When you boil it down, the main difference between an issuer vs acquirer comes down to who they work for. The issuer is the customer’s bank—the one that puts the credit card in their wallet and gives the thumbs-up (or down) on their transactions. The acquirer, on the other hand, is your bank, the one that sets up your merchant account and handles the card payments you receive.

Understanding the Key Players in Every Transaction

Every time a customer clicks “buy” on your website, a complex but lightning-fast process kicks off behind the scenes. Two major financial institutions—the issuer and the acquirer—are at the heart of every single one of these transactions. It’s easy to get them mixed up, but knowing exactly what each one does is your first step toward mastering your payments and winning more disputes.

Think of it as a quick negotiation between two parties. The issuer acts as the cardholder's representative, looking out for their customer's best interests. Its main job is to check if the cardholder has enough funds or credit and to sniff out any potential fraud before approving a purchase.

On the flip side, the acquirer is the merchant's representative. This is the bank that gives you a merchant account, connects you to the big card networks like Visa and Mastercard, and makes sure the money from a sale actually makes it to your business account. You can get a deeper dive into their role in our guide to acquiring banks.

Even though they have to work together to complete a payment, their core priorities couldn’t be more different. The issuer is all about keeping the cardholder happy and secure. The acquirer is focused on making payment processing smooth and reliable for you, the merchant. This difference really comes into play when a customer files a chargeback.

Key Takeaway: The issuer works for the customer, and the acquirer works for you. This simple fact shapes the entire flow of money and dictates how disputes are handled from start to finish.

This table gives you a quick breakdown of their core functions.

