You know the email.

A chargeback notification lands in your inbox. You open it, see the order number, recognize the product, and immediately know what comes next. Lost revenue, wasted time, and another round of digging through order details, shipping confirmations, and customer messages to defend a sale you already fulfilled.

For Shopify merchants, fraud rarely shows up as a neat technical problem. It shows up as operational drag. You lose the product, the payment, the time, and often the next hour you should've spent on inventory, ads, or retention. That's why real time fraud detection matters. Not because it sounds advanced, but because delayed detection turns preventable fraud into an expensive chargeback fight.

Why Fraud Is Costing Your Store More Than Just the Sale

The first mistake merchants make is treating fraud like a one-order problem.

It isn't. One bad order can trigger a chain reaction. You ship inventory you won't get back. You lose the original payment. You pay dispute fees. Your team spends time gathering evidence. If too many disputes pile up, your payment setup gets more fragile and your store operations get more stressful.

The scale of the problem got worse fast. Fraud losses reported to the Federal Trade Commission rose from $5.6 billion in 2021 to $8.8 billion in 2022, after a 30% year-over-year increase and a prior 70% increase from 2020 to 2021, according to Materialize's summary of FTC fraud loss data. That's not random bad luck. That's a market-wide warning that old review processes aren't keeping up.

Practical rule: If your fraud process starts after the order is approved, you're already late.

The hidden losses merchants ignore

Most Shopify operators can spot the obvious damage. The less obvious damage is what drains margin over time:

- Manual review time that pulls founders or ops staff into detective work.

- Fulfillment mistakes when suspicious orders slip through during busy periods.

- Customer friction when your team starts overcorrecting and manually blocks good buyers.

- More chargeback work because weak detection upstream creates stronger disputes downstream.

This is why real time fraud detection needs to be tied directly to your chargeback process. If your fraud controls don't reduce dispute losses, they're incomplete.

A lot of merchants still rely on scattered rules, a few Shopify risk signals, and gut instinct. That might catch the obvious stuff. It won't reliably catch fast-moving fraud or friendly fraud. If you want a practical next step, start with a tighter ecommerce chargeback protection strategy for Shopify stores and treat fraud review as revenue protection, not just order screening.

What has changed

Fraud used to be something stores reviewed in batches. A team checked risky orders later, after patterns emerged.

That doesn't work anymore. Online fraud moves too fast, and Shopify stores approve orders too quickly, for delayed review to save you consistently. The merchants keeping more revenue are the ones making decisions while the transaction is still live.

