You check your Shopify dashboard after a strong sales day. Revenue looks healthy. Your payout does not. The gap is not just processor markup or a random platform fee. A meaningful share starts with Mastercard interchange, and if your checkout operations are messy, that same order can cost you again in disputes.

Mastercard interchange is the fee paid between banks when a customer uses a Mastercard. For a Shopify merchant, it shows up as part of the total cost of accepting cards, and it cuts into margin on every order. Treating it like a fixed cost is a mistake. Rates shift based on the card used, the data sent with the transaction, and how cleanly the payment is processed.

That matters because high interchange and chargebacks often come from the same operational problems. Weak AVS and CVV checks, inconsistent billing data, rushed fraud settings, duplicate retries, and late captures can push a transaction into a more expensive risk profile. They also make the issuer less confident when a cardholder disputes the charge. You do not just pay more to accept the sale. You increase the odds of paying chargeback fees, losing revenue, and absorbing the cost of the product too.

For Shopify store owners, the practical move is simple. Tighten checkout data quality, review your fraud filters, use clear billing descriptors, and make sure your authorization and capture flow is clean. If your finance team wants a better way to spot where payment costs are bleeding margin, tools that use AI to turn financial data profitable can help connect fee patterns, failed payments, and dispute exposure before they become a larger profit problem.

Why Interchange Fees Silently Shrink Your Profits

A lot of merchants look at payment fees only when margins get tight. That's too late.

Interchange is one of those costs that doesn't feel dramatic on a single order. It feels annoying. Then you zoom out across a month of Shopify sales, returns, retries, and disputes, and you realize it's eating profit on nearly every transaction. It's a wholesale cost of taking cards, and you don't get to opt out if you want to accept Mastercard.

Most merchants also make a second mistake. They look at fees and chargebacks as separate problems. They're connected. The same operational mess that raises your effective card costs often creates the exact kind of low-confidence transaction banks don't want to defend later.

Your payout report is telling you something

When your payout looks thinner than expected, ask three questions:

- What card mix did I accept: Premium consumer cards and commercial cards can cost more than basic cards.

- How were transactions processed: Card-not-present flows usually cost more than cleaner, lower-risk transaction paths.

- Did payment ops create avoidable friction: Retries, failed captures, poor billing data, and weak fraud screening all add cost.

That's why finance cleanup matters. If you want a useful framework for turning raw numbers into better decisions, this piece on AI to turn financial data profitable is worth reading. The stores that protect margin usually aren't guessing. They're measuring.

Practical rule: If you can't explain why your blended card cost changed this month, you don't control it yet.

Why this matters more on Shopify

Shopify makes selling easy. It does not automatically make your payment economics efficient.

Fast-launch stores often grow into messy billing setups. Subscription logic gets bolted on. Fraud filters stay basic. Refund and retry behavior goes unreviewed. Then fees climb subtly while conversion data still looks healthy. That's dangerous because revenue can grow while cash efficiency gets worse.

Interchange is not just a payments topic. It's a profitability topic. And if your store gets hit with fraud or friendly fraud, it becomes a dispute topic too.