At a Glance: Issuer vs Acquirer Core Functions

Tracing a Payment from Click to Deposit

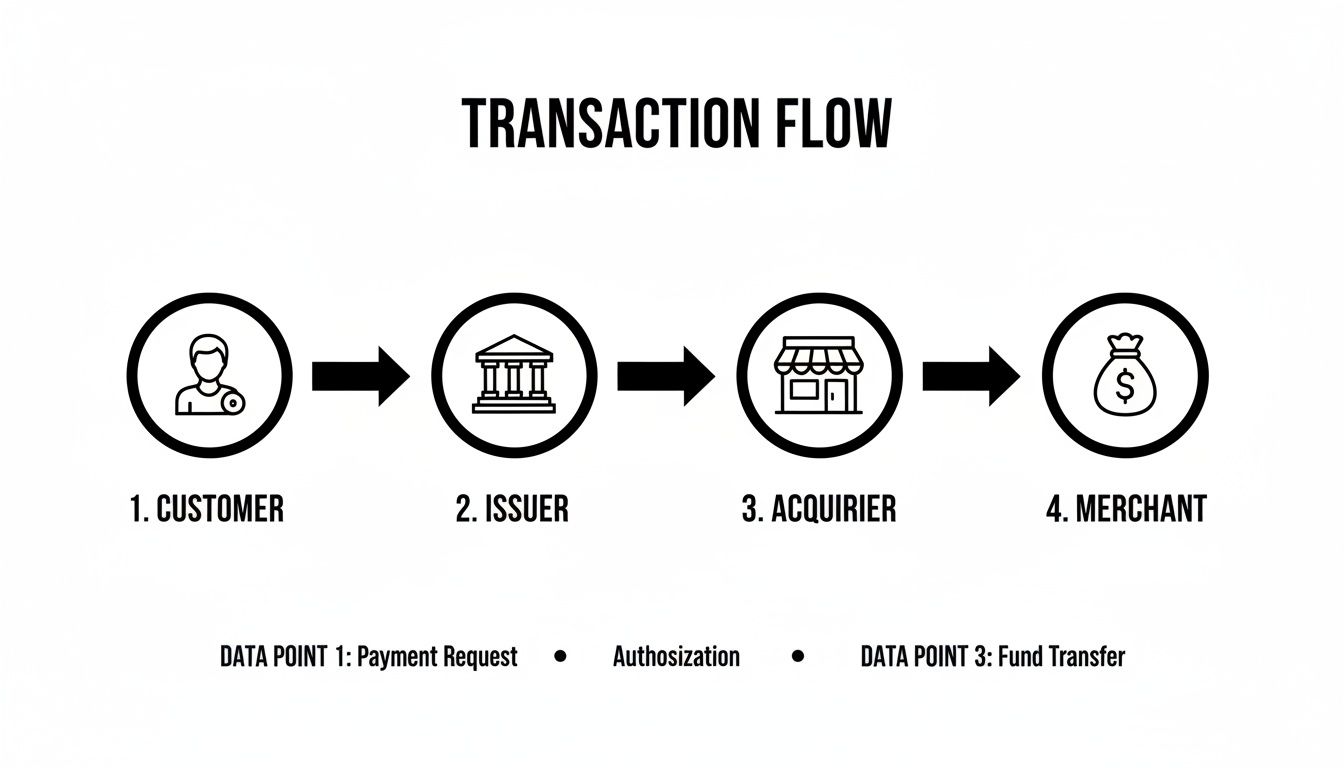

To really get the difference between an issuer and an acquirer, it helps to follow the money. Every single online purchase, no matter how small, sets off a rapid-fire chain of events that pulls in both of these key players. The wild part? This all happens in just a few seconds, creating a seamless link between your customer's wallet and your business account.

Let's walk through a typical transaction, starting right from the moment a customer hits "buy."

The Customer Clicks Pay

It all starts on your website. A customer has a cart full of items, heads to checkout, and types in their credit card details. When they click that "Pay" or "Complete Purchase" button, they're not just sending information to you—they're kicking off a much bigger conversation.

That single click sends the transaction details—the card number, expiration date, CVV, and purchase amount—straight to your payment gateway. The gateway wraps this information up securely and forwards it to the next stop: your acquirer. And this is where the acquirer’s main job really begins. To see exactly how gateways and acquirers fit together, you can learn more about what a payment processor does in our detailed guide.

The Acquirer and Issuer Communicate

Once your acquirer gets the transaction request, it essentially acts as a messenger. It pushes the information through the right card network, like Visa or Mastercard, which then delivers the request directly to the customer's issuing bank.

Now, the issuer takes center stage. In a split second, it runs several critical checks:

- Funds Verification: Does the cardholder actually have enough available credit or money in their account to cover this purchase?

- Security Checks: Is the card valid? Has it been reported lost or stolen? Do the details provided (like the CVV and address) match what’s on file?

- Fraud Analysis: Does this transaction look sketchy? The issuer uses its own fraud detection systems to flag anything unusual, like a purchase coming from a completely unexpected location.

Based on these checks, the issuer makes a final call: approve or decline.

The issuer holds the ultimate power of approval. It has the final say on whether a transaction can proceed, based entirely on protecting its cardholder and its own financial risk.

This response—an approval or a decline code—travels back along the same path. It goes from the issuer, through the card network, to your acquirer, and finally back to your website. That's when your customer sees either a confirmation screen or that dreaded error message.

This diagram breaks down the journey of a single payment from the customer all the way to the merchant.

As you can see, the acquirer acts on behalf of the merchant, while the issuer represents the customer, with the card networks making sure they can talk to each other.

Settlement: The Money Arrives

Even with an approved transaction, the process isn't quite finished. At the end of the day, the acquirer gathers up all your approved transactions and settles them in one big batch. It pulls the funds from all the different issuers and deposits the total amount (minus any processing fees, of course) into your merchant account.

This final step is what ensures you actually get paid for the sale.

The Chargeback Process Where Issuers and Acquirers Diverge

When a transaction goes smoothly, the issuer and acquirer work together in perfect harmony. But the moment a customer disputes a charge, their roles pivot, and their interests suddenly diverge. This is where truly understanding the difference between an issuer vs acquirer directly impacts your revenue.

The process kicks off when a cardholder contacts their issuing bank to question a charge. The issuer's main responsibility is to its cardholder, so it almost always sides with them initially. It files a chargeback, gives the customer a provisional credit, and pulls the funds back from your acquirer.

This action triggers your acquirer to debit the disputed amount from your merchant account, along with a separate chargeback fee. At this point, the acquirer’s role shifts from being a simple payment facilitator to your partner in defense. It notifies you of the dispute and gives you the platform to fight back through a process called representment.

The Issuer as Judge

Once you submit your defense, the issuer effectively acts as the judge and jury. It reviews the evidence you provided through your acquirer to decide if your original transaction was legitimate. Its decision is heavily influenced by card network rules and, of course, its duty to protect its customer.

The issuer is essentially asking one question: Did the merchant fulfill their side of the bargain fairly and prove it?

