That sinking feeling you get when you check your Shopify dashboard and see hard-earned revenue has simply vanished? It's a harsh reality for many online merchants, and the culprit is often a Mastercard chargeback.

This isn't just a minor bookkeeping annoyance; it's a direct hit to your profitability. A chargeback is a forced payment reversal started by a customer's bank, pulling money right out of your account long after you thought a sale was complete. You're left without the product and without the payment.

At ChargePay, we’ve turned this fight into a science. We’ve helped Shopify merchants recover over $2.8M+ across more than 100,000 disputes, and we carry a 92.4% win rate. We know exactly what it takes to get your money back.

Why Your Revenue Is Vanishing and How to Stop It

A huge piece of this problem is something called 'friendly fraud.' This is when a legitimate customer receives your product but disputes the charge anyway, essentially getting it for free. For stores in high-volume sectors like fashion or electronics, this can feel like a constant battle.

And it’s getting worse. A Mastercard-backed study revealed that this kind of first-party misuse is now behind a staggering 45% of all chargebacks. Globally, this is projected to cost businesses over $15 billion by 2026. This isn't just the cost of doing business—it's a serious threat to your bottom line.

Understanding the Battlefield

To fight back, you have to know what you're up against. A chargeback isn’t a simple refund. It's a formal, multi-stage dispute process with strict rules and deadlines set by the card networks.

On top of the lost revenue, each dispute also slaps you with a separate, non-refundable penalty fee from your payment processor. If you want to see how these hidden costs stack up, take a look at our guide on what a chargeback fee is and the damage it can do.

To give you a clearer picture, let's break down the moving parts.

A Mastercard Chargeback at a Glance

A chargeback isn't a simple two-way street between you and the customer. It involves several players, each with a specific role. Here’s a quick overview of the journey a dispute takes from start to finish.

| Stage | Key Player | What Happens |

|---|---|---|

| Transaction | Cardholder | Purchases an item from your store using their Mastercard. |

| Dispute | Cardholder & Issuing Bank | The customer contacts their bank (the issuer) to dispute the charge. |

| Chargeback | Issuing Bank & Acquirer | The issuer pulls the funds from your merchant account via your bank (the acquirer). |

| Notification | Acquirer & Merchant | You (the merchant) are notified of the chargeback and the funds are debited. |

| Representment | Merchant | You gather evidence and submit a rebuttal to fight the chargeback. |

| Final Decision | Card Network & Banks | The banks and Mastercard review the case and make a final ruling. |

Understanding this flow is the first step toward building a solid defense and taking control of the outcome.

Winning requires more than just knowing you were in the right; it demands a solid strategy and compelling evidence. To keep your business healthy, you also need to focus on growth to offset these unavoidable costs. A strong plan to increase Shopify sales is a crucial part of any resilient e-commerce strategy.

This guide will walk you through everything you need to know about Mastercard chargebacks. We'll cover the process, the reason codes, and how to build a representment case that actually wins. It’s time to stop seeing chargebacks as a loss and start treating them as a solvable problem.