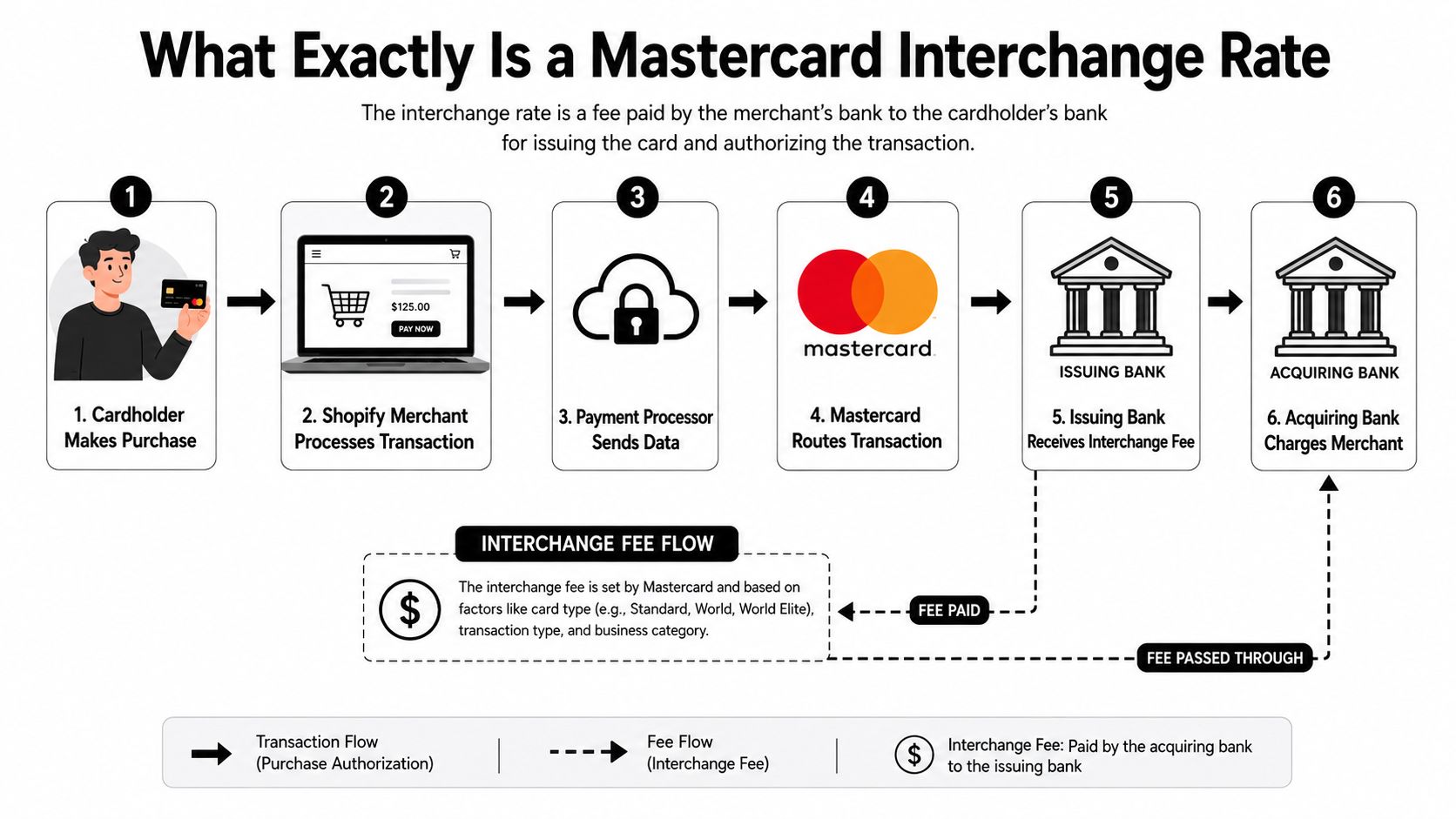

What Exactly Is a Mastercard Interchange Rate

A Mastercard interchange rate is the base card cost attached to a transaction. It is the fee that flows from the acquiring side of the payment to the issuing bank, then gets passed back to you inside your total processing cost. Mastercard's own merchant guidance defines interchange as a fee set within its network rules and paid by acquirers to issuers on purchase transactions (Mastercard merchant interchange guidance).

For a Shopify merchant, that matters for one reason. Interchange is not just a back-end banking fee. It directly changes what each order is worth after payment costs, and higher-risk transactions can push you into worse economics before a dispute even hits.

Who does what in the transaction

The roles are simple once you strip out the jargon.

- Issuing bank: The customer's bank. It issued the Mastercard and approves or declines the purchase.

- Acquiring bank: Your side of the transaction. It works with your processor to accept the payment and settle funds to your business.

If you want a plain-English breakdown of those roles, read this guide on acquirer vs issuer. This article with essential insights on card issuers for businesses is also useful if you want the issuer side explained clearly.

Why there is no single Mastercard rate

Shopify store owners often ask for “the Mastercard interchange rate” as if one number applies to every order. That is the wrong mental model.

