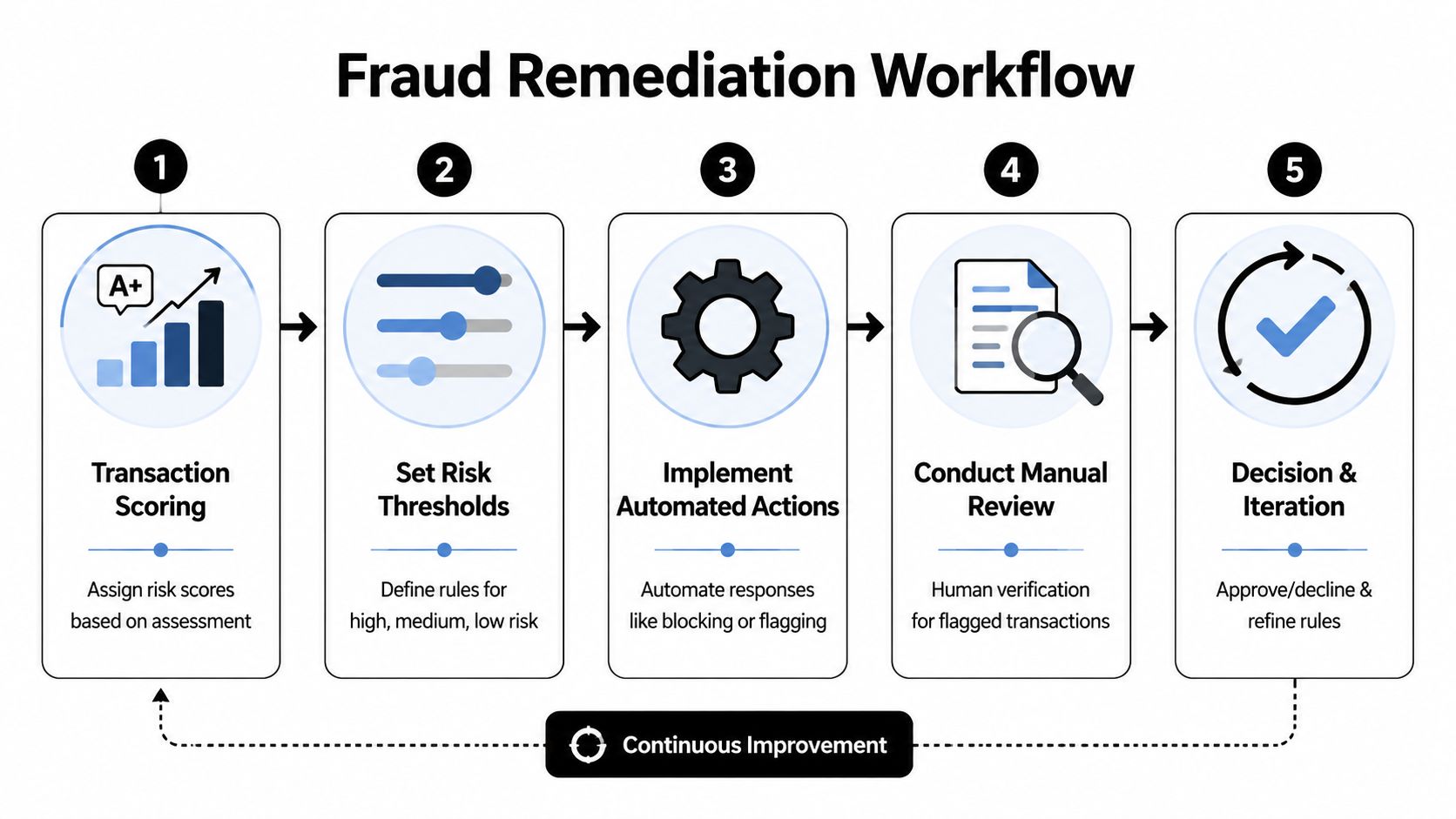

Prioritize Remediation and Implement Controls

A fraud risk assessment only matters if it changes what happens next. Once you've scored an order, you need a control that matches the risk.

That's also the standard regulators expect in more formal settings. The OCC says management should use the results of its fraud risk assessment to design the risk management system, which means the output should drive real controls such as blocks, reviews, and testing, as explained in the OCC's bulletin on fraud risk management principles.

Match each risk band to one action

Most stores need three paths.

Accept low-risk orders

Don't slow down good customers. If the order looks consistent with normal buying behavior and your verification signals are clean, ship it.Review medium-risk orders

Money is usually won or lost with these orders. Manual review should focus on confirming identity, delivery intent, and whether the order behavior makes sense.Block or refund high-risk orders

If the order tells a bad story, don't ship and hope for the best. Canceling a clearly risky transaction is often cheaper than eating a later chargeback.

Make manual review specific

Manual review fails when it turns into “stare at the order and guess.”

Use a short checklist with targeted actions:

- Verify contactability: Call or email and see whether the customer responds in a normal way.

- Check consistency: Compare name, address, phone, email, and order details for obvious mismatch.

