Ever wondered who actually makes it possible for you to get paid every time a customer swipes their card or clicks ‘buy now’? That’s your merchant acquirer, the unsung hero working behind the scenes of every single transaction you process.

Think of them as your business's backstage pass to the world of digital payments. They are the essential link that connects your shop—whether online or brick-and-mortar—to the global payment system.

Your Business's Most Important Financial Partner

Without an acquirer, accepting credit or debit cards would be flat-out impossible. They are the ones responsible for giving your business a special merchant account, which is specifically designed to receive funds from card sales.

This isn't the same as your regular business bank account; it's more like a dedicated holding pen for your transaction revenue before it officially hits your books. We break down this distinction further in our guide comparing a merchant account vs a payment gateway.

The Growing Importance of Merchant Acquirers

The role of a merchant acquirer has become even more vital as e-commerce continues to explode. Their job is about much more than just moving money around—they also shoulder a significant amount of financial risk on your behalf.

A merchant acquirer is the financial institution that acts as the intermediary between merchants and card networks like Visa or Mastercard, enabling businesses to accept card payments. The global merchant acquiring market was valued at $28.2 billion and is projected to surge to $31.24 billion. Discover more insights about the merchant acquirer market on Research and Markets.

This growth isn't just a number; it shows how absolutely essential these services are for businesses of all sizes. So, what exactly does an acquirer do for you?

- Sets Up Your Merchant Account: They start by underwriting your business to figure out the risk involved, then provide the special account you need to accept card payments.

- Talks to the Card Networks: When a customer pays, the acquirer routes that transaction information through networks like Visa, Mastercard, or American Express to get it approved.

- Gets Your Money Settled: After a sale is approved, the acquirer collects the cash from the customer’s bank (known as the issuer) and deposits it safely into your merchant account.

To give you a clearer picture of where the acquirer fits in, let's quickly look at all the key players involved in a typical online sale.

The Key Players in a Card Transaction

Getting a handle on your relationship with your acquirer is the first step toward better managing your payments, fees, and overall financial health. They're not just a service provider; they're a core partner in your business's success.

