If you're selling on Shopify, third party fraud isn't some abstract banking problem. It's a direct hit to your cash flow, your ops team, and your chargeback rate.

We've handled 100K+ disputes and recovered $2.8M+ for merchants. The pattern is painfully familiar. A fraudster gets access to stolen identity data or a customer account, places what looks like a normal order, receives the goods, and then your store gets stuck with the chargeback. You lose the product, the revenue, the shipping cost, and your time.

The threat is getting worse. Account takeover fraud, a classic third-party fraud pattern, caused nearly one-third of reported fraud losses for U.S. businesses and grew 141% from H1 2021 to H1 2025, according to the 2025 TransUnion Global Fraud Report. If you're still treating fraud like a simple stolen-card problem, you're behind.

Most Shopify merchants don't need more theory. They need a plan that stops bad orders before fulfillment and helps them fight the disputes that still get through. That's what this guide is for.

Your Store Is a Target for Third-Party Fraud

Third party fraud usually starts long before the order hits your Shopify admin. The criminal already has stolen credentials, breached personal data, or access to a real customer's account. By the time they buy from your store, the attack is already in motion.

Why Shopify merchants get hit so often

Shopify stores are attractive because they're fast to check out, easy to automate against, and often full of high-resale inventory. Fraudsters don't need to break your store directly. They just need a weak point somewhere in the customer journey.

That could be a reused password from another breach. It could be a phishing attack against your customer. It could be a compromised app, support tool, or vendor in your stack.

Practical rule: If your fraud controls only look at the payment itself, you're missing the part of the attack that matters most.

A fraudulent order rarely looks dramatic. It often looks normal enough to pass quick manual review. That's why merchants keep shipping these orders and only realize what happened when the dispute notification arrives days or weeks later.

This is beatable if you treat it like a system problem

You don't fix third party fraud with a single app setting. You fix it by tightening account security, reviewing orders with context, and building a clean dispute workflow for the orders that still slip through.

If you want the broader prevention playbook, our guide to ecommerce fraud prevention for Shopify merchants covers the full stack. For this article, stay focused on one thing: how third party fraud turns into chargebacks, and exactly what to do about it.

What Third-Party Fraud Really Is (And Is Not)

Third party fraud means the legitimate customer did not place or approve the order. Someone else used that customer's card, account, identity details, or a mix of stolen information to get through checkout.

For Shopify merchants, that distinction matters because it changes how you respond to the chargeback. Across more than 100,000 disputes, we keep seeing the same mistake. Merchants call every disputed order "fraud," then submit the wrong evidence and lose cases they could have handled better.

What it includes

On Shopify, third party fraud usually shows up in four forms:

- Stolen card use: A fraudster checks out with card details taken through phishing, skimming, breaches, or malware.

- Account takeover: They access a real customer account and use saved cards, stored addresses, Shop Pay details, loyalty balances, or the customer's order history to look legitimate.

- Synthetic identity abuse: They combine real and fake identity details to pass basic screening and place an order that looks clean enough to ship.

- Application-style abuse: They use stolen or fabricated information to create accounts, apply for financing, or pass identity checks tied to higher-risk purchases.

If your store relies on basic payment approval alone, you will miss a lot of this. Card authorization only tells you the payment credential worked. It does not confirm the actual cardholder or account owner was behind the order. That is why many Shopify merchants add fraud filter apps for Shopify stores and still get hit with fraud chargebacks. The tool itself matters less than whether you are reviewing the right signals.

What it is not

Third party fraud is different from friendly fraud.

Friendly fraud happens when the customer, or someone in their household, made the purchase and later disputes it. The order may be valid. The claim is what breaks.

That difference should control your dispute strategy from day one. In a third party fraud case, the issuer is focused on unauthorized use. Your records need to show what happened at checkout, what account activity changed before purchase, and whether the order matched normal customer behavior. In a friendly fraud case, you are usually proving recognition, delivery, and post-purchase use.