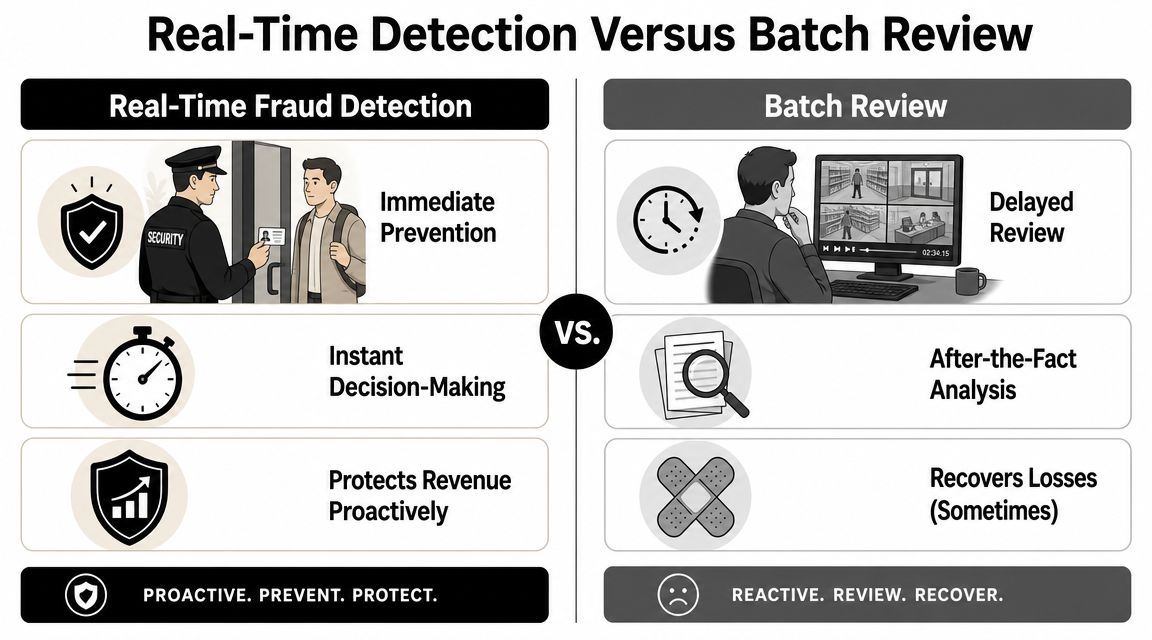

Real-Time Detection Versus Batch Review

Real time fraud detection is a security guard at the door. Batch review is someone watching the camera footage tomorrow morning.

That's the difference.

If your system reviews orders after they're processed, packed, or fulfilled, you're not preventing much. You're documenting losses. For Shopify stores, that distinction matters because a fraud review that happens too late still leaves you with the same chargeback headache.

What real time actually means

Modern fraud systems are built to make decisions in milliseconds, not hours or days. They watch live transaction activity, score risk immediately, and trigger action before the payment moves further through your process. A good overview of this shift also appears in this look at transaction monitoring solutions for modern fraud workflows.

Batch review does the opposite. It waits. Maybe it checks every hour. Perhaps daily. Maybe when someone on your team finally has time. By then, the order may already be authorized, fulfilled, or disputed.

Real-Time vs. Batch Fraud Analysis

| Feature | Real-Time Detection | Batch Review |

|---|---|---|

| Decision speed | Evaluates live orders immediately | Reviews activity later |

| Prevention ability | Can block, verify, or hold suspicious orders before fulfillment | Usually catches issues after the damage is done |

| Usefulness for chargebacks | Helps stop some disputes before they start and improves evidence quality | Often leaves you reacting after the sale is lost |

| Customer experience | Better when risk decisions are precise and fast | Can create delayed outreach and inconsistent handling |

| Team workload | Reduces manual review when automation is set correctly | Creates queues, exceptions, and cleanup work |

| Operational mindset | Preventive | Reactive |

A late fraud alert isn't protection. It's a postmortem.

Why Shopify merchants should care

Shopify stores live on speed. Fast checkout, fast fulfillment, fast customer service. Fraudsters like that. The faster your store runs, the easier it is for a stolen card order to look normal for just long enough to get through.

That's why batch review is a bad fit for most direct-to-consumer brands. It asks humans to catch what software should catch instantly. If you're doing volume, or even moderate volume during promotions, humans will miss things. They always do.

Real time fraud detection doesn't replace judgment. It puts judgment where it belongs. Before shipment, not after the dispute email.