The Mastercard Chargeback Process Explained

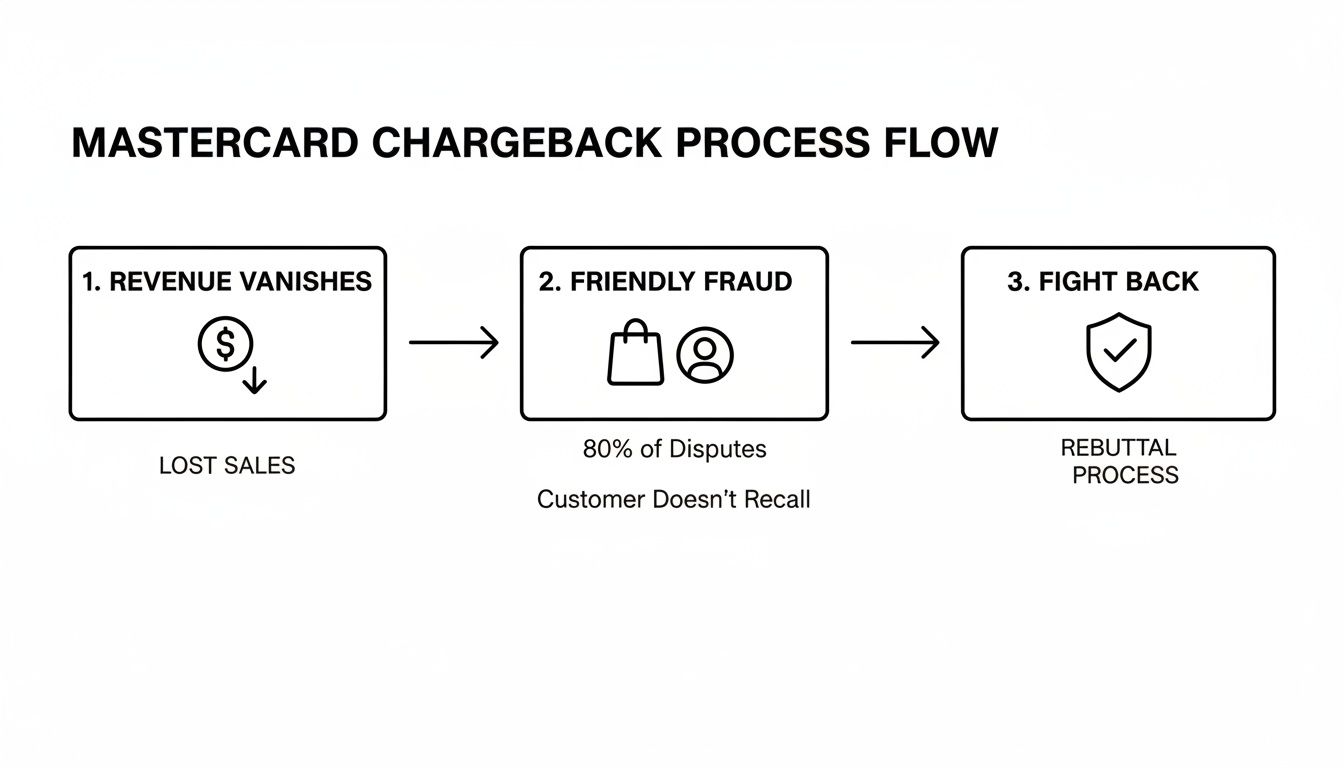

When a customer disputes a Mastercard transaction, it kicks off a formal process that can feel confusing and stacked against you. Think of it as a small-scale court case where your payment processor and the customer's bank are the lawyers, and Mastercard acts as the judge. Understanding each step is your best bet for knowing where and when to fight back to recover your revenue.

The whole thing starts with the cardholder. Instead of just contacting you for a refund, they go straight to their bank—the issuing bank—and claim there’s an issue with the charge. The bank then fires off the chargeback, immediately pulling the funds from your merchant account through your bank, also known as the acquirer. Just like that, the money is gone before you even get a chance to tell your side of the story.

This is the point where you really feel the sting. Not only is the sale revenue reversed, but you also get hit with a non-refundable chargeback fee of around $15 to $40. The system can feel intimidating, but once you know the rules of the game, you can navigate it effectively.

The Key Players in a Chargeback Dispute

Four main parties are involved in every Mastercard chargeback. Knowing who's who helps clear up why certain steps take so long.

- The Cardholder: This is your customer who made the original purchase.

- The Issuing Bank: The customer's bank (like Chase or Bank of America). They start the dispute for their customer.

- The Acquiring Bank: This is your bank or payment processor (like Shopify Payments or Stripe). They pass the chargeback info to you and represent you to the card network.

- Mastercard: The card network that sets all the rules, manages the process, and makes the final call if the banks can't agree.

Once the money is pulled from your account, you get a notification, and the clock starts ticking. This is your one and only shot to challenge the dispute. If you want a deeper dive into how this works across different card brands, you can learn more about bank chargebacks in our detailed guide.

This process flow shows just how quickly a simple transaction can turn into a battle for your revenue.

The diagram lays it all out: from lost revenue and friendly fraud to fighting back. It makes it clear that a proactive defense isn't just an option—it's a necessary part of doing business.