If the true cardholder never approved the order, focus on account access, checkout signals, and identity inconsistencies. If the cardholder did approve it and later disputed, focus on recognition, fulfillment, and prior customer behavior.

A short explainer on that distinction is worth watching before you build your dispute workflow:

Why merchants mislabel this

Shopify merchants usually mislabel third party fraud for one reason. They start with the chargeback reason code and stop there.

That costs real money. If you treat an unauthorized transaction like a fulfillment dispute, you send tracking and delivery proof when the issuer wants login history, device data, AVS and CVV results, account changes, and order context. If you treat friendly fraud like third party fraud, you miss the customer recognition evidence that wins.

Use this quick filter before you build your response:

| Situation | Likely category | What matters most |

|---|---|---|

| Saved card used on an existing account after login changes | Third party fraud | Login history, device change, address change |

| New order from a cardholder who denies knowing your brand | Third party fraud | AVS, CVV, IP, shipment details |

| Repeat customer claims "I didn't get it" despite delivery | Often not third party fraud | Delivery proof, prior history, product use evidence |

Classify the case correctly first. Then build the dispute response around that reality. That one change will improve your recovery rate faster than adding another generic fraud setting.

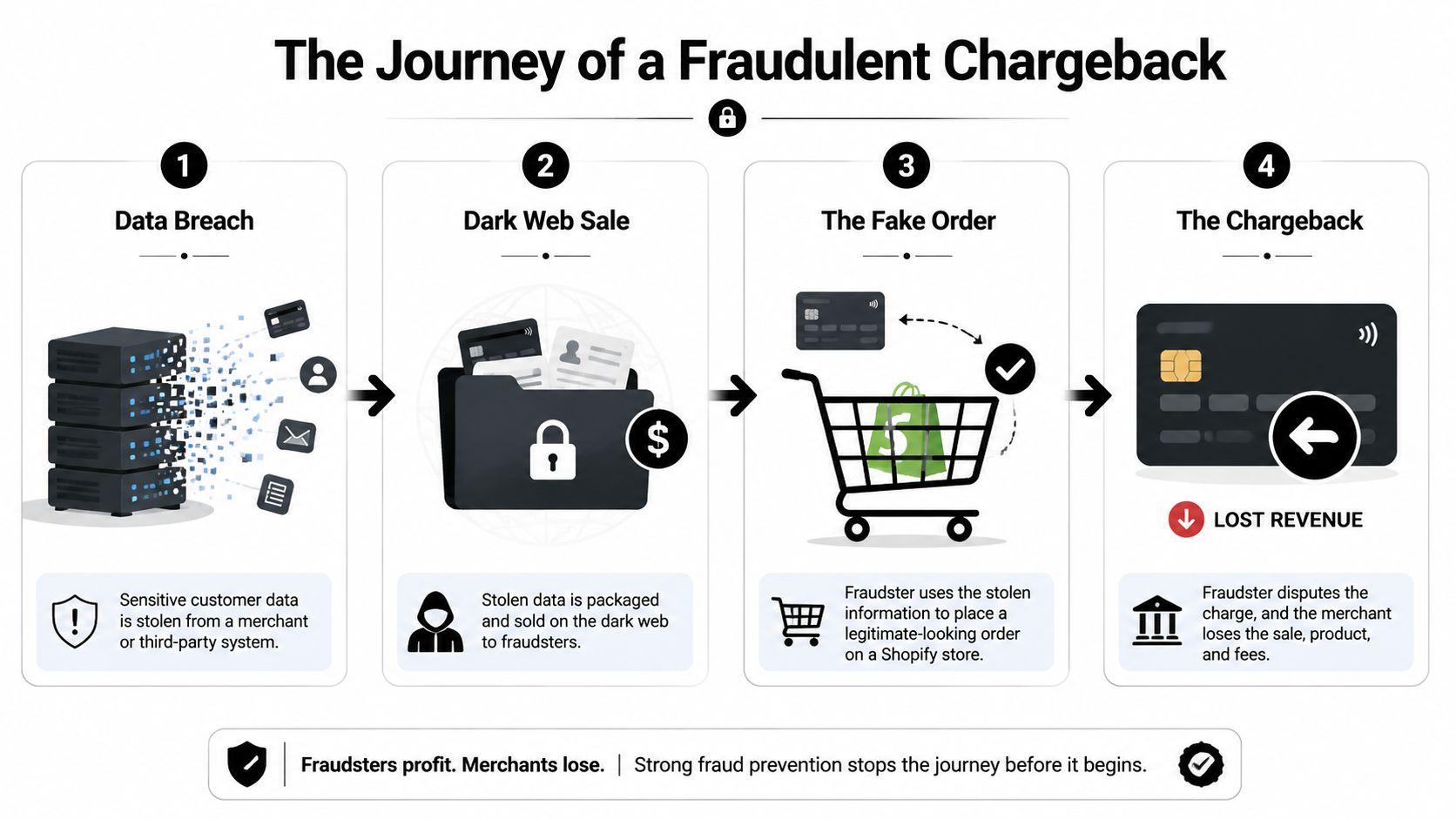

How Fraudsters Turn Stolen Data Into Chargebacks

Most chargebacks tied to third party fraud start upstream. The order on your store is just the final move.

In 2024, 35.5% of all breaches were third-party related, up from 29% in 2023, and SecurityScorecard counted 355 third-party breach cases in its 2025 Global Third-Party Breach Report. For a Shopify merchant, that means a weak vendor, app, processor integration, or service provider can become the entry point.

The usual attack chain

A typical attack looks like this:

Data gets exposed

Credentials or identity data are stolen through a breach, phishing campaign, malware, or credential stuffing attack.The fraudster tests what still works

They try logins on retail sites, email accounts, payment wallets, and customer accounts. Reused passwords make this much easier.They place an order that blends in