Critical Insight: The issuer makes the final decision on whether a chargeback is reversed. Your acquirer is your advocate, but the issuer holds all the power in the dispute resolution process.

This is why providing clear, compelling evidence is so critical. A detailed breakdown of the Visa chargeback process can give you a better sense of the specific rules you need to follow. The issuer won't do the investigative work for you; the burden of proof is entirely on the merchant.

The Acquirer as Your Advocate

Your acquirer's job is to manage the communication between you and the issuer. A good acquirer will offer tools and support to help you build a strong case. However, they are also managing their own risk. If you have too many chargebacks, you become a high-risk client for them.

This creates a delicate balance. The acquirer wants to support you but must also enforce the rules set by the card networks and issuers.

This dynamic has become even more complex as the nature of disputes has changed. Chargebacks are no longer just about clear-cut criminal fraud. In fact, more than half of all chargebacks now stem from non-fraudulent issues. According to recent industry data, only 45% of chargebacks are fraud-related, with the rest coming from things like confusing billing descriptors, shipping delays, or refund friction. This means merchants are increasingly fighting disputes rooted in customer service gaps rather than outright theft.

A Practical Plan for Winning More Disputes

Knowing the difference between an issuer and an acquirer is a solid first step. But what really matters is turning that knowledge into a strategy that actually protects your revenue.

When a dispute lands, your goal is simple: make it incredibly easy for your acquirer to help you and for the issuer to rule in your favor. This all comes down to a proactive plan—one that stops disputes before they start and gives you the best shot at winning the ones you can't avoid.

Your first line of defense is always prevention. Since the issuer’s number one job is to protect their cardholder, a lot of disputes pop up from basic customer service friction. You can get way ahead of these problems by focusing on clarity and communication.

Fortify Your Defenses Proactively

Preventing disputes is always cheaper and way less stressful than fighting them. Start by looking at the common pain points that make a customer call their bank in the first place.

- Clarify Your Billing Descriptor: Make sure your billing descriptor is something customers will recognize instantly. "SPARKLEJEWELRY.COM" is a world away from a generic corporate name like "SJ HOLDINGS LLC," which someone might not connect to their purchase.

- Provide Proactive Customer Service: Don't hide your contact information. An easy-to-reach customer service team can solve an issue long before it escalates into a chargeback.

- Set Clear Expectations: Be upfront about everything—shipping times, return policies, product details. The more a customer knows, the less likely they are to feel like they were misled.

By tackling these common triggers, you're taking away the reasons an issuer would even need to step in. You're solving the customer's problem before they ask their bank to do it for them.

Master Your Representment Strategy

When a dispute does happen, your acquirer is your advocate. Your job is to arm them with undeniable proof that the transaction was legit. The evidence you pull together needs to be clear, concise, and directly challenge the cardholder's claim.

Key Insight: Your representment package isn't just a pile of documents; it's a compelling argument. You're telling a story with evidence to prove to the issuer that you held up your end of the deal.

A strong rebuttal letter zero-in on the specific reason code and includes compelling evidence to back it up. For a deeper dive, check out our guide on how to win a credit card dispute.

Getting this right is more important than ever. Chargebacks are expected to cost merchants a staggering $33.79 billion globally in 2025, a number set to jump to $41.69 billion by 2028. For small businesses, this is a heavy burden, with chargeback volumes already surging over 10% in 2024 alone. This is exactly why about half of all merchants now outsource their dispute management.

How Automation Helps You Manage Disputes Better

Trying to manually track the endless back-and-forth between your business, your acquirer, and the issuer is a recipe for disaster. It's a slow, painful process filled with opportunities for costly mistakes. This is where automation tools don't just help—they completely change the game, acting like an expert translator between everyone involved in a dispute.

Instead of forcing you to dig through old order histories, shipping logs, and customer emails, an AI-powered platform like ChargePay does all the heavy lifting. It automates the entire evidence-gathering process, pulling together the exact documents you need to build a case you can actually win.

This isn't just about saving a few hours a week. Switching from manual to automated dispute management fundamentally strengthens your position in every single chargeback case. You'll meet every deadline and submit professional, compelling evidence every single time.

Speaking the Right Language for Issuers and Acquirers

The secret to winning a dispute is giving the issuer evidence that directly refutes the specific reason code they cited. This is where an automated system truly shines, tailoring each response to the strict requirements of the card networks.