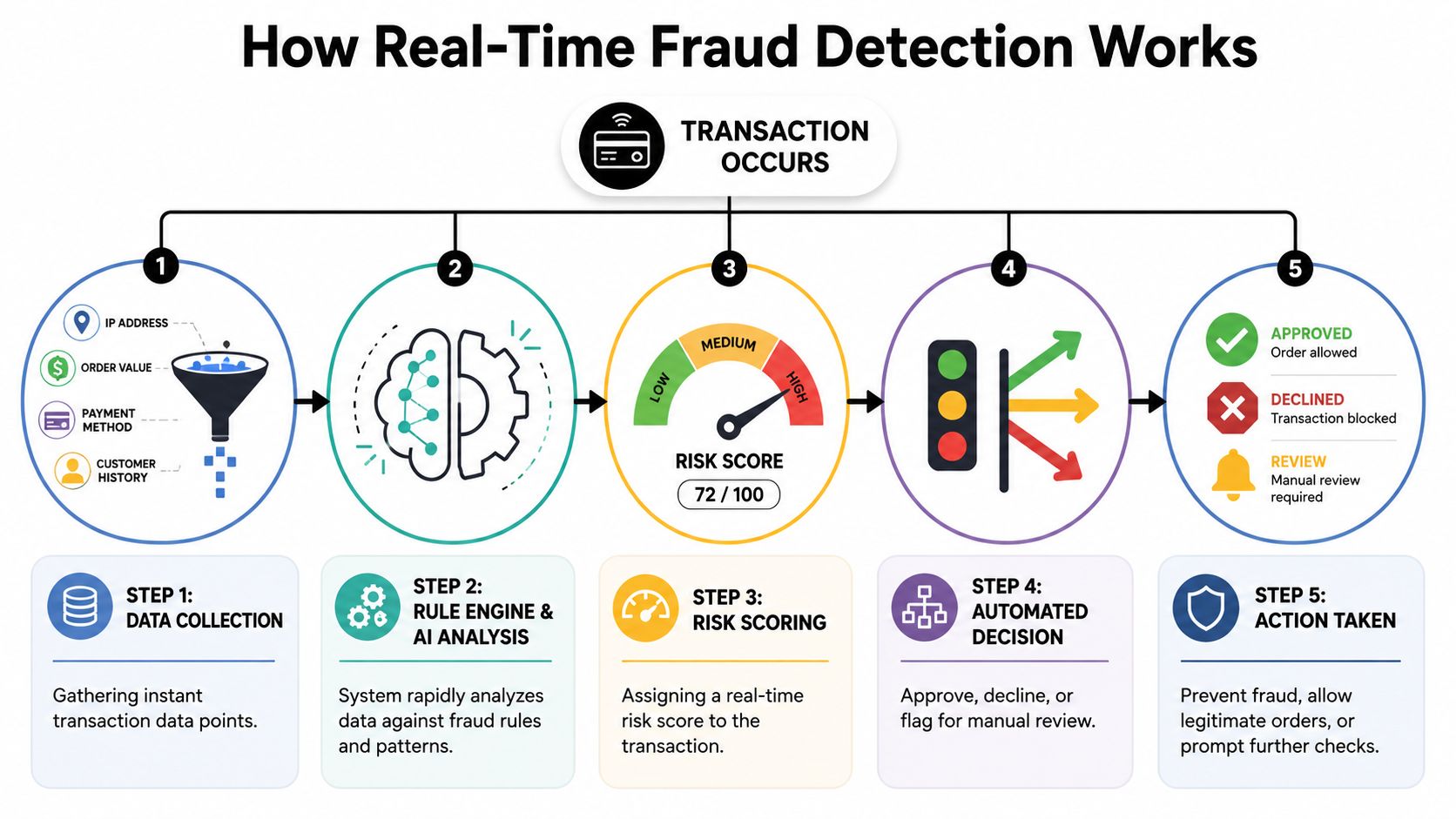

How Real-Time Fraud Detection Works

A stolen-card order hits your Shopify store at 2:07 p.m. By 2:08, it should be approved, blocked, or held. If your system cannot make that call before fulfillment starts, you are giving fraudsters a head start.

Real-time fraud detection is a decision engine. It pulls live order signals, compares them against rules and risk patterns, scores the order, and triggers the next action while the customer is still at checkout or the order is still fresh.

The signals that matter

Single checks fail. Fraudsters know how to pass a ZIP code check or use a clean-looking email address. What catches them is signal stacking.

For Shopify merchants, the useful signals usually include:

- Device intelligence to spot repeat devices tied to suspicious orders or account behavior

- Network data to add context about connection risk and location inconsistencies

- Digital footprint to judge whether the buyer identity looks established or thin

- Behavior patterns to catch rushed checkouts, scripted actions, or activity that does not match normal shopper behavior

- Store-specific history such as prior orders, refund patterns, shipping changes, and high-risk product combinations

That last point gets missed all the time. Generic fraud scores help, but Shopify merchants need store context. An order is not risky only because of the card or device. It can become risky because it matches the same patterns that led to your last chargeback. That is why your fraud controls should connect to your broader chargeback prevention strategy for Shopify stores, not sit in a separate tool that only spits out alerts.

What the system does with a live order

The flow is simple.

A customer submits an order. The system checks billing and shipping consistency, order velocity, customer history, device context, payment details, and checkout behavior. Then it assigns a risk score and routes the order into one of three buckets:

- Approve if the order looks normal

- Block if the risk is obvious

- Hold for review or verification if the order needs one more check

The mechanics are not mysterious. They are just fast. Teams that want a more technical reference can review how to build a Python intrusion detection system, which shows the same core idea. Watch events in real time, evaluate them against rules, and act before the problem spreads.

Good systems also watch for patterns across short time windows, not just one order at a time. A fraudster may place several small orders quickly, change shipping details across attempts, or test multiple cards before landing a bigger purchase. Those patterns matter because many bad orders look harmless in isolation.

Why this matters in plain English

You are trying to answer one question fast. Does this look like a customer buying, or a fraudster probing your checkout?