Mastercard interchange is a rate schedule, not a flat fee. The final rate depends on the card type, the transaction setup, the merchant category, and the quality of data sent with the payment. Two orders can run through the same checkout on the same day and still price differently.

That difference matters more than it seems. Transactions that look riskier to the network or to the issuer often cost more to process. Those same transactions are also more likely to turn into disputes, fraud claims, or chargebacks later. That means bad payment setup can hit your margin twice. First through higher interchange or qualification problems, then through dispute fees, lost revenue, and fulfillment losses.

For Shopify merchants, this shows up in familiar places. Subscription rebills with weak stored credential setup. Orders with incomplete billing data. Cross-border transactions with thin customer verification. Manual workarounds after failed payments. Those are not just operations issues. They raise the odds of both fee leakage and chargeback exposure.

A Mastercard interchange rate is one part pricing rule, one part risk signal. If your transaction data is weak, your processing cost can rise before the chargeback arrives.

The Key Factors That Determine Your Rates

Your Mastercard cost on Shopify is set long before you see the payout.

It starts with who is buying, how the order is processed, and how your business is coded by the processor. Get those inputs wrong and you do not just pay more interchange. You also raise the odds of fraud reviews, friendly fraud, and chargebacks that turn an expensive order into a lost one.

Card product sets the baseline

The card itself is the first pricing signal. Consumer debit usually lands lower than consumer credit. Premium rewards cards and commercial cards usually cost more. If your store attracts corporate buyers, affluent shoppers, or gift-heavy seasonal traffic, your average cost per order can climb fast even when sales look healthy.

That matters for margin planning. A store with a higher share of premium cards cannot judge payment cost the same way a low-ticket essentials brand does.

How the payment is submitted changes the rate

Interchange also depends on the transaction path. Clean e-commerce authorizations with strong customer and billing data tend to qualify better than manual entries, exception processing, or messy retry behavior.

For Shopify merchants, this is a payments operations issue, not just a checkout issue.

- Stored credentials need to be set up correctly: Subscription rebills and repeat purchases can price worse if the original consent and transaction indicators are weak.

- Manual fixes create expensive exceptions: Keyed adjustments, offline captures, and staff workarounds often increase cost and increase dispute risk later.

- Authentication quality affects both fees and chargebacks: Better billing details and verification help issuers trust the transaction. That can improve qualification and make disputes easier to defend.

Cross-border orders make this harder. International traffic changes your card mix, increases issuer caution, and creates more points of failure in billing, currency, and customer verification. If that is a growing part of your business, read this guide to cross-border e-commerce for Shopify brands.

Your MCC can quietly raise or lower every order

Your merchant category code, or MCC, is one of the biggest pricing levers merchants ignore. Mastercard assigns different interchange treatment by merchant type, so a bad classification can hurt every transaction you process.

Stores often face this pitfall. A processor may place you in a category that is too broad, outdated, or incorrect for how you sell today. If your product mix changed, if you added subscriptions, or if your brand sits between retail and services, your setup deserves a review.

Use this checklist with your payment provider:

| Factor | Why it changes cost | What Shopify merchants should check |

|---|---|---|

| Card product | Premium and commercial cards usually cost more | Your customer card mix |

| Transaction method | Exception handling and weak transaction data can qualify worse | Checkout flow, retries, stored credentials |

| MCC | Merchant classification can shift your pricing treatment | Processor setup and merchant classification |

Merchant advice: Ask your processor to confirm your MCC in writing and explain why it fits your current business model. If they cannot answer clearly, keep pushing.

Small misses become expensive fast

A few basis points across thousands of Shopify orders is real margin loss. Add a higher dispute rate on top and the problem gets worse. You pay more to process the sale, then pay again when the issuer reverses it and your processor adds a chargeback fee.

Treat interchange review and chargeback prevention as the same profit-protection job. That is the hidden link many merchants miss.

Real Examples of Mastercard Interchange Rates in 2026

Your Shopify store can have a healthy conversion rate and still lose margin on the back end. A customer checks out with a premium Mastercard, the order later turns into a dispute, and now you have three costs tied to one sale. Interchange, processor markup, and a chargeback fee. That is why rate examples matter. They show which orders carry more hidden risk before the dispute ever lands.