From Retrieval Request to Representment

Sometimes, before a full-blown chargeback hits, the issuing bank might send a retrieval request. This isn't a chargeback yet; it's just a request for more information about the transaction, like a copy of the sales receipt. Responding to this quickly and accurately can sometimes stop a dispute in its tracks.

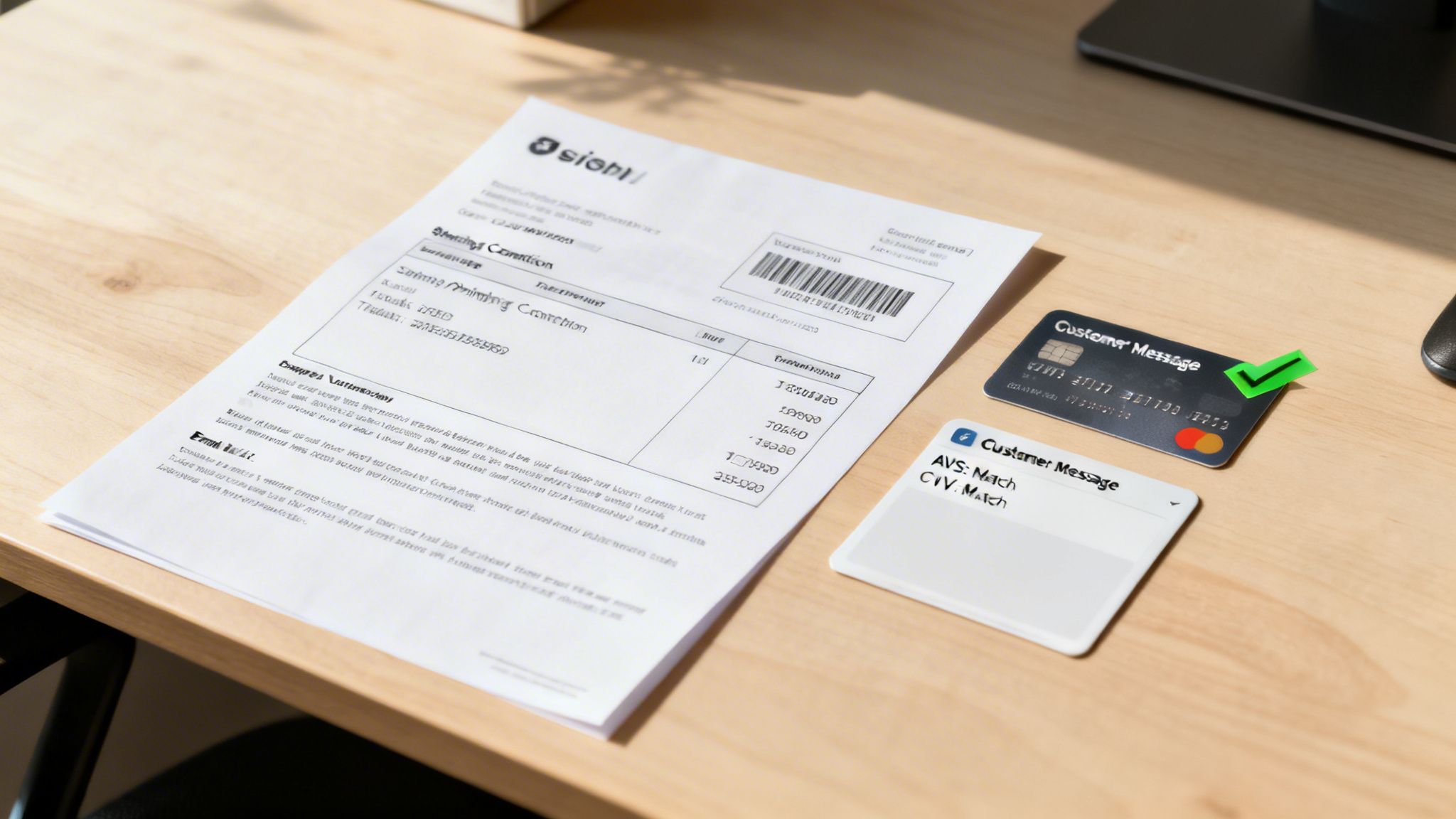

If the issue moves forward, you enter the representment stage. This is your formal opportunity to "re-present" the transaction to the issuing bank, armed with evidence proving it was legitimate. You'll need to gather documents like shipping confirmations, delivery photos, AVS/CVV match results, and any emails or messages you exchanged with the customer.