How Money Travels from Customer to Your Bank

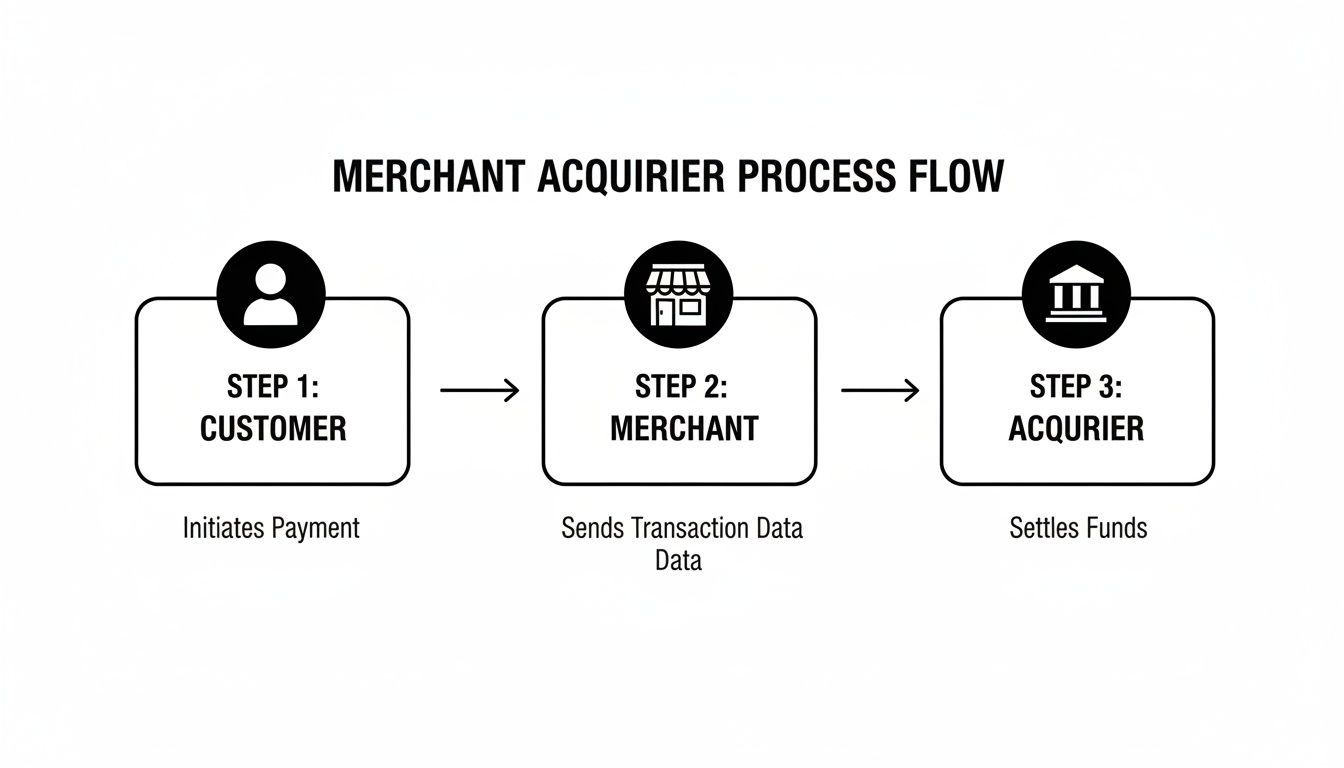

When a customer smacks the "Pay" button on your site, it triggers a lightning-fast chain reaction that feels instantaneous but actually involves a handful of key players. To really get what a merchant acquirer does, you need to understand this journey.

Think of it as a financial relay race. Each runner has a specific job to get the money from your customer’s wallet to your bank account, and the acquirer is right in the thick of it.

As you can see, the acquirer is the central hub. It fields transaction requests from you (the merchant) and makes sure the funds move correctly. The whole trip happens in three main stages: authorization, clearing, and settlement.

The First Leg of the Race: Authorization

The race starts the second your customer enters their payment details. This first step is all about getting a quick "yes" or "no" from their bank.

- The Signal: Your website’s payment gateway securely grabs the customer's card info and shoots it over to the payment processor. The processor acts like a translator, converting this data into a language everyone in the payment chain understands.

- The Request: The processor passes the transaction details to your merchant acquirer. Your acquirer then sends this request through the right card network, like Visa or Mastercard.

- The Verdict: The card network pings the customer's bank (the issuing bank). The issuer checks for sufficient funds and any fraud red flags before sending an approval or decline code all the way back. This entire round trip happens in about two seconds.

The Second Leg of the Race: Clearing

Just because a sale is authorized doesn't mean the cash has moved. That approval is just a promise to pay. The clearing phase is where all the day's approved transactions are bundled up and sorted out.

At the end of each business day, you’ll send a batch of all your authorized sales to your acquirer. The acquirer then organizes these transactions and pushes them through the card networks to the correct issuing banks, telling them exactly how much they owe.

This behind-the-scenes step is critical. It’s the formal accounting process where the acquirer and issuer swap transaction data, confirming the final amounts before any real money changes hands.

Think of it like a restaurant tab. Authorization is when the bartender swipes your card to make sure it works. Clearing is when the restaurant tallies up all the tabs at the end of the night to figure out who owes what.

The Final Lap: Settlement

Settlement is the moment you've been waiting for—when the money finally hits your account. This is where your merchant acquirer truly earns its keep.

After the clearing process, the issuing banks transfer the funds for all approved transactions to your acquirer. The acquirer then takes out all the necessary fees (interchange fees, card network fees, and their own markup) before depositing the final amount into your merchant account. This usually takes one to three business days.

For businesses juggling both in-person and online sales, a smooth flow of funds depends on solid POS software integration for retail and eCommerce.

This entire relay race—from your customer's click to the cash in your account—is managed and guaranteed by your merchant acquirer. They're the ones setting up the accounts, handling the communication, and ultimately, making sure you get paid.

Acquirers, Issuers, Processors, and Gateways Explained

The world of payments can feel like a bowl of alphabet soup. Terms like acquirer, issuer, processor, and gateway get thrown around, and it's easy to get them mixed up. But knowing who does what is absolutely critical to running your business smoothly.

When something goes wrong with a transaction—and eventually, it will—you need to know exactly who to call.

Let's break down these four major players. The best way to think of them is as a specialized team, where each member has a very specific job to get your money from your customer’s wallet into your bank account.

Understanding these roles isn't just trivia; it's practical, need-to-know information. It helps you troubleshoot problems faster, make sense of your monthly statements, and appreciate how the entire system works together to support every single sale you make.

The Acquirer: Your Business’s Bank

We’ve already touched on this, but it’s worth repeating: the merchant acquirer is your business's bank in the payment world. They are the financial institution that gives you a merchant account, which is your license to accept card payments.