Real shoppers usually behave in consistent ways. Fraud attacks often create bursts, mismatches, retries, and awkward account behavior. Real-time detection catches that behavior while there is still time to stop the shipment, cancel the order, or add verification.

Here's a useful visual walkthrough of the same idea:

For Shopify merchants, the takeaway is straightforward. Stop obsessing over whether a vendor says “AI.” Focus on whether the system can read live Shopify order data, make a clear decision immediately, and hand clean evidence into your dispute workflow. That is how you reduce chargebacks instead of just logging them.

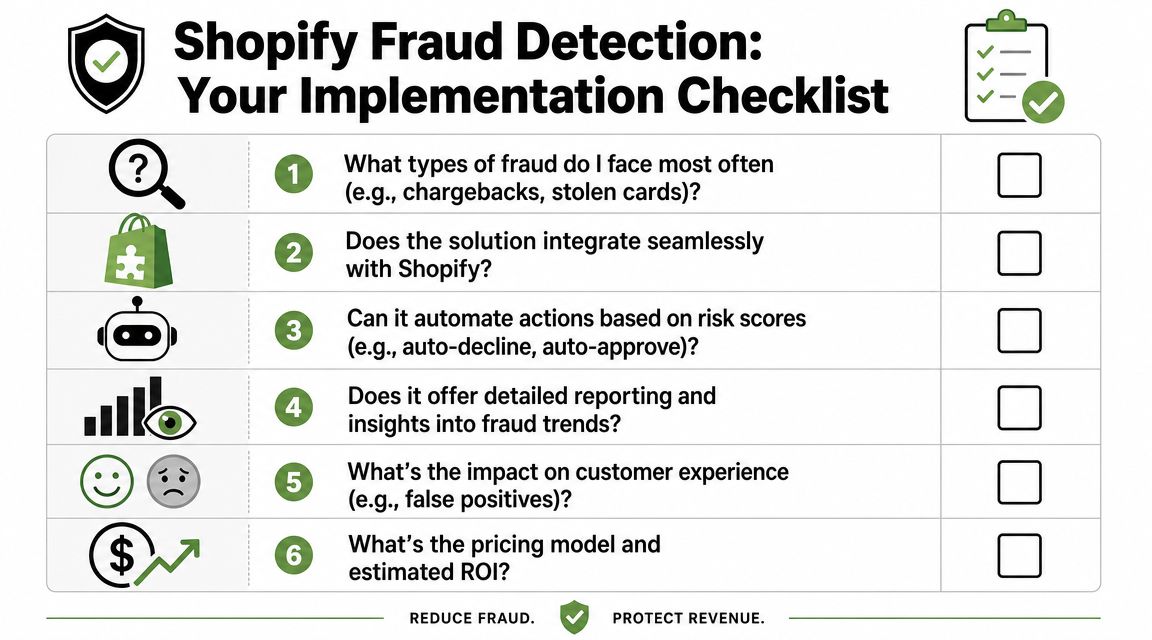

Your Implementation Checklist for Shopify

Most fraud tools sound good in a demo. Then you install them, get buried in alerts, and still lose chargebacks.

Use a checklist. If a vendor can't give you a clean answer to these questions, keep looking.

Start with workflow, not features

The first question isn't “Does this use AI?”

The first question is “What happens to an order after the tool says it's risky?” If the answer is “you get an email alert,” that's not enough. Alerts create work. Good systems reduce work.

You should also review your broader chargeback prevention approach for Shopify at the same time, because fraud screening and dispute handling need to work together.

The checklist

- Shopify integration

Ask how thoroughly it connects to Shopify. You want order data, customer history, fulfillment status, and payment context available without duct-taping multiple systems together.

Checkout impact

Ask whether the tool adds friction or delay to checkout. Fraud controls that slow down legitimate buyers can hurt conversion and still miss bad orders.

Decision options

Some stores need auto-decline for obvious risk. Others need hold-and-review logic for expensive items or first-time customers. If the tool only flags and never acts, it leaves your team holding the bag.

Signal quality

Ask what data the tool uses. Device, behavior, and transaction context matter more than one blunt rule like AVS mismatch or order value alone.

Manual review support

If an order gets flagged, can your team understand why quickly? A black-box score with no context wastes time and leads to bad decisions.

Evidence collection

This one gets missed all the time. If a disputed order comes back weeks later, can the system preserve the useful facts you'll need?