They don't always go for the biggest basket. Smart fraudsters choose products that resell fast and won't trigger obvious review.They redirect or conceal fulfillment clues

They may ship to a freight forwarder, a new address, or an address tied to a mule. Sometimes they use a real customer's account so the order history makes the purchase look normal.The cardholder notices later

The bank receives a fraud complaint. Then the chargeback lands on your desk.

Why these orders fool merchants

Fraudsters know what your team checks first. They know merchants look for messy addresses, odd email domains, and giant order values. So they adjust.

They'll use clean-looking emails. They'll copy a normal shipping format. They'll buy just enough to make the order worth it, but not enough to look ridiculous.

That matters even more in card-not-present commerce, where you never see the buyer face to face. If you need a refresher on that risk model, read our breakdown of card-not-present fraud in ecommerce.

The dangerous order isn't the one that looks obviously fake. It's the one that looks almost normal.

Why the chargeback comes last

By the time the issuer labels the transaction as fraud, your store has already absorbed most of the damage. The goods are gone. The payout may have settled. Your support team may have already dealt with the confused real customer.

That delay is why prevention and dispute handling have to work together. If those teams or tools are disconnected, you keep losing the same type of order twice. First in fulfillment, then again in the dispute.

Red Flags You Can Spot Before Shipping an Order

You don't need perfect fraud detection to cut losses. You need a reliable hold-or-ship process for suspicious orders.

A lot of bad orders announce themselves if you slow down for five minutes and look at the right signals inside Shopify.

Signals inside the order

Start with the basic mismatches:

- Billing and shipping don't line up: That doesn't always mean fraud, but it should slow you down. Fraudsters often don't control the legitimate cardholder's home address, so they route goods somewhere else.

- IP location clashes with the order story: If the cardholder is supposedly local but the login or order behavior points somewhere else entirely, review it.

- Multiple payment attempts before success: Fraudsters test cards and retry. Real buyers usually don't fail several times and then suddenly get everything right.