- Analogy: The Team Captain. Your acquirer is your direct partner in the payments game. They recruit you (by approving your merchant account), manage the team's finances, and ultimately take responsibility for the final score—getting you paid. They represent your interests to the rest of the payment system.

Their main job is to "acquire" funds from your customer’s bank on your behalf. They're the ones who deposit the money into your account after a transaction is settled. Simple as that.

The Issuer: Your Customer's Bank

On the other side of every transaction is the issuing bank, or issuer. This is your customer’s bank—the one that put their logo on the credit or debit card they just used.

- Analogy: The Customer's Bank Manager. The issuer’s primary loyalty is to the cardholder, not you. Their job is to check if their customer has enough funds or credit to make a purchase and then give a thumbs-up or thumbs-down to the transaction.

When a customer disputes a charge, who do they call? Their issuer. The issuer is the one who kicks off the chargeback process against your business. This makes it vital to understand the difference between an acquirer and an issuer. You can learn more in our detailed comparison of acquirer vs issuer roles.

The Processor: The Data Translator

Next up is the payment processor. Processors are the technical workhorses of the payment ecosystem. They're responsible for securely shuffling transaction data between you, the acquirer, the card networks (like Visa and Mastercard), and the issuer.

- Analogy: The Data Translator. A processor speaks the highly technical, encrypted language of payments. When a customer clicks "buy," the processor takes that raw data, wraps it in layers of security, and translates it into a format that the banks and card networks can understand. They ensure it's a smooth, secure conversation.

Often, an acquirer will have a preferred processor they work with, or they might even handle processing in-house. But they are distinct roles. The processor is all about the secure movement of data.

While an acquirer is a financial institution focused on your account and funds, the processor is the technology company making sure the transaction request gets where it needs to go safely and quickly.

The Gateway: The Secure Messenger

Finally, there’s the payment gateway. If you run an online store, this is your virtual credit card terminal. It’s the secure software on your checkout page that captures your customer’s payment information.

- Analogy: The Secure Messenger. The gateway is like a trusted courier who picks up a highly sensitive package (your customer’s card details) and delivers it securely to the next stop (the processor). Its most important job is to protect that information at the very start of its journey.

The gateway encrypts the card data immediately, protecting you from having to handle sensitive information directly and drastically reducing your PCI compliance burden. It's the secure front door for every online transaction.

Who Does What in Your Payment Chain

To tie this all together, here’s a simple table breaking down the key players and their responsibilities. Think of it as your cheat sheet for the payment processing world.

Knowing these differences is empowering. If you have an issue with funds being deposited into your account, you talk to your acquirer. If customers complain your checkout page is buggy, you check with your gateway provider. And if there’s a massive, system-wide outage? It might just be the processor.

Why Your Acquirer Is So Concerned About Risk and Chargebacks

Your merchant acquirer isn't just another vendor on your expense list—they're a financial partner with real skin in the game. When they give you a merchant account, they’re effectively co-signing on every single transaction you process. This means they are deeply invested in your success, but also in your risk profile.

Think of them like an insurance company. Before an insurer hands you a policy, they assess how likely you are to file a claim. In the same way, an acquirer underwrites your business to get a feel for its financial stability and its potential for expensive problems like fraud and chargebacks.

They are shouldering a significant financial liability for your business. When a transaction goes sideways, the acquirer is often the one left holding the bag until the situation is resolved.

The Financial Stakes of Every Transaction

When a customer files a chargeback, the whole payment process slams into reverse. The customer’s bank (the issuer) immediately yanks the funds back from your merchant acquirer. The acquirer then has to debit that same amount from your merchant account to cover the loss.

But what happens if your account doesn't have enough cash to cover it? This is where the acquirer’s risk becomes painfully real. They have a contractual obligation to pay the issuer back, which means they have to front the disputed amount from their own pocket and then chase you down for the money.

This is the single biggest reason acquirers care so much about how you run your business. Every chargeback isn't just a risk to you; it's a direct financial threat to them. They're essentially giving you a line of credit with every sale.

As e-commerce continues to boom, so do the stakes. Global acquiring revenues have climbed to around $48 billion, mostly because more small businesses are setting up shop online. But this growth has also triggered a spike in e-commerce fraud, piling more pressure onto the acquirers who underwrite all that risk.

This financial exposure is exactly why they watch your account like a hawk for any sign of trouble.

Why Your Chargeback Ratio Is So Important

To keep their risk in check, acquirers focus on one critical metric: your chargeback ratio. It’s a simple calculation—the number of chargebacks you get in a month divided by your total transactions for that same month.