What a strong setup looks like

A practical Shopify stack should do four things well:

| Priority | What to look for |

|---|---|

| Fast decisioning | Risk scoring before fulfillment |

| Flexible actions | Approve, block, or review workflows |

| Clear audit trail | Order-level details your team can understand |

| Dispute readiness | Evidence preserved for later chargeback response |

What to ask your vendor: “When a high-risk order is flagged, what happens automatically, and what still lands on my team?”

One recommendation most stores need

Don't buy a fraud tool that stops at risk scoring.

For Shopify merchants, a useful setup usually includes detection, order action, and dispute support in one workflow. That can mean pairing your store's checkout controls with a platform such as ChargePay for the chargeback side, especially when friendly fraud slips through and you need the system to turn order data into a dispute response instead of another manual task.

If the software creates a longer to-do list, it's not solving the problem.

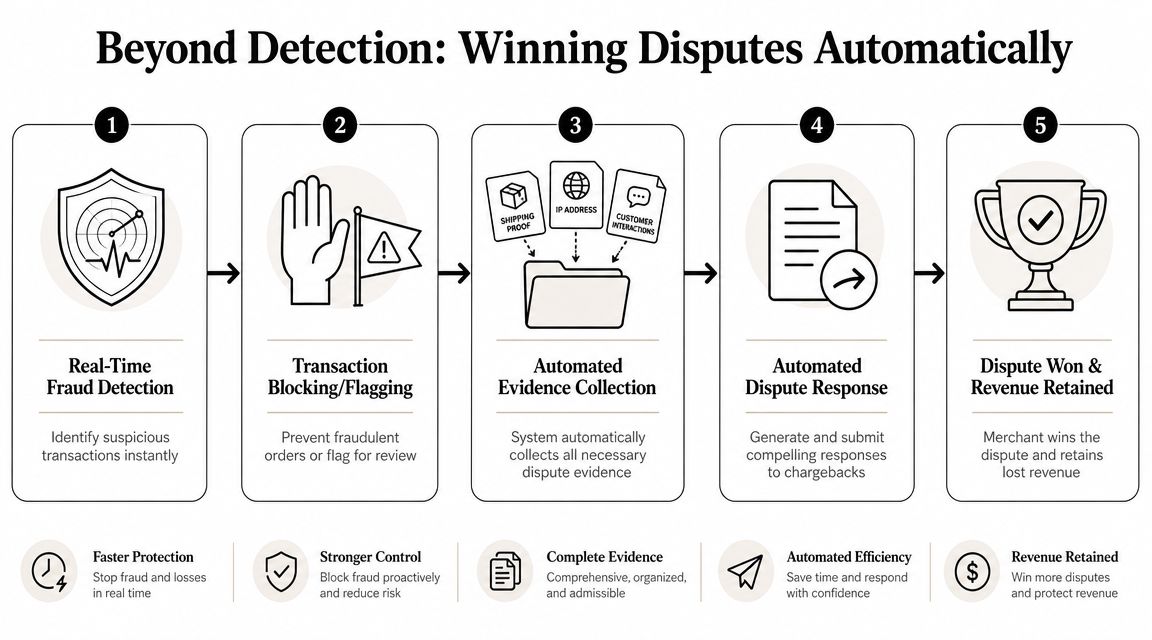

From Detection to Winning Disputes Automatically

A fraud alert doesn't recover money.

That's the part many merchants learn the hard way. You can detect a suspicious order perfectly and still lose the revenue if nobody blocks it, verifies it, or builds the dispute response later. Detection matters. But detection alone is unfinished work.

Detection is only half the job

Merchants often get sold the wrong thing. They buy software that flags risk, then assume the fraud problem is handled.

It isn't. As Confluent's explanation of real-time streaming for fraud prevention makes clear, real-time fraud detection is not the same as real-time fraud prevention. Flagging a suspicious payment is useless if you still lose the money. Value lies in blocking the payment immediately or using that detection data to build the evidence needed to fight the chargeback later.

What the closed loop should look like

A useful workflow looks like this:

- The system detects suspicious behavior early.

- It triggers an action, such as blocking, pausing, or escalating the order.

- It stores the right evidence while the details are fresh.

- If a dispute appears later, the response is generated and submitted without your team rebuilding the story from scratch.

That's the gap a lot of merchants need to fix. Real-time signals shouldn't disappear after checkout. They should flow into your dispute operation.