Mastercard's published U.S. schedules make one point clear. The expensive part is rarely “accepting Mastercard” by itself. The expensive part is the type of Mastercard used, the transaction category, and whether that sale later becomes a refund or chargeback problem. Mastercard also said it would reduce published and effective U.S. credit card interchange rates for at least five years for certain U.S.-issued consumer and commercial credit transactions at U.S. merchant locations in its settlement announcement. You still need to check the actual schedule because “lower” does not mean “cheap” across your mix.

2026 Mastercard interchange rate examples

Using Mastercard's U.S. merchant schedule examples, here is the kind of spread a Shopify merchant can run into across common categories (Mastercard U.S. merchant interchange rates):

| Card Type | Transaction Scenario | Typical Interchange Rate |

|---|---|---|

| Consumer credit core card | U.S. credit example | 1.58% + $0.10 |

| Consumer credit World Elite | U.S. credit example | 2.30% + $0.10 |

| Commercial credit | U.S. credit example | 2.90% + $0.10 |

| Service Industry category | U.S. merchant schedule category example | 1.15% + $0.05 |

That gap is your margin at work.

A $200 order paid with a core consumer card costs far less in interchange than the same $200 order paid with a commercial card. If that higher-cost order also turns into a chargeback, you lose the revenue, eat the fee stack, and spend time fighting the dispute. Premium and commercial card volume often shows up in higher-ticket orders, which makes the downside bigger when fraud screening and order review are weak.

Why many Shopify merchants did not feel any savings

Store owners heard about lower published rates and expected payouts to improve. Many saw no meaningful change because their real cost sits inside a blended average.

Here is what usually explains it:

- Card mix got worse: More World, World Elite, and commercial cards can erase any reduction on lower-cost consumer transactions.

- Dispute-prone orders stayed expensive: Fraud-heavy orders are costly on the front end and even worse after a chargeback.

- Processor pricing still controls the final bill: Interchange can move down while markup, monthly fees, or cross-border costs keep total acceptance costs high.

For Shopify brands, the fix is operational. Pull a payment report by card type, AOV, and dispute rate. Then compare it against your processor setup. If you have not reviewed Shopify payment processors and fee structures, do that before you assume interchange is the whole problem.

One more point. The orders with the highest interchange are often the same orders you should review hardest for fraud and fulfillment risk. That is the hidden link many guides skip. If a transaction is expensive to accept and more likely to be disputed, you need tighter address checks, cleaner order data, and better post-purchase evidence on that slice of volume first.

How Shopify Merchants Can Reduce Interchange Costs

You can't eliminate interchange, but you can stop making it worse. This calls for disciplined operations, not wishful thinking.

Clean up the transactions you already have

Most savings come from qualification, not magic negotiation.

- Audit your MCC first: If your business is in the wrong category, every other optimization starts from a bad base.

- Review recurring billing setup: Make sure subscriptions, renewals, and card-on-file transactions are configured correctly so they don't fall into expensive exception handling.

- Reduce manual fixes: Every hand-edited billing flow increases the chance of a downgraded transaction and weaker evidence later.

Mastercard's schedules are granular enough that small category differences matter. In Canada's April 2026 schedule, for example, Digital Commerce appears at 1.60% in the core column while Base is 1.65%, which shows how small qualification differences can affect cost at scale (Mastercard Canada interchange schedule April 2026).

Tighten fraud controls because it helps twice

Merchants usually miss the bigger win at this point.

Better fraud prevention doesn't just reduce bad orders. It also improves the quality of the transaction record. Stronger customer verification, better AVS and billing accuracy, cleaner device and order data, and fewer forced retries all make the payment look more legitimate to the bank that has to approve it and later judge it in a dispute.

Use tools you already have before adding complexity:

- Shopify Fraud Analysis: Review patterns, not just individual flags.

- 3D Secure where supported: Use it selectively where risk justifies friction.