- Review order context: Ask whether the purchase matches the store's usual buying pattern.

- Check delivery risk: Look for rerouting, forwarding, pickup complexity, or unusual urgency.

- Document the review: Save notes in a way your support and dispute teams can use later.

A medium-risk queue should reduce uncertainty. If it only delays shipping without improving your decision, it's wasting labor.

There's a policy angle here too. If your internal processes around approvals, exceptions, and expense-related edge cases are messy, it helps to download ReceiptGen's policy template and adapt the structure for your store's fraud review rules. The point isn't expense policy itself. It's having a written standard your team can follow when pressure hits.

Fix the most expensive weakness first

Don't try to tighten every control at once. If most of your painful disputes come from one channel, one product category, or one shipping pattern, start there.

I'd rather see a merchant build one strong review flow for risky first-time orders than create ten weak controls that nobody consistently applies.

Use Your Risk Assessment to Win Chargebacks

A chargeback hits your Shopify dashboard two weeks after delivery. The order looked normal when it came in, the package was delivered on time, and support never heard a complaint. If your team has to rebuild the story from scattered notes, you're already behind.

Your fraud risk assessment should do more than approve or reject orders. It should leave a usable record of why you accepted the transaction, what checks were completed, and what happened after checkout. That record is often the difference between a weak response and a credible representment case.

A risk record becomes evidence

Friendly fraud is where this matters most. The cardholder may have placed the order, received it, and still disputed the charge. In that case, the bank needs to see that the purchase was consistent with normal customer behavior and that your store followed a reasonable review process before fulfillment.

A useful record usually shows:

- billing and shipping details matched

- verification checks supported the order

- device, email, or purchase behavior fit the transaction context

- no warning sign was strong enough to justify cancellation

- fulfillment and delivery happened as expected

That gives you a decision trail, not a pile of disconnected screenshots. For Shopify merchants, that matters because you rarely have enterprise fraud teams or custom case systems. You need evidence you can pull from the tools you already use and turn into a clear chargeback representment process for Shopify merchants.

Good dispute evidence shows what you knew at the time, what you checked, and why the order was approved.

That same discipline shows up in stronger payment operations more broadly. Bridge Global's payment intelligence for finance is a useful example of how transaction context can support decisions after the payment itself.

Capture context before the dispute arrives

A lot of chargebacks are lost for a simple reason. The merchant starts collecting proof only after the dispute notice comes in.

By then, key context is gone or harder to prove. Support notes are incomplete. Verification results were never saved. The team remembers why the order looked safe, but memory does not win disputes.

Store these details as part of the original review and fulfillment flow:

- checkout verification results

- customer communication history

- fulfillment, tracking, and delivery records

- timestamps for order review and approval

- refund requests, address changes, or cancellation attempts before the dispute

This is the practical trade-off. More documentation takes time, but rebuilding missing evidence later takes more time and usually produces worse results. For most Shopify stores, the goal is not perfect documentation on every order. It is consistent documentation on the orders most likely to come back as chargebacks.

Keep fraud review and disputes on the same system

If fraud review lives in one tool and disputes live in someone's inbox, evidence gets lost. We see this all the time with growing stores. Ops approves the order, support handles the customer, and whoever fights the chargeback has to piece everything together from Shopify, email, tracking pages, and internal messages.

A shared workflow fixes that. It can be simple if your volume is low: Shopify Flow, gateway rules, help desk notes, and a dispute folder with a naming standard your team follows. But once chargebacks are frequent, manual collection starts to break down.

ChargePay is one option for merchants who want that dispute work handled automatically. It is an AI-powered chargeback management app for Shopify merchants that generates representment responses, assembles evidence packages, and submits them before issuer deadlines.