- New customer, expensive basket, rush shipping: That's a classic risk bundle. The urgency is the point. They want the package moving before anyone notices.

Signals inside the customer account

These are often stronger than the order itself:

- Shipping address changed right before purchase

- Password reset followed by a fast checkout

- Stored card used after a long period of inactivity

- Unusual product mix compared with past orders

Those are account takeover fingerprints. The fraudster isn't just buying. They're using a trusted customer profile to lower your guard.

If you're using Shopify apps or rules to score orders, tune them around those behaviors. This guide to choosing a fraud filter app for Shopify can help you tighten those rules.

Hold any order where the account behavior changed more than the basket did.

What to do when you see a red flag

Don't default to canceling everything suspicious. That creates support pain and blocks good customers.

Use a simple review path:

| Red flag level | Action |

|---|---|

| Minor mismatch with otherwise clean signals | Send to manual review |

| Account changes plus order anomalies | Put on hold and verify |

| Multiple high-risk signals together | Cancel or require stronger verification |

For manual review, check whether the customer responds coherently, whether the shipping destination makes sense, and whether the timeline matches normal buying behavior. A fraudster can fake some fields. They usually can't fake the full story for long.

Building Your Fraud Prevention Toolkit

Across more than 100,000 disputes, one pattern keeps showing up. Shopify merchants lose the most money when they treat fraud prevention and chargeback response as separate jobs.

Basic checks like AVS, CVV, and Shopify's default fraud signals are a starting point. They are not a system. A fraudster with full card data or access to a real customer account can pass static checks and still leave you holding the chargeback.

The fix is simple. Build your fraud stack around two goals at the same time: stop bad orders before fulfillment, and preserve the evidence you will need if the issuer dispute arrives anyway.

What each layer does well

Use a layered setup because each control catches a different failure point.

| Tool | Good for | Weak spot |

|---|---|---|

| AVS and CVV | Catching low-effort stolen card use | Weak when the fraudster has complete card details |

| Manual review | Adding human judgment on unclear orders | Slow, inconsistent, and expensive at volume |

| 3D Secure | Pushing authentication to the issuer | Adds checkout friction and does not stop every fraud claim |

| Device intelligence | Flagging risky devices, proxies, and repeat abuse | Needs clean rules or you will block good customers |

| Behavioral analytics | Finding suspicious session patterns and account misuse | Works best when tied to enough checkout and account data |

| MFA and step-up verification | Protecting accounts and high-risk transactions | Hurts conversion if triggered too often |

The setup I recommend for Shopify merchants

Set up your controls in this order.

First, protect the customer account. Tighten login security, watch for account edits before checkout, and log every change that could matter in a dispute. If a chargeback hits later, that account history can help explain why the order looked legitimate at the time.

Next, score more than the payment fields. Use device signals, session behavior, account age, order velocity, and profile change events. Shopify merchants who only review AVS and CVV are giving fraudsters a very easy test to pass.

Then add step-up verification only for risk spikes. Reserve extra checks for orders with clear warning signs. That protects conversion while giving you a stronger record to submit if the cardholder later claims unauthorized use.

Last, connect fraud decisions to your dispute workflow. Every canceled order, approved review, and fraud chargeback should feed back into your rules. If your prevention system never learns from dispute outcomes, it stays expensive and mediocre.

If you want that loop in one place, read this guide to automated chargeback and dispute management using AI. The point is not automation for its own sake. The point is faster evidence collection, cleaner case files, and better rule updates after each loss or win.

Your vendor stack matters too

Fraud risk also shows up in your operations. If your team copies order details between inboxes, spreadsheets, forms, and review tools, you create delays and lose evidence quality. That hurts prevention and it hurts representment.

Clean up the handoff. Tools like DigiParser integrations can help route structured order or document data into fraud review workflows without manual copy and paste.