Why this matters for friendly fraud

Not every chargeback comes from obvious card theft. Some come from buyers who received the product, recognize the charge, and still dispute it.

That's why detection data matters even after an order ships. If you can connect transaction behavior, customer history, fulfillment proof, and order context into one evidence package, your dispute response gets much stronger. A deeper breakdown of that workflow appears in this guide to automated chargeback and dispute management using AI.

Good fraud operations don't stop at “this looks risky.” They answer “what action happens next, and who gets the money back?”

For Shopify stores, this is the operational standard to aim for. Detection should feed prevention when possible, and dispute automation when prevention comes too late.

Measuring Success and Tuning Your System

If you can't tell whether your fraud setup is blocking bad orders or blocking good customers, you're guessing.

That's why tuning matters. Real time fraud detection isn't a one-time install. It's an operating system for decision-making, and it gets better when you feed it better signals and review the outcomes objectively.

The two outcomes you need to watch

Start with a simple question after every policy change or tool update.

Are you stopping more fraud without creating more customer damage?

That boils down to two practical checks:

- False positives are legitimate customers you accidentally block, delay, or challenge.

- Chargeback performance tells you whether suspicious orders are still turning into lost disputes and revenue leakage.

If your store starts declining good buyers, your fraud controls are too blunt. If you approve too much risky traffic, you'll feel it later in disputes and support tickets.

Data quality changes the outcome

Many stores often get lazy. They rely on weak signals and then wonder why their decisions are inconsistent.

The quality of your data directly affects accuracy. One analysis summarized by Unit21's discussion of precision in fraud data points found 95.21% true positive rates for phone-number matches and 85.02% for physical-address matches. The point isn't that one field solves fraud. The point is that stable, identity-linked data beats vague heuristics.

What tuning looks like in practice

You don't need a data science team to tune a Shopify fraud workflow. You need discipline.

- Review blocked orders and check whether good customers are getting caught for the wrong reasons.

- Look at disputed orders and ask what signals were visible at checkout but ignored.

- Prioritize stronger fields such as confirmed phone and address data when available.

- Trim noisy rules that generate work without improving outcomes.

Better fraud decisions usually come from better inputs, not more complicated dashboards.

The stores that improve fastest are the ones that treat fraud review like margin optimization. They don't chase perfect detection. They reduce preventable losses while keeping checkout usable for real customers.

Stop Fighting Fraud and Start Winning Disputes

A Shopify order clears, your team ships it, and two weeks later the chargeback hits. You lose the product, the revenue, the fulfillment cost, and more staff time cleaning up a mess that should have been stopped or documented at checkout.

That is why fraud strategy cannot end at detection.

Real time fraud detection only pays off when it drives the next action fast. Approve the right orders. Stop the obvious bad ones. Hold the risky edge cases before they become shipments, chargebacks, and support headaches. Then keep the order data, customer details, and transaction history organized so your team is not rebuilding evidence from scratch after the dispute arrives.

For Shopify merchants, the mistake is buying a fraud tool that stops at alerts. Alerts do not recover money. A useful setup connects checkout risk decisions to post-purchase evidence and dispute workflows. If you need a clearer view of that process, read this guide to chargeback representment for e-commerce merchants.

The mistake to avoid

Do not turn your team into a manual review department.

If your app flags an order and then waits for someone to investigate, collect screenshots, write a response, and submit the case, you still have an operations problem. You just paid for one more screen to monitor. Shopify stores need a system that acts on risk and carries the paperwork forward when fraud slips through.

The standard to aim for

A good Shopify setup does four things well:

- Screens orders before fulfillment so bad transactions do not turn into shipped losses

- Applies clear next steps so risky orders are canceled, held, or reviewed without confusion

- Stores the right evidence automatically so disputes are supported by actual order data

- Handles chargebacks with automation so your team is not buried in repetitive admin work

ChargePay fits that operating model for Shopify merchants. It focuses on connecting fraud signals, evidence capture, and automated dispute handling instead of leaving store teams to piece the process together manually. The pay-per-win model also keeps the cost tied to recovered revenue, which is how this should be judged in the first place.

Stop treating fraud as a stream of alerts. Treat it like margin protection. Detect risk early, keep the evidence, and automate the dispute work so more chargebacks turn back into revenue.

.svg)

.svg)

.svg)

.svg)