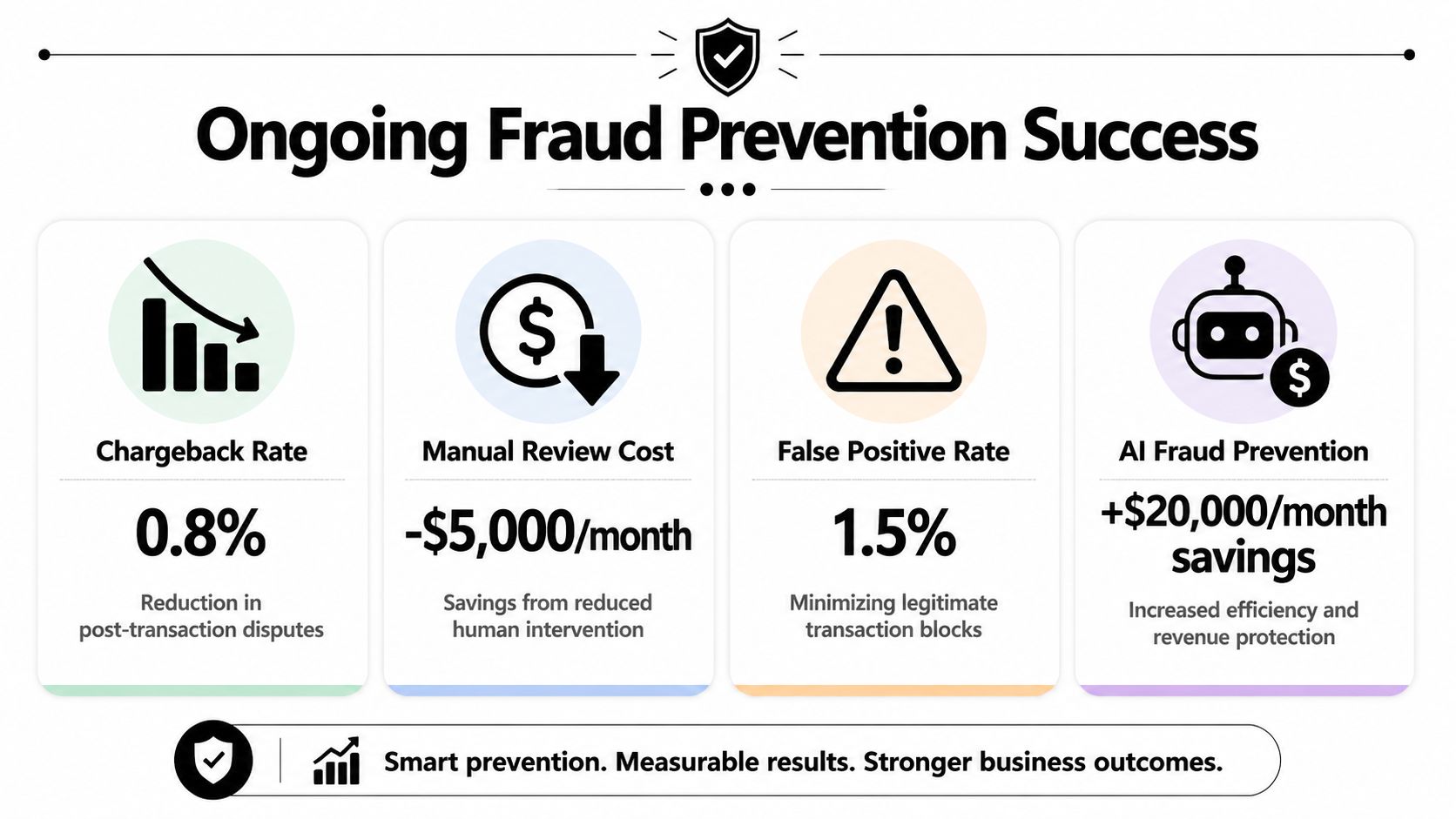

Monitor KPIs and Let AI Handle the Rest

A fraud risk assessment loses value fast if you do not revisit it. Shopify stores change week to week. New products launch, ad channels shift, repeat buyers behave differently during promotions, and fraudsters test whatever looks easiest to exploit.

That means your review process needs a feedback loop, not a one-time setup. Public guidance points the same direction. Teams are expected to monitor how controls perform over time and update them as risks change, as described in Fraud.com's discussion of continuous fraud risk assessment.

Watch the numbers that change decisions

You do not need a sprawling BI project. You need a small set of KPIs that help you decide what to tighten, what to relax, and where chargebacks are coming from.

Track items like these:

- Chargeback rate by product or channel: Shows where losses cluster.

- Manual review rate: Shows whether your team can keep up with flagged orders.

- Approved orders that later dispute: Shows where your rules are missing preventable risk.

- False positives: Shows where good customers are getting blocked or delayed.

- Representment win and loss themes: Shows which evidence holds up.

Another useful reference is AI for detecting financial anomalies, which explains how teams use pattern detection to surface exceptions worth review. The exact use case is different from e-commerce fraud, but the discipline is the same. Watch for drift, outliers, and repeated failure points.

Review based on pain, not calendar dates

Do not wait for a monthly meeting if the warning signs are already there. If one SKU starts attracting “not as described” disputes, review the product page, fulfillment accuracy, and support history. If one paid channel suddenly sends low-quality traffic, tighten rules there before you tighten the whole store. If manual review volume climbs but chargebacks stay flat, your thresholds are wasting time.

This short video shows how automated chargeback workflows fit into that ongoing process.

For merchants who want the operational side mapped out, this guide to automated chargeback and dispute management using AI is a useful next step.

Build a system your team can actually maintain

At low volume, a spreadsheet and a few rule checks can be enough. At higher volume, that approach starts to fail. Reviews become inconsistent, evidence collection slips, and your team spends more time chasing disputes than preventing them.

That is the trade-off Shopify merchants run into all the time. Big-enterprise fraud programs assume dedicated analysts and custom tooling. Most stores do not have that. You need a process built around the data and workflows you already have in Shopify, your gateway, your help desk, and your fulfillment stack.

If chargebacks are eating margin and your team is stuck reacting after the fact, install ChargePay from the Shopify App Store. It has a Built for Shopify badge and a pay-per-win model, so you pay when money is recovered.

.svg)

.svg)

.svg)

.svg)