Card networks like Visa and Mastercard have very strict limits for this ratio, usually hovering around 0.9% to 1%. If your business starts creeping over that line, it sends up major red flags for your acquirer.

A high chargeback ratio is a clear signal that something’s not right. It could point to problems with:

- Product or Service Quality: Customers aren’t happy with what they bought.

- Customer Service: Buyers can’t get help from you, so they go straight to their bank.

- Fraudulent Transactions: Your fraud prevention tools aren't catching bad actors.

From the acquirer's point of view, a high ratio makes you a high-risk partner. This can lead to some serious consequences, like higher processing fees, a mandatory hold on your funds (called a reserve), or even losing your merchant account entirely.

Understanding the high costs associated with false positives in financial compliance adds another layer to why acquirers are so cautious. Managing this relationship isn't just about saving one sale; it's about protecting one of your most critical financial partnerships. To learn more, check out our guide on effective chargeback risk management.

Build a Stronger Acquirer Relationship Through Smart Chargeback Management

Now that you've got a handle on how your acquirer sees risk, it's time to flip the script from problem to solution. Keeping a healthy relationship with your merchant acquirer isn't a "set it and forget it" kind of deal. You have to actively show them you're a responsible, low-risk partner.

The single most effective way to do that? Get a firm grip on your chargebacks.

When disputes pile up or are handled poorly, your chargeback ratio starts climbing. That sets off all sorts of alarm bells for your acquirer, straining the partnership and leading to nasty surprises like higher fees or even a suspended account. The goal isn't just to win back money—it's to manage disputes so well that your business stays in the clear.

The Downside of Manual Dispute Management

For a lot of merchants, especially when they're starting out, fighting chargebacks is a manual grind. Someone on the team gets stuck tracking disputes, digging through order histories for evidence, and trying to write convincing responses to send back to the banks.

Not only is this process painfully slow, but it’s also stunningly ineffective. Your team members aren't dispute experts. They often don't know what kind of evidence issuing banks actually care about or how to present it.

The outcome is predictable: low win rates, lost revenue, and a chargeback ratio that just keeps creeping up. From your acquirer's perspective, this looks like you don't have control of your own house, making you a much riskier client to keep on the books.

How AI Automation Changes the Game

This is where smart automation completely rewrites the rules. Instead of burning hours on manual tasks that don't work, you can use technology to fight chargebacks more intelligently and win more often. AI-powered systems plug right into your payment platforms and order management systems to do the heavy lifting for you.

Here’s how it transforms your process:

- Automatic Evidence Gathering: The second a chargeback hits, the system is already at work, pulling all the relevant data—customer info, order details, shipping confirmations, IP addresses, you name it.

- Professional Response Generation: It then takes that evidence and assembles it into a professional, correctly formatted dispute response that’s tailored to the specific chargeback reason code.

- Submission and Tracking: The response gets submitted on time, every time. The system then tracks the outcome, so you always have a clear picture of how you’re doing.

This automated approach isn't just a time-saver; it fundamentally improves your results. By presenting clear, compelling evidence in a format that banks recognize and respect, you can seriously boost your win rates and knock that chargeback ratio back down to a healthy level.

By automating the dispute process, you send a powerful signal to your merchant acquirer: you are proactively managing your risk. This demonstrates that you are a reliable partner, which strengthens your relationship and protects your ability to accept payments without interruption.

This is especially critical for merchants on platforms like Shopify and PayPal. For these users, acquirers often have to work with multiple processors—a setup preferred by 56% of decision-makers. But when chargebacks are managed poorly, those margins get eaten away fast. ChargePay's pay-per-success model automates disputes across these platforms, interfacing smoothly with acquirers to improve issuer relations and recover up to 80% of funds, hands-free. In a world with 5.3 billion e-commerce users, that's a lot of revenue to protect. You can learn more about merchant payment trends.

Building Trust Through Better Metrics

At the end of the day, your relationship with your acquirer is built on trust, and in this world, trust is built on data. When your chargeback win rates go up and your dispute ratio goes down, you’re giving your acquirer the hard data they need to see you as a valuable, low-risk merchant.

This positive feedback loop pays off in the long run. A strong relationship can lead to better processing rates and more favorable terms, all while securing your payment processing for the future. Adopting a smarter approach to disputes is one of the most impactful investments you can make in your business. If you're interested, you might want to check out our guide on other chargeback management solutions.

Got Questions About Merchant Acquirers? We Have Answers.