A study by Mastercard found that merchants lose about 75% of the chargebacks they fight. But that number is misleading—it's heavily skewed by small businesses that don't have the time or tools to fight back effectively. At ChargePay, we win 92.4% of disputes for our Shopify merchants because our AI knows exactly what evidence to submit for every single case.

Arbitration: The Final Stage

If the issuing bank denies your representment, the fight doesn't have to be over. You have one last option: escalating the case to arbitration. This is the final stage where Mastercard steps in directly to review all the evidence from both sides and make a final, binding decision.

Be warned, though—arbitration is a risky and expensive move. It comes with hefty fees (often $500 or more), and if you lose, you're on the hook for them. This step is usually only worth it for very high-value disputes where your evidence is rock-solid. For most Shopify merchants, winning at the representment stage is the most practical and cost-effective goal.

Common Mastercard Reason Codes and How to Defeat Them

When a Mastercard chargeback hits your account, it doesn’t just show up randomly. It comes with a four-digit reason code, which is the bank's official story for why your customer is disputing the charge. Think of it as the headline for the complaint against you.

Knowing what these codes mean is your first step toward fighting back and keeping your hard-earned revenue.

If you're running a Shopify store, you'll notice a few codes pop up more than others, especially ones tied to fraud or product issues. But here’s the catch: the official reason isn't always the real reason. A dispute coded as "fraud" might actually be "friendly fraud"—where a legitimate customer buys something, receives it, and then tries to get their money back anyway.

And this problem is about to get a lot bigger. Projections show that by 2028, the world will see a staggering 324 million Mastercard chargebacks each year. That’s a 24% leap from 2026 alone. This boom is fueled by easier dispute processes for shoppers and the non-stop growth of ecommerce, where friendly fraud runs rampant.

For Shopify merchants, this is a direct hit to the bottom line, with friendly fraud potentially making up 75% of all chargebacks.

Let's unpack the most common codes you'll face and give you a clear-cut checklist of the evidence you need to win.

Top Mastercard Reason Codes and Your Evidence Checklist

To fight back effectively, you have to match the right evidence to the right reason code. It's like having the right key for a specific lock. Below is a quick guide to some of the most frequent codes and the exact proof you'll need to submit a winning response.

| Reason Code | Common Cause | Key Evidence to Submit |

|---|---|---|

| 4837 | No Cardholder Authorization: The customer claims they didn't make or approve the purchase. This is a classic flag for potential friendly fraud. | AVS/CVV match results, IP address geolocation matching the billing address, previous successful order history, and any customer emails or chats. |

| 4853 | Cardholder Dispute: The customer admits they made the purchase but claims the item was not as described, defective, or never arrived. | Product page screenshots, detailed product descriptions, proof of delivery (tracking number and photo), and a copy of your return policy. |

| 4840 | Fraudulent Processing of Transactions: Usually suggests a transaction was processed multiple times or an incorrect amount was charged. | A copy of the transaction receipt showing the correct, single charge. If it was a duplicate, show proof that you already refunded the extra charge. |

| 4863 | Cardholder Does Not Recognize: A variation of code 4837, often caused by an unclear billing descriptor on their bank statement. | Proof of a clear billing descriptor, AVS/CVV match, and IP address verification. Customer communication is also very helpful here. |

Having this checklist ready turns a confusing, defensive scramble into a clear, actionable plan. It’s the difference between losing revenue and protecting it.

Code 4837 No Cardholder Authorization

This is one of the most common codes out there and a huge red flag for friendly fraud. The customer is flat-out saying, "I didn't buy this."

While this can point to real criminal fraud, it’s far more likely that the customer simply forgot about the purchase, didn't recognize your store's name on their statement, or is deliberately trying to get something for free.