ChargePay is one practical example in the Shopify ecosystem. It connects chargeback handling to fraud operations so signals from disputes can improve future order decisions. That is how you reduce losses over time. You do not just block more fraud. You also build stronger cases for the transactions you approve.

Your Game Plan When a Fraud Chargeback Hits

When a fraud chargeback lands, speed matters. But evidence quality matters more.

A weak response packed with screenshots and random notes won't move the issuer. A focused response that shows why the transaction looked legitimate at the time of purchase gives you a real shot.

What to gather first

Build around objective records:

- AVS and CVV results: Show whether the payment details passed the checks you had in place.

- Order timeline: Include timestamps for account login, checkout, payment, and any profile edits.

- IP and device context: If the session behavior matched the customer's normal pattern, include that. If you have device recognition or session risk tools, use them.

- Delivery proof: Tracking, delivery confirmation, and the destination address matter.

- Customer history: Prior successful orders, unchanged buying patterns, or earlier deliveries can help.

If the customer account was involved, include evidence of prior legitimate usage. If the transaction came from a brand new account, focus harder on checkout verification and fulfillment details.

What banks need to understand

Your job isn't to say "we don't think this was fraud." Your job is to show that the transaction passed reasonable controls and matched a believable customer pattern at the time.

That standard is getting tougher because fraudsters are getting better. Alloy points out that generative AI is helping criminals create more believable fake identity information and bypass attempts, which is why stronger dynamic controls like behavioral analytics and device intelligence are now recommended in its discussion of AI-enhanced third-party fraud defenses.

If your evidence only proves the card was charged, you'll lose. If your evidence proves the order fit a legitimate customer pattern, your odds improve.

How to structure the response

Keep it tight:

Start with the order summary

Product, amount, order date, customer account context.List the verification signals

Payment checks, account status, login or session consistency, shipping logic.Add fulfillment proof

Tracking, carrier confirmation, destination details.Attach supporting records

Keep them organized and labeled.

If you're still writing these manually, use a repeatable workflow. Our guide to chargeback representment for Shopify merchants gives you the structure.

Win More Disputes With AI and Automation

Manual dispute handling breaks down fast. Deadlines pile up. Evidence sits in different systems. Your team writes inconsistent responses. That's how good cases get lost.

This is exactly where automation earns its keep. Recorded Future notes that 30% of breaches involved a third-party vendor in 2024 and argues that continuous monitoring matters because periodic reviews miss real-time compromise. That's a useful reminder from its write-up on third-party risk statistics and continuous monitoring. Fraud moves fast. Your response system has to move faster.

What good automation should actually do

Look for a workflow that can:

- Pull evidence automatically: Order data, tracking, payment results, and customer history shouldn't be gathered by hand every time.

- Build case logic consistently: Each response should follow a strong structure, not depend on who happened to write it that day.

- Submit before the deadline: Late evidence is useless evidence.

- Learn from outcomes: Won and lost disputes should improve future responses and fraud rules.

This same principle applies to customer communication. If your support team needs help replying clearly during fraud reviews or post-dispute conversations, tools like this tool to generate AI replies can speed up draft creation. Just don't let generic replies replace actual evidence.

For merchants who want the full dispute process on autopilot, ChargePay is built for that job. It uses AI to gather evidence, prepare representment, and submit disputes without manual work. ChargePay reports a 92.4% win rate, has handled 200K+ cases, recovered $10.8M+, and offers a pay-per-win model. It also has a 4.9-star rating and a Built for Shopify badge. If you want the deeper workflow, read this guide to automated chargeback and dispute management using AI.

The bigger point is simple. Third party fraud won't disappear. But merchants who connect fraud prevention, evidence collection, and dispute automation stop bleeding revenue on every bad order.

Install ChargePay from the Shopify App Store if you want chargebacks handled without the manual scramble. It's built for Shopify, rated 4.9 stars, and uses a pay-per-win model, so you only pay when money is recovered.

.svg)

.svg)

.svg)

.svg)