Let's be honest, the payments world is full of jargon and complex relationships. It’s no surprise that questions come up, especially about the role your merchant acquirer plays. Think of them as your business's most important financial partner—getting clear on how they work is key to making smart decisions and keeping your payment processing smooth.

This section cuts through the noise. We’re tackling the most common questions merchants have about acquirers with straight-to-the-point answers. This will lock in what we’ve already covered and give you the practical knowledge you need.

Can I Choose My Own Merchant Acquirer on Shopify or Stripe?

This is probably one of the biggest points of confusion for e-commerce store owners. The short answer is no. When you sign up for an all-in-one platform like Shopify Payments or Stripe, you’re not just getting a payment button—you’re getting a bundled service.

These platforms are payment service providers (PSPs). They package the merchant account, payment gateway, and acquiring bank relationship into one simple solution. It’s incredibly convenient and lets you get up and running fast because they handle the direct relationship with the acquirer for you.

But convenience doesn't mean you're off the hook. Shopify and Stripe are still on the line for your chargebacks, which is exactly why they watch your account like a hawk. If your chargeback rate creeps up, they won’t think twice about holding your funds or even shutting down your ability to take payments.

The takeaway? Even though you don't pick the acquirer yourself on these platforms, you're still playing by their rules and risk thresholds. Proactive dispute management is just as critical, if not more so.

What Is the Difference Between a Merchant Acquirer and a Merchant Account?

It helps to think of this like your personal banking. The merchant acquirer is the bank, and the merchant account is the bank account they give you.

- The merchant acquirer is the financial institution itself. They’re the ones underwriting your business, assessing your risk profile, and giving you a direct line to the card networks. They are the service provider.

- The merchant account is the special type of account they set up for you. You can’t just funnel credit card payments into your standard business checking account; you need this specific account designed to receive funds from card transactions.

So, the acquirer is the provider, and the merchant account is the product they provide. Your acquirer "acquires" the funds from your customer’s bank and deposits that money into the merchant account they opened for you. You can't have one without the other.

How Do Merchant Acquirers Make Money?

Merchant acquirers are businesses, and they make their money by taking a small slice of every transaction you process. These fees are typically bundled into a single percentage called the Merchant Discount Rate (MDR).

When you get your processing statement, that MDR isn't just one fee. It’s actually made up of three distinct parts:

- Interchange Fee: This is the biggest chunk, and it goes straight to the customer’s issuing bank (like Chase or Bank of America). The card networks set these rates, so they aren't negotiable.

- Assessment Fee: This is a much smaller fee that goes to the card networks (Visa, Mastercard, etc.) for the use of their payment rails.

- Acquirer's Markup: This is the part the acquirer keeps as profit. It’s their payment for providing the service, technology, and, most importantly, taking on the financial risk of your transactions.

On top of the MDR, acquirers might also charge for other things like monthly account maintenance, setup costs, or penalties for issues like excessive chargebacks. Their entire business model revolves around processing a massive volume of transactions while carefully managing the risk that comes with it.

Why Would a Merchant Acquirer Decline My Business Application?

Getting turned down for a merchant account is frustrating, but it almost always boils down to one simple word: risk. Remember, the acquirer is financially on the hook for your chargebacks. If they believe your business is likely to generate more losses than profits, they'll simply say no.

Here are a few of the most common reasons an application gets denied:

- High-Risk Industry: Some business models are just naturally prone to higher rates of fraud and chargebacks. Think industries like online gaming, subscription boxes with free trials, travel, and stores selling adult products.

- Poor Credit History: The acquirer will look at both your personal and business credit. A shaky financial history is a huge red flag that suggests you might not be able to cover potential chargeback losses yourself.

- Previous Processing History: The payments industry talks. If you racked up a high chargeback rate with a previous acquirer, you could end up on the MATCH list (Member Alert to Control High-Risk Merchants), making it very difficult to get approved elsewhere.

- Sloppy Application: If information on your application is missing, inconsistent, or just doesn't add up, an acquirer might deny it simply because they can't properly verify who you are and what you do.

Ultimately, the acquirer is running a calculation: potential profit vs. potential loss. If the risk side of that equation looks too heavy, they’ll pass on the partnership to protect themselves.

The single best way to prove you’re a low-risk, reliable partner to your acquirer is to manage chargebacks effectively. ChargePay uses AI to automate the entire dispute process, helping you recover up to 80% of lost revenue and keep your chargeback ratio safely in the green. Strengthen your acquirer relationship and protect your bottom line by visiting https://www.chargepay.ai.

.svg)

.svg)

.svg)

.svg)