How to Fight It

Your mission is simple: prove the real cardholder placed the order. You need to connect the dots between the customer, their card, and the transaction.

- AVS and CVV Results: This is your first and best piece of evidence. Show that the Address Verification System (AVS) and the CVV code entered at checkout matched the bank's records.

- IP Address Geolocation: Provide the IP address from the order and show that it maps to the customer’s billing or shipping city. It’s hard to claim fraud when the order came from their own house.

- Previous Order History: Has this customer ordered from you before with the same card and address? Show this history. It builds a pattern of legitimate behavior.

- Customer Communications: Dig up any emails, live chats, or social media messages you have from the customer. Anything where they discuss the order is gold.

Code 4853 Cardholder Dispute

This code covers a broad range of issues where the customer acknowledges making the purchase but isn't happy with what they got. For ecommerce stores, this usually means "not as described" or "defective merchandise."

At ChargePay, we see merchants lose these "he said, she said" disputes all the time because they lack the right documentation. Our AI automatically pulls every piece of relevant data—from order notes to delivery photos—to build a case that banks can't ignore, leading to our 92.4% win rate.

How to Fight It

Here, you need to prove that what you sent is exactly what you advertised on your Shopify store.

- Product Page Screenshots: Submit a screenshot of the product page from when the customer made the purchase. Make sure it includes the description, photos, and price.

- Proof of Delivery: This is non-negotiable. Provide the tracking number showing the package was delivered to the correct address. A delivery confirmation photo is even stronger.

- Your Return Policy: Include your store's return policy and point out that the customer never tried to contact you for a return or exchange. Many customers skip this step, which seriously weakens their chargeback claim.

If you want to dive deeper into all the things that can trigger a dispute, check out our guide covering the top reasons for a chargeback.

Turning these confusing codes into a simple action plan is how you stop hemorrhaging money. By matching the right evidence to the right reason code, you can turn a major headache into a routine process for recovering revenue.

Building a Winning Representment Case

Getting that Mastercard chargeback notification can feel like a punch to the gut. It often seems like the bank has already decided you're in the wrong. But it’s not over yet. The representment process is your one shot to push back, tell your side of the story, and get your money back.

This isn’t about firing off a quick, angry email. It's about methodically building an airtight case that shows the chargeback is bogus and the original transaction was completely valid.

And you have to move fast. While Mastercard technically gives you 45 days to respond, that number is dangerously misleading. Your payment processor will give you a much, much shorter deadline—usually somewhere between 7 to 10 days—to get all your evidence together. If you miss that window, you automatically lose. It’s a done deal.

The Anatomy of a Powerful Rebuttal

A winning representment case is all about compelling evidence. Your job is to assemble a clear, logical story that leaves no room for doubt in the reviewer's mind. You need to dismantle the cardholder’s claim, piece by piece, with cold, hard proof.

Think of yourself as a detective. The customer made a claim ("I never bought this," or "This isn't what I ordered"), and you need to present the facts that prove them wrong. Your rebuttal letter should be short and to the point, acting as a cover sheet that summarizes the rock-solid evidence you've attached.

We see merchants lose disputes every single day, not because they were at fault, but because their evidence was a mess or just plain incomplete. At ChargePay, our AI has crunched the data from over 100,000 disputes to figure out exactly what evidence wins. It's how we've hit a 92.4% win rate for our Shopify merchants—by building the perfect evidence package, every time.

Your Compelling Evidence Checklist

The exact proof you need will change depending on the chargeback reason code, but a strong case nearly always has a mix of these elements. The key is to organize it so a busy bank employee can understand your side in under a minute.

Transaction and Order Details: Start with the basics. A copy of the order receipt showing the date, time, and purchase amount is your foundation.

Proof of Authorization: This is your best weapon against "I didn't authorize this" claims. You need to show the AVS (Address Verification System) and CVV match results. A positive match here is huge.

IP Address Geolocation: Show the IP address the customer used to place the order and where it's located. If it matches their billing or shipping city, their fraud claim starts to look pretty weak.