Let's say a customer claims they never received their package—a classic chargeback reason. The system instantly gets to work, pulling:

- Shipping confirmation showing the customer’s address.

- Delivery verification from the carrier, complete with a timestamp.

- Customer communications proving you addressed their questions.

All this evidence gets compiled into a perfectly structured rebuttal that speaks directly to the issuer’s concerns. Your acquirer can then present this clean, organized package, which not only makes their job easier but also seriously boosts your odds of getting the chargeback reversed. It’s like having an expert on your team who knows exactly what an issuer needs to see to rule in your favor.

The Power of Automation: Automation acts as your expert agent, translating your transaction data into the precise language and evidence formats that both acquirers and issuers require. This streamlines the process and helps you recover revenue you would otherwise lose.

Building a Stronger Merchant Reputation

When you consistently submit well-documented, evidence-based responses, you're doing more than just winning individual disputes. You're also building a better reputation with your acquirer. When they see that you’re proactively and effectively managing chargebacks, they start to see you as a lower-risk merchant.

Over time, this improved standing can lead to better processing terms and a more supportive partnership. Ultimately, automation bridges the communication gap in the whole issuer vs acquirer dynamic by making sure your side of the story is always presented clearly, professionally, and with undeniable proof. For a deeper dive into how this all works, check out our complete guide to automated chargeback and dispute management using AI.

Your Top Questions About Issuers and Acquirers, Answered

When you're trying to make sense of the payment world, it’s easy to get tangled up in the roles of issuers and acquirers. Let's clear up some of the most common questions merchants have, especially when a dispute lands on your desk.

Who Has the Final Say in a Chargeback: Issuer or Acquirer?

The issuer has the final say. Always.

Think of your acquirer as your legal counsel in the chargeback court. They help you prepare your case and present it on your behalf, but they don't make the final ruling. The issuer is the judge and jury, and their primary loyalty is to their cardholder—the customer.

The issuer reviews the evidence from both sides against the card network's rulebook and makes the binding decision.

Can I Talk Directly to My Customer’s Issuing Bank?

No, you can't just pick up the phone and call the customer’s bank. All communication during a chargeback dispute has to follow a very specific, structured path.

Your acquirer is your one and only point of contact. You give them your evidence, and they are responsible for passing it up the chain through the card network to the issuer. It’s a formal process designed to keep everything standardized and fair.

Key Takeaway: Your business relationship is with your acquirer, not the issuer. The single best thing you can do is build a rock-solid, evidence-backed case to give your acquirer. That’s your only shot at influencing the issuer's decision.

What Should My Acquirer Do to Help Me Fight Disputes?

A good acquirer is more than just a payment gateway; they should be a partner in your corner when disputes pop up. While the level of support varies, here’s what you should expect from a solid acquiring partner:

- A Clear Portal: An intuitive online system where you can see new chargeback alerts and easily upload your evidence.

- Educational Resources: Helpful guides, best practices, and tips on how to put together a winning case for different reason codes.

- Responsive Support: A real team you can reach out to when you have questions about a specific case or what kind of evidence you need.

At the end of the day, your acquirer's job is to facilitate the process. The heavy lifting of gathering compelling evidence still falls on you, the merchant.

Why Do Issuers Seem to Always Side with the Cardholder?

It’s not just a feeling; there’s a reason for it. The issuer's entire business model is built on keeping their cardholders happy and feeling secure. They have a direct relationship with the customer who they want to keep using their card.

When a cardholder disputes a charge, the issuer's default stance is often to trust their customer and issue a provisional credit. This "customer-first" approach is baked into their service. To overcome this built-in bias, your evidence can't just be good—it has to be undeniable. You need to prove, without a doubt, that the charge was valid and you delivered on your promise.

The pressure is mounting on everyone. A recent Mastercard report projects that global chargeback volumes will climb to 324 million transactions by 2028. For merchants, the financial hit is staggering—losing an estimated $4.61 for every dollar lost to chargebacks. This makes fighting back effectively more critical than ever. You can learn more about these chargeback trends and their impact here.

Stop letting manual dispute management drain your time and money. ChargePay uses AI to automate the entire representment process, building evidence-based cases that recover up to 80% of your lost revenue. See how much you can get back at https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)