- Address and billing consistency checks: These are simple, and they matter.

Push your processor on the right questions

Most merchants ask for a lower rate. That's too vague. Ask operational questions instead.

- Which transactions are downgrading: Get examples, not generalities.

- What data fields are missing: If you do B2B or wholesale, ask whether richer transaction data could improve qualification.

- Where do retries happen: Failed payment loops create costs and confusion.

If you're still comparing provider economics, this guide on Shopify payment processors helps frame what to review beyond headline pricing.

Stores lower effective cost when finance, ops, and fraud review the same payment data together. Looking at fees alone is too narrow.

Build a monthly review habit

Don't leave payment costs buried inside bookkeeping.

Create a short monthly review that checks:

- Card mix changes

- Chargeback reasons

- Authorization failures

- Refund volume

- Processor statement anomalies

That review won't just lower acceptance cost. It will surface the exact payment behaviors that later show up as disputes.

The Hidden Transaction Fees Beyond Interchange

A lot of fee guides stop at interchange. That's incomplete.

Your total card acceptance cost also includes network fees tied to what occurs during transaction processing. If your store has failed captures, odd retry patterns, delayed workflows, or exception processing, you can get charged in ways that have nothing to do with the published interchange percentage.

The fee most merchants won't notice until it adds up

In April 2026, Mastercard introduced a Force Post Transaction Fee of nine cents per transaction in the U.S. region, alongside other fee updates (April interchange and network fee updates).

That's the warning sign. Network costs now punish messy operations more directly.

If your store or payment stack relies on after-the-fact fixes, forced postings, repeated authorization attempts, or error-prone capture flows, you need to care about more than the Mastercard interchange rate.

What Shopify merchants should do about it

Here's the practical playbook:

- Track failed payment workflows: Don't let subscription retries or inventory timing create sloppy authorization behavior.

- Review statement line items: Hidden fees usually sit in places merchants rarely read.

- Cut avoidable card volume where appropriate: For some use cases, bank payment alternatives may make more sense. If you're exploring that side, this guide to compare ACH solutions and fees gives useful context.

- Know your dispute-related fee exposure: A chargeback isn't just lost revenue. It often adds processing and administrative cost too. This explainer on what is a chargeback fee is worth keeping handy.

If your checkout flow creates payment exceptions, your processor statement will reflect it long before your P&L tells you why margin slipped.

Connecting Interchange Downgrades and Chargebacks

This is the link most merchants miss.

The same transaction problems that can push a payment into a worse-cost bucket can also weaken your position in a dispute. Missing billing data, weak customer verification, unclear stored credential logic, manual processing workarounds, and messy retry behavior all signal a less reliable transaction trail. Banks notice that.

Bad payment hygiene creates two losses

First, you pay more to process the order.

Then, if the customer files an unauthorized or fraud-related claim, you may have weaker evidence to fight back. That's why payment quality matters beyond fees. A transaction that looks sloppy on the front end often becomes hard to defend on the back end.

This is also why chargeback mitigation should sit next to payments ops, not in a separate silo. If your team treats disputes as only a support issue, you'll keep paying for the same mistakes twice. This guide on chargeback mitigation is a good place to tighten that process.

What to fix first

Focus on the basics that support both cost control and dispute defense:

- Make billing and shipping data cleaner

- Reduce manual transaction exceptions

- Use stronger authentication when order risk is high

- Document fulfillment clearly

- Review recurring transaction logic

You don't need a perfect system. You need a payment trail that holds up when an issuer reviews it.

Chargeback prevention and interchange management belong in the same conversation because they both come back to transaction quality. If the payment is cleaner, it usually costs less to accept and is easier to defend.

If chargebacks are still draining revenue after you've cleaned up payment operations, install ChargePay from the Shopify App Store. It's built for Shopify merchants, has a 4.9-star rating and a Built for Shopify badge, and fights disputes automatically with a 92.4% win rate, 200K+ cases handled, and $10.8M+ recovered for merchants. If you're tired of losing margin to both bad fees and bad disputes, this is the fastest way to stop the second leak.

.svg)

.svg)

.svg)

.svg)