Shipping and Delivery Confirmation: This is non-negotiable for any "item not received" claim. You must provide a valid tracking number and a screenshot of the delivery confirmation showing it arrived at the customer's address. If you have a photo of the delivery, that's even better.

Customer Communication Records: Did the customer email you or use your site's live chat? Include screenshots of every single conversation. This is especially powerful if they asked for a tracking update or mentioned they had received the item.

Order History: Is this a repeat customer? If they've successfully ordered from you before using the same card and shipping details without any issues, it shows a pattern of legitimate behavior.

Product and Policy Information: For "not as described" claims, provide screenshots of the product page and a copy of your store’s return policy. This proves you were transparent and shows the customer didn't follow the correct process for a return.

Putting all of this together can feel like a full-time job, which is why we created a detailed guide on how to master the chargeback representment process. It breaks down every step you need to take.

Fighting a Mastercard chargeback is a battle you can absolutely win, but you have to show up prepared. By building a thorough and professional representment case, you give yourself the best possible chance to protect the revenue you worked so hard to earn.

Proactive Strategies to Prevent Chargebacks

Let's be honest: the best way to deal with a Mastercard chargeback is to make sure it never happens in the first place. While winning a dispute feels good and gets your money back, a smart prevention strategy saves you from ever entering the ring. This protects your revenue, your products, and most importantly, your time.

These preventative steps don't have to be some massive, complicated overhaul. Often, it's the small, strategic tweaks to your Shopify store and how you talk to customers that make the biggest difference, turning potential disputes into simple fixes or even happy, repeat buyers.

The financial hit from a chargeback is no joke. It's always more than just the original sale amount. For merchants in high-risk sectors like fashion and electronics, a single chargeback can cost an average of $110 in the U.S. The impact on small businesses can be devastating, with studies showing 1 in 5 merchants hit by fraud eventually have to file for bankruptcy.

Fine-Tune Your Billing and Policies

So much of this comes down to avoiding confusion. When a customer sees a charge on their statement they don't recognize, their first instinct is to call their bank, not you.

An easy win here is to set a clear billing descriptor. Instead of a cryptic code like "SPKL*WEBSHOP," make sure the name that appears on their statement is instantly recognizable—like "SPARKLE JEWELRY." This one tiny change can stop countless "Cardholder Does Not Recognize" disputes before they start.

Next, you need to make your store policies impossible to miss. Your refund and return policies should be crystal clear, easy to find, and fair. A transparent policy builds trust and gives customers a direct path to resolving issues with you, heading off a chargeback before it even becomes a thought.

Fortify Your Checkout with Fraud Filters

While some chargebacks are from confused customers, others are just plain old criminal fraud. This is where basic security at your checkout becomes your first line of defense. Think of these tools as a digital bouncer, stopping shady transactions before they can ever cause a problem.

Setting up solid defenses is a core part of any good chargeback strategy. You can learn more by checking out our guide on the payment fraud essentials. For now, start with these two fundamental tools:

- Address Verification System (AVS): This tool simply checks if the billing address the customer enters matches what the bank has on file for that card. A mismatch is a huge red flag for fraud.

- Card Verification Value (CVV): Always, always require the three or four-digit security code from the back of the card. This proves the customer physically has the card, which makes it much harder for fraudsters who only have a stolen card number.

These checks are standard features on platforms like Shopify and give you critical evidence if you ever do need to fight a chargeback down the road.

Make Customer Service Your Best Weapon

Never underestimate the power of great customer service. It's one of the most effective chargeback prevention tools you have. When customers can easily find your contact info and get a quick, helpful response, they are far less likely to escalate a problem to their bank.

Plaster your contact information everywhere—on every page of your site, if you can. Offer a few different ways for people to get in touch, like email, a phone number, or live chat, and be clear about your response times. A little empathy and a quick solution can turn a potential dispute into a positive experience, saving you hundreds of dollars in the process.

Let Automation Handle the Fight and Win Back Your Money

Trying to fight a Mastercard chargeback by hand is a tough game. It's complicated, eats up your time, and honestly, feels like an uphill battle. It pulls you away from what you should be doing—running and growing your Shopify store. You're left digging for evidence, trying to write the perfect rebuttal, and racing against deadlines, all while the odds feel stacked against you.

This manual process is exactly what "friendly fraudsters" are banking on. They know that for a single transaction, most business owners are just too swamped to put up a proper fight. But this is where you can flip the script by letting automation step in.

Let AI Handle the Heavy Lifting

We created ChargePay with Shopify merchants like you in mind. Our AI platform does more than just help you keep track of disputes—it takes over the entire process for you. For every single chargeback you get, it automatically gathers the evidence and submits the strongest possible case.

We've trained our AI on the lessons learned from over 100,000 disputes we've managed for other Shopify stores. It knows exactly what proof a bank needs to see to overturn a chargeback, whether the reason is "no cardholder authorization" or "product not as described."

What's the result of all that learning? We've successfully recovered over $2.8M+ for our merchants and hold a 92.4% win rate. While merchants fighting on their own often take the loss, ChargePay helps turn a frustrating process into a predictable win.

Why Automation Just Makes Sense

Manually fighting chargebacks is a constant drain on your time and money. Automation, on the other hand, gives you a clear return by saving you time and getting your lost sales back. It’s a real competitive advantage.

Here’s what you get when you let automation take over your defense:

- Instant Responses: Our AI submits evidence in real-time. You never have to sweat a processor's tight 7-10 day deadline again.

- Optimized Evidence: The system automatically pulls the important stuff—AVS/CVV results, IP address data, shipping confirmations, and customer emails—to build the most compelling case.

- No Manual Work: Forget about digging through old orders and spending hours writing rebuttal letters. We manage the entire representment process from beginning to end.

This is all possible because we’ve built a solution that plugs right into the Shopify world. As a 'Built for Shopify' app with a 4.9-star rating, we're a partner that thousands of merchants trust. You can check out a complete guide to automated chargeback management to see exactly how this technology changes the game.

Best of all, ChargePay works on a pay-per-win model. You only pay a fee when we successfully get your money back. There's absolutely zero risk.

Stop letting chargebacks chip away at your revenue and distract you from your business. Install ChargePay from the Shopify App Store and let our AI make your chargeback problem a thing of the past.

Your Mastercard Chargeback Questions Answered

Dealing with a Mastercard chargeback can feel like you're navigating a maze blindfolded, especially when your hard-earned revenue is at stake. Let's clear up the confusion with some straight answers to the questions we hear most often from merchants.

What Is the Difference Between a Mastercard Chargeback and a Refund?

Think of a refund as a handshake agreement. You and your customer agree that a purchase needs to be reversed, you return the money, and you both move on. It’s a straightforward process that you control.

A Mastercard chargeback is a whole different beast. It's a forced reversal initiated by the customer's bank, completely bypassing you. Not only do you get hit with non-refundable penalty fees (usually $15-$40), but it also damages your standing with payment processors. In most cases, you lose the product and the revenue.

How Long Do I Have to Respond to a Mastercard Chargeback?

This is where things get tricky. Mastercard's official rulebook says you have 45 days to respond, but that number can be dangerously misleading. Your payment processor, who is the one that actually alerts you to the dispute, sets its own, much shorter deadline.

If you're a Shopify merchant, you'll find you often have just 7-10 days to pull together all your evidence and submit your response. Miss that tiny window, and it's an automatic loss. This is exactly why having an automated response system is so vital.

Can I Really Win Against Friendly Fraud Chargebacks?

Absolutely. "Friendly fraud"—where a legitimate customer disputes a valid charge—is a numbers game. These customers are often betting on the fact that you'll be too swamped to fight back. You can, and should, win these disputes with the right evidence.

This is where your data becomes your best defense. Things like AVS/CVV match results, delivery confirmation with photos, and IP address logs are incredibly powerful. They systematically prove the purchase was legitimate and the order was delivered. This data-driven approach is exactly how ChargePay achieves a 92.4% win rate for our merchants—we dismantle false claims with undeniable proof.

Stop letting disputes chip away at your profits. ChargePay automates your entire chargeback defense using AI, recovering your revenue while you get back to building your business. Install ChargePay from the Shopify App Store and make chargebacks a solved problem.

.svg)

.svg)

.svg)

.svg)